|

市場調査レポート

商品コード

1683147

南米の種子処理市場:市場シェア分析、産業動向、成長予測(2025~2030年)South America Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の種子処理市場:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

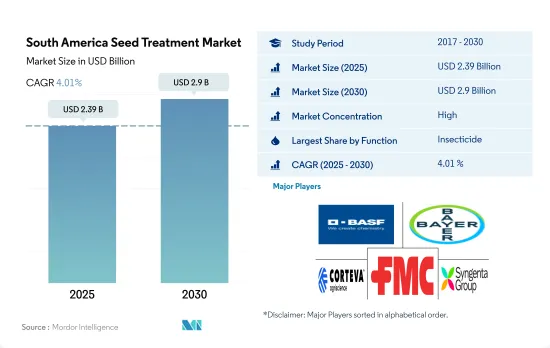

南米の種子処理市場規模は2025年に23億9,000万米ドルと推定・予測され、2030年には29億米ドルに達し、予測期間(2025~2030年)のCAGRは4.01%で成長すると予測されています。

生産性の向上と健康な苗の確立の必要性が市場の成長を後押ししている

- 南米の種子処理産業は著しい成長を遂げています。市場額は2017年と比較して2022年には51.7%増加しました。この成長の原動力となったのは、健全な苗の保護と定着における種子施用技術の利点に対する認識の高まりと、全体的な生産性向上の必要性です。

- ブラジルとアルゼンチンは、さまざまな真菌病から作物を保護するために種子処理を多用している著名な農業国です。ブラジルとアルゼンチンの種子処理剤の合計市場シェアは大きく、地域市場の77.9%をブラジルが、約3.1%をアルゼンチンが占めています。

- 殺虫剤種子処理が主要なシェアを占めており、その市場額は2023~2029年にかけて35.3%の大幅な増加が見込まれています。

- 南米における殺菌剤種子処理は、大豆、トウモロコシ、小麦、果物などの主要作物に影響を及ぼす真菌病が蔓延しているため、近年重要性を増しています。大豆さび病、うどんこ病、フザリウム頭枯病を含むこれらの病害は、作物の収量と品質に重大なリスクをもたらします。その結果、南米の農業従事者は、作物を保護し収量損失を減らすために、殺菌剤種子処理への依存度を高めています。これらの要因により、殺菌剤セグメントの市場規模は予測期間中に33.6%増加すると予想されます。

- 作物の保護と収量を向上させるために種子処理が受け入れられつつあることと、その利点に関する農業従事者の意識の高まりが、予測期間における市場の成長を促進すると予想されます。

生育初期の病害虫から種子や苗を保護する必要性により、種子処理の採用率が高まる

- 南米における種子処理市場は、作物の初期病害虫から種子や苗を保護する必要性に対する農業従事者の意識の高まりによって、大きな成長を遂げています。この地域の主要作物である大豆、トウモロコシ、小麦、果物、野菜は、種子処理アプリケーションを受け入れています。注目すべきことに、種子処理市場は2017~2022年までの歴史的期間に51.7%という目覚ましい成長を示しました。

- 2022年には、ブラジルが南米最大の市場として圧倒的な地位を占め、同地域の市場シェアの77.9%を占めました。同国の目覚ましい拡大は、食糧安全保障に対するニーズの高まりや、大豆などの主要作物における種子処理製品の利用拡大など、いくつかの要因に起因しています。

- 南米の種子処理産業第2位の市場であるアルゼンチンは、干ばつや高温といった厳しい環境条件に見舞われています。これらの要因が、農業従事者が作物の生育初期に種子処理技術を採用する原動力となりました。種子処理法を採用することで、農業従事者はより早い発芽を促し、土壌伝染性病害を効果的に防除することができます。このアプローチは、同国の厳しい気候による悪影響を緩和する上で極めて重要であり、農業従事者は作物の収量を高め、農業生産性を持続的に維持することができます。

- 南米の種子処理市場は、予測期間中にCAGR 4.3%を記録すると予測されます。この成長は、農作物を保護し、収量を向上させ、病害虫によってもたらされる作物の初期成長の課題に対処する上で、種子処理剤が提供する計り知れない価値について、農業従事者の間で認識が高まっていることに起因しています。

南米の種子処理市場動向

耐病性耕運機のような代替アプローチにより、同地域のヘクタール当たりの種子処理消費量が減少

- 過去の期間において、1ヘクタール当たりの種子処理剤の消費量は顕著に減少しており、2017年のデータと比較すると、2022年には1ヘクタール当たり1,000gの大幅な減少が認められました。この減少は主に様々な要因に起因しており、種子処理剤使用量の減少に寄与している極めて重要な理由の1つは除草剤耐性耕運機の採用が増加していることです。これらの耕運機は除草剤の散布に耐えるように遺伝子操作されており、農業従事者は追加の種子処理を必要とせずに雑草を防除することができます。その結果、従来の種子処理剤の需要は減少しています。ブラジル、アルゼンチン、パラグアイなどの主要農業国は、大豆、小麦、トウモロコシなどの主要作物にこれらの除草剤耐性耕種子を採用しています。

- 除草剤耐性に加えて、遺伝子組み換え作物の栽培が広まったことも、種子処理剤の消費に大きな影響を与えています。遺伝子組み換え作物は、さまざまな病害虫に対する抵抗性を持つ形質が組み込まれるように操作されているため、これらの作物には種子処理が不要になるものもあります。その結果、遺伝子組み換え作物を栽培する農業従事者は、従来の種子処理剤への依存度を減らしています。

- ヘクタール当たりの種子処理剤消費量の減少に寄与しているもうひとつの重要な要因は、耐病性耕運機の採用です。これらの栽培品種は、一般的な植物病害に抵抗するように品種改良または遺伝子操作されているため、病害に特化した種子処理剤の必要性が減少しています。より多くの農業従事者が耐病性耕運機を採用するにつれて、ヘクタール当たりのある種の種子処理剤使用量に対する全体的な需要は大幅に減少しています。

アゾキシストロビンの浸透移行性により、処理した植物に吸収され、長期間の防除効果が得られます。

- シペルメトリン、メタラキシル、マラチオン、アバメクチン、アゾキシストロビンは、南米で一般的に使用されている種子処理剤の有効成分です。種子処理は、種子や苗を病害虫から早期に保護します。土壌に播種すると同時に、種子の周囲に保護バリアを作り、潜在的な脅威から保護します。

- シペルメトリンは接触殺虫剤として、主に処理された種子や植物の表面に残り、保護バリアを形成することで、幅広い害虫に対して迅速なノックダウン効果を発揮します。2022年の価格はトン当たり2万1,100米ドルでした。シペルメトリンの作用機序は昆虫の神経系を混乱させ、麻痺を引き起こし、最終的には死に至らしめる。

- マラチオンの全身作用により、アブラムシ、オオヨコバイ、アザミウマ、ウロコバチ、特定のイモムシなど多様な害虫を効果的に駆除でき、2022年の価格は1トン当たり12万4,000米ドルでした。マラチオンの作用機序には、昆虫の適切な神経機能に不可欠な酵素であるアセチルコリンエステラーゼの阻害が含まれます。

- 2022年の価格が1トン当たり4,400米ドルのMetalaxylは、Pythium、Phytophthora、特定のべと病などの土壌伝染性病原体から種子や苗を早期に保護します。Metalaxylは、真菌細胞のRNA形成を阻害することで効果を発揮します。この阻害により、必須タンパク質の合成が妨げられ、真菌の成長と繁殖が阻害されます。

- 2022年の価格は1トン当たり4,500米ドルで、アゾキシストロビンの全身活性により処理した植物に吸収され、真菌細胞のミトコンドリア呼吸を阻害することで、新芽や葉を含むさまざまな植物部位に長期にわたる保護を記載しています。

南米種子処理産業概要

南米の種子処理市場はかなり統合されており、上位5社で65.66%を占めています。この市場の主要企業は、BASF SE、Bayer AG、Corteva Agriscience、FMC Corporation、Syngenta Groupです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- アルゼンチン

- ブラジル

- チリ

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 機能

- 殺菌剤

- 殺虫剤

- 殺線虫剤

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- アルゼンチン

- ブラジル

- チリ

- その他の南米

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル(世界レベル概要、市場レベル概要、主要な事業セグメント、財務、従業員数、主要情報、市場ランク、市場シェア、製品・サービス、最近の動向分析を含む)

- BASF SE

- Bayer AG

- Corteva Agriscience

- FMC Corporation

- Sumitomo Chemical Co. Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 53759

The South America Seed Treatment Market size is estimated at 2.39 billion USD in 2025, and is expected to reach 2.9 billion USD by 2030, growing at a CAGR of 4.01% during the forecast period (2025-2030).

The need to improve productivity and establish healthy seedlings is fueling the growth of the market

- The South American seed treatment industry is experiencing significant growth. The market value increased by 51.7% in 2022 compared to 2017. This growth was driven by growing awareness of the benefits of seed-applied technologies in protecting and establishing healthy seedlings and the need to improve overall productivity.

- Brazil and Argentina are prominent agricultural nations that heavily utilize seed treatments to protect their crops from a range of fungal diseases. The combined market share of seed treatments in Brazil and Argentina is significant, with Brazil accounting for 77.9% and Argentina accounting for around 3.1% of the regional market.

- The insecticide seed treatments held the major share, and their market value is expected to increase significantly by 35.3% between 2023 and 2029 because of the growing recognition of the effectiveness of seed treatments in combatting insect vectors and safeguarding crop productivity.

- Fungicide seed treatment in South America has gained significant importance in recent years due to the prevalence of fungal diseases that affect key crops like soybeans, corn, wheat, and fruits. These diseases, including soybean rust, powdery mildew, and Fusarium head blight, pose a significant risk to crop yields and quality. Consequently, farmers in South America are increasingly relying on fungicide seed treatments to safeguard their crops and reduce yield losses. These factors are expected to increase the market value of the fungicide segment by 33.6% during the forecast period.

- The growing acceptance of seed treatment to enhance crop protection and yield, coupled with the increasing awareness among farmers regarding its advantages, is anticipated to drive the market's growth in the forecast period.

The need to protect seeds and seedlings from early-growth pests and diseases will increase the adoption rate of seed treatment

- The seed treatment market in South America is experiencing significant growth, driven by the increasing awareness among farmers regarding the need to protect seeds and seedlings from early crop diseases and insect pests. The region's major crops, including soybean, maize, wheat, fruits, and vegetables, have embraced seed treatment applications. Notably, the market for seed treatment exhibited impressive growth of 51.7% over the historical period spanning from 2017 to 2022.

- In 2022, Brazil held the dominant position as the largest market in South America, representing 77.9% of the region's market share. The country's remarkable expansion can be attributed to several factors, including the growing need for food security and the escalating utilization of seed treatment products in key crops like soybeans.

- Argentina, the second-largest market in the South American seed treatment industry, experiences challenging environmental conditions such as drought and hot temperatures. These factors drove farmers to adopt seed treatment techniques during the early stages of crop growth. By employing seed treatment methods, farmers can promote faster germination and effectively control soil-borne diseases. This approach proves crucial in mitigating the adverse effects of the country's harsh climate, enabling farmers to enhance crop yields and sustainably maintain agricultural productivity.

- The South American seed treatment market is projected to register a CAGR of 4.3% during the forecast period. This growth can be attributed to the increasing recognition among farmers regarding the immense value offered by seed treatments in safeguarding their crops, enhancing yields, and countering early crop growth challenges posed by infestations.

South America Seed Treatment Market Trends

Alternative approaches like disease-resistant cultivators reduce the seed treatment consumption per hectare in the region

- Over the historical period, there was a remarkable decrease in the consumption of seed treatments per hectare, with a significant reduction of 1,000 g per ha noted in 2022 when compared to the data from 2017. This decline was primarily attributed to various factors, including one of the pivotal reasons contributing to the decline in seed treatment usage is the increasing adoption of herbicide-resistant cultivators. These cultivators are genetically engineered to withstand the application of herbicides, allowing farmers to control weeds without the need for additional seed treatments. As a result, the demand for conventional seed treatments has reduced. Major agricultural countries like Brazil, Argentina, and Paraguay adopt these herbicide resistance cultivators in their major crops like soybeans, wheat, and maize.

- In addition to herbicide resistance, the widespread cultivation of genetically modified crops has significantly impacted seed treatment consumption. Genetically modified crops are engineered to possess built-in traits that offer resistance to various pests and diseases, rendering some seed treatments unnecessary for these crops. Consequently, farmers planting genetically modified crops have reduced their reliance on traditional seed treatments.

- Another crucial factor contributing to the decline in seed treatment consumption per hectare is the adoption of disease-resistant cultivators. These cultivators have been bred or engineered to resist common plant diseases, thereby reducing the need for disease-specific seed treatments. As more farmers adopt disease-resistant cultivators, the overall demand for certain types of seed treatment usage per hectare has decreased significantly.

Azoxystrobin's systemic activity allows it to be absorbed by treated plants, providing extended protection

- Cypermethrin, metalaxyl, malathion, abamectin, and azoxystrobin are commonly used active ingredients in seed treatment chemicals in South America. Seed treatment provides early protection to seeds and seedlings against pests and diseases. It creates a protective barrier around the seed, shielding it from potential threats as soon as it is sown in the soil.

- Cypermethrin, as a contact insecticide, remained primarily on the surface of treated seeds or plants, forming a protective barrier for quick knockdown action against a wide range of insect pests. It was priced at USD 21.1 thousand per metric ton in 2022. The mode of action of cypermethrin involves disrupting the nervous systems of insects, leading to paralysis and, ultimately, their death.

- Malathion's systemic action enabled effective control of diverse insect pests, including aphids, leafhoppers, thrips, scales, and certain caterpillar species, with a price of USD 124 thousand per metric ton in 2022. Malathion's mode of action involves inhibiting acetylcholinesterase, an enzyme essential for proper nerve function in insects.

- Metalaxyl, priced at USD 4.4 thousand per metric ton in 2022, provided early protection to seeds and seedlings from soil-borne pathogens such as Pythium, Phytophthora, and certain downy mildews. Metalaxyl works by inhibiting the formation of RNA in fungal cells. This disruption prevents the synthesis of essential proteins, leading to the inhibition of fungal growth and reproduction

- With a price of USD 4.5 thousand per metric ton in 2022, azoxystrobin's systemic activity allowed it to be absorbed by treated plants, providing extended protection to different plant parts, including new growth and foliage, by inhibiting the mitochondrial respiration in fungal cells.

South America Seed Treatment Industry Overview

The South America Seed Treatment Market is fairly consolidated, with the top five companies occupying 65.66%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, FMC Corporation and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Argentina

- 4.3.2 Brazil

- 4.3.3 Chile

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Insecticide

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 FMC Corporation

- 6.4.5 Sumitomo Chemical Co. Ltd

- 6.4.6 Syngenta Group

- 6.4.7 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms