インドの種子処理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

India Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 164 Pages

- 納期

- 2~3営業日

- 商品コード

- 1686644

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

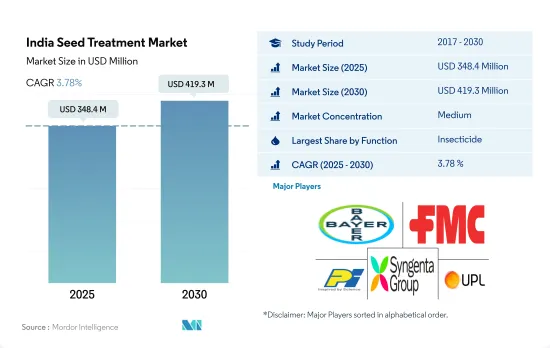

インドの種子処理市場規模は2025年に3億4,840万米ドルと推定され、2030年には4億1,930万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは3.78%で成長すると予測されます。

高度な種子技術へのニーズの高まりと政府の支援が市場を牽引

- インドの化学殺菌剤の種子処理市場は、作物保護における種子処理の重要性に対する意識の高まりにより、過去の期間に大きな成長を遂げました。種子処理は、種子を菌類病害から守り、発芽率を向上させ、健全な植物樹立を確保する上で極めて重要です。

- 殺菌剤は種子処理薬品の中で2番目に重要であり、2022年には9.0%のシェアを占めています。これは、植物の種子や苗の段階が土壌や種子を媒介とする病害に対してより脆弱であるためです。

- 種子処理市場における殺虫剤セグメントは、2022年に2億8,060万米ドルと評価されました。化学殺虫剤による種子処理では、イミダクロプリド、クロチアニジン、チアメトキサム、フィプロニル、クロルピリホスといった有効成分の重要性が高いです。

- 国内の農家も、高品質と播種後の最大限の発芽率を確保するため、これらの化学薬品で前処理された種子の購入を検討しています。中央政府やいくつかの州政府は、農民に種子処理の使用を認識させ、近代的農業慣行への意欲を高めるための取り組みを行っています。例えば、マディヤ・プラデシュ州政府は、1,000の村で知識の乏しい農民を訓練し、大豆などの作物の栽培を促進するため、スパイラル・グレーダーと種子処理ドラム・プログラムを開始しました。

- 根こぶ線虫は、果物や野菜作物に影響を与える線虫の中でも最も危険な種類で、ニンジンで34.0%、ジャガイモで26.0%、トマトで23.0%、戦場ヶ原で22.0%、ブリンジャルで21.0%の収量損失を引き起こすことが知られています。殺線虫剤種子処理は果菜類で最も一般的であり、2022年のシェアは9.1%でした。

インドの種子処理市場動向

病気や害虫の早期防除に対する意識の高まりと導入が種子処理の消費を増加させている

- 過去一定期間、種子処理農薬の1ヘクタール当たりの消費量は安定しています。2022年に記録された消費量は1ヘクタール当たり125.46グラムでした。この安定性は、種子処理技術の進歩、病害虫管理方法の改善、既存の農薬製剤の有効性など、さまざまな要因によるものです。

- 種子処理は、種子や土壌を媒介とする病虫害の有害な影響から種子や苗を守る上で重要な役割を果たしています。種子処理剤は、サトウキビ(根腐れ病、萎凋病)、落花生(茎腐敗病、種子腐敗病、苗腐敗病、白紋羽病)、稲(根こぶ線虫、根こぶ病)といった重要作物の害虫や病害を駆除します。

- 作物の出芽と生育は、種子処理法を用いることで、これらの有害要因から効果的に遮断することができます。種子処理製品には大きな利点があるため、農業分野での利用が不可欠となっています。

- 種子需要の約70%は、農家が自家採種した種子を利用することで満たされています。しかし、これらの種子は種子病害や土壌病害に弱いです。そのため、病気や害虫の発生から作物を守るためには、種子処理を実施することが極めて重要です。この必要性から、種子処理製品の利用が増加しています。

- 拡大する農業活動には、種子処理を含む効果的な作物保護対策が必要です。初期段階の病害虫から作物を守る種子処理の利点に対する農民の意識の高まりが、種子処理製品の普及と1ヘクタール当たりの散布率の増加に寄与しています。

種子の市場性を高めるための種子処理剤の使用に関する政府機関の促進活動

- 種子処理は、作物の出穂や生育に影響を及ぼす種子や土壌を媒介する病害虫から種子や苗を守る上で重要な役割を果たしています。種子を媒介とする病虫害は、農家が直面する作物収量を減少させるいくつかの大きな課題です。シペルメトリン、アバメクチン、アゾキシストロビン、マラチオン、メタラキシルは、インドで最も一般的に使用されている種子処理剤です。

- シペルメトリンは非全身土壌作用型のピレスロイド系殺虫剤で、インドでは秋蒔きまたは冬蒔きの小麦や大麦の球根虫や針金虫の被害を軽減するための種子処理剤です。2022年の価格はトン当たり2万1,000米ドルでした。

- アバメクチンはイベルメクチン系に属し、線虫に対して高い固有活性を持っています。トウモロコシ、大豆、綿花の生産において、根を攻撃する線虫から幼植物を守るために使用されます。2022年の価格はトン当たり8,700米ドル。

- アゾキシストロビンは広域スペクトラムの予防的種子処理殺菌剤で、農作物の収量低下を引き起こす子実体菌類、真菌類、子のう菌類、担子菌類の防除に推奨されます。2022年のアゾキシストロビンの価格は1トン当たり4,500米ドルでした。

- さまざまな規制や政府機関が、種子の市場性を高めるために種子処理の使用を奨励しています。例えば、インド政府は、カリフシーズン中にすべての重要作物で種子処理を100%確実に行うための全国キャンペーンを開始する計画を発表しました。農薬業界団体、ATMA、CIPMCs、KVK、農民クラブ、SAU、NGOなどは、種子処理100%キャンペーンにおいて重要な役割を果たすことができます。このことは、国内の種子処理剤の価格にさらに影響を与えると予想されます。

インドの種子処理産業の概要

インドの種子処理市場は適度に統合されており、上位5社で56.48%を占めています。この市場の主要企業は以下の通りです。 Bayer AG, FMC Corporation, PI Industries, Syngenta Group and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- インド

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 機能

- 殺菌剤

- 殺虫剤

- 殺線虫剤

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- Crystal Crop Protection Ltd

- FMC Corporation

- PI Industries

- Rallis India Ltd

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 53540

The India Seed Treatment Market size is estimated at 348.4 million USD in 2025, and is expected to reach 419.3 million USD by 2030, growing at a CAGR of 3.78% during the forecast period (2025-2030).

The market is driven by the growing need for advanced seed technologies and government support

- The Indian seed treatment market for chemical fungicides has experienced significant growth during the historical period due to the rising awareness about the importance of seed treatment in crop protection. Seed treatment is crucial in safeguarding seeds from fungal diseases, improving germination rates, and ensuring healthy plant establishment.

- Fungicides are the second most important among seed treatment chemicals, and they accounted for a share of 9.0% in 2022. This is because the seeds and seedling stages of plants are more vulnerable to soil and seed-borne diseases.

- The insecticide segment in the seed treatment market was valued at USD 280.6 million in 2022. Active ingredients such as imidacloprid, clothianidin, thiamethoxam, fipronil, and chlorpyrifos are of high importance in chemical insecticide seed treatment.

- Farmers in the country are also looking to buy seeds that are pre-treated with these chemicals to ensure high quality and a maximum percentage of germination after sowing. The central government and several state governments are taking initiatives to make farmers aware of the use of seed treatment and enhance their motivation toward modern agricultural practices. For instance, the Government of Madhya Pradesh launched a spiral grader and seed treatment drum program to train the less-knowledgeable farmers in 1,000 villages and boost the cultivation of crops like soybeans.

- Root-knot nematode is the most dangerous among the nematode species that affect fruits and vegetable crops and is known to cause a yield loss of 34.0% in carrots, 26.0% in potatoes, 23.0% in tomatoes, 22.0% in the battleground, and 21.0% in brinjal. Nematicide seed treatment is most common in fruits and vegetable crops, and it accounted for a share of 9.1% in 2022.

India Seed Treatment Market Trends

Growing awareness and adoption of early control of diseases and pests are raising the seed treatment consumption

- Over the historical period, the per-hectare consumption of seed treatment pesticides has remained consistent. In 2022, the recorded consumption stood at 125.46 grams per hectare. This stability can be attributed to various factors, such as advancements in seed treatment technologies, improved disease and pest management practices, and the efficacy of existing pesticide formulations.

- Seed treatment plays a crucial role in protecting seeds and seedlings against the harmful impact of seed and soil-borne diseases and insect pests. Seed treatment products control pests and diseases in significant crops such as sugarcane (root rot and wilt), groundnut (stem rot, seed rot, seedling rot, and white grubs), and rice (root-knot nematode and root rot disease).

- Crop emergence and growth can be effectively shielded from these detrimental factors by employing seed treatment methods. The significant advantages associated with seed treatment products are driving their indispensable utilization in the agriculture sector.

- Approximately 70% of seed requirements are fulfilled by farmers utilizing their own seed stock. However, these seeds are more vulnerable to seed and soil-borne diseases. Thus, it is crucial to implement seed treatment to safeguard crops from the emergence of diseases and pests. This necessity consequently increased the utilization of seed treatment products.

- Expanding agricultural activities necessitate effective crop protection measures, including seed treatment. Farmers' heightened awareness of the benefits of seed treatment in protecting crops from early-stage diseases and pests has contributed to the increased adoption of these products and their application rates per hectare.

Promotional activities of government agencies to use seed treatments to increase the marketability of seeds

- Seed treatment plays an important role in protecting seeds and seedlings from seed and soil-borne diseases and insect pests affecting crop emergence and growth. Seed-borne diseases and pests are a few major challenges farmers face that decrease crop yield. Cypermethrin, abamectin, azoxystrobin, malathion, and metalaxyl are the most commonly used seed treatment chemicals in India.

- Cypermethrin is a non-systemic soil-acting pyrethroid insecticide seed treatment for reducing wheat bulb fly and wireworm damage to autumn or winter-sown wheat and barley in India. It was valued at a price of USD 21.0 thousand per metric ton in 2022.

- Abamectin belongs to the ivermectin chemical class and has high intrinsic activity against nematodes. It is used to protect young plants from root-attacking nematodes in the production of corn, soybeans, and cotton. It was priced at USD 8.7 thousand per metric ton in 2022.

- Azoxystrobin is a broad-spectrum, preventative seed treatment fungicide with systemic properties recommended for the control of Deuteromycetes, Oomycetes, Ascomycetes, and Basidiomycetes fungi that cause yield losses in crops. In 2022, azoxystrobin was priced at USD 4.5 thousand per metric ton.

- Various regulations and government agencies are encouraging the use of seed treatments to increase the marketability of seeds. For instance, the Government of India announced plans to launch a countrywide campaign for ensuring 100% seed treatment in all important crops during the kharif season. Pesticide industry associations, ATMAs, CIPMCs, KVKs, farmers clubs, SAUs, NGOs, etc., can play an important role in the campaign for 100% seed treatment. This is expected to further affect the price of seed treatment chemicals in the country.

India Seed Treatment Industry Overview

The India Seed Treatment Market is moderately consolidated, with the top five companies occupying 56.48%. The major players in this market are Bayer AG, FMC Corporation, PI Industries, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Insecticide

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Crystal Crop Protection Ltd

- 6.4.6 FMC Corporation

- 6.4.7 PI Industries

- 6.4.8 Rallis India Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

インドの種子処理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 164 Pages

- 納期

- 2~3営業日