|

市場調査レポート

商品コード

1686297

アジア太平洋地域の種子処理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia Pacific Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の種子処理:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 213 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

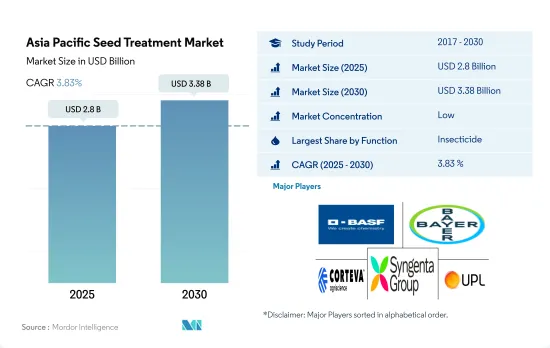

アジア太平洋地域の種子処理市場規模は2025年に28億米ドルと推計され、2030年には33億8,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは3.83%で成長する見込みです。

種子は土壌伝染性昆虫の影響を受けやすいため、殺虫剤がアジア太平洋地域の種子処理市場を独占

- アジア太平洋地域では、種子を保護し作物の成績を高めるために、種子処理が重要な慣行となっています。これらの処理は、種子を媒介する病気、害虫、線虫を駆除し、健康な苗を確保し、作物の定着を改善するのに役立ちます。

- 種子処理剤の市場価値は、歴史的期間に29.2%の成長を経験しました。このような上昇傾向は、苗の保護と成長、生産性の向上のために種子処理が提供する利点に対する認識が高まっていることに起因しています。

- 中国とインドは、アジア太平洋地域市場で種子処理剤の大きなシェアを占める主要な農業国です。中国はこの地域の市場額の約16.8%を占め、インドは2022年に約12.4%の市場シェアを占めました。

- 殺虫剤種子処理が市場を独占し、2022年にはアジア太平洋地域の種子処理市場の77.6%を占める。昆虫は種子や苗に深刻な被害を与える可能性があり、その結果、苗立ちが悪くなったり、発芽が制限されたり、収量が低下したりします。殺虫剤種子処理は、これらの害虫による被害を防ぎ、より健康で活力のある苗をもたらします。

- 殺菌剤を種子に散布すると、保護バリアが形成され、立枯病、苗立枯病、根腐病などの病害の予防と防除に役立ちます。殺菌剤種子処理は、2022年のアジア太平洋地域殺菌剤市場で21.2%という大きなシェアを占めています。

- 同市場は予測期間中(2023~2029年)にCAGR 4.0%を記録して成長すると予想されます。この成長は主に、人口増加のニーズを満たすための食糧生産需要の高まりによってもたらされると予測されます。作物の収量を最適化し、病気や害虫による損失を最小限に抑えるため、農家は種子処理剤を採用するようになっています。

生育初期の病害虫から種子や苗を保護する必要があるため、種子処理剤の採用率が高まる可能性があります。

- アジア太平洋地域の種子処理市場は、作物の初期病害虫から種子や苗を保護する必要性に対する農家の意識の高まりにより、著しい成長を遂げています。米、小麦、マンゴー、ブドウ、バナナ、綿花など、この地域の主要作物の農家は、種子処理アプリケーションを採用しています。

- 2022年には、中国がアジア太平洋地域の主要市場に浮上し、市場の16.7%という大きなシェアを占めました。この優位性は、同国の目覚しい成長を後押しした様々な要因の組み合わせに起因しています。これらの要因には、食糧安全保障の必要性の高まりや、コメや小麦などの作物における種子処理製品の採用の拡大が含まれます。

- アジア太平洋地域の種子処理市場を独占しているのは、穀物・穀類分野です。2022年には、このセグメントは市場総額の50.3%を占める。この優位性は、穀物・穀類がこの地域の主食作物であり、農地のかなりの部分が穀物・穀類の栽培に充てられているためと考えられます。その経済的重要性と様々な病害虫に対する高い感受性から、種子処理は成長の初期段階において穀物や穀類を保護する上で重要な役割を果たしています。

- アジア太平洋地域では、食糧需要の増加により作付面積が増加しています。農家は、同じ土地で作付けを繰り返したり、年間の作付け回数を増やしたりすることが多いです。このような集約化により、種子を媒介とする様々な病気や昆虫の発生リスクが高くなり、その結果、種子処理の使用量が増加しています。アジア太平洋地域の種子処理市場は、予測期間中(2023年~2029年)に大きく成長し、CAGRは4.0%を記録すると予測されています。

アジア太平洋地域の種子処理市場動向

種子や苗を保護する意識の高まりが種子処理農薬の消費を促進

- アジア太平洋地域の種子処理剤の平均消費量は、2022年には1ヘクタール当たり261.08グラムとなりました。種子処理は、作物の生産性を保護し向上させる効果と効率により、近年ますます普及しています。

- アジア太平洋地域諸国の農業慣行が激化し、より高い生産性へのニーズが高まる中、アジア太平洋地域の農家は、作物を病気や害虫、その他のストレスから保護する効果的な手段として作物保護の重要性を認識するようになり、それによって収量減少のリスクを減らしています。

- 種子処理は、種子の腐敗、苗立枯病、立枯病、根腐病、うどんこ病、べと病、初期疫病などの葉面病害など、いくつかの真菌性病害を予防し、作物を保護することができます。有効成分の使用は、対象病害と種子処理要件に基づいているため役立ちます。メタラキシル、カルベンダジム、キャプタンが、アジア太平洋地域市場で種子処理製品に最も使用されている有効成分です。

- 種子処理は、害虫や線虫に対しても使用されています。例えば、根こぶ線虫は、果物や野菜作物に影響を与える線虫の中で最も危険な種であり、ニンジンで34%、ジャガイモで26%、トマトで23%、ビンロウリで22%、ブリンジャルで21%の収量損失を引き起こすことが知られているが、種子処理によって効果的に軽減することができます。

- アジア太平洋地域諸国の種子処理業界では、より正確で効率的な種子処理施用を可能にする技術の進歩が見られます。これらの進歩には、改良された種子処理製剤や高度な種子処理装置が含まれ、この地域の農家による種子処理剤の使用量の増加につながっています。

アジア太平洋地域の様々な政府機関による促進活動の増加が需要と価格を牽引

- 種子処理は、種子や土壌を媒介とする病害や、作物の出芽や成長に影響を与える害虫から種子や苗を守る上で重要な役割を果たしています。シペルメトリン、アバメクチン、アゾキシストロビン、マラチオン、メタラキシルは、アジア太平洋地域で最も一般的に使用されている種子処理薬品です。

- シペルメトリンは非全身土壌作用型のピレスロイド系殺虫剤です。秋冬播種の小麦や大麦の球根虫や針金虫の被害を軽減するため、種子処理に使用されます。2022年の価格はトン当たり2万1,000米ドル。

- アバメクチンはイベルメクチン系に属し、線虫に対して高い固有活性を持っています。トウモロコシ、大豆、綿花の生産において、根を攻撃する線虫から幼植物を守るために使用されます。2022年の価格はトン当たり8,700米ドルでした。

- アゾキシストロビンは、農作物の収量低下を引き起こす子実体菌類、真菌類、子のう菌類、担子菌類の防除に推奨される、浸透性特性を持つ広域予防種子処理殺菌剤です。2022年、アゾキシストロビンの価格はトン当たり4,500米ドルでした。

- 政府機関によるさまざまな規制は、種子の市場性を高めるために種子処理の使用を奨励しています。インド政府は、カリフシーズン中にすべての重要作物で種子処理を100%確実に行うためのキャンペーンを全国的に展開することを決定しました。農薬業界団体、ATMA、CIPMCs、KVK、農民クラブ、SAU、NGOなどは、100%種子処理を推進するキャンペーンにおいて重要な役割を果たすことができます。このような取り組みは、今後数年間、同地域の種子処理剤価格にさらに影響を与える可能性があります。

アジア太平洋地域の種子処理産業の概要

アジア太平洋地域の種子処理市場は断片化されており、上位5社で33.38%を占めています。この市場の主要企業は以下の通りです。 BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 1ヘクタール当たりの農薬消費量

- 有効成分の価格分析

- 規制の枠組み

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 機能

- 殺菌剤

- 殺虫剤

- 殺線虫剤

- 作物タイプ

- 商業作物

- 果物・野菜

- 穀物

- 豆類・油糧種子

- 芝・観賞用

- 生産国

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- Crystal Crop Protection Ltd

- FMC Corporation

- Nufarm Ltd

- PI Industries

- Syngenta Group

- UPL Limited

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 51830

The Asia Pacific Seed Treatment Market size is estimated at 2.8 billion USD in 2025, and is expected to reach 3.38 billion USD by 2030, growing at a CAGR of 3.83% during the forecast period (2025-2030).

Insecticides dominated the Asia-Pacific seed treatment market as seeds are more susceptible to soil-borne insects

- Seed treatment is an important practice in Asia-Pacific to protect seeds and enhance crop performance. These treatments help control seed-borne diseases, pests, and nematodes, ensuring healthy seedlings and improved crop establishment.

- The market value of seed treatment experienced a growth of 29.2% during the historical period. This upward trend can be attributed to the increasing recognition of the advantages offered by seed treatment for protecting and enhancing the growth of seedlings and their productivity.

- China and India are the leading agricultural nations that hold a significant share of seed treatments in the Asia-Pacific market. China constituted approximately 16..8% of the regional market value, while India held around 12.4% market share in 2022.

- Insecticide seed treatment dominated the market, accounting for 77.6% of the Asia-Pacific seed treatment market in 2022. Insects can severely damage seeds and seedlings, which can result in poor stand establishment, limited germination, and yield losses. Insecticide seed treatments prevent the damage posed by these pests, resulting in seedlings that are healthier and more vigorous.

- Fungicides applied to seeds form a protective barrier that aids in the prevention and control of diseases such as damping off, seedling blight, and root rot. Fungicide seed treatment held a significant share of 21.2% in the Asia-Pacific fungicide market in 2022.

- The market is expected to grow during the forecast period (2023-2029), registering a CAGR of 4.0%. This growth is primarily anticipated to be driven by the rising demand for food production to meet the needs of a growing population. In order to optimize crop yields and minimize losses due to diseases and insects, farmers are increasingly adopting seed treatments.

The need to protect seeds and seedlings from early-growth pests and diseases may increase the seed treatment adoption rate

- The seed treatment market in Asia-Pacific is experiencing significant growth, driven by farmers' increasing awareness of the need to protect seeds and seedlings from early crop diseases and insect pests. Farmers of the region's major crops, including rice, wheat, mangoes, grapes, bananas, and cotton, are adopting seed treatment applications.

- In 2022, China emerged as the leading market within Asia-Pacific, accounting for a substantial share of 16.7% of the market. This dominance can be attributed to a combination of factors that fueled the country's impressive growth. These factors include the increasing imperative for ensuring food security and the escalating adoption of seed treatment products in crops such as rice and wheat.

- The grains & cereals segment dominates the Asia-Pacific seed treatment market. In 2022, the segment accounted for 50.3% of the market's total value. This dominance can be because they are staple crops in the region, and a significant portion of agricultural land is dedicated to their cultivation. Due to their economic importance and high susceptibility to various pests and diseases, seed treatment plays a vital role in protecting grains and cereals during the early stages of growth.

- Crop intensity has been rising in Asia-Pacific as a result of increased food demand. Farmers often practice repeated cropping or intensify the number of crop cycles per year on the same land. This intensification leads to a higher risk of various seed-borne diseases and insect outbreaks, resulting in an increase in seed treatment usage. The Asia-Pacific seed treatment market is projected to witness significant growth during the forecast period (2023-2029) and register a CAGR of 4.0%.

Asia Pacific Seed Treatment Market Trends

The growing awareness to protect seeds and seedlings is driving the consumption of seed treatment pesticides

- The average consumption of seed treatment chemicals in Asia-Pacific was 261.08 grams per hectare in 2022. Seed treatment has become increasingly popular in recent years due to its effectiveness and efficiency in protecting and enhancing crop productivity.

- As agricultural practices in these countries are intensifying and the need for higher productivity is growing, Asia-Pacific farmers are becoming more aware of the importance of crop protection as an effective means of protecting crops from diseases, pests, and other stresses, thereby reducing the risk of yield loss.

- Seed treatment can prevent and offer protection to crops against several fungal diseases, including seed rot, seedling blight, damping off, root rot, and foliar diseases like powdery mildew, downy mildew, and early blight. The use of active ingredients helps as they are based on target diseases and seed treatment requirements. Metalaxyl, carbendazim, and captan are the most used active ingredients in seed treatment products in the Asia-Pacific market.

- Seed treatments are also being used against insect pests and nematodes. For instance, the root-knot nematode is the most dangerous among the nematode species that affect fruit and vegetable crops and is known to cause a yield loss of 34% in carrots, 26% in potatoes, 23% in tomatoes, 22% in bottle gourds, and 21% in brinjal, which can effectively be mitigated by seed treatment practices.

- The seed treatment industry in Asia-Pacific countries is witnessing technological advancements that enable more precise and efficient seed treatment applications. These advancements include improved seed treatment formulations and advanced seed treatment equipment, leading to higher usage of seed treatment chemicals by farmers in the region.

Increasing promotional activities by various government agencies across Asia-Pacific drives the demand and price

- Seed treatment plays an important role in protecting seeds and seedlings from seed and soil-borne diseases and insect pests affecting crop emergence and growth. Cypermethrin, abamectin, azoxystrobin, malathion, and metalaxyl are the most commonly used seed treatment chemicals in Asia-Pacific.

- Cypermethrin is a non-systemic soil-acting pyrethroid insecticide. It is used in seed treatment for the reduction of wheat bulb fly and wireworm damage to autumn/winter sown wheat and barley. It was valued at a price of USD 21.0 thousand per metric ton in 2022.

- Abamectin belongs to the ivermectin chemical class and has high intrinsic activity against nematodes. It is used to protect young plants from root-attacking nematodes in corn, soybean, and cotton production. It was priced at USD 8.7 thousand per metric ton in 2022.

- Azoxystrobin is a broad-spectrum preventative seed treatment fungicide with systemic properties recommended for the control of Deuteromycetes, Oomycetes, Ascomycetes, and Basidiomycetes fungi that cause yield losses in crops. In 2022, azoxystrobin was priced at USD 4.5 thousand per metric ton.

- Various regulations by government agencies are encouraging the use of seed treatments to increase the marketability of seeds. The Government of India has decided to launch a countrywide campaign for ensuring 100% seed treatment in all important crops during the kharif season. Pesticide industry associations, ATMAs, CIPMCs, KVKs, farmers clubs, SAUs, NGOs, etc., can play an important role in the campaign promoting 100% seed treatment. Such initiatives may further affect the price of seed treatment chemicals in the region over the coming years.

Asia Pacific Seed Treatment Industry Overview

The Asia Pacific Seed Treatment Market is fragmented, with the top five companies occupying 33.38%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Syngenta Group and UPL Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 Australia

- 4.3.2 China

- 4.3.3 India

- 4.3.4 Indonesia

- 4.3.5 Japan

- 4.3.6 Myanmar

- 4.3.7 Pakistan

- 4.3.8 Philippines

- 4.3.9 Thailand

- 4.3.10 Vietnam

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Insecticide

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

- 5.3 Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Myanmar

- 5.3.7 Pakistan

- 5.3.8 Philippines

- 5.3.9 Thailand

- 5.3.10 Vietnam

- 5.3.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Crystal Crop Protection Ltd

- 6.4.6 FMC Corporation

- 6.4.7 Nufarm Ltd

- 6.4.8 PI Industries

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms