アジア太平洋のペット用食事:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia-Pacific Pet Diet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 252 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693999

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

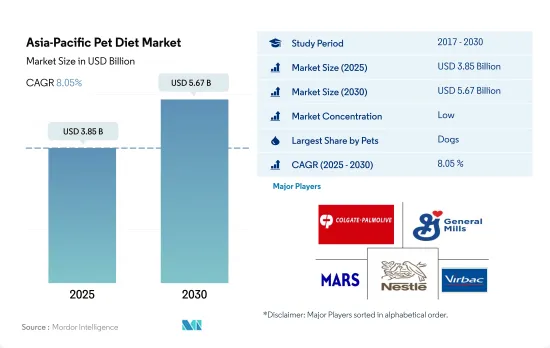

アジア太平洋のペット用食事の市場規模は、2025年には38億5,000万米ドルと推定され、2030年には56億7,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは8.05%で成長する見込みです。

アジア太平洋の人口が多く、様々な健康問題に罹患しやすいことから、犬がアジア太平洋のペット用動物食市場を独占しています。

- アジア太平洋のペット用動物用飼料市場は、2017~2021年の間に41.4%という大幅な急増を示しました。この著しい成長は、ペットの栄養科学と研究の継続的な進歩が、ペットの幅広い健康状態に効果的に対処できるより専門的な食事の創造につながったことに起因しています。その結果、2022年にはアジア太平洋のペットフード市場の10.5%をペット用動物飼料が占めるようになりました。

- アジア太平洋のペット用動物飼料市場では犬が最大のシェアを占め、2022年には市場の約48.1%を占めました。この犬の高い市場シェアは、主に他のペットに比べてこの地域の人口が多く、その結果、犬の様々な病気の発生率が増加傾向にあることに起因しています。犬の動物用食事の市場規模は、予測期間中にCAGR 8.4%を記録すると予測されています。

- 猫は、2022年に36.8%と第2位の市場シェアを占めています。猫用動物用飼料市場は、同地域における猫の飼育数の増加に牽引され、増加傾向にあります。猫の動物用飼料市場は、この地域の動物セグメントの中で最も急速に成長すると予測され、予測期間中のCAGRは8.7%と予想されます。

- その他のペット動物は、2022年の市場金額の15.1%を占めています。2022年にはペット数の39.5%を占めるため、その他のペット動物用飼料には潜在的な市場があります。その他のペットの動物用飼料市場は、予測期間中にCAGR 4.3%を記録すると予測されています。

- ペット数の増加と様々な健康状態をサポートする動物用飼料の能力は、予測期間中に市場を促進すると予想される主要因です。

動物用飼料の利点に関する認知度が高く、ペット数が多いことから、中国がアジア太平洋のペット用飼料市場を独占しています。

- ペット用動物用飼料は、特定のペットの健康問題に対処するために設計され、毎日の食事要件を満たすために必要なペットに不可欠な栄養を提供する特別に配合された飼料です。2022年には、動物用ペットフードはアジア太平洋ペットフード市場の10.6%を占めました。アジア太平洋のペットの飼い主の間で、ペットの健康問題やペットの人間化に関する意識が高まっていることから、同地域のペット用動物食市場は2017~2021年の間に40%増加しました。さらに、同期間中にペット数が12%増加したことも、市場増加の大きな要因の1つです。

- アジア太平洋では、中国がペット用動物用飼料市場の最大国で、2022年には9億5,250万米ドルを占めました。同国のシェアが高いのは、ペット数が多いためで、2022年にはアジア太平洋のペット数の53.9%を占めました。さらに、ペットの親として若い人口が多く存在するため、動物用食餌の使用に対する意識が高まり、需要が増加しています。

- 日本とオーストラリアは、ペット数が多いこと、ペットの人間化が進んでいること、これらの国のペットの親がペットフード製品に支出する意欲があることから、2022年の同地域のペット用動物用飼料市場の主要国でした。

- しかし、ペットの飼育率の上昇と都市化の進展により、タイとインドが予測期間中にそれぞれCAGR 13.6%と13.5%で急速に成長すると予想されます。

- ペットのヒューマニゼーションが進み、動物用飼料の使用に関する認識が高まっていること、ペットの親として若年層の人口が増加していることが、予測期間中にCAGR 8.0%で同地域のペット用飼料市場を牽引すると予測されます。

アジア太平洋のペット用食事の市場動向

この地域の猫の飼育数は、多種多様なキャットフード製品やサービスを通じて、購入から動物の世話までの支援を提供するペットカフェやペットショップを含む、新しく進化した購入エコシステムによって牽引されています。

- アジア太平洋では、猫は犬に比べて市場シェアが低く、2022年のペット数に占める割合は26.1%に過ぎないです。中国、インド、オーストラリアなどの国々では、猫を伴侶としている間にリラックスしてストレスが軽減されるといった健康上の利点から、ペットの飼育が増加しています。そのため、ペットとしての猫の飼育数は2017~2022年の間に0.28%増加しました。

- インドネシアやマレーシアのような国では、犬の親よりも猫の親の方が数が多く、2021年には猫のペット数がそれぞれ47%と34%を占めます。このため、これらの国ではドッグフードよりもキャットフードに投資する企業が増えています。中国では、都市部において猫を含むペットの数が増加しており、ペット総飼育数は2018~2020年にかけて10.2%増加し、2020年には都市部で1億80万人に達します。猫の飼育数は2020年の7,440万匹から2022年には8,250万匹に増加しているが、これはCOVID-19の大流行時にコンパニオンとして飼われるペット猫が増加したためです。猫の寿命は20年以上であるため、これは長期的な影響を及ぼすと予想されます。

- この地域では、ペットカフェやペットショップがオープンし、多種多様なペットフード製品やサービスを通じて、購入から動物の世話まで支援することで、ペットの採用と購入の新たなエコシステムが発展しつつあります。ベトナムでは、The Meow House by R Houseがベジタリアン・ヴィーガンフードを提供する猫カフェであり、猫の家となっています。健康上の利点による猫の飼育の増加、アジア太平洋諸国の文化的規範、ペット生態系の変化といった要因が、この地域での猫の飼育を後押ししています。

プレミアム化とペットの人間化という動向の高まりが、ペットの飼い主の支出増につながっています。

- アジア太平洋諸国では、ペットのヒューマニゼーションが進み、市販のペットフードを与えるようになったこと、さまざまな種類のペット用食事が入手可能になったこと、ペットの親がプレミアム価格を支払うことを厭わず、良質なプレミアムペットフードを好むようになったことなどが要因となって、ペットの支出が増加しています。さらに、ペットの犬の支出シェアが高く、2022年のペット支出額の38.9%を占めているのは、犬の飼い主が他のペットに比べて犬の餌の消費量が多いため、高品質のペットフードを与えているからです。例えば、オーストラリアでは犬が最も人気のあるペットであり、2022年には約40%の世帯が犬を飼っています。このような要因が予防医療の需要を押し上げ、このような特殊食の需要を高めています。

- 中国、インド、韓国はこの地域の主要なペット市場であり、ペット支出の伸びを記録しています。これらの国々では、特にCOVID-19の大流行後、健康を確保するためにペットに必要な栄養をより意識するようになったため、良質なプレミアムペットフードを与えるペットの数が増加しています。例えば、香港のキャットフード市場では、2022年のペットフード売上高の75%をプレミアムペットフード部門が占めています。ペットフードのオンライン販売は、ウェブサイトで入手できる膨大な数の商品と注文のしやすさから、特に中国の市場で高い割合を占めています。例えば、2022年の中国のオンラインチャネルによるペット売上は58.3%であるのに対し、ペットショップチャネルの寄与は28.1%です。

- ペットフードに対する需要の高まりと、ペットのための良質なフードに対する意識の高まりにより、調査期間中、この地域のペットの親によるペットへの支出は増加しました。

アジア太平洋のペット用食事産業概要

アジア太平洋のペット用食事市場は細分化されており、上位5社で15.61%を占めています。この市場の主要企業は、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、General Mills Inc.、Mars Incorporated、Nestle(Purina)、Virbacです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ製品

- 糖尿病

- 消化器過敏症

- 口腔ケア食

- 腎臓

- 尿路疾患

- その他の動物用飼料

- ペット

- 猫

- 犬

- その他

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- フィリピン

- 台湾

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Affinity Petcare SA

- Alltech

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- PLB International

- Schell & Kampeter Inc.(Diamond Pet Foods)

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The Asia-Pacific Pet Diet Market size is estimated at 3.85 billion USD in 2025, and is expected to reach 5.67 billion USD by 2030, growing at a CAGR of 8.05% during the forecast period (2025-2030).

Dogs dominate the Asia-Pacific pet veterinary diet market owing to their large population in the region and their susceptibility to various health issues

- The Asia-Pacific pet veterinary diet market witnessed a significant surge of 41.4% between 2017 and 2021. This significant growth can be attributed to the continuous advancements in pet nutrition science and research, leading to the creation of more specialized diets that can effectively address a wide range of health conditions in pets. As a result, pet veterinary diets accounted for 10.5% of the Asia-Pacific pet food market in 2022.

- Dogs held the largest share in the Asia-Pacific pet veterinary diets market, accounting for about 48.1% of the market in 2022. This higher market share of dogs is mainly attributed to their large population in the region compared to other pets, resulting in an increasing trend in the incidence of various diseases in dogs. The dog veterinary diets market value is anticipated to register a CAGR of 8.4% during the forecast period.

- Cats held the second-largest market share of 36.8% in 2022. The cat veterinary diet market is witnessing an increasing trend, driven by the rising cat population in the region. The market for cat veterinary diets is projected to be the fastest-growing among animal segments in the region, with an expected CAGR of 8.7% during the forecast period.

- The other pet animals accounted for 15.1% of the market value in 2022. There is a potential market for veterinary diets in other pet animals, as they accounted for 39.5% of the pet population in 2022. The other pet veterinary diets market is anticipated to register a CAGR of 4.3% during the forecast period.

- The growing pet population and the ability of veterinary diets to support various health conditions are the major factors anticipated to drive the market during the forecast period.

China dominates the Asia-Pacific pet veterinary diet market due to higher awareness about the benefits of veterinary diets and the presence of a higher pet population

- Pet veterinary diets are specially formulated diets that are designed to address specific pet health issues and provide essential nutrition for pets required to meet daily dietary requirements. In 2022, pet veterinary diets accounted for 10.6% of the Asia-Pacific pet food market. The growing awareness about pet health concerns and pet humanization trend among pet owners in Asia-Pacific increased the pet veterinary diets market in the region by 40% between 2017 and 2021. Additionally, the increase in pet population by 12% during the same period is also one of the major factors for the increase in the market.

- In Asia-Pacific, China was the largest country in the pet veterinary diets market, accounting for USD 952.5 million in 2022. The country's higher share was due to its higher pet population, which was 53.9% of the Asia-Pacific pet population in 2022. Additionally, the significant presence of the younger population as pet parents has increased their demand, with a higher awareness about the use of veterinary diets.

- Japan and Australia were the major countries in the pet veterinary diets market in the region in 2022 because of their higher pet population, the higher pet humanization trend, and the willingness of pet parents in these countries to spend on pet food products.

- However, growing pet adoption and increasing urbanization are anticipated to drive Thailand and India faster, at CAGRs of 13.6% and 13.5%, respectively, during the forecast period.

- The increasing pet humanization and growing awareness about the usage of veterinary diets and the increasing younger adult population as pet parents are anticipated to drive the pet veterinary diet market in the region at a CAGR of 8.0% during the forecast period.

Asia-Pacific Pet Diet Market Trends

The regional cat population is driven by a new and evolving purchase ecosystem, including pet cafes and pet stores providing assistance ranging from purchasing to taking care of the animals through a wide variety of cat food products and services

- In the Asia-Pacific, cats have a lower share in the market compared to dogs and accounted for only 26.1% of the regional pet population in 2022. Countries such as China, India, and Australia have witnessed increased pet ownership due to health benefits such as feeling relaxed and less stressed while having cats as companions. Therefore, the cat population as a pet increased by 0.28% between 2017 and 2022.

- Cat parents are higher in number than dog parents in countries such as Indonesia and Malaysia, with their cat pet populations accounting for 47% and 34%, respectively, in 2021, because of their religious and cultural norms that prefer the adoption of cats as pets over dogs. This drives companies to invest more in cat food in these countries than dog food. In China, there has been an increase in the number of pets, including cats, in urban areas, and the total pet population increased by 10.2% between 2018 and 2020 to reach 100.8 million in urban areas in 2020. The cat population increased from 74.4 million in 2020 to 82.5 million in 2022 because of a rise in pet cats being adopted for companionship during the COVID-19 pandemic. This is expected to have long-term effects as the life span of cats is more than 20 years.

- A new pet adoption and purchase ecosystem is evolving in the region, with the opening of pet cafes and stores providing assistance ranging from purchasing to taking care of the animals through a wide variety of pet food products and services. In Vietnam, The Meow House by R House is a cat cafe that serves vegetarian and vegan food and is a home for cats. Factors such as the rise in the adoption of cats due to health benefits, cultural norms in Asia-Pacific countries, and changes in the pet ecosystem are helping boost cat adoption in the region.

Rising trends of premiumization and pet humanization are leading to increased expenditure among pets owners

- In Asia-Pacific countries, there has been a rise in pet expenditure because of factors such as an increase in pet humanization leading to the feeding of pets with commercial pet food, availability of different types of pet diets, and pet parents preferring good quality premium pet food as they are willing to pay premium prices. Moreover, pet dogs have a higher expenditure share and accounted for 38.9% of the pet expenditure in 2022 because dog owners feed them high-quality pet food due to the higher consumption of food by dogs compared to other pets. For instance, in Australia, dogs are the most popular pets, and about 40% of households had a pet dog in 2022. Such factors are boosting the demand for preventive care and demand for these specialized diets.

- China, India, and South Korea are the major pet markets in the region, which have registered growth in pet expenditure. These countries have witnessed a high number of pets being fed good quality premium pet food, especially after the COVID-19 pandemic, as they are more aware of their pet's nutritional requirements for ensuring good health. For instance, in Hong Kong's cat food market, the premium pet food segment accounted for 75% of pet food sales in 2022. Online sales of pet food are high in the market, especially in China, due to the vast number of products available on the websites and the ease of ordering. For instance, in 2022, China's pet sales from online channels were 58.3% compared to the pet store channel's contribution of 28.1%.

- The rising demand for pet food and growing awareness about good quality food for their pets resulted in an increase in pet expenditure by pet parents in the region during the study period.

Asia-Pacific Pet Diet Industry Overview

The Asia-Pacific Pet Diet Market is fragmented, with the top five companies occupying 15.61%. The major players in this market are Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), General Mills Inc., Mars Incorporated, Nestle (Purina) and Virbac (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Product

- 5.1.1 Diabetes

- 5.1.2 Digestive Sensitivity

- 5.1.3 Oral Care Diets

- 5.1.4 Renal

- 5.1.5 Urinary tract disease

- 5.1.6 Other Veterinary Diets

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Country

- 5.4.1 Australia

- 5.4.2 China

- 5.4.3 India

- 5.4.4 Indonesia

- 5.4.5 Japan

- 5.4.6 Malaysia

- 5.4.7 Philippines

- 5.4.8 Taiwan

- 5.4.9 Thailand

- 5.4.10 Vietnam

- 5.4.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Affinity Petcare SA

- 6.4.2 Alltech

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 General Mills Inc.

- 6.4.6 Mars Incorporated

- 6.4.7 Nestle (Purina)

- 6.4.8 PLB International

- 6.4.9 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 252 Pages

- 納期

- 2~3営業日