南米のペット用食事:市場シェア分析、産業動向、成長予測(2025~2030年)

South America Pet Diet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 209 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693988

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

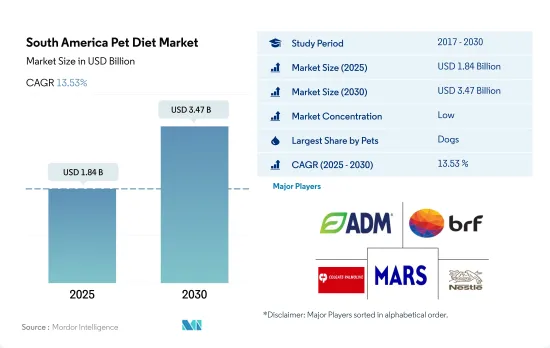

南米のペット用食事市場規模は2025年に18億4,000万米ドルと推定され、2030年には34億7,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは13.53%で成長する見込みです。

犬の疾病の増加により、犬用飼料がペット用食事市場を席巻

- ペット用食事は、ペットの特定の健康状態に対処するために配合された特殊なペットフード製品です。南米市場では、2017~2021年にかけてペット用食事の金額が73.7%という大幅な伸びを示しました。この成長は、ペットの栄養科学と研究の進歩により、ペットの幅広い健康問題に対処できるより専門的な食事が開発されたことに起因しています。その結果、2022年の南米のペットフード市場に占めるペット用食事の割合は10.6%となりました。

- 南米のペット用動物食市場は犬が支配的で、2022年には57.1%のシェアを占めています。犬セグメントのシェアが高いのは、この地域では他のペットに比べて犬の飼育数が多いこと、犬の様々な病気の発生率が増加していることが主要原因です。ペット用食事市場の犬セグメントの金額は、予測期間中に15.6%のCAGRで推移すると予測されています。

- その他のペット動物は、潜在的な健康問題を予防するためのペット用食事に対する多様な要件を反映して、第2位の市場シェアを占めています。その他のペット動物用のペット用食事市場は、2022年に2億9,810万米ドルに達しました。予測期間中のCAGRは7.9%で、安定した成長が見込まれています。

- 猫は2022年に18.6%の市場シェアを占めました。ペット用食事市場の猫セグメントは、同地域における猫の飼育数の増加に牽引され、増加傾向にあります。動物用食餌の猫セグメントは、予測期間中に16.1%の予想CAGRを記録し、この地域で最も急成長すると予測されています。

- ペット数の増加と様々な健康状態をサポートするペット用食事の能力が、予測期間中の市場を牽引すると予測されています。

ペット数が多く、ペットの病気の発生率が増加していることから、ブラジルがペット用食事市場を独占

- ペット用食事は、ペットの特定の病気や感染症に対処・管理する上で重要な役割を果たし、予防と治療の両面で役立っています。ペットの健康と福祉の重要性が高まるにつれ、ペット用食事はこの地域のペットフード市場で重要性を増しています。2022年には、ペット用食事は南米のペットフード市場の10.6%を占めました。

- 南米のペット用食事市場は、2017~2022年の間に50%以上の着実な増加を示しました。この急増は、COVID-19パンデミックの間にペットの飼育が増加したことや、ペット特有のニーズに対応した幅広い食事オプションが利用可能になったことなどの要因によるものと考えられます。

- 国によるペット用食事市場はブラジルが最も大きく、2022年の市場規模は6億9,340万米ドル、次いでアルゼンチンが2億2,070万米ドルです。ブラジルが地域別で最大の市場シェアを持つのは、他国に比べてペット数が多いこと、製造施設が確立していること、プレミアム化が進んでいることなどが理由です。例えば、2022年のブラジルのペット数は1億5,640万人であるのに対し、アルゼンチンのペット数は4,630万人に過ぎないです。

- 専門店は有力な流通チャネルとなっており、2022年には南米のペット用食事市場の32.6%を占めます。ブラジルの大手専門店ブランドであるPetzは、2021年に138の店舗と116の動物病院を展開し、ブラジル全土で急速に存在感を高めています。

- ペットの様々な感染症を治療するために特別に配合された多様なペット用食事が入手可能であることに加え、ペットの飼い主がペットの健康増進のために投資意欲を高めていることが、南米のペット用食事市場を牽引しており、予測期間中にCAGR 14.2%を記録すると予測されています。

南米のペット用食事の市場動向

ブラジルは、狭い居住空間への適応性とメンテナンスの手間が少ないという利点から、この地域で最大の猫の飼育数を占める

- 南米のペット猫の飼育数は着実に増加しており、2019~2022年の間に13.3%増加しました。この増加傾向は、COVID-19パンデミックによってもたらされた長期間の自宅監禁の間、コンパニオンとしての猫の採用率が高くなったことに起因しています。この地域の国々の中では、ブラジルが最大の猫の飼育数を保有しており、2022年時点で猫の飼育数全体の約55.5%を占めています。南米では、2022年のペット数全体に占める猫の割合は19.3%です。このように猫の割合が相対的に低いのは、犬がより実用的で価値のあるペットと考えられている文化的認識に起因していると考えられます。猫の数は、同地域における犬の総個体数の50.0%に過ぎないです。

- 狭い居住空間でも窮屈さを感じさせない猫の順応性は、犬と比べて維持費が安いことも相まって、猫の飼育を好む傾向が強まっています。この動向により、地域全体で猫の飼育頭数が大幅に増加しています。ブラジルだけでも、2020年時点で約1,430万世帯が猫をペットとして飼っています。アルゼンチンでは猫の飼育率はさらに高く、31.4%、つまり460万世帯が猫をペットとして飼っています。

- この地域の重要な新たな動向は、猫カフェの設立です。2021年現在、ブラジルには約20の猫カフェがあり、快適な環境で猫と触れ合いながら飲み物を楽しむというユニークな機会を客に提供しています。このような猫カフェの動向は、狭い居住空間にも適応できる猫の能力と相まって、この地域で人気のペットとしての猫の飼育をさらに促進する可能性を秘めています。

ペット用高級獣医食の消費増加とペットの人間化の進展がペット支出を増加させた

- 南米におけるペット支出は一貫した成長を示しており、2019~2022年の間に約18.1%増加します。この増加動向は、同地域全体でペットの飼い主数が増加していることに起因しています。ブラジルでは、同期間にペットを所有する世帯数が増加し、CAGR 1.3%を記録しました。アルゼンチンでは、ペットの飼育数が増加し、2016~2020年にかけてCAGR 1.4%を記録しました。

- 同地域のペットオーナーはペットの人間化にますます力を入れるようになっており、高所得者層は天然成分で作られた製品を選ぶことで売上成長を促進し、ペット製品のプレミアム化を推進しています。ペットの動物用食事への支出は、2022年のペット一匹当たりの支出全体の約15.7%を占めています。同国のペット1匹当たりの栄養補助食品支出は、2017年の158.4米ドルから2022年には200.2米ドルに増加しました。2017~2022年にかけて、ペットの動物用食事に支出する飼い主数は、犬で年間約39.6%、猫で18.7%、その他のペット動物で14.7%増加しました。南米諸国の中では、ブラジルが1頭当たりのペット支出額が最も高く、88.4米ドルに達し、僅差でアルゼンチンが2022年に65.1米ドルで続きました。ブラジルのペット支出額が高いのは、主にペットの健康に対する支出が増加しているためです。

- 流通チャネルの中では、ペットショップ、動物病院、スーパーマーケットなどのオフラインの小売チャネルが、この地域のペット用動物食製品の好ましい流通チャネルです。しかし、COVID-19の大流行時には、ペット用食事のeコマース導入が増加しました。

- プレミアムペット用食事の消費量の増加とペットの人間化の進展が、予測期間中の同地域のペット支出を促進すると予想されます。

南米のペット用食事の産業概要

南米のペット用食事市場は細分化されており、上位5社で29.54%を占めています。この市場の主要企業は、ADM、BRF Global、Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)、Mars Incorporated、Nestle(Purina)です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブ製品

- 糖尿病

- 消化器過敏症

- 口腔ケア食

- 腎臓

- 尿路疾患

- その他のペット用食事

- ペット

- 猫

- 犬

- その他

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- アルゼンチン

- ブラジル

- その他の南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Alltech

- BRF Global

- Colgate-Palmolive Company(Hill's Pet Nutrition Inc.)

- FARMINA PET FOODS

- General Mills Inc.

- Mars Incorporated

- Nestle(Purina)

- Schell & Kampeter Inc.(Diamond Pet Foods)

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 50001470

The South America Pet Diet Market size is estimated at 1.84 billion USD in 2025, and is expected to reach 3.47 billion USD by 2030, growing at a CAGR of 13.53% during the forecast period (2025-2030).

Dogs dominated the veterinary diets market owing to the increasing prevalence of diseases among dogs

- Veterinary diets are specialized pet food products formulated to address specific health conditions in pets. In the South American market, the value of pet veterinary diets witnessed a significant increase of 73.7% between 2017 and 2021. This growth can be attributed to advancements in pet nutrition science and research, leading to the development of more specialized diets capable of addressing a wider range of health issues in pets. As a result, pet veterinary diets accounted for 10.6% of the South American pet food market in 2022.

- The South American pet veterinary diet market is dominated by dogs, and they accounted for a share of 57.1% in 2022. The higher share of the dog segment is mainly due to the large population of dogs in the region compared to other pets and the increased incidence of various diseases in dogs. The value of the dog segment of the veterinary diet market is anticipated to register a CAGR of 15.6% during the forecast period.

- Other pet animals hold the second-largest market share, reflecting the diverse requirements for veterinary diets to prevent potential health problems. The veterinary diet market for other pet animals reached a value of USD 298.1 million in 2022. It is anticipated to experience steady growth, registering a CAGR of 7.9% during the forecast period.

- Cats held a market share of 18.6% in 2022. The cat segment of the veterinary diet market is witnessing an increasing trend, driven by the rising cat population in the region. The cat segment of the veterinary diets is projected to be the fastest-growing in the region, registering an expected CAGR of 16.1% during the forecast period.

- The growing pet population and veterinary diets' ability to support various health conditions are anticipated to drive the market during the forecast period.

Brazil dominated the pet veterinary diets market owing to its large pet population and increasing incidence of pet diseases

- Veterinary diets play a crucial role in addressing and managing specific diseases and infections in pets, serving both preventive and curative purposes. With the growing importance of pet health and well-being, veterinary diets have gained significant importance in the region's pet food market. In 2022, veterinary diets accounted for 10.6% of the South American pet food market.

- The South American pet veterinary diets market witnessed a steady increase of more than 50% between 2017 and 2022. This surge can be attributed to factors such as increased pet adoption during the COVID-19 pandemic and the availability of a wider range of dietary options for pets' specific needs.

- Brazil has the largest country-wise veterinary diets market, with a value of USD 693.4 million in 2022, followed by Argentina, with a value of USD 220.7 million in 2022. Brazil has the largest regional market share because of its high pet population compared to other countries, well-established manufacturing facilities, and growing premiumization. For instance, in 2022, the pet population in Brazil was 156.4 million, whereas the pet population in Argentina was only 46.3 million.

- Specialty stores have become a prominent distribution channel, accounting for 32.6% of the South American veterinary diets market in 2022. Petz, a leading specialty store brand in Brazil, rapidly expanded its presence throughout the country with 138 stores and 116 veterinary clinics in 2021.

- The availability of a diverse range of veterinary diets specifically formulated to treat various pet infections, along with pet owners' willingness to invest more in improving the health of their pets, is driving the veterinary diets market in South America, which is projected to register a CAGR of 14.2% during the forecast period.

South America Pet Diet Market Trends

Brazil accounted for the largest cat population in the region due to their advantages of adaptability to smaller living spaces and lower maintenance

- The pet cat population in South America has been steadily growing, increasing by 13.3% between 2019 and 2022. This upward trend can be attributed to the higher adoption rates of cats as companions during the extended periods of home confinement brought on by the COVID-19 pandemic. Among the countries in the region, Brazil holds the largest cat population, accounting for about 55.5% of the total cat population as of 2022. In South America, cats comprised 19.3% of the overall pet population in 2022. This relatively lower proportion of cats can be attributed to cultural perceptions wherein dogs are considered more practical and valued pets. The number of cats represents only 50.0% of the total dog population in the region.

- The adaptability of cats to smaller living spaces without feeling confined, coupled with their lower maintenance costs compared to dogs, contributed to an increasing preference for cat ownership. This trend has led to a significant rise in the pet cat population across the region. In Brazil alone, as of 2020, about 14.3 million households owned cats as pets. In Argentina, the rate of cat ownership was even higher, with 31.4% of households, which is 4.6 million households with cats as pets.

- An important emerging trend in the region is the establishment of cat cafes. As of 2021, there were around 20 cat cafes in Brazil, providing customers with a unique opportunity to enjoy a drink while interacting with cats in a comfortable setting. This growing trend of cat cafes, coupled with the cat's ability to adapt to smaller living spaces, has the potential to further enhance the adoption of cats as popular pets in the region.

Higher consumption of premium pet veterinary diets and growing pet humanization have increased pet expenditure

- Pet expenditure in South America has shown consistent growth, with an increase of about 18.1% between 2019 and 2022. This upward trend can be attributed to the rising number of pet owners across the region. In Brazil, the number of households owning a pet grew in the same period, registering a CAGR of 1.3%. In Argentina, pet ownership increased, registering a CAGR of 1.4% between 2016 and 2020.

- Pet owners in the region are increasingly focused on pet humanization, with higher-income individuals driving sales growth by opting for products made with natural ingredients, driving pet product premiumization. The expenditure on pet veterinary diets accounted for about 15.7% of the total pet expenditure per pet in 2022. The pet nutraceutical expenditure per pet in the country increased from USD 158.4 in 2017 to USD 200.2 in 2022. From 2017 to 2022, the number of pet owners spending on pet veterinary diets increased by about 39.6% for dogs, 18.7% for cats, and 14.7% for other pet animals annually. Among South American countries, Brazil had the highest pet expenditure per animal, reaching USD 88.4, followed closely by Argentina at USD 65.1 in 2022. This higher pet expenditure in Brazil is mainly due to the country's increased spending on pet health.

- Among distribution channels, offline retail channels such as pet shops, vet clinics, and supermarkets are the preferred distribution channels for pet veterinary diet products in the region. However, during the COVID-19 pandemic, the adoption of e-commerce for pet veterinary diets increased.

- The higher consumption of premium pet veterinary diets and growing pet humanization are anticipated to drive pet expenditure in the region during the forecast period.

South America Pet Diet Industry Overview

The South America Pet Diet Market is fragmented, with the top five companies occupying 29.54%. The major players in this market are ADM, BRF Global, Colgate-Palmolive Company (Hill's Pet Nutrition Inc.), Mars Incorporated and Nestle (Purina) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Product

- 5.1.1 Diabetes

- 5.1.2 Digestive Sensitivity

- 5.1.3 Oral Care Diets

- 5.1.4 Renal

- 5.1.5 Urinary tract disease

- 5.1.6 Other Veterinary Diets

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Alltech

- 6.4.3 BRF Global

- 6.4.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.4.5 FARMINA PET FOODS

- 6.4.6 General Mills Inc.

- 6.4.7 Mars Incorporated

- 6.4.8 Nestle (Purina)

- 6.4.9 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

南米のペット用食事:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 209 Pages

- 納期

- 2~3営業日