|

市場調査レポート

商品コード

1940887

東南アジアのフードサービス:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Southeast Asia Foodservice - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 東南アジアのフードサービス:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 260 Pages

納期: 2~3営業日

|

概要

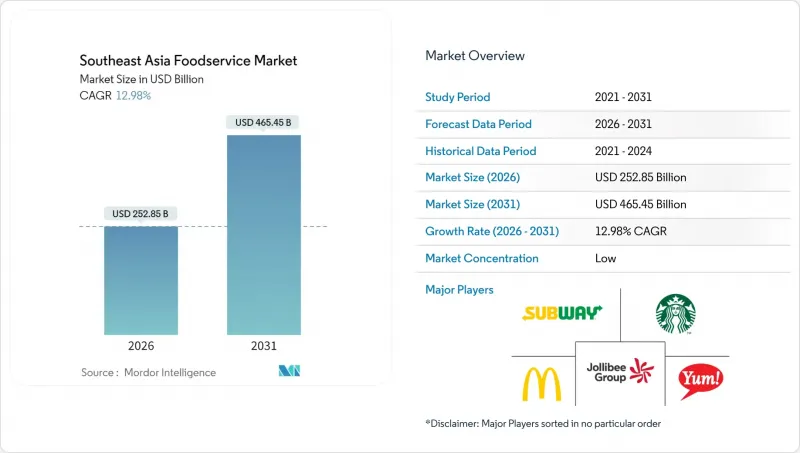

東南アジアのフードサービス市場は、2025年の2,238億米ドルから2026年には2,528億5,000万米ドルへ成長し、2026年から2031年にかけてCAGR12.98%で推移し、2031年までに4,654億5,000万米ドルに達すると予測されています。

経済成長、都市化、スマートフォン利用の増加により、飲食店やデリバリーサービスの消費者基盤が拡大しております。2022年から2023年にかけて、国際観光客数はほぼ倍増し、ホテルや路上店舗での消費を促進しました。クイックサービス形式やクラウドキッチンの台頭は、東南アジア市場における利便性、スピード、そしてより効率的な拡大モデルを優先する市場の変化を浮き彫りにしています。独立系事業者が店舗網の大半を占める一方で、チェーングループはフランチャイズ、テクノロジー、集中購買を活用し、急速に規模を拡大しています。Grabが主導するデリバリーアグリゲーターは競争を激化させており、レストランは収益性向上のため、手数料戦略や店舗内経済性の見直しを迫られています。

東南アジア外食産業市場の動向と洞察

デジタル注文・デリバリーの急速な普及

デジタル注文プラットフォームは、単なる利便性以上の価値を提供し、東南アジアのフードサービスバリューチェーンを変革しています。これらのプラットフォームはリアルタイムデータを活用し、飲食店が需要を正確に予測し、在庫管理をより効率的に行うことを支援します。これにより、予測型発注システムを通じて食品廃棄量を最大23%削減できた飲食店も少なくありません。ベトナムは、急速な都市化(現在40%超)と2024年時点で約8,800万人に達する大規模なオンライン人口に支えられ、このデジタル変革をリードしています。Grabなどのアプリは、フードデリバリー、デジタル決済、ロイヤルティプログラム、事業者向け融資を単一プラットフォームに統合したビジネスモデルで市場を再構築しています。この統合はプラットフォームの顧客生涯価値を高めるだけでなく、飲食店が顧客獲得コストを削減するのにも貢献しています。こうしたデジタルエコシステムの拡大に伴い、東南アジアの急速に変化する外食市場において、運営効率が向上し、飲食店と消費者の関わり方が再定義されつつあります。

クラウドキッチンとバーチャルキッチンがコンセプト検証と市場拡大を推進

パンデミック期に注目を集めたクラウドキッチンは、今や東南アジアのフードサービス市場における重要な成長戦略となっています。これらのキッチンは、レストランブランドが新たなアイデアをテストし、コストを大幅に抑えながら急速に拡大することを可能にします。従来の店内飲食レストランと比較して、60~70%少ない投資で済みます。しかしながら、市場の成熟に伴い、高い配達コストやブランド差別化の難しさといった課題から、業界再編が進んでいます。この動向は特にシンガポールで顕著であり、複数の事業者が撤退しています。競争力を維持するため、主要クラウドキッチン事業者はイノベーションに注力しています。垂直農法を導入して食材の安定供給を確保し、AIを活用したツールでメニューを最適化しています。これらの戦略により、仮想ブランド全体で品質を保ちつつ、食材コストを15~20%削減することが可能となっています。さらに、GoToのような企業はクラウドキッチンと少数の実店舗を組み合わせたハイブリッドモデルを導入しています。このアプローチにより、ブランドの認知度向上と顧客エンゲージメントの強化が図られています。こうした動きは、テクノロジーと戦略的拡大がレストランブランドの運営と成長の在り方を再構築している、同地域の外食産業市場における広範な変革を浮き彫りにしています。

分断された規制と複雑なライセンシング制度

複数のASEAN市場で事業を展開するレストランチェーンは、規制の違いにより重大な課題に直面しています。3つ以上の管轄区域で事業を管理する事業者のコンプライアンスコストは、通常、収益の8~12%を占めます。インドネシアでは複雑なハラール認証要件に対応する必要があり、タイでは厳格な外資所有規制が施行されています。シンガポールは厳格な食品安全基準により、さらに複雑さを増しています。こうした異なる規制には、現地の専門知識と専用のコンプライアンスシステムが求められます。さらに、食品安全認証に関する相互承認協定が欠如しているため、企業は個別の品質保証システムを維持せざるを得ず、単一市場に注力する競合他社と比較して15~20%の運営コスト増となっています。最近のASEAN経済統合に向けた取り組みには可能性が見られますが、実施は2027年以降と予想されており、拡大を目指す企業にとって即時の救済策とはなり得ません。

セグメント分析

2025年現在、東南アジアにおけるクイックサービスレストラン(QSR)の市場シェアは42.20%と高い水準を維持しております。その優位性は、効率的な運営と技術活用によるもので、多様な市場において一貫した顧客体験を保証しています。標準化されたプロセスと厨房自動化システムの導入により、QSRは労働力への依存度を25~30%削減。このアプローチにより、賃金上昇コストの管理と高いサービス水準の維持を両立させております。マクドナルドやKFCなどの主要チェーンは、デジタル注文システムやモバイル決済オプションに多額の投資を行っております。例えばマクドナルドは、東南アジアにおける注文の大半が現在デジタルチャネル経由であると報告しております。このセグメントは、便利な食事への文化的シフトや、インドネシア、タイ、ベトナムの都市部における拡大する中産階級の多忙なライフスタイルに支えられ、成長を続けております。

クラウドキッチンは外食産業で最も急成長している分野であり、2031年までCAGR18.62%が見込まれています。これらのキッチンはデリバリー業務に特化することで、店舗運営費や好立地への依存を不要とし、業界を変革しています。当初はパンデミック時の解決策として登場したクラウドキッチンは、現在では主要な成長戦略へと発展しました。既存ブランドは、従来型店舗と比較して60~70%低い資本投資で新コンセプトを試験導入することが可能となります。GoToが2025年までに400店舗のフランチャイズ展開を計画していることは、クラウドキッチンとデジタルプラットフォームの統合を浮き彫りにしています。このモデルは、決済処理、顧客獲得、在庫管理など、レストランパートナーに不可欠な技術支援を提供します。しかし、シンガポールのような成熟市場では、統合圧力が高まる中、混雑した市場で差別化を図ることや配達効率の向上といった課題に事業者は直面しています。

2025年現在、独立店舗が69.10%という圧倒的な市場シェアを占めており、東南アジアにおける本場の味や地域に根ざした食体験への強い嗜好を反映しています。こうした店舗は、多くの場合家族経営で代々受け継がれており、柔軟なメニュー構成や文化的に本場の味を再現した料理を提供することで繁栄しています。特に人口密集都市部では、地域コミュニティの集いの場として重要な役割を果たしています。地元の嗜好や旬の食材に迅速に対応できる能力は顧客満足度において優位性をもたらし、個別対応のサービスやカスタマイズされたメニューを通じてチェーン店競合他社を凌駕することも少なくありません。しかしながら、独立系事業者は食材費の高騰、規制要件の厳格化、新技術導入の必要性といった課題に直面しています。管理資源と規模の経済性を有する大規模事業者は、こうした圧力に対処する上でより有利な立場にあります。

チェーン店は年間平均成長率(CAGR)13.29%で急速に拡大しています。資金調達の容易さと効率的な運営システムが成長の原動力となり、複数市場への迅速な展開を可能にしています。技術投資とサプライチェーンの効率化により、チェーン店は食品コストを15~20%削減しつつ、全店舗で一貫した品質を維持。これにより個人経営店に対して大きな競争優位性を確立しています。例えば、ジョリビーはベトナムで200店舗に拡大し、コンポーズコーヒーを3億4,000万米ドルで買収しました。これは地域チェーンが文化的適合性と運営効率を組み合わせ、世界のブランドと競争する手法を示しています。フランチャイズモデルも人気を集めており、チェーン運営の効率性と現地市場への知見を融合させています。この手法により、より迅速な拡大が可能となり、親会社の資本要件が軽減され、独立した起業家に実績あるビジネスシステムが提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- デジタル注文・配送の急速な普及

- クラウドキッチンとバーチャルキッチンがコンセプト検証と市場拡大を推進

- カスタマイズ機能によるパーソナライゼーション:オーダーメイド形式とデータ駆動型提案

- 観光・ホスピタリティ業界との連携による飲食サービスの強化

- 健康とウェルネスの動向は、クリーンラベルと植物由来食材を重視したメニューに焦点が当てられています

- エンドツーエンドの業務技術(POSシステム、厨房自動化、非接触決済を含む)

- 市場抑制要因

- 分断された規制と複雑なライセンシング制度

- 生鮮食品のサプライチェーン変動性

- 人件費の上昇と人材不足

- アグリゲーター手数料とラストマイルコストが収益性を低下させます。

- 規制環境

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 業界の主な動向

- 店舗数

- 平均注文金額

- メニュー分析

第6章 市場セグメンテーション

- 外食産業のタイプ

- カフェ&バー

- 料理別

- バー&パブ

- カフェ

- ジュース/スムージー/デザートバー

- 専門コーヒー&ティーショップ

- 料理別

- クラウドキッチン

- フルサービスレストラン

- 料理別

- アジア

- 欧州

- ラテンアメリカ

- 中東料理

- 北米

- その他のフルサービスレストラン料理

- 料理別

- クイックサービスレストラン

- 料理別

- ベーカリー

- バーガー

- アイスクリーム

- 肉料理中心の料理

- ピザ

- その他のQSR料理

- 料理別

- カフェ&バー

- 店舗

- チェーン店

- 独立店舗

- 立地

- レジャー

- 宿泊施設

- 小売り

- 単独店舗

- 旅行

- サービス形態

- 店内飲食

- テイクアウト

- デリバリー

- 国

- インドネシア

- マレーシア

- フィリピン

- シンガポール

- タイ

- ベトナム

- 東南アジアその他

第7章 競合情勢

- 主要な戦略的動きs

- 市場シェア分析

- 企業概況

- 企業プロファイル

- Doctor's Associates Inc.

- Domino's Pizza, Inc.

- Inspire Brands Inc.

- Jollibee Foods Corporation

- Marrybrown Sdn Bhd

- McDonald's Corporation

- Minor International PCL

- Nando's Group Holdings Ltd

- Restaurant Brands International Inc.

- Secret Recipe Cakes & Cafe Sdn Bhd

- Starbucks Corporation

- Thai Beverage PCL

- The Wendy's Company

- Tung Lok Restaurants(2000)Ltd

- Yum!Brands Inc.

- Zen Corporation Group PCL

- BreadTalk Group Ltd

- JDE Peet's N.V

- Max's Group, Inc.

- Church's Texas Chicken