|

市場調査レポート

商品コード

1911774

欧州の乳製品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Europe Dairy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の乳製品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 303 Pages

納期: 2~3営業日

|

概要

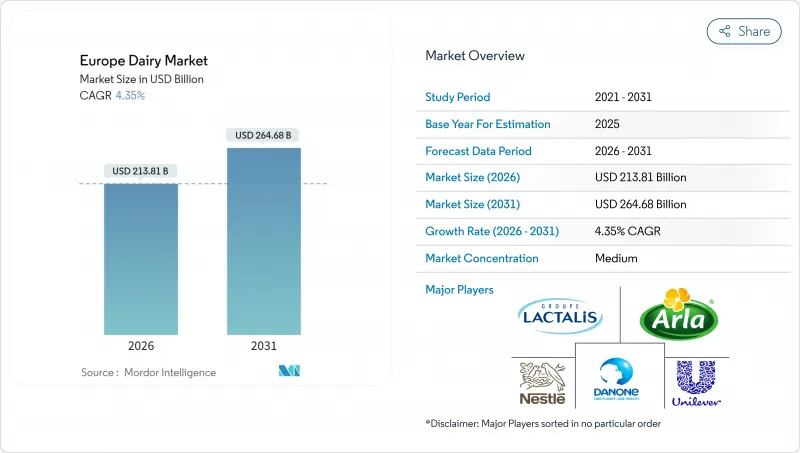

欧州の乳製品市場は、2025年に2,049億米ドルと評価され、2026年の2,138億1,000万米ドルから2031年までに2,646億8,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは4.35%と見込まれています。

需要は従来の液体乳から、有機製品、乳製品デザート、タンパク質強化製品などのプレミアム・機能性カテゴリーへと移行しています。免疫サポート、腸内環境、骨の強化に焦点を当てた効能表示を背景に、機能性ヨーグルトや強化チーズ製品の技術革新が加速しています。健康意識の高まりにより、ギリシャヨーグルトや強化ミルク製品を含む、低脂肪・高タンパク・プロバイオティクス豊富な乳製品への需要が増加しています。EUの厳格な食品安全・表示規制は、国内乳製品の純度とトレーサビリティを確保することで消費者の信頼を強化しています。これに対応し、主要加工業者はカーボンニュートラル認証の導入、リサイクル可能な包装材の採用、農家との緊密な連携を進めています。こうした取り組みは生乳の安定供給と高級品棚の確保に寄与しています。液体乳の消費量が減少する中、持続可能性への要請が牛群の最適化、生産能力の転換、高利益率をもたらす付加価値製品の投資を促進しています。生乳価格の上昇を相殺し規模の経済を達成するため、協同組合と多国籍企業が合併を追求する中、競合情勢は激化しています。

欧州乳製品市場の動向と洞察

有機・自然派乳製品に対する消費者需要の高まり

欧州の消費者、特に健康志向の強い層は、食品選択において透明性と持続可能性をますます重視するようになり、有機乳製品セグメントに大きな変化をもたらしています。この変化する嗜好は、従来の有機認証の枠組みを超えています。加工業者は現在、人工添加物の排除と「農場から食卓まで」のストーリーの推進に注力し、消費者の期待に応えようとしています。西欧市場はこの動向の最前線にあり、これらの地域の消費者は認証有機製品に対してプレミアム価格を支払う意欲が高い傾向にあります。欧州連合有機規則2018/848は、品質保証のための標準化された枠組みを提供し、有機表示に対する消費者の信頼を確保することで、この変化において重要な役割を果たしています。Skal Europe Organizationのデータによれば、2025年までにドイツ消費者の22%、イタリア消費者の28%が持続可能な方法で生産された食品に対してプレミアム価格を支払うと予測されています。この需要拡大を受け、主要協同組合は垂直統合戦略の採用を加速させています。協同組合は農家との長期パートナーシップを通じ有機牛乳の安定供給を確保し、市場における一貫したプレミアムポジショニングを維持しています。有機製品のプレミアム価格は通常、従来型乳製品価格の20~30%上回ります。有機サプライチェーン内で事業規模を拡大できる加工業者にとって、このプレミアムは持続可能な利益率拡大の重要な機会となり、有機乳製品セグメントの経済的持続可能性を強化しています。

ミニパックや携帯用サイズなど、製品形態の革新

欧州の消費者は、信頼できる乳製品原料を用いた贅沢な体験を求めることで、乳製品デザートカテゴリーの成長を牽引しています。これに対し乳業メーカーは、フルーツ入りヨーグルト、塩キャラメルカスタード、抹茶クリームデザートなど、伝統的要素と現代的な工夫を融合させた製品開発で応えています。サフランやバニラといった多様な風味プロファイル、ティラミスやスペキュロスといった地域特産品を探求することで、消費拡大と幅広い年齢層の獲得を図っています。この進化は、健康志向から感情的な満足感とプレミアム体験を重視する戦略的転換を反映しており、アイスクリーム、チーズケーキ、冷凍デザートがこのカテゴリーの成長を牽引しています。また、伝統的な乳製品メーカーが菓子類メーカーと提携し、乳製品の栄養価と贅沢な味わいを融合させたハイブリッド製品を開発するなど、カテゴリーを超えたイノベーションもこの分野を活性化させています。2024年には、ラクタリスとネスレの合弁会社が「ピアチェーレ・ディ・ヨーグルト」を発表。ミルククリームを配合することで滑らかな食感を実現し、ヨーグルトを贅沢なセグメントに位置付けました。さらに、外食産業の回復もカテゴリー成長を支えています。レストランやカフェでは、顧客満足度を高め平均取引額を増加させる高利益率メニューとして、プレミアム乳製品デザートを重視する傾向が強まっています。

EUにおける生乳価格の高騰

欧州連合(EU)全域における生乳価格の上昇は、乳製品バリューチェーン全体に大きなマージン圧力をもたらしており、加工業者はコスト転嫁と消費者価格感応度のバランスを取ることを迫られています。欧州の乳価上昇は、乳生産量の減少が要因です。米国農務省(USDA)の予測によれば、EUの乳生産量は2024年の1億4,960万トンから2025年には1億4,940万トンへとわずかに減少する見込みです。欧州委員会市場観測所によれば、飼料費の上昇、エネルギーコストの高騰、気候変動による乳牛へのストレスが乳量減少を招いていることが要因となり、牛乳価格は依然として歴史的平均を上回っています。このコスト圧迫は、特にコモディティ乳製品の加工業者にとって困難な状況です。価格弾力性の制約によりコスト上昇分の転嫁が難しく、利益率の圧縮や、消費者価格への耐性が高いプレミアムセグメントへの市場シェアシフトの可能性が生じています。こうした状況を受け、大手加工業者は長期契約や協同組合所有構造を通じて乳原料の安定供給を確保し、コスト予測可能性を高める垂直統合への戦略的動きが進んでいます。一方、中小規模の加工業者は、有利な乳価交渉やコスト調整期の一時的な利益率圧縮を吸収する規模に欠けるため、リスクが高まっています。

セグメント分析

2025年時点で欧州乳製品市場におけるチーズの割合は34.78%を占めており、同地域の長いチーズ製造の伝統と高度な加工技術が、世界の輸出競争力を高めていることを示しています。欧州のチーズ分野における主導的地位は、多様なチーズ品種と原産地呼称保護制度による認証によってさらに支えられており、国際市場でのプレミアム価格設定を可能にしております。これは特にパルミジャーノ・レッジャーノや熟成ゴーダといった特産チーズにおいて顕著です。乳製品デザートは最も成長が速いカテゴリーであり、2031年までにCAGR4.48%が見込まれています。この成長は、プレミアム化の動向と、乳製品と菓子類の境界を曖昧にする革新的な形態によって牽引されています。バター生産は、健康志向の消費者嗜好や植物由来代替品との競合による課題に直面している一方、ヨーグルトはプロバイオティクス技術革新と機能性訴求に支えられ、着実な成長を続けています。

乳製品は多様な動向を示しています。植物性代替品の台頭により生乳の消費量は減少する一方、UHT牛乳やフレーバーミルクは利便性と長期保存性から需要を伸ばしています。クリーム製品はプレミアム価格を実現していますが、生乳供給量の制約や外食産業における植物性代替品との競合により、販売数量には限界があります。この製品構成の変化は、消費者がより豊かな味わいと機能性を求める傾向を反映しています。その結果、従来型のコモディティ乳製品は、付加価値の高いカテゴリーに市場シェアを奪われつつあります。これらのカテゴリーは、より優れた体験や健康効果を提供することでプレミアム価格を正当化しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 有機・自然派乳製品に対する消費者需要の高まり

- ミニパックや携帯用サイズなど、製品形態におけるイノベーション

- 乳製品デザートや贅沢な乳製品ベースのスナックへの消費者志向の高まり

- 付加価値のある機能性乳製品への需要増加

- カーボンニュートラル乳認証がプレミアム棚スペースを開拓

- 欧州産チーズに対する堅調な輸出需要

- 市場抑制要因

- EUにおける生乳価格の高騰

- 伝統的な液体乳製品の消費減少

- スコープ3の脱炭素化コストが畜群の合理化を促進

- 北欧における家畜由来炭素税の導入動向

- 消費者行動分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額ベース/数量ベース)

- 製品タイプ別

- バター

- チーズ

- ナチュラルチーズ

- チェダー

- カッテージ

- リコッタ

- パルメザン

- その他

- プロセスチーズ

- ナチュラルチーズ

- クリーム

- 生クリーム

- クッキングクリーム

- ホイップクリーム

- その他(クロッテッドクリーム、サワークリーム)

- 乳製品デザート

- アイスクリーム

- チーズケーキ

- 冷凍デザート

- その他(プリン・デザート類、トリフル、フール)

- 牛乳

- 加糖練乳

- フレーバーミルク

- 生乳

- UHTミルク(超高温殺菌乳)

- 粉ミルク

- ヨーグルト

- ドリンカブル

- スプーナブル

- サワーミルク飲料

- 流通チャネル別

- オントレード

- オフトレード

- コンビニエンスストア

- 専門店

- スーパーマーケットおよびハイパーマーケット

- オンライン小売

- その他(倉庫型会員制店、ガソリンスタンドなど)

- 国別

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- スウェーデン

- ベルギー

- ポーランド

- オランダ

- その他欧州地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Lactalis Group

- Nestle SA

- Danone SA

- Arla Foods Amba

- Royal FrieslandCampina

- Muller Group

- Savencia Fromage and Dairy

- Sodiaal

- DMK Group

- Valio

- Emmi

- Hochland

- Meggle

- Froneri

- Glanbia Plc

- Hochland Group

- Zott SE and Co. KG

- Arla Foods Cooperative

- Tirol Milch

- Unilever PLC