アジア太平洋のポリカーボネート(PC)-市場シェア分析、産業動向、成長予測(2024年~2029年)

Asia-Pacific Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 183 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693836

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

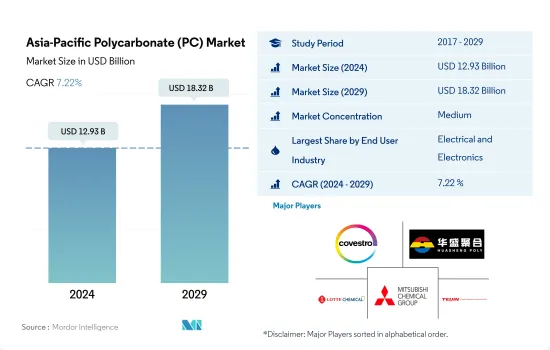

アジア太平洋のポリカーボネート(PC)市場規模は2024年に129億3,000万米ドルと推定され、2029年には183億2,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは7.22%で成長する見込みです。

優位性を維持する電気・電子産業

- ポリカーボネートは汎用性と耐久性に優れているため、さまざまな産業で広く利用されています。冷蔵庫、農業用ハウス、工業用・公共用建築物、ファサード、手術器具、ドラッグデリバリーシステム、血液透析膜、血液リザーバー、血液フィルターなどに応用されています。この地域では電気・電子産業がポリカーボネートの最大の消費者であり、2022年の市場シェアの45%以上を占めています。

- 2017~2019年にかけて、ポリカーボネート需要は着実な成長を遂げ、前年比成長率はそれぞれ5.14%、3.53%でした。この成長を牽引したのは、主にエレクトロニクス産業における生産の増加です。

- 2020年には、COVID-19パンデミックにより操業、旅行、貿易が制限され、ポリカーボネート需要は前年比3.71%減少しました。特に影響を受けたのは自動車産業と産業機械産業で、2019年の数量はそれぞれ12.52%と16.65%減少しました。しかし、規制が緩和されるにつれて、ポリカーボネートの需要は徐々に回復し、中国とインドが成長を牽引する重要な役割を果たしました。

- 従来のアクリルやガラスをポリカーボネートで代用する動向の高まりが、予測期間中の同材料の需要を牽引すると予想されます。アジア太平洋のすべてのエンドユーザー産業の中で、インドの電気・電子産業が最も高い成長を遂げると予測されており、予測期間中の数量ベースでのCAGRは7.63%です。全体として、この地域のポリカーボネート需要は、予測期間を通じて数量ベースでCAGR 5.66%、金額ベースでCAGR 7.22%を記録すると予想されます。

中国は数量でも金額でも優位を保つ

- アジア太平洋は世界最大のポリカーボネート消費国で、2022年には63.07%以上のシェアを占めます。アジア太平洋では、ポリカーボネートは電気・電子、自動車、航空宇宙部品製造、医療機器製造産業で様々な用途が見出されています。

- 2017~2019年にかけて、ポリカーボネートの需要は、主に中国やインドのような国々におけるプラスチック包装産業の急成長によって、着実な成長を示しました。2020年には、パンデミック時の操業・貿易制限による労働者の不足や原料不足など、様々な抑制要因が様々なエンドユーザー産業に深刻な影響を及ぼし、それによって同地域のポリカーボネート需要にマイナスの影響を与えました。中でもオーストラリアのポリカーボネート需要は大きな影響を受けました。2020年の同国の需要量は前年比40.96%減少したが、地域による前年比減少率は3.71%でした。

- 2021年には、規制が緩和され、ポリカーボネート需要は大流行前の水準まで回復しました。この成長の主要原動力となったのは、インドなどにおける産業活動の急成長です。この成長傾向は予測期間を通じて続くと予想され、ポリカーボネート需要の伸びはインドがすべての国の中で最も高いです。全体として、アジア太平洋のポリカーボネート需要は予測期間中にCAGR 5.60%(数量ベース)を記録すると予想されます。

アジア太平洋のポリカーボネート(PC)市場動向

ASEAN諸国の急成長がエレクトロニクス生産を促進

- アジア太平洋では、2020~2021年にかけて電気・電子機器の生産収入が13.9%増加しました。エレクトロニクスセグメントは、ほとんどのアジア諸国の輸出総額の20~50%を占めています。テレビ、ラジオ、コンピューター、携帯電話などの民生用電子機器製品の大部分はASEAN地域で生産されています。

- ASEANはハードディスクドライブの生産をリードしており、ハードディスクドライブの80%以上がASEAN域内で生産されています。全体として、ASEANの電気・電子(E& E)産業は、他の産業よりも外国からの投入物や技術に依存しており、E& E輸出の53%は、ASEANのE& E輸出に組み込まれた外国付加価値(FVA)または外国からの投入物によるものです。

- タイやマレーシアのような国々は、域内のエレクトロニクス生産をリードしています。東南アジア最大級の電子機器組立基地を有するタイは、ハードドライブ、集積回路、半導体の生産でリードしています。エアコン製造では第2位、世界の冷蔵庫市場では第4位です。

- エレクトロニクス産業は、中国や日本のようなアジアの経済大国との貿易改善を促進するASEANの統合生産ネットワークから大きな恩恵を受けています。

- 中国は電気製品の世界輸出で11.2%のシェアを占め、2019~2020年にかけてデジタル製品の輸出で5.8%の成長を記録しました。アジア開発銀行によると、中国はこの地域の電子機器に大きな市場を提供しています。タイ、日本、中国、マレーシア、インド、フィリピンなどの国々は、エレクトロニクスの生産で引き続きこの地域をリードしています。

アジア太平洋のポリカーボネート(PC)産業概要

アジア太平洋のポリカーボネート(PC)市場は適度に統合されており、上位5社で59.21%を占めています。この市場の主要企業は、Covestro AG、Hainan Huasheng New Material Technology、Lotte Chemical、Mitsubishi Chemical Corporation、Teijin Limitedなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 包装

- 輸出入動向

- ポリカーボネート(PC)貿易

- 価格動向

- 形態動向

- リサイクル概要

- ポリカーボネート(PC)のリサイクル動向

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- マレーシア

- 韓国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 工業・機械

- 包装

- その他

- 国名

- オーストラリア

- 中国

- インド

- 日本

- マレーシア

- 韓国

- その他のアジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- CHIMEI

- Covestro AG

- Formosa Plastics Group

- Hainan Huasheng New Material Technology Co., Ltd.

- LG Chem

- Lotte Chemical

- Mitsubishi Chemical Corporation

- Sinochem

- Sinopec SABIC Tianjin Petrochemical Company(SSTPC)

- Teijin Limited

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

The Asia-Pacific Polycarbonate (PC) Market size is estimated at 12.93 billion USD in 2024, and is expected to reach 18.32 billion USD by 2029, growing at a CAGR of 7.22% during the forecast period (2024-2029).

Electrical and electronics industry to maintain its dominance

- Polycarbonates are widely utilized in various industries due to their versatile and durable nature. They find applications in refrigerators, agricultural houses, industrial and public buildings, facades, surgical instruments, drug delivery systems, hemodialysis membranes, blood reservoirs, and blood filters. The electrical and electronics industry has been the largest consumer of polycarbonate in the region, and it accounted for over 45% of the market share in 2022.

- Between 2017 and 2019, polycarbonate demand experienced steady growth, with Y-o-Y rates of 5.14% and 3.53%, respectively. The increasing production in the electronics industry primarily drove this growth.

- In 2020, the COVID-19 pandemic led to operational, travel, and trade restrictions, resulting in a decline in the demand for polycarbonates by 3.71% compared to the previous year. The automotive and industrial machinery industries were particularly affected, experiencing declines of 12.52% and 16.65% in their 2019 volumes, respectively. However, as the restrictions eased, the demand for polycarbonates gradually recovered, with China and India playing a significant role in driving the growth.

- The growing trend of substituting traditional acrylics and glass with polycarbonates is expected to drive the demand for the material in the forecast period. Among all end-user industries in the Asia-Pacific region, the electrical and electronics industry in India is projected to witness the highest growth, with a CAGR of 7.63% in terms of volume during the forecast period. Overall, the regional demand for polycarbonates is expected to record a CAGR of 5.66% in volume terms and 7.22% in value terms throughout the forecast period.

China to maintain its dominance both in terms of volume and value

- The Asia-Pacific region is the largest consumer of polycarbonates globally, occupying a share of over 63.07% in 2022. In the Asia-Pacific region, polycarbonates find various applications in the electrical and electronics, automotive, aerospace components manufacturing, and healthcare devices manufacturing industries.

- During 2017-2019, the demand for polycarbonates witnessed steady growth, mainly driven by the rapid growth in the plastic packaging industry in countries like China and India. In 2020, various restraining factors, like worker unavailability and raw material shortages caused by operational and trade restrictions during the pandemic, severely affected various end-user industries, thereby negatively affecting the polycarbonate demand in the region. Among all countries, the polycarbonate demand in Australia was affected severely. In 2020, the country's Y-o-Y demand volume declined by 40.96%, whereas the regional Y-o-Y decline was 3.71%.

- In 2021, as the restrictions eased, the polycarbonate demand rose back to its pre-pandemic level. This growth was majorly driven by the rapid growth in industrial activities in countries like India. This growth trend is expected to continue throughout the forecast period, with India witnessing the highest growth in polycarbonate demand among all countries. Overall, the polycarbonate demand in the Asia-Pacific region is expected to record a CAGR of 5.60% (in volume) during the forecast period.

Asia-Pacific Polycarbonate (PC) Market Trends

Rapid growth in ASEAN countries to foster electronics production

- The Asia-Pacific region saw an increase in electrical and electronics production revenue by 13.9% from 2020 to 2021. The electronics sector accounts for 20-50% of the total value of most Asian countries' exports. Consumer electronics such as televisions, radios, computers, and cellular phones are largely manufactured in the ASEAN region.

- ASEAN leads the production of hard drives, with over 80% of hard drives being manufactured in the region. Overall, the electrical and electronics (E&E) industry in ASEAN relies more on foreign inputs and technology than other industries, with 53% of E&E exports arising from foreign value added (FVA) or foreign inputs integrated into ASEAN's E&E exports.

- Countries like Thailand and Malaysia lead in the production of electronics in the region. Thailand, home to one of the largest electronics assembly bases in Southeast Asia, leads in the production of hard drives, integrated circuits, and semiconductors. It ranks second in manufacturing air conditioning units and fourth in the global refrigerators market.

- The electronics industry has greatly benefitted from ASEAN's integrated production networks, which foster improved trade with larger Asian economies like China and Japan.

- China held an 11.2% share of global exports in electrical products and registered a growth of 5.8% in the export of digital products from 2019 to 2020. According to the Asian Development Bank, China provides a large market for electronics in the region. Countries such as Thailand, Japan, China, Malaysia, India, and the Philippines continue to lead the region in the production of electronics.

Asia-Pacific Polycarbonate (PC) Industry Overview

The Asia-Pacific Polycarbonate (PC) Market is moderately consolidated, with the top five companies occupying 59.21%. The major players in this market are Covestro AG, Hainan Huasheng New Material Technology Co., Ltd., Lotte Chemical, Mitsubishi Chemical Corporation and Teijin Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polycarbonate (PC) Trade

- 4.3 Price Trends

- 4.4 Form Trends

- 4.5 Recycling Overview

- 4.5.1 Polycarbonate (PC) Recycling Trends

- 4.6 Regulatory Framework

- 4.6.1 Australia

- 4.6.2 China

- 4.6.3 India

- 4.6.4 Japan

- 4.6.5 Malaysia

- 4.6.6 South Korea

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Country

- 5.2.1 Australia

- 5.2.2 China

- 5.2.3 India

- 5.2.4 Japan

- 5.2.5 Malaysia

- 5.2.6 South Korea

- 5.2.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 CHIMEI

- 6.4.2 Covestro AG

- 6.4.3 Formosa Plastics Group

- 6.4.4 Hainan Huasheng New Material Technology Co., Ltd.

- 6.4.5 LG Chem

- 6.4.6 Lotte Chemical

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 Sinochem

- 6.4.9 Sinopec SABIC Tianjin Petrochemical Company (SSTPC)

- 6.4.10 Teijin Limited

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 183 Pages

- 納期

- 2~3営業日