北米のポリカーボネート(PC):市場シェア分析、産業動向、成長予測(2024~2029年)

North America Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693834

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

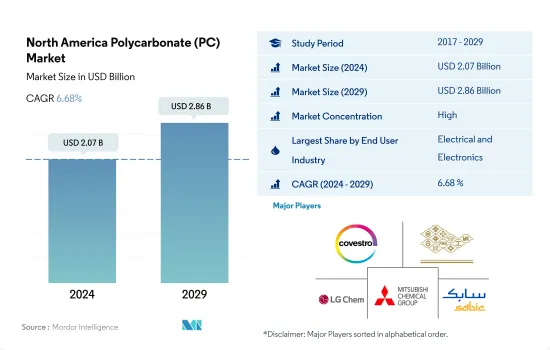

北米のポリカーボネート(PC)市場規模は2024年に20億7,000万米ドルと推定され、2029年には28億6,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは6.68%で成長する見込みです。

ポリカーボネート製造の技術進歩が市場需要を押し上げる

- ポリカーボネートは、その高い衝撃強度、軽量性、耐紫外線性、光学トランスミッション、電気特性、その他多くの特性により、この地域で人気があります。ポリカーボネートシートの衝撃強度は一般的なガラスの200倍。ポリカーボネートは、ガラスと同じ90%の光を透過することができます。同地域のポリカーボネート需要は、2023年には2022年比で金額ベースで7.93%の成長が見込まれています。

- 有毒なビスフェノール(BPA)の代わりに炭酸ガス(CO2)を原料とするポリカーボネートの新しい生産技術の動向の高まりが、近年の市場を牽引しています。

- 同地域のポリカーボネート市場は、2020年に金額ベースで2019年比7.8%減少しました。同時期のCOVID-19パンデミックにより、米国、メキシコ、カナダなど数カ国で全国的な操業停止が発生し、生産設備が3ヶ月近く停止しました。サプライチェーンの混乱、原料不足、地域全体の貿易交流の停止がこのような落ち込みをもたらしました。しかし、2021年には、生産設備の年間生産能力への再開により、需要は2020年比18.24%の成長率で回復しました。

- ポリカーボネートは北米の電気・電子産業で様々な用途に広く使用されています。北米におけるポリカーボネート樹脂の消費量は約12万6,000トンです。民生用電子機器製品における高強度・軽量材料の動向の高まりが、北米におけるポリカーボネート樹脂の需要を牽引すると予想されます。電気・電子産業は北米で最も急成長しているエンドユーザー産業であり、2023~2029年の予測期間中に金額ベースでCAGR 8.29%を記録すると予想されます。

米国が北米のポリカーボネート市場を独占、建設活動の活発化とエレクトロニクス医療産業の成長による

- 2022年のポリカーボネート樹脂の世界消費量に占める北米の割合は金額ベースで10.2%。ポリカーボネートは北米において、自動車、建築・建設、電気・電子、医療など様々な産業で重要なポリマーです。

- 米国は建設、電気・電子、医療産業の成長により、国別では北米地域で最大のポリカーボネート樹脂消費国です。ポリカーボネートの最大のエンドユーザー産業の一つである同国の建設産業は、2022年に7万6,000トン近い消費量を占めました。新設床面積は2022年の58億平方メートルから2029年には74億平方メートルに達すると予想されています。成長する建設産業におけるポリカーボネート樹脂の需要は、予測期間中(2023~2029年)に金額ベースでCAGR 6.46%を記録すると予想されます。

- メキシコでは、自動車生産とエレクトロニクス産業などの成長により、ポリカーボネート樹脂の需要が大幅に増加しています。メキシコは北米第2位の自動車生産国です。2022年の生産台数は378万台で、2021年比で7.67%増加しました。同国の民生用電子機器産業も成長しており、2027年には220億米ドルに達すると予想されています。これらの要因が、予測期間中のメキシコにおけるポリカーボネート樹脂の需要を促進すると予想されます。

- また、既存の材料と同様の強度を持ち、軽量であることから、先端材料の使用も増加しています。こうした動向は、予測期間中、北米のポリカーボネート需要を牽引するとみられます。ポリカーボネートはガラスに比べて6倍軽く、2倍安いため、多くの用途で広くガラスに取って代わりつつあります。

北米のポリカーボネート(PC)市場動向

技術革新の力強い成長が産業全体の成長を後押し

- 北米の電気・電子機器生産は、スマートテレビ、冷蔵庫、エアコンなどの民生用電子機器製品需要の増加と技術の進歩が相まって、2017~2019年にかけて1.4%以上のCAGRを記録しました。電子技術革新の急速なペースは、より新しくより高速な電子製品への需要を促進しています。その結果、この地域の電気・電子機器生産も増加しています。

- 北米の電子機器売上高は、生産施設の操業停止、サプライチェーンの混乱、その他様々な制約のため、COVID-19の影響により、2020年には2019年比で約9%減少しました。その結果、同地域の電気・電子機器生産による収益は2020年に前年比4.7%減少しました。

- 2021年には、同地域の消費者向け電子機器の売上高は約1,130億米ドルに達し、2020年より4%増加しました。その結果、北米の電気・電子機器生産は2021年に前年比13.8%増となりました。

- 2027年には、北米は電気・電子機器生産で第3位の地域となり、世界市場の約10.5%のシェアを占めると予測されています。効率性と低コストを実現するために、仮想現実、IoTソリューション、ロボット工学などの先進技術が民生用電子機器製品に登場したことが、民生用電子機器産業に大きなメリットをもたらしています。同地域の民生用電子機器産業は、2023年の1,276億米ドルから2027年には約1,618億米ドルの市場規模に達すると予測されています。その結果、同地域の電気・電子製品の需要は増加すると予測されます。

北米のポリカーボネート(PC)産業概要

北米のポリカーボネート(PC)市場はかなり統合されており、上位5社が100%を占めています。この市場の主要企業は、Covestro AG、Formosa Plastics Group、LG Chem、Mitsubishi Chemical Corporation、SABICなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 包装

- 輸出入動向

- ポリカーボネート(PC)貿易

- 価格動向

- 形態動向

- リサイクル概要

- ポリカーボネート(PC)のリサイクル動向

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 工業・機械

- 包装

- その他

- 国名

- カナダ

- メキシコ

- 米国

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- CHIMEI

- Covestro AG

- Formosa Plastics Group

- LG Chem

- Lotte Chemical

- Luxi Group

- Mitsubishi Chemical Corporation

- SABIC

- Teijin Limited

- Trinseo

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 5000172

The North America Polycarbonate (PC) Market size is estimated at 2.07 billion USD in 2024, and is expected to reach 2.86 billion USD by 2029, growing at a CAGR of 6.68% during the forecast period (2024-2029).

Technological advancements in the manufacturing of polycarbonate to boost market demand

- Polycarbonate is popular in the region for its high impact strength, lightweight, UV resistance, optical transmission, electrical, and many other properties. The impact strength of the polycarbonate sheet is 200 times more than common glass. Polycarbonate can transmit 90% of light through it, the same as glass. The demand for polycarbonate in the region is expected to grow by 7.93%, by value, in 2023 compared to 2022.

- The rising trend of new production technology of polycarbonate from carbon dioxide gas (CO2) instead of bisphenol (BPA), which is toxic in nature, has driven the market over recent years.

- The polycarbonate market in the region declined by 7.8% in terms of value in 2020 compared to 2019. The COVID-19 pandemic during the same period halted production facilities for nearly three months because of nationwide lockdowns in several countries, including the United States, Mexico, and Canada. The supply chain disruptions, raw material shortages, and stoppage of trade exchanges across the region resulted in such a decline. However, the demand regained in 2021 with a growth rate of 18.24% compared to 2020, owing to the resumption of production facilities to its annual capacity output.

- Polycarbonate is widely used in the electrical and electronics industry for various applications in North America. The industry consumed nearly 126 thousand tons of polycarbonate resin in North America. The rising trend of high-strength and lightweight material in consumer electronics is expected to drive the demand for polycarbonate resins in North America. The electrical and electronics industry is expected to be the fastest-growing end-user industry in North America, registering a CAGR of 8.29%, by value, during the forecast period, 2023-2029.

The United States to dominate the North American polycarbonate market owing to rising construction activities and growth in the electronics and medical industries

- North America accounted for 10.2% by value of the global consumption of polycarbonate resins in 2022. Polycarbonate is a key polymer in North America for various industries, including automotive, building and construction, electrical and electronics, and medical.

- The United States is the largest country-wise consumer of polycarbonate resin in the North American region, owing to growth in its construction, electrical and electronics, and medical industries. The country's construction industry, one of the largest end-user industries of polycarbonate, accounted for consumption of nearly 76,000 tons in 2022. The new floor area is expected to reach 7.4 billion square footage by 2029 from 5.8 billion square footage in 2022. The demand for polycarbonate resin in the growing construction industry is expected to register a CAGR of 6.46% by value during the forecast period (2023-2029).

- The demand for polycarbonate resin is increasing significantly in Mexico owing to growth in vehicle production and electronics, among other industries. Mexico is the second-largest vehicle producer in North America. It produced 3.78 million units in 2022, a 7.67% increase over 2021. The country's consumer electronics industry is also growing, expected to reach USD 22 billion by 2027. These factors are expected to drive the demand for polycarbonate resins in Mexico during the forecast period.

- The use of advanced materials is also growing, as they provide strength similar to existing ones and are lightweight. Such trends are expected to drive the demand for polycarbonate in North America over the forecast period. Polycarbonate is widely replacing glass in many applications because it is six times lighter and two times cheaper than glass.

North America Polycarbonate (PC) Market Trends

Strong growth of technological innovations to augment the overall growth of the industry

- Electrical and electronics production in North America witnessed a CAGR of over 1.4% between 2017 and 2019 owing to the advancement of technology, coupled with the increasing demand for consumer electronics products, such as smart TVs, refrigerators, air conditioners, and other products. The rapid pace of electronic technological innovation is driving the demand for newer and faster electronic products. As a result, it has also increased the electrical and electronics production in the region.

- Electronic device sales in North America fell by around 9% in 2020 compared to 2019, owing to the COVID-19 impact, because of the production facility shutdowns, supply chain disruptions, and various other constraints. As a result, revenue from electrical and electronics production in the region decreased by 4.7% in 2020 compared to the previous year.

- In 2021, the sales of consumer electronics in the region reached around USD 113 billion, 4% higher than in 2020. As a result, North America's electrical and electronics production grew by 13.8% in 2021 in terms of revenue compared to the previous year.

- By 2027, North America is projected to be the third-largest region for electrical and electronics production and account for a share of around 10.5% of the global market. The emergence of advanced technologies such as virtual reality, IoT solutions, and robotics into consumer electronic products to achieve efficiency and low cost has provided a significant advantage to the consumer electronics industry. The consumer electronics industry in the region is projected to reach a market volume of around USD 161.8 billion by 2027 from USD 127.6 billion in 2023. As a result, the demand for electrical and electronic products in the region is projected to increase.

North America Polycarbonate (PC) Industry Overview

The North America Polycarbonate (PC) Market is fairly consolidated, with the top five companies occupying 100%. The major players in this market are Covestro AG, Formosa Plastics Group, LG Chem, Mitsubishi Chemical Corporation and SABIC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polycarbonate (PC) Trade

- 4.3 Price Trends

- 4.4 Form Trends

- 4.5 Recycling Overview

- 4.5.1 Polycarbonate (PC) Recycling Trends

- 4.6 Regulatory Framework

- 4.6.1 Canada

- 4.6.2 Mexico

- 4.6.3 United States

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Country

- 5.2.1 Canada

- 5.2.2 Mexico

- 5.2.3 United States

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 CHIMEI

- 6.4.2 Covestro AG

- 6.4.3 Formosa Plastics Group

- 6.4.4 LG Chem

- 6.4.5 Lotte Chemical

- 6.4.6 Luxi Group

- 6.4.7 Mitsubishi Chemical Corporation

- 6.4.8 SABIC

- 6.4.9 Teijin Limited

- 6.4.10 Trinseo

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

北米のポリカーボネート(PC):市場シェア分析、産業動向、成長予測(2024~2029年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日