欧州のポリカーボネート(PC):市場シェア分析、産業動向、成長予測(2024年~2029年)

Europe Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 178 Pages

- 納期

- 2~3営業日

- 商品コード

- 1693835

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

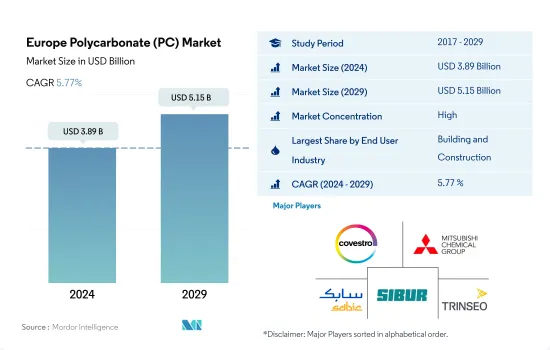

欧州のポリカーボネート(PC)市場規模は2024年に38億9,000万米ドルと推定され、2029年には51億5,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは5.77%で成長する見込みです。

今後の建設プロジェクトがポリカーボネート需要を押し上げる

- ポリカーボネート(PC)は、その高い衝撃強度、軽量性、耐紫外線性、光学伝送により、コンパクトディスク、防弾ガラス、自動車ヘッドランプレンズ、屋根材、グレージングなど様々な用途に使用されています。2022年、欧州のポリカーボネート(PC)市場は、金額ベースで世界のポリカーボネート(PC)市場の19%を占めました。

- 2020年、COVID-19パンデミックのため、PC市場は2019年と比較して金額ベースで10.41%減少しました。サプライチェーンの混乱、原料不足、地域全体の貿易交流の停止が原因です。生産設備の再開により、2021年のPC樹脂需要は2020年に比べ金額ベースで19.22%増加しました。

- 自動車と建築・建設がこの地域のPC樹脂の最大消費者です。同地域の新築床面積は、2023年の78億平方フィートから2029年には95億平方フィートに達すると予想されます。同地域の自動車生産台数は、2023年の1,830万台から2029年には2,070万台に達すると予測されます。この地域の建設と自動車生産の増加は、今後数年間PC樹脂の需要を牽引すると予測されます。

- 航空宇宙は、この地域でPC樹脂のエンドユーザー産業として最も急成長しており、予測期間中のCAGRは金額ベースで7.38%と予測されます。航空宇宙産業における高強度・軽量材料の動向の高まりが、この地域におけるPC樹脂の需要を牽引すると予想されます。同地域の航空機部品生産収入は、2023年の2,432億米ドルから2029年には3,488億米ドルに達すると予測されています。同地域における航空宇宙部品の生産拡大が、PC樹脂の需要を牽引すると予測されます。

自動車生産がこの地域のポリカーボネートの成長を押し上げる可能性

- 2022年のポリカーボネート樹脂の世界消費量は、欧州が19%(数量ベース)を占めます。ポリカーボネートはフランスやドイツなどの欧州諸国で、自動車、航空宇宙、電気・電子などさまざまな産業で使用されています。ドイツ、ロシア、イタリアなどの国々が、この地域におけるポリカーボネート樹脂の主要消費国です。

- ドイツは、航空宇宙産業、自動車産業、電気・電子産業が成長しているため、この地域で最大のポリカーボネート消費国です。航空機部品と自動車生産は、2021年に地域レベルで売上高で約16.9%、数量で20.19%のシェアを占め、ポリカーボネート樹脂の需要を牽引しています。自動車と電気・電子機器生産の増加は、ポリカーボネート樹脂の需要を牽引すると予想されます。

- イタリアにおけるポリカーボネート樹脂の需要は、自動車産業と電気・電子産業における生産の増加により大幅に増加しています。イタリアは欧州連合(EU)第5位の自動車生産国です。2022年の生産台数は108万台で、同地域の6.13%(台数ベース)を占めています。同国の電気・電子産業も拡大しており、2023年には171億5,000万米ドルの収益が見込まれます。これらの要因が、予測期間中の欧州におけるポリカーボネート樹脂の需要を牽引すると予想されます。

- ポリカーボネート樹脂の消費国としては英国が最も急成長しており、予測期間(2023~2029年)の売上高によるCAGRは6.19%となる見込みです。同地域で最も高いCAGR 3.4%(数量ベース)を示す自動車生産の伸びが、同国のPC樹脂需要を牽引すると予想されます。

欧州のポリカーボネート(PC)市場動向

技術革新が民生用電子機器市場を後押し

- 欧州の電気・電子機器生産は、2017~2021年にかけて3.8%以上のCAGRを記録しました。電子技術革新の急速なペースが、より新しく高速な電気・電子製品に対する一貫した需要を促進しています。その結果、この地域の電気・電子機器生産の需要も増加しています。

- リモートワークや遠隔学習によりコンピューターやノートパソコンの需要が増加しているにもかかわらず、欧州の消費者向け電子機器セグメントのユーザー1人当たりの平均売上高は6.3%減少しました。2020年の売上高は約2,521億米ドルでした。その結果、2020年の同地域の電気・電子機器生産は、前年比2.8%減となりました。

- 2021年には、欧州の電気・電子機器輸出は約2,283億7,000万米ドルとなり、2020年と比較して12.4%増加しました。その結果、同地域の電気・電子機器生産は増加し、2021年には前年比11.6%を記録しました。

- ロボット工学、仮想現実と拡張現実、IoT(モノのインターネット)、5G接続は予測期間中に成長すると予想されます。技術の進歩の結果、民生用電子機器の需要は予測期間中に上昇すると予想されます。同地域のコンシューマーエレクトロニクスセグメントの売上は、2023年の1,211億米ドルから2027年には約1,572億米ドルに達すると予測されます。2027年までに、欧州は世界市場の約12.7%を占める第2位の電気・電子機器生産国になると予測されています。その結果、民生用電子機器の増加により、今後数年間は電気・電子機器生産の需要が増加すると予測されます。

欧州のポリカーボネート(PC)産業概要

欧州のポリカーボネート(PC)市場はかなり統合されており、上位5社が100%を占めています。この市場の主要企業は、Covestro AG、Mitsubishi Chemical Corporation、SABIC、SIBUR Holding PJSC、Trinseoなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 包装

- 輸出入動向

- ポリカーボネート(PC)貿易

- 価格動向

- 形態動向

- リサイクル概要

- ポリカーボネート(PC)のリサイクル動向

- 規制の枠組み

- EU

- フランス

- ドイツ

- イタリア

- ロシア

- 英国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 工業・機械

- 包装

- その他

- 国名

- フランス

- ドイツ

- イタリア

- ロシア

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- CHIMEI

- Covestro AG

- Formosa Plastics Group

- LG Chem

- Lotte Chemical

- Mitsubishi Chemical Corporation

- SABIC

- SIBUR Holding PJSC

- Teijin Limited

- Trinseo

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 5000173

The Europe Polycarbonate (PC) Market size is estimated at 3.89 billion USD in 2024, and is expected to reach 5.15 billion USD by 2029, growing at a CAGR of 5.77% during the forecast period (2024-2029).

Upcoming construction projects to boost polycarbonate demand

- Polycarbonate (PC) is used in various applications, such as compact discs, bullet-proof glasses, car headlamp lenses, roofing, and glazing, due to its high impact strength, lightweight property, UV resistance, and optical transmission. In 2022, the European polycarbonate (PC) market accounted for 19% of the global polycarbonate (PC) market in terms of value.

- In 2020, due to the COVID-19 pandemic, the PC market declined by 10.41% in terms of value compared to 2019, attributed to supply chain disruptions, raw material shortages, and the halting of trade exchanges throughout the region. With the resumption of production facilities, the demand for PC resin increased by 19.22% in terms of value in 2021 compared to 2020.

- Automotive and building and construction are the region's largest consumers of PC resin. The region's new construction floor area is expected to reach 9.5 billion sq. ft in 2029 from 7.8 billion sq. ft in 2023. Vehicle production in the region is projected to reach 20.7 million units in 2029 from 18.3 million units in 2023. The region's increasing construction and vehicle production is projected to drive the demand for PC resin over the coming years.

- Aerospace is the region's fastest-growing end-user industry for PC resin, with a projected CAGR of 7.38% in terms of value during the forecast period. The rising trend of high-strength and lightweight materials in the aerospace industry is expected to drive the demand for PC resin in the region. The region's aircraft component production revenue is projected to reach USD 348.8 billion in 2029 from USD 243.2 billion in 2023. The growing production of aerospace components in the region is projected to drive the demand for PC resin.

Automotive production may boost the growth of polycarbonate across the region

- Europe accounted for 19% (by volume) of the global consumption of polycarbonate resin in 2022. Polycarbonate is used in European countries, such as France and Germany, in various industries, including automotive, aerospace, and electrical and electronics. Countries such as Germany, Russia, and Italy are the leading consumers of polycarbonate resin in the region.

- Germany is the largest consumer of polycarbonate in the region due to its growing aerospace, automotive, and electrical and electronics industries. Aircraft components and vehicle production held a share of around 16.9% by revenue and 20.19% by volume in 2021 at the regional level, driving the demand for polycarbonate resin. The growing automotive and electrical and electronics production is expected to drive the demand for polycarbonate resin.

- The demand for polycarbonate resin in Italy is increasing significantly due to growing production in the automotive and electrical and electronics industries. Italy is the European Union's fifth-largest vehicle producer. In 2022, the country produced 1.08 million units, 6.13% (by volume) of the region. The country's electrical and electronics industry is also expanding, and the revenue is projected to amount to USD 17.15 billion in 2023. These factors are expected to drive the demand for polycarbonate resins in Europe during the forecast period.

- The United Kingdom is expected to be the fastest-growing consumer of polycarbonate resin, with a CAGR of 6.19% by revenue during the forecast period (2023-2029). The growth in vehicle production, with the highest CAGR of 3.4% (in volume) in the region, is expected to drive the demand for PC resin in the country.

Europe Polycarbonate (PC) Market Trends

Technological innovations to boost the consumer electronics market

- Europe's electrical and electronics production registered a CAGR of over 3.8% between 2017 and 2021. The rapid pace of electronic technological innovation is driving consistent demand for newer and faster electrical and electronic products. As a result, it has also increased the demand for electrical and electronics production in the region.

- Despite the increased demand for computers and laptops due to remote working and distance learning, the average revenue per user in the European consumer electronics segment dropped by 6.3%. It generated a revenue of around USD 252.1 billion in 2020. As a result, in 2020, the electrical and electronic production in the region decreased by 2.8% by revenue compared to the previous year.

- In 2021, Europe's electrical and electronic equipment exports were around USD 228.37 billion, 12.4% higher compared to 2020. As a result, electrical and electronic production in the region increased and registered 11.6% in 2021 compared to the previous year.

- Robotics, virtual reality and augmented reality, IoT (Internet of Things), and 5G connectivity are expected to grow during the forecast period. As a result of technological advancements, demand for consumer electronics is expected to rise during the forecast period. The consumer electronics segment in the region is projected to reach a revenue of around USD 157.2 billion in 2027 from USD 121.1 billion in 2023. By 2027, Europe is projected to be the second-largest electrical and electronics production accounting for around 12.7% of the global market. As a result, the rise in consumer electronics is projected to increase the demand for electrical and electronics production in the coming years.

Europe Polycarbonate (PC) Industry Overview

The Europe Polycarbonate (PC) Market is fairly consolidated, with the top five companies occupying 100%. The major players in this market are Covestro AG, Mitsubishi Chemical Corporation, SABIC, SIBUR Holding PJSC and Trinseo (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polycarbonate (PC) Trade

- 4.3 Price Trends

- 4.4 Form Trends

- 4.5 Recycling Overview

- 4.5.1 Polycarbonate (PC) Recycling Trends

- 4.6 Regulatory Framework

- 4.6.1 EU

- 4.6.2 France

- 4.6.3 Germany

- 4.6.4 Italy

- 4.6.5 Russia

- 4.6.6 United Kingdom

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Country

- 5.2.1 France

- 5.2.2 Germany

- 5.2.3 Italy

- 5.2.4 Russia

- 5.2.5 United Kingdom

- 5.2.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 CHIMEI

- 6.4.2 Covestro AG

- 6.4.3 Formosa Plastics Group

- 6.4.4 LG Chem

- 6.4.5 Lotte Chemical

- 6.4.6 Mitsubishi Chemical Corporation

- 6.4.7 SABIC

- 6.4.8 SIBUR Holding PJSC

- 6.4.9 Teijin Limited

- 6.4.10 Trinseo

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

欧州のポリカーボネート(PC):市場シェア分析、産業動向、成長予測(2024年~2029年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 178 Pages

- 納期

- 2~3営業日