|

市場調査レポート

商品コード

1693838

南米のポリカーボネート(PC)- 市場シェア分析、産業動向、成長予測(2024~2029)South America Polycarbonate (PC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米のポリカーボネート(PC)- 市場シェア分析、産業動向、成長予測(2024~2029) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 148 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

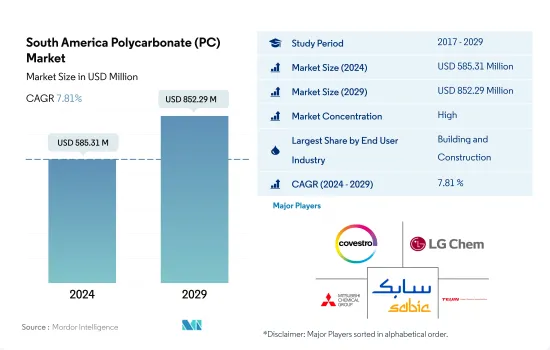

南米のポリカーボネート(PC)市場規模は2024年に5億8,531万米ドルと推定・予測され、2029年には8億5,229万米ドルに達し、予測期間中(2024~2029年)のCAGRは7.81%で成長すると予測されます。

急速な技術進歩がポリカーボネートの需要を拡大

- ポリカーボネートは熱可塑性ポリマーの一種で、強靭で、グレードによっては光学的に透明です。成形、成型、熱成形が容易です。同地域のポリカーボネート需要は、2021年と比較して2022年には数量ベースで7.7%増加したが、これは主に生産高と製造活動の増加によるものです。

- 電気・電子産業が最大の消費者で、2022年の消費量全体の約17.38%を占めます。ポリカーボネートは、その電気抵抗と軽量特性により、冷蔵庫、エアコン、コーヒーメーカー、フードミキサー、洗濯機、ヘアドライヤー、スチームアイロン、水タンクなどの電子機器に広く使用されています。ポリカーボネートは、その特性を高めるために複合材料としても使用されています。また、電気・電子機器需要の急増と技術の進歩により、同地域で最も急成長している産業でもあります。この産業からのPC需要は、予測期間中に金額ベースでCAGR 8.41%を記録すると予測されています。

- 建築・建設産業はポリカーボネートの第2位の消費者で、2022年の総消費量の約13.33%を占めます。ポリカーボネートは、高い耐衝撃性と耐熱性、軽量性、耐久性、高い光学的透明性、優れた難燃性により、様々な用途に有用です。窓や天窓から壁パネルやルーフドーム、外部LED照明エレメントに至るまで、建築・建設製品に広く使用されています。予測期間中、同産業からのPC需要は数量ベースでCAGR 5.38%を記録する見込みです。

予測期間中、南米のポリカーボネート市場はブラジルが支配的

- 2022年のポリカーボネート(PC)樹脂の世界消費量に占める南米の割合は3.03%です。PCは南米では自動車、航空宇宙、電気・電子など様々な産業で重要なポリマーです。

- ブラジルは市場消費量において最大の国で、そのシェアは2022年には約40%に達し、航空宇宙、自動車、電気・電子産業の成長により2021年の7.33%から上昇します。2021年の市場シェアは、航空機部品が約96.2%、自動車が約67.9%でした。自動車産業と電気・電子産業におけるこのような生産拡大は、ポリカーボネート樹脂の需要を促進すると予想されます。

- アルゼンチンのPC樹脂需要は、自動車産業や電気・電子産業などの生産拡大に伴い大幅に増加しています。同国は南米第2位の自動車生産国で、2022年の生産台数は80万3,377台と、2021年比で9.01%増加しました。同国は南米で最も急成長しているPC樹脂の消費国となり、予測期間(2023~2029年)の売上高CAGRは8.19%となる見込みです。2029年には、自動車生産がこの地域市場規模ベースで5.12%のシェアを占めると予想され、これが予測期間中の同国におけるこの樹脂の需要を牽引すると期待されています。

- その他の南米の地域セグメントはPC樹脂の最大消費国の一つであり、チリ、ペルー、コロンビア、ボリビアなどの国々で構成されています。この地域セグメントは南米の建設活動のかなりのシェアを占めており、2022年には数量ベースで15.29%に達し、これが今後数年間のPC需要を促進すると予想されます。

南米のポリカーボネート(PC)市場動向

技術革新の急速なペースが産業の成長を後押し

- 南米では、ブラジルが2017年の同地域の電気・電子製品生産収益の約40%という大きなシェアを占めています。2017年、ブラジルのエレクトロニクス製品はeコマースセグメントで20%近い普及率を示しました。同地域における技術の進歩は、スマートテレビ、スマート冷蔵庫、スマートエアコン、その他の電気・電子製品などの民生用電子機器製品に対する需要を増加させました。南米の電気・電子製品の生産収入は、2017~2019年にかけて6.16%以上のCAGRを記録しました。

- 2020年、パンデミックによるリモートワークやホームエンターテイメント用の民生用電子機器製品の需要増加に伴い、同地域の電気・電子製品の生産は、前年比売上高成長率1.1%で増加しました。可処分所得の増加、高級品に対する需要の増加、技術の進歩、生活水準の向上は、電気・電子機器市場の成長を促す主要因のひとつです。その結果、同地域では、2021年の電気・電子機器生産も売上高で14.9%の割合で増加しました。

- 電子技術革新の急速なペースは、より新しく高速な電気・電子製品に対する一貫した需要を促進しています。その結果、同地域の電気・電子機器生産の需要も増加しています。LG、Samsung、Microsoft、Panasonic、Dell、Intel、Toshiba、Sony、Philips、Sharp、Apple、Lenovoといった多国籍企業の進出も、電気・電子機器市場にプラスの影響を与えています。このような要因はすべて、予測期間中に同地域の電気・電子機器の生産高を7%前後の割合で押し上げると予想されます。

南米のポリカーボネート(PC)産業概要

南米のポリカーボネート(PC)市場はかなり統合されており、上位5社で72.39%を占めています。この市場の主要企業は、Covestro AG、LG Chem、Mitsubishi Chemical Corporation、SABIC、Teijin Limitedなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 包装

- 輸出入動向

- ポリカーボネート(PC)貿易

- 価格動向

- 形態動向

- リサイクル概要

- ポリカーボネート(PC)のリサイクル動向

- 規制の枠組み

- アルゼンチン

- ブラジル

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 工業・機械

- 包装

- その他

- 国名

- アルゼンチン

- ブラジル

- その他の南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Covestro AG

- LG Chem

- Mitsubishi Chemical Corporation

- SABIC

- Teijin Limited

- Trinseo

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 5000176

The South America Polycarbonate (PC) Market size is estimated at 585.31 million USD in 2024, and is expected to reach 852.29 million USD by 2029, growing at a CAGR of 7.81% during the forecast period (2024-2029).

Fast-paced technological advancements to augment the demand for polycarbonates

- Polycarbonates are a class of thermoplastic polymers that are strong, tough, and, in some grades, optically transparent. They are easy to shape, mold, and thermoform. The demand for polycarbonates in the region increased by 7.7% in terms of volume in 2022 compared to 2021, majorly due to increased production output and manufacturing activities.

- The electrical and electronics industry is the largest consumer, accounting for approximately 17.38% of the overall consumption in 2022. Polycarbonates are widely used in electronic appliances such as refrigerators, air conditioners, coffee machines, food mixers, washing machines, hair dryers, steam iron, and water tanks, owing to their electrical resistance and lightweight properties. Polycarbonates are also used as a composite to enhance their properties. The industry is also the fastest growing in the region due to the rapid increase in the demand for electrical and electronic devices and technological advancements. The demand for PC from the industry is projected to register a CAGR of 8.41%, by value, during the forecast period.

- The building and construction industry is the second-largest consumer of polycarbonate, accounting for approximately 13.33% of the total consumption in 2022. Polycarbonate is useful in various applications due to its high impact and heat resistance, lightweight property, durability, high optical clarity, and excellent flammability resistance. It is widely used in building and construction products, ranging from windows and skylights to wall panels and roof domes and exterior LED lighting elements. During the forecast period, the demand for PC from the industry is expected to register a CAGR of 5.38% in volume terms.

Brazil to dominate the South American polycarbonate market over the forecast period

- South America accounted for 3.03% of the global consumption of polycarbonate (PC) resins in 2022. PC is an important polymer in South America for various industries, including automotive, aerospace, and electrical and electronics.

- Brazil is the largest country in terms of market consumption, with a share of around 40% in 2022, a rise from the 7.33% share registered in 2021 owing to its growth in its aerospace, automotive, and electrical and electronics industries. The country's production of aircraft components and vehicles accounted for market shares of around 96.2% and 67.9%, respectively, in 2021. Such production growth in the automotive and electrical and electronics industries is expected to drive the demand for polycarbonate resins.

- Argentina's demand for PC resins is increasing significantly in line with growing production in the automobile and electrical and electronics industries, among others. The country is the second-largest vehicle producer in South America, having produced 803,377 units in 2022, a 9.01% rise over 2021. The country is expected to be the fastest-growing consumer of PC resins in South America, with a CAGR of 8.19% by revenue during the forecast period (2023-2029). Vehicle production is expected to account for a 5.12% share of the regional market by volume by 2029, which is, in turn, expected to drive the demand for this resin in the country during the forecast period.

- The Rest of South America's regional segment is one of the largest consumers of PC resin and consists of countries such as Chile, Peru, Colombia, and Bolivia. The regional segment accounts for a considerable share of construction activity in South America, amounting to 15.29% by volume in 2022, which is expected to foster demand for PC over the coming years.

South America Polycarbonate (PC) Market Trends

Rapid pace of technological innovations to boost the industry growth

- In South America, Brazil held the major share of nearly 40% of the region's electrical and electronics production revenue in 2017. In 2017, Brazilian electronics products had a penetration of nearly 20% in the e-commerce sector. The advancement of technology in the region increased the demand for consumer electronics products, such as smart TVs, smart refrigerators, smart air conditioners, and other electrical and electronic products. South American electrical and electronics production revenue witnessed a CAGR of over 6.16% between 2017 and 2019.

- In 2020, with the rise in demand for consumer electronics for remote working and home entertainment due to the pandemic, the production of electrical and electronic products in the region increased at a growth rate of 1.1% by revenue compared to the previous year. Rising disposable income, increased demand for luxury products, technological advancements, and improvement in living standards are some of the major factors driving the electrical and electronics market's growth. As a result, in the region, electrical and electronics production also increased at a rate of 14.9% by revenue in 2021.

- The rapid pace of electronic technological innovation is driving consistent demand for newer and faster electrical and electronic products. As a result, it has also increased the demand for the production of electrical and electronics in the region. The penetration of multinational companies, like LG, Samsung, Microsoft, Panasonic, Dell, Intel, Toshiba, Sony, Philips, Sharp, Apple, and Lenovo, also positively affects the electrical and electronics market. All such factors are expected to fuel the production revenue of electrical and electronics in the region during the forecast period at a rate of around 7%.

South America Polycarbonate (PC) Industry Overview

The South America Polycarbonate (PC) Market is fairly consolidated, with the top five companies occupying 72.39%. The major players in this market are Covestro AG, LG Chem, Mitsubishi Chemical Corporation, SABIC and Teijin Limited (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Polycarbonate (PC) Trade

- 4.3 Price Trends

- 4.4 Form Trends

- 4.5 Recycling Overview

- 4.5.1 Polycarbonate (PC) Recycling Trends

- 4.6 Regulatory Framework

- 4.6.1 Argentina

- 4.6.2 Brazil

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Country

- 5.2.1 Argentina

- 5.2.2 Brazil

- 5.2.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Covestro AG

- 6.4.2 LG Chem

- 6.4.3 Mitsubishi Chemical Corporation

- 6.4.4 SABIC

- 6.4.5 Teijin Limited

- 6.4.6 Trinseo

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms