|

市場調査レポート

商品コード

1692070

アジア太平洋の豆腐:市場シェア分析、産業動向、成長予測(2025年~2030年)Asia-Pacific Tofu - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の豆腐:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

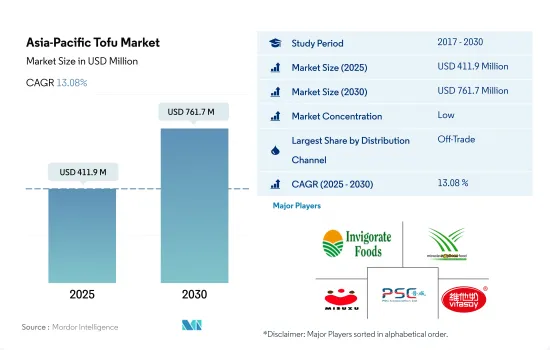

アジア太平洋の豆腐市場規模は、2025年に4億1,190万米ドルと推定され、2030年には7億6,170万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは13.08%で成長すると予測されます。

- アジア太平洋地域では、オフトレードセグメントからの豆腐の販売額は2020年に2019年から28.33%増加しました。2020年には、レストランや外食店舗が閉鎖されたため、多くの家庭がスーパーマーケットやオンライン・チャネルから豆腐を含む植物性食品を購入しました。さらに、消費者はパンデミックによる封鎖の中、パニック買いにより肉代替製品を備蓄しました。

- アジア太平洋地域で豆腐製品が消費される流通チャネルは、非売品部門が支配的です。オフ・トレード・セグメンテーションの全サブ・セグメントのうち、スーパーマーケットとハイパーマーケット・セグメンテーションが主要チャネルであり、2021年の市場シェアの68%を占めています。こうした小売業態の成長は、事業拡大やスーパーマーケットやハイパーマーケットの増加といった要因とともに、同地域の代用肉市場にプラスの影響を与えました。Walmart China、Sun Art Retail Group Ltd、Carrefour Chinaなどの中国の大手小売業者は、消費者を引き付けるために植物由来の豆腐製品を独立した棚スペースで販売し始めました。

- オン・トレード・セグメントは、アジア太平洋地域における代替肉消費の流通チャネルとして急成長を遂げる可能性が高いです。予測期間中のCAGRは14.97%を記録すると予測されます。全国的に植物ベースの食品に対する需要が高まっており、消費者は革新的なバリエーションにより関心を寄せています。そのため、レストランや外食産業は、火鍋、中華風バーベキュー、豆腐スナックなどの革新的な豆腐製品を継続的に発売しており、予測期間には消費者の需要増に対応するため、さらに多くの豆腐製品を革新していくと予想されます。

外食店での豆腐料理需要の高まりが同分野の売上を押し上げる

- このセグメントは2020年から2022年にかけて金額ベースで19.1%の大幅な成長を遂げています。豆腐は伝統的なアジア料理の一部です。豆腐は、製造方法、食感、風味、使い方に微妙な地域差がある料理の一般的な材料です。インポッシブル・フーズ、ジャスト、KFC、カーギルなどの大手企業は、自社製品を革新し、APAC市場で最大の肉消費量を占める中国市場に参入しています。

- しかし、インドの豆腐市場は高い成長が見込まれており、予測期間中のCAGR値は13.60%と予測されています。顧客の食の選択肢が菜食主義にシフトする中、豆腐は理想的な肉の代替品として台頭してきました。豆腐は、環境に優しく残酷な扱いを受けない、非常に優れた蛋白源とみなされています。その結果、豆腐は代替品として受け入れられ、衝動買いする消費者の間で人気が高まっているのと思われます。国内ではベジタリアンの数も多く、2021年時点で3,400万人を超えており、売上を牽引しています。一般的に外食でしか肉を食べない人々も、外食で代替肉の選択肢を探すようになっています。

- この地域の豆腐市場は予測期間中にプラス成長が見込まれ、すべての国でCAGR値が13.17%以上になると予測されています。大豆は豆腐製造の主要原料です。大豆の生産量が比較的少ない地域の一部では、業界の生産量を満たすために大豆を輸入しなければならないです。アジア太平洋は、豆腐がすでに不可欠な文化の一部となっているため、今後も巨大市場であり続けると思われます。各国は、豆腐の生産に必要な大豆と凝固剤の生産を強化し、他国への依存度を下げる必要があります。

アジア太平洋の豆腐市場動向

大豆生産の不確実性が価格高騰を引き起こす

- 2022年のアジア太平洋地域の豆腐の平均価格は6.03米ドル/kgでした。2022年の最高価格はマレーシアとオーストラリアで記録され、7米ドル/kgでした。オーストラリアでは、豆腐は高級品として販売されているため、価格上昇率が高いです。より安価な選択肢もあるが、オーストラリアの消費者はオーストラリア産の原材料を使った豆腐をより好みます。また、「Australian Grown Certified(オーストラリア産認証)」のラベルが付いた豆腐の需要が高く、有機大豆から作られた豆腐はより高いプレミアム価格で売られています。

- 日本における豆腐の価格は、2022年には1kgあたり6米ドルでした。ロシアのウクライナ侵攻後、日本の小売業者は大豆の輸入コスト上昇に直面しているが、需要は依然旺盛です。ウクライナ戦争、円安、中国からの輸入増加により、海外産大豆の価格は2022年には前年比約30%、2015年には同75%上昇しました。こうしたコスト上昇にもかかわらず、豆腐の平均価格は300gあたり約0.50~0.60米ドルと、2015年とほぼ同じ水準にとどまりました。輸入大豆は現在、豆腐1ブロックの約12%を占め、2020年の約6~7%から上昇しています。

- アジア太平洋諸国の政府は、輸入への過度な依存を減らすため、大豆の国内生産を増やすことを目指しています。2022年、中国は9,600万トン以上の大豆を輸入し、国内消費量の85%近くを占めました。しかし、中国はこの状況を変えるため、今後4年間で国内の大豆生産を40%増加させようとしています。2022年1月に農業農村部(MARA)が発表した農作物栽培に関する第14次5ヵ年計画によると、中国は自給率向上のため、大豆生産量を2021年の1,640万トンから2025年までに2,300万トンに増やす計画です。

アジア太平洋の豆腐産業の概要

アジア太平洋の豆腐市場は細分化されており、上位5社で25.64%を占めています。この市場の主要企業は以下の通り。 Invigorate Foods Pvt. Ltd, Miracle Soybean Food International Corporation, Misuzu Corporation, PSC Corporation Limited and Vitasoy International Holdings Ltd(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 豆腐

- 規制の枠組み

- オーストラリア

- 中国

- インド

- 日本

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 流通チャネル

- オフ・トレード

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オン・トレード

- オフ・トレード

- 国名

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- その他のアジア太平洋

第5章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Hangzhou Bean Food Co. Ltd.

- Invigorate Foods Pvt. Ltd

- Leong Guan Food Manufacturer Pte Ltd.

- Miracle Soybean Food International Corporation

- Misuzu Corporation Co. Ltd

- Morinaga Milk Industry Co. Ltd

- PSC Corporation Limited

- Pulmuone Corporate

- Vitasoy International Holdings Ltd

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Asia-Pacific Tofu Market size is estimated at 411.9 million USD in 2025, and is expected to reach 761.7 million USD by 2030, growing at a CAGR of 13.08% during the forecast period (2025-2030).

- In the Asia-Pacific region, tofu's sales value from the off-trade segment increased by 28.33% in 2020 from 2019. In 2020, many households purchased plant-based foods, including tofu, from supermarkets and online channels as restaurants and foodservice outlets were shut. Moreover, consumers stockpiled meat substitute products due to panic buying amid pandemic-induced lockdowns.

- The off-trade segment is the dominant distribution channel through which tofu products are consumed in the Asia-Pacific region. Of all the sub-segments of the off-trade segment, the supermarkets and hypermarkets segment is the major channel, and it accounted for 68% of the market share in 2021. The growth of these retail formats, along with factors like business expansion and the increase in supermarkets and hypermarkets, positively impacted the meat substitute market in the region. The major retailers in China, including Walmart China, Sun Art Retail Group Ltd, and Carrefour China, have started selling plant-based tofu products with a separate shelf space to attract consumers.

- The on-trade segment is likely to be the fastest-growing distribution channel for the consumption of meat substitutes in the Asia-Pacific region. It is projected to record a CAGR of 14.97% in the forecast period. There is a growing demand for plant-based food across the country, and consumers are more interested in innovative variants. Thus, restaurants and the foodservice sector are continuously launching innovative tofu variants, such as hot pot, Chinese-style barbeque, and tofu snacks, and are expected to innovate more tofu products in the forecast period to cater to the growing demand from consumers.

Rising demand for tofu dishes at foodservice outlets boosting the segment sales

- The segment has seen significant growth of 19.1% by value from 2020 to 2022. Tofu is a part of traditional Asian cuisine. It is a common ingredient in dishes with subtle regional variations in methods of production, texture, flavor, and usage. Giants like Impossible Foods, Just, KFC, and Cargill are innovating their products and entering the Chinese market, which accounts for the largest meat consumption within the APAC market.

- However, the Indian tofu market is expected to see high growth and is projected to witness a CAGR value of 13.60% during the forecast period. As customers shift their food choices to vegan alternatives, tofu has emerged as an ideal meat substitute. Tofu is regarded as a very good source of protein that is also eco-friendly and devoid of cruelty. Tofu may have increased in popularity among consumers as an acceptable replacement and impulsive buy as a result. The number of vegetarians is also high in the country, which was over 34 million as of 2021, driving the sales. People who generally eat meat out of home only are also now looking for alternative meat options in the dine-in.

- The tofu market in the region is expected to see positive growth during the forecast period, with all the countries projected to witness a CAGR value of more than 13.17%. Soybean is a major raw material for tofu production. In certain parts of the region where soybean production is relatively low, it has to be imported to satisfy the industry's production volume. Asia-Pacific will continue to be a huge market for tofu, as it is already an integral part of the culture. Countries will need to step up their production of soybeans and coagulants needed for the production of tofu to decrease reliance on other nations.

Asia-Pacific Tofu Market Trends

Uncertainty in soybean production is causing a spike in prices

- In 2022, the average price of tofu in Asia-Pacific was USD 6.03/kg. The highest price in 2022 was recorded in Malaysia and Australia at USD 7/kg. In Australia, tofu is sold as a premium product and, therefore, has a higher price markup. Although cheaper options are available, Australian consumers have a higher preference for tofu made from Australian ingredients. Demand is also more for tofu with the "Australian Grown Certified" label, while tofu made from organic soybeans is sold for a higher premium.

- The price of tofu in Japan was USD 6/kg in 2022. Following Russia's invasion of Ukraine, Japanese retailers are facing higher import costs for soybeans, although demand remains strong. The war in Ukraine, the weaker Yen, and increased imports from China caused soybeans produced overseas to cost around 30% more in 2022 than the previous year and 75% more than in 2015. Despite these rising costs, average tofu prices remained at about USD 0.50-0.60 per 300 grams, which was almost the same as in 2015. Imported soybeans now make up about 12% of a block of tofu, up from around 6-7% in 2020.

- Governments in Asia-Pacific aim to increase domestic soybean production to reduce their excessive reliance on crop imports. In 2022, China imported more than 96 million tons of soybeans, which made up nearly 85% of its domestic consumption. However, China seeks to boost domestic soybean production by 40% over the next four years to change this situation. According to the 14th Five Year Plan on crop farming released by the Ministry of Agriculture and Rural Affairs (MARA) in January 2022, China plans to increase soybean production from 16.4 million tons in 2021 to 23 million tons by 2025 to improve self-sufficiency.

Asia-Pacific Tofu Industry Overview

The Asia-Pacific Tofu Market is fragmented, with the top five companies occupying 25.64%. The major players in this market are Invigorate Foods Pvt. Ltd, Miracle Soybean Food International Corporation, Misuzu Corporation Co. Ltd, PSC Corporation Limited and Vitasoy International Holdings Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Tofu

- 3.2 Regulatory Framework

- 3.2.1 Australia

- 3.2.2 China

- 3.2.3 India

- 3.2.4 Japan

- 3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Distribution Channel

- 4.1.1 Off-Trade

- 4.1.1.1 Convenience Stores

- 4.1.1.2 Online Channel

- 4.1.1.3 Supermarkets and Hypermarkets

- 4.1.1.4 Others

- 4.1.2 On-Trade

- 4.1.1 Off-Trade

- 4.2 Country

- 4.2.1 Australia

- 4.2.2 China

- 4.2.3 India

- 4.2.4 Indonesia

- 4.2.5 Japan

- 4.2.6 Malaysia

- 4.2.7 South Korea

- 4.2.8 Rest of Asia-Pacific

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Hangzhou Bean Food Co. Ltd.

- 5.4.2 Invigorate Foods Pvt. Ltd

- 5.4.3 Leong Guan Food Manufacturer Pte Ltd.

- 5.4.4 Miracle Soybean Food International Corporation

- 5.4.5 Misuzu Corporation Co. Ltd

- 5.4.6 Morinaga Milk Industry Co. Ltd

- 5.4.7 PSC Corporation Limited

- 5.4.8 Pulmuone Corporate

- 5.4.9 Vitasoy International Holdings Ltd

6 KEY STRATEGIC QUESTIONS FOR MEAT SUBSTITUTES INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms