北米の豆腐:市場シェア分析、産業動向、成長予測(2025年~2030年)

North America Tofu - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 177 Pages

- 納期

- 2~3営業日

- 商品コード

- 1692069

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

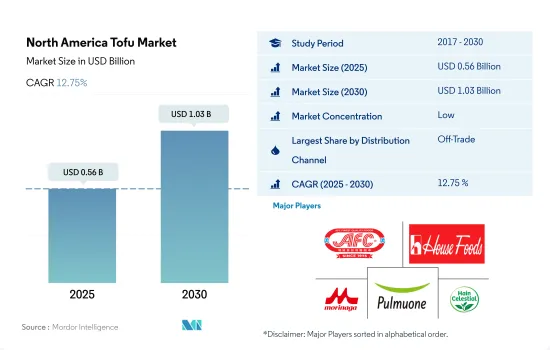

北米の豆腐市場規模は2025年に5億6,000万米ドルと推定・予測され、2030年には10億3,000万米ドルに達し、予測期間中(2025年~2030年)のCAGRは12.75%で成長すると予測されます。

アジア系レストランの増加が市場成長を牽引

- 北米の豆腐市場の流通チャネルを支配しているのは非取引部門です。オフ・トレード部門では、オンライン・チャネルのサブセグメントが最も急成長しています。予測期間中のCAGRは15.93%を記録すると予測されています。eコマースの成長により、企業は顧客のニーズをより便利に満たし、より大きな対応可能市場に到達できるようになりました。豆腐の主なeコマース・チャネルは、消費者への直接販売、クリック・アンド・コレクト、食料品小売店への配送、コンシェルジュ・サービスの4つです。大手豆腐メーカーのハウス・フーズ・アメリカは、カリフォルニアの施設を3万6,000平方フィートまで拡張し、豆腐の生産量を50%増やしました。同様に、プルムオーネは米国西部のカリフォルニア州フラートンで3つの豆腐製造工場を運営しています。

- オン・トレード部門は、主にアジア系レストランや外食業者、アジア系市場で構成されています。アジア料理には豆腐を使った料理や調理法が数多くあります。アジア料理はこの地域で最も急成長している食品動向のひとつと言われています。これまでのところ、2022年には米国内に東アジアと東南アジアをテーマにしたレストランが68,000軒以上ありました。さらに、かなりの数のアジア系移民が北米に居住しています。

- オン・トレード・チャネルは全体として最も急成長しているセグメントであり、2023年から2029年までのCAGRは12.49%を記録すると予測されています。レストランや外食事業者は、肉の理想的な代用品である豆腐を料理に取り入れるようになりました。豆腐は良質な蛋白源であり、ダイエット志向の人々に無農薬で環境に優しい選択肢を提供します。豆腐は近年、十分な代用品として、また衝動買いの選択肢として、顧客の間で人気が高まっています。

急速な製品投入が市場に活気をもたらしています。

- 国別では、米国がこの地域の豆腐市場をリードしており、予測期間中、金額ベースで最も速いCAGR 11.84%を記録すると予測されます。需要の高まりは、購買力の向上と健康と環境に対する意識の高まりによるものです。アメリカの消費者は新製品を試すことに非常に前向きであるため、絶え間ない製品の発売が同国での豆腐の販売を促進する主な要因となっています。さらに、この地域は大豆の生産基盤がしっかりしているため、メーカーが価格をコントロールしやすいです。

- 市場では、ひよこ豆ベースの豆腐の導入が動向しています。ChikfuやFranklin Farmsのようなメーカーは、それぞれ2020年と2021年にこの地域でひよこ豆ベースの豆腐を発売しました。この発売は、大豆アレルギーの消費者だけでなく、新しい製品を試したがる消費者にもアピールするために行われました。米国では、大豆アレルギーの消費者は一般人口の0.5%未満です。これらの製品には、遺伝子組み換え食品不使用、低脂肪、アレルゲン不使用などの謳い文句もあり、消費者は食生活を多様化するために植物由来の選択肢を増やすことができます。

- カナダは豆腐の第2位の市場です。この市場は、従来の肉の味と食感に正確に匹敵するものを求めるブランドによって、ますます推進されています。政府の支援も、同国での豆腐の売上げを押し上げる大きな要因となっています。カナダ政府は植物性食品を重要な成長産業として位置づけています。2021年には、植物性タンパク質産業を含むスーパークラスター・イニシアチブのために1億7,300万米ドルの投資が行われました。したがって、カナダの豆腐市場は予測期間中に金額ベースで10.68%のCAGRで推移すると予測されます。

北米の豆腐市場の動向

豆腐市場の成熟化に伴い、市場価格は安定化する見込み

- 最近の調査によると、米国住民の約5%が自らをベジタリアンと考え、3%がビーガンと考えています。そのため、この地域のビーガン市場は、いくつかの製品の発売によって大きく成長しています。この地域の豆腐の価格は、市場の萌芽的性質のため、ほとんど変わらないです。他の肉代替製品に比べ、豆腐は安価で手ごろなため(2022年にはテクスチャード・ベジタブル・プロテインより107%安い)、小売店の棚に並ぶ人気商品となっています。

- 需要の高まりは米国全体の豆腐価格の上昇につながり、2017年から2022年にかけて6.25%成長しました。市場に参入する企業が増え、売り手は買い手を確保するために価格勝負に出るようになっています。大豆は現在、世界中で供給の混乱に直面しています。米国のインフレは大豆製品のコストに影響を及ぼしています。加えて、米国の大豆農家は、労働力不足、土地賃借料の上昇、大豆生産国の天候不順などを理由に価格を引き上げ、これが域内の大豆価格の上昇につながっています。

- 豆腐は一般的に大豆から作られます。しかし最近では、北米市場でひよこ豆から作られる豆腐の人気が高まっています。ひよこ豆製品に対する国内需要の拡大が価格設定を支え、生産の伸びを加速させています。2023年から2024年にかけては、高値が高値を治めるように働くため、ひよこ豆市場は全般的に弱含みが予想されます。他の多くの農産物とは異なり、一部のひよこ豆品種の価格はこの1年で上昇しました。例えばKabuliとB-90ひよこ豆の価格は1ポンド当たり約45~60セントで、前年比10~13セント上昇しています。

北米の豆腐産業の概要

北米の豆腐市場は細分化されており、上位5社で24.48%を占めています。この市場の主要企業は以下の通り。 American Food Company, House Foods Group Inc., Morinaga Milk Industry, Pulmuone Corporate and The Hain Celestial Group, Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第3章 主要産業動向

- 価格動向

- 豆腐

- 規制の枠組み

- カナダ

- メキシコ

- 米国

- バリューチェーンと流通チャネル分析

第4章 市場セグメンテーション

- 流通チャネル

- オフ・トレード

- コンビニエンスストア

- オンライン・チャネル

- スーパーマーケットとハイパーマーケット

- その他

- オン・トレード

- オフ・トレード

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米

第5章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Albertsons Companies

- American Food Company

- Hodo Inc.

- House Foods Group Inc.

- Morinaga Milk Industry Co. Ltd

- Pulmuone Corporate

- Superior Natural LLC

- The Hain Celestial Group, Inc.

第6章 CEOへの主な戦略的質問

第7章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The North America Tofu Market size is estimated at 0.56 billion USD in 2025, and is expected to reach 1.03 billion USD by 2030, growing at a CAGR of 12.75% during the forecast period (2025-2030).

Rising Asian restaurants driving the market growth

- The off-trade segment dominates the distribution channels of the North American tofu market. In the off-trade segment, the online channel sub-segment is the fastest-growing. It is projected to record a CAGR of 15.93% over the forecast period. The growth of e-commerce has allowed businesses to satisfy their customer needs more conveniently and reach a larger addressable market. The four main e-commerce channels for tofu are direct-to-consumer, click-and-collect, retail grocery delivery, and concierge services. House Foods America, a leading tofu manufacturer, produced 50% more tofu in its Californian facility by expanding its footprint to a 36,000-square-foot facility. Similarly, Pulmuone operates three tofu manufacturing plants in Fullerton, CA, in the Western United States.

- The on-trade segment is primarily composed of Asian restaurants and foodservice operators, as well as Asian markets. There are many dishes and preparations in Asian cuisine with tofu varieties. Asian cuisine is reportedly one of the fastest-growing food trends in the region. So far, in 2022, there were over 68,000 East Asian and Southeast Asian-themed restaurants in the United States. Moreover, a significant number of Asian immigrants reside in North America.

- The on-trade channel is the overall fastest-growing segment, which is projected to record a CAGR of 12.49% from 2023 to 2029. Restaurants and foodservice operators have adapted to include tofu in their offerings, as it is an ideal substitute for meat. Tofu is a good source of protein, providing a cruelty-free and more eco-friendly option to diet-conscious individuals. Tofu has become more popular among customers as an adequate substitute and impulse-buy option in recent years.

Rapid product launches are creating an excitement in the market

- By country, the United States is the leading market for tofu in the region and is projected to register the fastest CAGR of 11.84% by value during the forecast period. The higher demand is due to higher purchasing power and surging health and environmental awareness. Constant product launches are the key factor promoting the sales of tofu in the country because American consumers are highly open to trying new products. Moreover, the region has a strong soybean production base, which makes it easier for the manufacturers to have better control over their prices.

- The introduction of chickpea-based tofu is trending in the market. Manufacturers like Chikfu and Franklin Farms released chickpea-based tofu in the region in 2020 and 2021, respectively. The launch was made to appeal to consumers who are curious about trying new products, as well as soy-allergic consumers. In the United States, soy-allergic consumers make up less than 0.5% of the general population. These products also come with claims like GMO-free, low-fat, and allergen-free, giving consumers more plant-based options to diversify their diets.

- Canada is the second-leading market for tofu. The market is increasingly propelled by brands seeking to match the taste and texture of conventional meat precisely. Governmental support is also a major factor boosting the sales of tofu in the country. The Canadian government has identified plant-based foods as an important and growing industry. In 2021, an investment of USD 173 million was made for the Supercluster Initiative, including the plant protein industry. Thus, the Canadian tofu market is projected to record a CAGR of 10.68% by value during the forecast period.

North America Tofu Market Trends

Market prices are anticipated to stabilize as the tofu market is maturing

- According to a recent survey, about 5% of US residents consider themselves vegetarians, and 3% consider themselves vegans. Thus, the regional vegan market has grown significantly with the launch of several products. The prices of tofu have remained almost the same in the region because of the budding nature of the market. Compared to other meat substitute products, tofu is cheaper and more affordable (107% cheaper than textured vegetable protein in 2022), thus making it a popular product on retail shelves.

- The rising demand led to an increase in the prices of tofu across the United States, growing by 6.25% from 2017 to 2022. More companies are entering the market, and sellers are engaging in the price game to secure buyers. Soybean is currently facing supply disruptions worldwide. Inflation in the United States has had an impact on the cost of soybean products. In addition, soybean farmers in the United States increased prices due to labor shortages, increasing land rental costs, and weather uncertainty in soybean-producing countries, which has led to a rise in soybean prices in the region.

- Tofu is typically made from soybeans. However, in recent times, tofu made from chickpeas has been gaining popularity in the North American market. The expanding domestic demand for chickpea products has supported the pricing and accelerated production growth. A generally weaker chickpea market is expected in 2023-2024, as high prices work to cure high prices. Unlike many other agricultural commodities, the prices of some chickpea variants have risen over the past year. Kabuli and B-90 chickpeas, for example, are priced anywhere from about 45 to 60 cents/lb, up by 10 to 13 cents on the year.

North America Tofu Industry Overview

The North America Tofu Market is fragmented, with the top five companies occupying 24.48%. The major players in this market are American Food Company, House Foods Group Inc., Morinaga Milk Industry Co. Ltd, Pulmuone Corporate and The Hain Celestial Group, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 INTRODUCTION

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

- 2.3 Research Methodology

3 KEY INDUSTRY TRENDS

- 3.1 Price Trends

- 3.1.1 Tofu

- 3.2 Regulatory Framework

- 3.2.1 Canada

- 3.2.2 Mexico

- 3.2.3 United States

- 3.3 Value Chain & Distribution Channel Analysis

4 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 4.1 Distribution Channel

- 4.1.1 Off-Trade

- 4.1.1.1 Convenience Stores

- 4.1.1.2 Online Channel

- 4.1.1.3 Supermarkets and Hypermarkets

- 4.1.1.4 Others

- 4.1.2 On-Trade

- 4.1.1 Off-Trade

- 4.2 Country

- 4.2.1 Canada

- 4.2.2 Mexico

- 4.2.3 United States

- 4.2.4 Rest of North America

5 COMPETITIVE LANDSCAPE

- 5.1 Key Strategic Moves

- 5.2 Market Share Analysis

- 5.3 Company Landscape

- 5.4 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 5.4.1 Albertsons Companies

- 5.4.2 American Food Company

- 5.4.3 Hodo Inc.

- 5.4.4 House Foods Group Inc.

- 5.4.5 Morinaga Milk Industry Co. Ltd

- 5.4.6 Pulmuone Corporate

- 5.4.7 Superior Natural LLC

- 5.4.8 The Hain Celestial Group, Inc.

6 KEY STRATEGIC QUESTIONS FOR MEAT SUBSTITUTES INDUSTRY CEOS

7 APPENDIX

- 7.1 Global Overview

- 7.1.1 Overview

- 7.1.2 Porter's Five Forces Framework

- 7.1.3 Global Value Chain Analysis

- 7.1.4 Market Dynamics (DROs)

- 7.2 Sources & References

- 7.3 List of Tables & Figures

- 7.4 Primary Insights

- 7.5 Data Pack

- 7.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 177 Pages

- 納期

- 2~3営業日