インドのコールドチェーン物流:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

India Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1910699

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

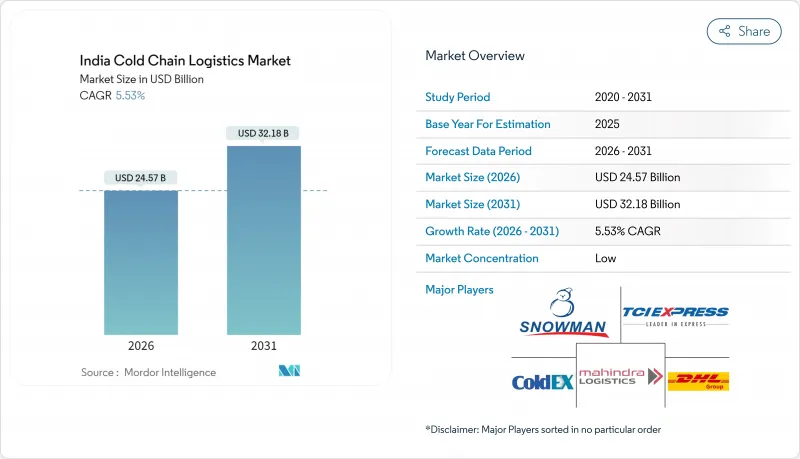

2026年のインドにおけるコールドチェーン物流市場の規模は245億7,000万米ドルと推定され、2025年の232億8,000万米ドルから成長が見込まれます。

2031年までの予測では321億8,000万米ドルに達し、2026年から2031年にかけてCAGR5.53%で拡大する見通しです。

都市部における外食産業の急成長、倉庫施設への公的補助金、生物学的製剤を多用する医薬品パイプラインが相まって、従来の分散型バルク貯蔵から統合型エンドツーエンド温度管理ソリューションへの決定的な移行を推進しております。インド冷却行動計画は省エネルギー資産を推進し、国家物流政策は効率性向上を示す物流対GDP比率を目標としており、事業者の車両更新やAIベースのルート計画導入を促進しています。LNG対応高速道路、電子食料品配送ハブ、eVIN対応ワクチン監視システムは、信頼性の高い超低温流通の需要を強化しています。一方、高効率コンプレッサーへの輸入関税障壁や慢性的な冷凍車ドライバー不足が短期的な勢いを抑制する一方で、規模の優位性を持つ統合型事業者に有利な参入障壁を高めています。太陽光ハイブリッドデポやグリーンエネルギー冷凍車フリートへの民間投資は、カーボンニュートラルに沿った成長軌道を模索するプレイヤーの差別化をさらに進めています。

インドのコールドチェーン物流市場の動向と洞察

全国ガス網の拡張がLNG燃料冷凍トラック輸送を可能に

全国的なパイプライン整備により、2030年までに天然ガス普及率は70%に達する見込みです。これにより1,000ヶ所のLNG給油拠点が整備され、冷蔵車両はディーゼル燃料と比較して約20%の燃料費削減、長距離輸送では約25%の二酸化炭素排出量削減が可能となります。グジャラート州とラージャスターン州では既に輸出量の多いルートにLNG回廊が整備されており、マハーラーシュトラ州のブドウ・タマネギ輸出業者は輸送中の温度管理が安定化することで恩恵を受けています。インド石油公社が2025年までに50ヶ所のLNG小売拠点を設置する目標は、給油間隔の短縮と冷凍車転換プログラムの加速につながります。よりクリーンな燃焼によるメンテナンス費用の削減は、フリート所有者にとってライフサイクルコストを30~40%削減し、インドのコールドチェーン物流市場における採用曲線にさらなる追い風をもたらします。

政府補助による大型冷蔵倉庫計画

首相キサン・サンパダ・ヨジャナ(PM Kisan Sampada Yojana)の下、394件の認可プロジェクトが標準化されたハブ建設により、果物・野菜の収穫後損失25~30%の抑制を目指しています。国立コールドチェーン開発センターは、パッキングハウスと輸送仕様を統一するエンジニアリングテンプレートを提供し、インドのコールドチェーン物流市場全体での相互運用性を向上させています。補助金は小規模農業州の資金不足を補いますが、実施には地域の電力網の信頼性とオペレーター研修が不可欠であり、太陽光バックアップ設備の改修に向けた官民連携が促進されています。

地方都市における電力網の不安定性

大都市圏外の冷蔵倉庫では頻繁な停電が発生し、ディーゼル発電機への依存を招いています。これによりエネルギーコストが18~22%増加し、温度変動のリスクが高まることで生鮮食品の価値が損なわれる恐れがあります。アッサム州の太陽光発電プロトタイプは4~10℃を30時間維持可能ですが、初期費用の高さが小規模生産者の導入を妨げています。農村部のコールドチェーン持続可能性には、長期的な送電網の近代化が依然として不可欠です。

セグメント分析

冷蔵倉庫は2025年時点でインドのコールドチェーン物流市場の40.62%を占めております。これは歴史的に農業大口商品への投資が分断されていたことに起因し、現在も容量増強に対してPMキサン・サンパダ補助金(農業支援補助金)が適用されております。冷蔵輸送ルートの80%は道路輸送が担っておりますが、専用貨物回廊(DFC)の整備により輸送モードの転換が進み、滞留時間の短縮が期待されております。バーコードラベル貼付からキット化に至る付加価値サービスは、オムニチャネル小売業者がワンストップソリューションを求める中、2031年までCAGR5.22%で市場を牽引すると予測されます。スノーマン・ロジスティクスなどの事業者は、品質保証監査やパレット再集荷を扱う統合デスクに隣接したマルチクライアント用冷蔵室を設置し、クロスドック処理速度を向上させています。

包括的なサービス需要の高まりは、公共・民間複合デポモデルの創出にもつながっています。このモデルでは、施設投資と3PL管理契約を分離することで、中小規模の生産者も初期投資なしで改良施設を利用可能となります。CONCOR社の鉄道対応冷凍コンテナは東部の漁業拠点まで到達し、鮮度劣化を抑制。これによりインドの海運輸出向けコールドチェーン物流市場規模が拡大しています。航空貨物回廊はニッチ市場であり、取扱量の2%未満を占めるに過ぎませんが、欧州や北米向けの高価値生物製剤の輸送には依然として不可欠です。小売業者がWMSプラットフォームを倉庫の温度記録に直接連携させる中、サービスプロバイダーはSKU回転を最適化しエネルギーピークを削減するデータ分析ダッシュボードの収益化を進めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 都市化に伴う外食産業の急成長

- 政府補助による大型冷蔵倉庫計画

- 医薬品バイオロジクス及びワクチンパイプラインの拡大

- 電子食料品(E-grocery)におけるラストマイル冷蔵配送需要

- AI最適化ルート・積載計画の導入

- グリーンエネルギーを基盤とした冷蔵トラックフリート

- 市場抑制要因

- 第2/3級都市における電力網の不安定性

- 小規模倉庫の所有権の分散

- 冷凍トラック運転手不足

- 高効率コンプレッサーに対する高い輸入関税

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- サービスタイプ別

- 冷蔵保管

- 公共倉庫

- 民間倉庫

- 冷蔵輸送

- 道路輸送

- 鉄道

- 海上輸送

- 航空便

- 付加価値サービス

- 冷蔵保管

- 温度タイプ別

- 冷蔵(0~5℃)

- 冷凍(-18~0℃)

- アンビエント

- 超低温冷凍(-20℃未満)

- 用途別

- 果物・野菜

- 食肉・家禽類

- 魚介類

- 乳製品・冷凍デザート

- ベーカリー・菓子類

- 即席食品

- 医薬品・生物学的製剤

- ワクチン及び臨床試験用資材

- 化学品・特殊材料

- その他の生鮮品

- 地域別

- 北インド

- デリー首都圏(NCR)

- パンジャブ州

- ハリヤーナー州

- その他

- 南インド

- カルナータカ州

- タミル・ナードゥ州

- テランガナ州

- その他

- 西インド

- マハラシュトラ州

- グジャラート州

- その他

- 東インド

- 西ベンガル州

- オディシャ州

- その他

- 中部インド

- マディヤ・プラデーシュ州

- チャッティースガル州

- 北インド

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Snowman Logistics Ltd

- ColdEx Logistics Pvt Ltd

- TCI Express Ltd

- DHL Supply Chain India

- Mahindra Logistics Ltd

- Gubba Cold Storage Ltd

- Cold Star Logistics Pvt Ltd

- CONCOR Cold Chain Logistics

- Crystal Logistics Cool Chain Ltd

- R. K. Foodland Pvt Ltd

- Indraprastha Cold Storage

- Arihant Cold Storage

- Godamwale

- Siddhi Cold Chain

- Coldrush Logistics

- Coldman Warehousing & Distribution

- Indicold Private Limited

- GK Cold Chain Solutions

- Transworld

- CEVA Logistics(Stellar Value Chain Solutions Pvt Ltd)

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日