|

市場調査レポート

商品コード

1645123

アフリカのコールドチェーンロジスティクス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Africa Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカのコールドチェーンロジスティクス:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

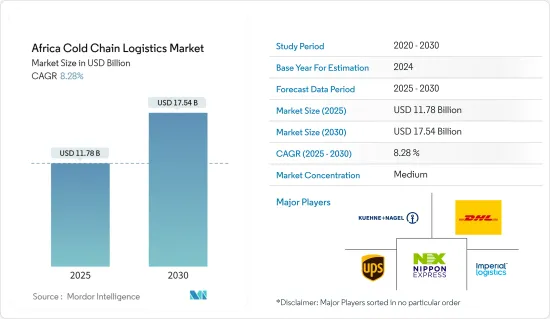

アフリカのコールドチェーンロジスティクス市場規模は2025年に117億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.28%で、2030年には175億4,000万米ドルに達すると予測されています。

アフリカでは、効率的なコールドチェーン包装ソリューションに対する需要が大幅に増加しています。こうした関心の高まりは、同大陸の経済成長に加え、温度に敏感な製品の品質と安全性に対する需要の高まりによるものです。コールドチェーン産業は、同大陸における温度管理された商品に対する需要の増加、多くの新規企業の参入、政府の取り組みやプログラムによって活性化すると期待されています。南アフリカの長期的な輸送ニーズに対応するため、南アフリカでは複合一貫輸送システムの建設を監督する「国家輸送マスタープラン2050」という計画が進行中です。

輸出業者、輸入業者、物流業者の増加に伴い、南アフリカは新興経済国の様相を呈しています。効率的なコールドチェーンを維持することは、これらのセクターの成長を促進し、その寿命を維持するために不可欠です。

A.P.モラーキャピタルは、2023年3月初旬にベクターロジスティクスを買収すると発表しました。A.P.モラーキャピタルによると、この買収はベクターロジスティクスに、サプライチェーンの専門知識とロジスティクス・サービスで独立するという使命を加速させる絶好の機会を提供します。また、アフリカにおける需要の高まりに対応するため、対象地域を拡大し、より広い地域でサービスを提供できるよう活動を広げていく。

アフリカのコールドチェーンロジスティクス市場動向

包装・冷凍食品への需要の高まり

アフリカでは、包装された低温保存食品の需要が増加しています。都市化、ライフスタイルの変化、高所得層の増加がこの開発の一因となっています。これらの製品に対する需要の伸びは、経済開発、近代的な小売店の普及、コールチェーン・インフラの改善など、いくつかの要因によってもたらされています。

2024年2月、ベルリンで開催されたフルーツ・ロジスティカ2024の最後に、イタリアのリグーリア州ラ・スペツィア港と北アフリカを結ぶ強化された物流回廊が発表されました。この協力関係には、港湾システム公社とタロス・グループが関与しており、イタリアのマリーナ・ディ・カラーラ港とラ・スペツィア港とアフリカ沿岸のいくつかの目的地との間の農産物輸送の強化に重点を置いています。このイニシアチブは、特に農業食品分野での物流関係を強化することを目的としています。

アフリカ連合は、この地域における食糧安全保障を優先し、農業バリューチェーンにおける政策、資金援助、マルチステークホルダーによる介入を推進しています。食料安全保障と農業の効率性を高めるため、介入は農場での直接行動と、ある場所から別の場所への食料の移動を促進する支援システムに重点を置いています。

エジプトの水産物輸出が増加中

エジプトの水産業は成長を遂げており、コールドチェーンロジスティクスと大きな関係があります。この分野は、コールドチェーン技術とロジスティクスの進歩がその開発に貢献し、拡大しています。効率的なコールドチェーンシステムは、漁獲から市場出荷まで新鮮な水産物を確実に保存します。このようなロジスティクスの強化は、製品の賞味期限を延ばし、廃棄物を減らし、国際的な品質基準を満たす上で重要な役割を果たしています。エジプトの水産業におけるコールチェーンロジスティクスの統合は、その上昇軌道を牽引する重要な要因です。

エジプトの農業・干拓省は、2023年7月にエジプトの魚類生産量が200万トンに達し、自給率85%に達すると報告しています。報告書によると、エジプトの魚類生産量はアフリカで最も多く、世界で6番目、ティラピア生産量では3番目であり、国家プロジェクトがフル稼働することで輸出率の増加が見込まれています。

同省はまた、漁業セクターを支援するため、漁業を規制・促進する「湖沼保護・魚富開発局」を設立しました。船1隻あたり3万英ポンド(970米ドル)で、政府は漁船に追跡装置も装備しています。したがって、大量生産が可能なこの地域には、コールドチェーンロジスティクスの機会があります。

アフリカのコールドチェーンロジスティクス産業の概要

アフリカでのコールチェーンロジスティクス事業の確立には、温度管理された貯蔵施設や輸送を含む特殊なインフラが必要です。既存企業は主要なサプライヤーや顧客との関係を確立しているため、市場参入の障害となる可能性があります。しかし、この分野の発展的な性質と政府の潜在的な取り組みによって、新規参入者を惹きつけることができます。アフリカのコールドチェーンロジスティクス市場には、国内外を問わず既存の企業が存在し、競争力を発揮しています。各社のサービスの質、信頼性、地理的なカバー範囲、技術力は、競争の重要な要因です。この分野は進化しており、各社は競争に勝ち残るために常に革新的な取り組みを行っています。東南アジアの郵便サービス市場のリーダーは、日本通運、UPS、DHLです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- コールドチェーン施設の技術動向と自動化

- 政府の規制と取り組み

- 環境・温度管理された保管庫のスポットライト

- 輸送コストと保管コスト

- 排出基準および規制がコールドチェーン業界に与える影響

- 地政学とパンデミックが市場に与える影響

第5章 市場力学

- 市場促進要因

- 生鮮品に対する需要の高まり

- 健康意識の高まり

- 市場抑制要因

- 高コスト

- 適切なインフラの欠如

- 市場機会

- 政府のイニシアティブと投資

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン/サプライチェーン分析

第6章 市場セグメンテーション

- サービス別

- 保管

- 輸送

- 付加価値サービス(ブラスト冷凍、ラベリング、在庫管理など)

- 温度別

- 常温

- チルド

- 冷凍

- 用途別

- 園芸(生鮮果物・野菜)

- 乳製品(牛乳、アイスクリーム、バターなど)

- 肉、魚、鶏肉

- 加工食品

- 製薬、ライフサイエンス、化学

- その他の用途

- 国別

- エジプト

- モロッコ

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第7章 競合情勢

- 企業プロファイル

- Imperial Logistics LTD

- Cold Solutions East Africa

- ARCH Emerging Markets Partners Limited

- Nippon Express Co. Ltd

- Zenith Carex International Limited

- Ayoba Cold Storage

- Kennie-o Cold Chain Logistics(KCCL)

- Trans-nationwide Express PLC(TRANEX)

- Kuehne+Nagel

- Cool World Rentals

- DP World

- Lineage Logistics

- CCS Logistics

- AfriAg

- その他の企業

第8章 市場の将来

第9章 付録

- 資本フローの洞察

- 対外貿易統計-輸出と輸入、製品別、国別

- 運輸・倉庫業の経済への貢献

The Africa Cold Chain Logistics Market size is estimated at USD 11.78 billion in 2025, and is expected to reach USD 17.54 billion by 2030, at a CAGR of 8.28% during the forecast period (2025-2030).

The demand for efficient cold chain packaging solutions in Africa has increased significantly. This increase in interest is due to the continent's growing economy, as well as increasing demand for quality and security of temperature-sensitive products. The cold chain industry is expected to be boosted by the increasing demand for temperature-controlled goods in the continent, the entry of many new businesses, and the government's efforts and programs. To meet the country's long-term transport needs, South Africa has an ongoing plan, namely the National Transport Master Plan 2050, to oversee the construction of multimodal transport systems.

With growing exporters, importers, and logistics operators, South Africa is experiencing an emerging economy. Maintaining an efficient cold chain is essential to facilitate these sectors' growth and maintain their longevity.

A.P. Moller Capital announced that it would acquire Vector Logistics at the beginning of March 2023. According to A.P. Moller Capital, the acquisition provides Vector Logistics a great opportunity to accelerate its mission of going independent in supply chain expertise and logistics services. In this context, it will also expand its coverage to meet growing demand in Africa and broaden its activities to serve the wider geographic area.

Africa Cold Chain Logistics Market Trends

Demand for Packaged and Frozen Food is Rising

In Africa, the demand for packaged, cold-stored foods is increasing. Urbanization, changes in lifestyles, and the growth of a higher class are some of the factors that contribute to this development. The growth in demand for these products is being driven by several factors, including economic development, the proliferation of modern retail outlets, and improvements to cold chain infrastructure.

In February 2024, the strengthened logistics corridor between the Ligurian port of La Spezia in Italy and North Africa was unveiled at the end of Fruit Logistica 2024 in Berlin. The collaboration involves the Harbour System Authority and the Tarros Group, with a focus on enhancing the transportation of agricultural goods between the ports of Marina di Carrara and La Spezia in Italy and several African coastal destinations. The initiative aims to bolster logistical ties, particularly in the agri-food sector.

The African Union prioritizes food security in the region and promotes policy, funding, and multistakeholder interventions in the agricultural value chain. To increase food security and agricultural efficiency, the intervention focuses on direct farm action and support systems facilitating the movement of food from one place to another.

Egyptian Export of Seafood is on the Rise

Egypt's fishing industry is experiencing growth, with a significant connection to cold chain logistics. The sector is expanding as advancements in cold chain technology and logistics contribute to its development. Efficient cold chain systems ensure the preservation of fresh seafood from catch to market. This enhancement in logistics plays a crucial role in extending the shelf life of products, reducing waste, and meeting international quality standards. The integration of cold chain logistics in Egypt's fishing industry is a key factor driving its upward trajectory.

The Ministry of Agriculture and Land Reclamation in Egypt reported that Egyptian fish production hit 2 million tons, marking a rate of 85% self-sufficiency, in July 2023. According to the report, Egypt has the highest fish production in Africa, sixth in the world, and third in tilapia production, and is expected to increase export rates with national projects operating at full capacity.

The Ministry also founded the Lake Protection and Fish Wealth Development Authority to regulate and facilitate the fishing industry to support the fishing sector. For EGP 30,000 (USD 970) per vessel, the government is also equipping fishing vessels with tracking devices. Therefore, with massive production, there is an opportunity for cold chain logistics in the area.

Africa Cold Chain Logistics Industry Overview

Specialized infrastructure, including temperature-controlled storage facilities and transport, is required for the establishment of an African cold chain logistics operation. Existing companies have established relationships with key suppliers and customers, which could create obstacles to entry into the market. However, new entrants can be attracted by the evolving nature of this sector and potential government initiatives. The presence of established companies, both local and international, in the African cold chain logistics market exerts a competitive influence. The quality of the service, reliability, geographic coverage, and technical capabilities of the companies are important factors for competition. The sector is evolving, and companies are constantly innovative to stay ahead of the competition. The leaders in the Southeast Asian postal services market are Nippon Express, UPS, and DHL.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends and Automation in Cold Chain Facilities

- 4.3 Government Regulations and Initiatives

- 4.4 Spotlight on Ambient/Temperature-controlled Storage

- 4.5 Spotlight on Transportation Costs and Storage Costs

- 4.6 Impact of Emission Standards and Regulations on the Cold Chain Industry

- 4.7 Impact of Geopolitics and Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for Perishable Goods

- 5.1.2 Increasing Health Awareness

- 5.2 Market Restraints

- 5.2.1 High Cost Associated

- 5.2.2 Lack of adequate infrastructure

- 5.3 Market Opportunities

- 5.3.1 Government Initiatives and Investments

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers / Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

- 5.5 Industry Value Chain/Supply Chain Analysis

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Storage

- 6.1.2 Transportation

- 6.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 6.2 By Temperature

- 6.2.1 Ambient

- 6.2.2 Chilled

- 6.2.3 Frozen

- 6.3 By Application

- 6.3.1 Horticulture (Fresh Fruits and Vegetables)

- 6.3.2 Dairy Products (Milk, Ice-cream, Butter, etc.)

- 6.3.3 Meat, Fish, Poultry

- 6.3.4 Processed Food Products

- 6.3.5 Pharma, Life Sciences, and Chemicals

- 6.3.6 Other Applications

- 6.4 By Country

- 6.4.1 Egypt

- 6.4.2 Morocco

- 6.4.3 Nigeria

- 6.4.4 South Africa

- 6.4.5 Rest of Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 Imperial Logistics LTD

- 7.2.2 Cold Solutions East Africa

- 7.2.3 ARCH Emerging Markets Partners Limited

- 7.2.4 Nippon Express Co. Ltd

- 7.2.5 Zenith Carex International Limited

- 7.2.6 Ayoba Cold Storage

- 7.2.7 Kennie-o Cold Chain Logistics (KCCL)

- 7.2.8 Trans-nationwide Express PLC (TRANEX)

- 7.2.9 Kuehne+Nagel

- 7.2.10 Cool World Rentals

- 7.2.11 DP World

- 7.2.12 Lineage Logistics

- 7.2.13 CCS Logistics

- 7.2.14 AfriAg*

- 7.3 Other Companies

8 FUTURE OF THE MARKET

9 APPENDIX

- 9.1 Insights into Capital Flows

- 9.2 External Trade Statistics - Export and Import, by Product and by Country

- 9.3 Transport and Storage Sector Contribution to the Economy