|

市場調査レポート

商品コード

1690145

アジア太平洋のコールドチェーン物流:市場シェア分析、産業動向、成長予測(2025年~2030年)Asia-Pacific Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のコールドチェーン物流:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

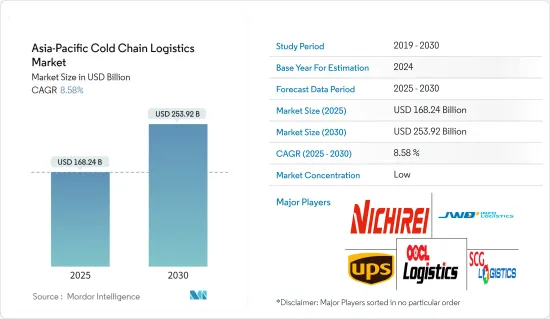

アジア太平洋のコールドチェーン物流市場規模は、2025年に1,682億4,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは8.58%で、2030年には2,539億2,000万米ドルに達すると予測されます。

冷蔵倉庫の増加や医薬品分野の市場開拓といった要因が、アジア太平洋のコールドチェーン物流市場の成長を牽引すると予想されます。

主なハイライト

- コールドチェーン物流はアジア太平洋で人気があります。同地域は世界人口の約60%を占める大規模な消費者基盤を有しています。可処分所得の増加や食生活の変化により、高級品への需要が高まっています。こうした製品の輸送も重要です。もちろんCOVID-19は、食品の安全性に対する懸念の高まりなど、アジアのコールドチェーン事業にも影響を与えています。これはすでに消費者の習慣を変えつつあり、生鮮食品や冷凍食品を従来のウェット・マーケットではなく、スーパーマーケットのような組織化された小売チャネルで購入する人が増えています。eコマースやオンライン食品小売の台頭も、冷凍食品の需要を促進しています。こうした動向は、この地域の低温貯蔵施設の需要を増大させ、インフラと輸送の改善へのさらなる投資を後押ししています。

- 日本はコールドチェーン物流の成熟市場と見なされており、複数の企業が優位を占めています。東京を拠点とするニチレイロジグループは、1945年に日本冷蔵株式会社として設立されました。今日、同社は倉庫業、冷蔵倉庫業、輸送サービスを日本および世界で提供しています。レストラン、小売店、食品メーカー、商社、卸売業者など、さまざまな業界の顧客が同社の低温物流サービスを利用しています。日本では2024年に「自動車運転業務の時間外労働の上限規制」が実施され、運輸・物流業界への影響が懸念されます。技術革新もまた、作業効率の向上、作業ミスの削減、事故防止につながると予想されます。

- コールドチェーン・アプリケーション用のRFID(Radio-Frequency Identification)技術の利用可能性と、コールドチェーン物流用の自動化ソフトウェアの採用は、市場プレーヤーに有利な成長機会を提供すると予測されます。近年のアジア太平洋では、旺盛な国内消費、eコマース産業の拡大、近代的な物流施設の開発により、高品質の産業用および物流用資産に対する需要が堅調に推移しています。可処分所得の増加と高齢化により、アジア太平洋にはヘルスケア用品に対する膨大な消費者層が存在します。食品の安全性に対する懸念が高まり、従来のウェット・マーケットと比較してスーパーマーケットなどの組織化された小売チャネルで生鮮食品や冷凍食品を購入する消費者の習慣が継続的に変化しています。

- 食生活パターンの変化により、肉、乳製品、魚介類など、温度に敏感で管理された温度での保管・輸送が必要な高級品への需要が高まっています。アジア太平洋では冷蔵倉庫のリース需要が堅調であるにもかかわらず、欧米の新興国市場に比べて冷蔵倉庫のキャパシティは限られています。冷蔵倉庫の賃貸料は、ドライ倉庫よりも高いです。しかし、作業手順、セキュリティ、温度、害虫駆除に関する標準化が進んでいないこと、運用コストの増加といった要因が、市場の成長を抑制しています。

アジア太平洋のコールドチェーン物流市場の動向

日本国内の水上貨物輸送量の減少

- 日本の国内貨物取扱量は毎年47億トンを超えます。水、鉄道、航空、道路など、あらゆる輸送手段が経済において重要な役割を果たしています。貨物輸送は主に製造業や消費によって生み出される需要に依存しているが、輸送はトラックや、ドローンを含むあらゆる種類の車両の需要を生み出しています。

- 日本では自動化の急速な開発が行われています。日本の物流業界は労働力不足に苦しんでおり、既存のドライバーは急速に高齢化しているため、商品販売に占める輸送コストの割合が高まる恐れがあります。

- トラック輸送と内航海運は、年間積載距離という点で、日本の物流業界を支配する輸送手段です。鉄道と航空輸送も商品輸送に利用されています。しかし、鉄道網は人の輸送に非常に効率的であるにもかかわらず、ほとんどの物流施設、倉庫、工場は道路とよりよくつながっています。

冷蔵倉庫の増加

- COVID-19の流行は、サプライチェーンの見通しに大きな変化をもたらし、健康への懸念とともに、業務効率を達成するためのデジタル・ハイエンド技術の利用拡大を可能にしました。物流業界の見通しの変化、大幅なコスト最適化の要求、最適な在庫管理は、アジア太平洋のコールドチェーン物流市場の成長をサポートすると予想されます。

- コールドチェーンシステムを構成するいくつかの倉庫は、温度に敏感な製品の理想的な保管・輸送条件を確保するように設計されています。複数の輸出産業は現在、コールドチェーン・ソリューションが提供する重要なリンクに依存しています。

- エンド・ツー・エンドのコールドチェーン・セキュリティがシステムの弱点となっているため、企業は効果的かつ効率的で信頼性の高いプロセスを構築するため、コールドチェーン業務に数百万米ドルを投資しています。さらに、アジア太平洋における食品や医薬品の需要の急増により、冷蔵倉庫の数が増加しています。そのため、冷蔵倉庫の増加がアジア太平洋のコールドチェーン物流市場の成長を後押しすると予想されます。

アジア太平洋のコールドチェーン物流産業の概要

アジア太平洋のコールドチェーン市場は非常に細分化されており、多くの世界企業や地元企業が需要の拡大に対応しています。UPS、OOCL物流、JWDは同市場における主要企業の一部です。コールドチェーン業界が直面する重大な課題は、膨大なエネルギーとスペースの消費、莫大な設定・変更コストです。保管温度や作業手順に関する標準化の欠如は、業界が直面するさらに重要な課題です。利用可能な冷蔵倉庫スペースの質と柔軟性は、かなりの懸念事項です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析方法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学

- 現在の市場シナリオ

- 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 技術動向と自動化

- 政府の規制と取り組み

- 環境・温度管理保管への注目

- 排出基準および規制がコールドチェーン業界に与える影響

- COVID-19の市場への影響

第5章 市場セグメンテーション

- サービス別

- 保管

- 輸送

- 付加価値サービス(ブラスト凍結、ラベリング、在庫管理など)

- 温度タイプ別

- チルド

- 冷凍

- 用途別

- 園芸(生鮮果物・野菜)

- 乳製品(牛乳、アイスクリーム、バターなど)

- 肉、魚、鶏肉

- 加工食品

- 製薬、ライフサイエンス、化学

- その他の用途

- 国別

- 中国

- 日本

- インド

- 韓国

- インドネシア

- タイ

- オーストラリア

- フィリピン

- その他のアジア太平洋

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- United Parcel Service of America

- OOCL Logistics Ltd

- JWD Infologistics Public Company Ltd

- Nichirei Logistics Group Inc.

- SCG Logistics Management Company Limited

- X2 Logistics Network(X2 GROUP)

- AIT Worldwide Logistics Inc.

- CWT PTE. LIMITED(CWT International Ltd)

- SF Express

- CJ Rokin Logistics*

第7章 アジア太平洋のコールドチェーン物流市場の将来性

第8章 付録

The Asia-Pacific Cold Chain Logistics Market size is estimated at USD 168.24 billion in 2025, and is expected to reach USD 253.92 billion by 2030, at a CAGR of 8.58% during the forecast period (2025-2030).

Factors such as the increasing number of refrigerated warehouses and the development of the pharmaceutical sector are expected to drive the growth of the Asia-Pacific cold chain logistics market.

Key Highlights

- Cold chain logistics are popular in the Asia Pacific. The region has a large consumer base, accounting for roughly 60% of the global population. Demand for premium products is increasing, driven by rising disposable incomes and a shift in dietary habits. Transportation for these products is also important. Of course, COVID-19 has had an impact on Asian cold chain operations, including increased concerns about food safety. This is already changing consumer habits, with more people buying fresh and frozen food from organized retail channels like supermarkets rather than traditional wet markets. The rise of e-commerce and online food retailing has also fueled demand for frozen foods. These trends have increased the demand for cold storage facilities in the region and bolstered further investments in infrastructure and transportation improvements.

- Japan is regarded as a mature market for cold chain logistics, with several players dominating. Nichirei Logistics Group Inc., based in Tokyo, was founded in 1945 as Nippon Reizo Inc. Today, the company provides warehousing, cold storage, and transportation services in Japan and around the world. Customers in a variety of industries use its low-temperature logistics services, including restaurants, retail stores, food manufacturers, trading companies, and wholesalers. The 'upper limit on overtime hours in automobile driving operations' will be implemented in Japan in 2024, raising concerns about the impact on the transportation and logistics industries. Technological innovation is also expected to improve work efficiency, reduce workplace errors, and prevent accidents.

- The availability of Radio-frequency identification (RFID) technologies for cold chain applications and the adoption of automated software for cold chain logistics is projected to offer lucrative growth opportunities for the market players. Recent years have seen robust demand for high-quality industrial and logistics assets in Asia-Pacific due to strong domestic consumption, the e-commerce industry's expansion, and the development of modern logistics facilities. Due to the rising disposable income and ageing population, Asia-Pacific has a vast consumer base for healthcare supplies. There are increasing concerns over food safety and a continuous shift in consumer habits to buy fresh and frozen food products from organized retail channels, such as supermarkets, compared to traditional wet markets.

- The shift in dietary patterns is increasing the demand for premium products, including meat, dairy, and seafood, which are temperature-sensitive and need to be stored and transported at controlled temperatures. Despite robust leasing demand for cold storage facilities in Asia-Pacific, cold storage capacity in the region is limited compared to that in developed western markets. Cold storage facilities command higher rental premiums than dry warehouses. However, factors such as lack of standardization about operating procedures, security, temperature, pest control, and increased operational costs restrain the market's growth.

Asia Pacific Cold Chain Logistics Market Trends

Decreasing Volume of Domestic Water Freight Transport in Japan

- Japan handles more than 4.7 billion tons of domestic freight every year. Every mode of transport, including water, rail, air, and road, fulfills a crucial role in the economy. While cargo transport relies primarily on demand created by manufacturing industries and consumption, transportation creates demand for trucks and vehicles of any kind, including drones.

- Rapid developments in automation are taking place in Japan. The Japanese logistics industry suffers labor shortages, and the existing drivers are rapidly aging, thereby threatening to increase the fraction of transport costs in the sale of goods.

- Trucking and coastal shipping are the Japanese logistics industry's dominant modes of transport in terms of yearly payload distance. Railway and air transport are also used for transporting goods. However, despite the railway network being highly efficient for the transport of people, most logistics facilities, warehouses, and factories are better connected to roads.

Increased Number of Refrigerated Warehouses

- The COVID-19 pandemic has resulted in a significant change in the supply chain outlook, enabling the growing usage of digital high-end technologies to attain operational efficiency along with health concerns. The changing logistics industry outlook, requirement for substantial cost optimization, and optimum inventory management are anticipated to support the growth of the Asia-Pacific cold chain logistics market.

- Several warehouses comprising cold chain systems are designed to ensure the ideal storage and transportation conditions for temperature-sensitive products. Multiple export industries are now dependent on the vital links provided by cold chain solutions.

- Businesses are investing millions of dollars in their cold chain operations to create effective, efficient, and reliable processes, as end-to-end cold chain security is the weak link in the system. Moreover, the number of refrigerated warehouses is increasing due to a surge in demand for food and pharmaceutical products in the Asia-Pacific region. Therefore, an increase in refrigerated warehouses is anticipated to boost the growth of the Asia-Pacific cold chain logistics market.

Asia Pacific Cold Chain Logistics Industry Overview

The Asia-Pacific cold chain market is highly fragmented, with many global and local players catering to the growing demand. UPS, OOCL Logistics, and JWD are some of the major players in the market. Critical challenges faced by the cold chain industry are enormous energy and space consumption and huge setup and modification costs. Lack of standardization related to storage temperature and operating procedures are a few more significant challenges the industry faces. The quality and flexibility of available cold warehousing space are a considerable concern.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Method

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS DYNAMICS

- 4.1 Current Market Scenario

- 4.2 Market Overview

- 4.3 Market Dynamics

- 4.3.1 Drivers

- 4.3.2 Restraints

- 4.3.3 Opportunities

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Technological Trends and Automation

- 4.7 Government Regulations and Initiatives

- 4.8 Spotlight on Ambient/Temperature-controlled Storage

- 4.9 Impact of Emission Standards and Regulations on Cold Chain Industry

- 4.10 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Services

- 5.1.1 Storage

- 5.1.2 Transportation

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, Etc.)

- 5.2 By Temperature Type

- 5.2.1 Chilled

- 5.2.2 Frozen

- 5.3 By Application

- 5.3.1 Horticulture (Fresh Fruits and Vegetables)

- 5.3.2 Dairy Products (Milk, Ice-cream, Butter, Etc.)

- 5.3.3 Meats, Fish, Poultry

- 5.3.4 Processed Food Products

- 5.3.5 Pharma, Life Sciences, and Chemicals

- 5.3.6 Other Applications

- 5.4 By Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 South Korea

- 5.4.5 Indonesia

- 5.4.6 Thailand

- 5.4.7 Australia

- 5.4.8 Philippines

- 5.4.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 United Parcel Service of America

- 6.2.2 OOCL Logistics Ltd

- 6.2.3 JWD Infologistics Public Company Ltd

- 6.2.4 Nichirei Logistics Group Inc.

- 6.2.5 SCG Logistics Management Company Limited

- 6.2.6 X2 Logistics Network (X2 GROUP)

- 6.2.7 AIT Worldwide Logistics Inc.

- 6.2.8 CWT PTE. LIMITED (CWT International Ltd)

- 6.2.9 SF Express

- 6.2.10 CJ Rokin Logistics*