米国のコールドチェーン物流:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

US Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690184

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

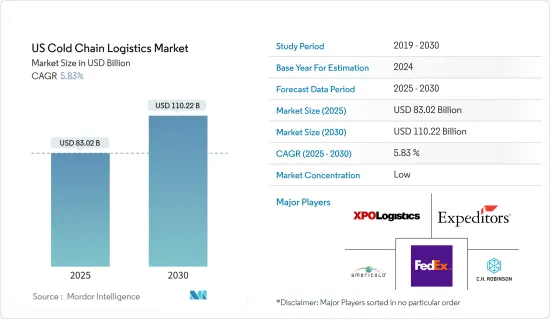

米国のコールドチェーン物流市場規模は2025年に830億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.83%で、2030年には1,102億2,000万米ドルに達すると予測されます。

主要ハイライト

- COVID-19の大流行により、国内の電子小売セクタと加工食品・飲食品の消費が大きく伸び、冷蔵保管スペースと物流の需要を押し上げました。生鮮食品や冷凍食品の注文が大きな割合を占めるオンライン食料品店の台頭も、市場の需要を支えています。温度変化に敏感な製品の生産と供給に対する政府の厳しい規制も、この市場に大きな利益をもたらしています。

- しかし、輸送・倉庫部門における労働力不足、高いエネルギー要件、コールドチェーン物流業務による環境への悪影響は、市場の成長を制限する可能性のある課題の一部です。高いエネルギー要件と環境への悪影響に関する課題に取り組むため、一部の企業はコールドチェーンインフラの稼働に必要なエネルギーを増加させるソリューションを導入しています。

- 人工知能(AI)、機械学習、モノのインターネット(IoT)、ロボット工学、ウェア、配送センターの自動化などの技術は、業務の効率化、運用コストの削減、より良い顧客体験の提供を目的として、参入企業によって取り入れられています。

- より広範な産業物流市場全体でアウトソーシングが増加しており、2021年同期間の30%から増加し、2022年5月までのリース活動全体の34%をサードパーティ・物流(3PL)プロバイダが占めています。この動向は、コストとより複雑な技術システムのため、冷蔵倉庫産業では特に一般的です。

- 米国農務省(USDA)によると、米国の冷蔵倉庫容量の72%は公開冷蔵倉庫(PRW)会社に委託されており、5年前の75%から減少しています。残りの28%は自社内のコールドチェーン事業者で、5年前の25%から増加しています。

- 生鮮品の輸入、生物製剤セグメントを含む製薬産業の成長、冷凍食品の消費拡大、医薬品の温度モニタリング規制などが、米国のコールドチェーン物流市場の需要促進要因となっています。

米国のコールドチェーン物流市場の動向

メキシコからの生鮮食品輸入の増加

- 米国は世界中から年間220億米ドル相当の生鮮食品を輸入しており、125カ国以上から生鮮食品を受け入れています。同国の生鮮野菜の32%、生鮮果実の55%は他国から輸入されています。

- ラテンアメリカと北米を結ぶ航空貨物で輸送される商品のほぼ70%は生鮮品です。米国が輸入する生鮮果物と野菜の77%はメキシコ産で、さらに11%はカナダ産です。

- メキシコは米国にとって最大の農産物貿易相手国であり、2022年の総輸入額は719億米ドル(輸入+輸出)でした。米国のメキシコへの農産物輸出は285億米ドル、メキシコからの輸入は434億米ドルです。メキシコから輸入される主要農産物は果物と野菜で、実際、米国が輸入する果物の44%、野菜の48%がメキシコ産です。

- 米国農務省(USDA)によれば、2022年、メキシコからの米国農産物輸入の83.6%は野菜、果物、飲料、蒸留酒でした。

- 米国は2022年、メキシコから生鮮、冷凍、加工果物、野菜、ナッツを含む187億米ドルの農産物を輸入しました。これらの輸入の98%強は、メキシコとテキサス、ニューメキシコ、アリゾナ、カリフォルニアの間の陸路港から米国に入港しています。青果物全体の89%近くを占める生鮮果物・野菜のみを考慮すると、輸入総額は166億米ドルにのぼります。

- これらの輸入は59万906個の4万ポンドトラックで出荷されました。メキシコからの米国産生鮮青果物輸入の約55%はテキサス州の陸上港を経由し、トラック32万5,467台分(116億米ドル相当)が到着しました。

冷凍食品の人気の高まり

- 米国冷凍食品協会(AFFI)の報告によると、2022年の冷凍食品の売上高は8.6%増の722億米ドルとなりました。その間の販売個数は減少したが、パンデミック前の水準を5%上回ったままでした。

- 2018~2022年の間に、冷凍食品のドル売上高は194億米ドルも増加し、パンデミックがこのカテゴリーの成長に与えた影響を明確にしました。冷凍食品のドル売上高は2018年以降一貫して上昇しているが、販売個数は2021年と2022年の両方でそれぞれ3.2%と5.1%減少しており、冷凍食品のコストに対するインフレの潜在的影響が浮き彫りになっています。

- 減少にもかかわらず、販売個数はパンデミック流行前の水準と比較すると依然高水準にあり、冷凍食品に対する需要が継続していることを示しています。これは特に冷凍加工肉、冷凍スナック、冷凍魚介類に当てはまり、これらはパンデミック流行前の水準と比較して販売個数が2桁増となっています。

- AFFIの新しい調査によると、買い物客の4分の1以上が3年前よりも冷凍野菜・果物を購入しており、これらの食品には多くの利点があると認識しています。冷凍野菜・果物は、家庭や人口層が農産物の消費量を増やし、食品廃棄物を減らすことを容易にします。米国における冷凍青果物の普及率は全体的に高く、94%の家庭が冷凍青果物を購入しています。

- 米国における冷凍果物・野菜の売上高は、2022年6月26日までの52週間で71億米ドルに達し、製品量はパンデミック前の水準を2億7,100万ポンド上回る39億ポンドとなりました。同セグメントの上位製品は、プレーン野菜、ジャガイモ、タマネギ、果物で、売上高はそれぞれ29億米ドル、23億米ドル、15億米ドルでした。

米国のコールドチェーン物流産業概要

米国のコールドチェーン物流市場は非常に細分化されており、温度変化に敏感な商品の国内と国際輸送を支援しています。太陽電池式冷蔵ユニット、多温度トラック、貨物最適化ソフトウェアの導入により開発が進んでいます。FedEx、XPO Logistics、Total Quality Logistics、Americold Logisticsなど、国際企業や地元企業がこの市場に進出しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- 製薬産業の成長

- メキシコからの生鮮食品輸入の増加

- 冷凍食品の人気上昇

- 抑制要因

- コールドチェーン作業による排出

- 労働力不足

- 機会

- エネルギー効率の高いソリューションの採用

- オンライン食料品ビジネスの台頭

- 促進要因

- 産業の魅力-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術動向と自動化に関する洞察

- 政府の規制と取り組みに関する洞察

- 産業のバリューチェーン/サプライチェーン分析

- 環境・温度管理された保管庫への注目

- 排出基準と規制がコールドチェーン産業に与える影響

- COVID-19が市場に与える影響

第5章 市場セグメンテーション

- サービス別

- 保管

- 輸送

- 付加価値サービス(ブラスト凍結、ラベリング、在庫管理など)

- 温度タイプ別

- 冷蔵

- 冷凍

- 常温

- 用途別

- 果物・野菜

- 乳製品(牛乳、バター、チーズ、アイスクリームなど)

- 魚、肉、水産物

- 加工食品

- 医療医薬品

- ベーカリー・製菓

- その他

第6章 競合情勢

- 市場集中概要

- 企業プロファイル

- FedEx

- XPO Logistics

- CH Robinson Worldwide

- JB Hunt

- Expeditors

- Total Quality Logistics

- Americold Logistics

- Burris Logistics

- Prime Inc.

- Lineage Logistics

- Arc Best

- Stevens Transport

- DHL Supply Chain

- United States Cold Storage

- DB Schenker

- Covenant Transportation Services*

第7章 市場の将来

第8章 付録

目次

The US Cold Chain Logistics Market size is estimated at USD 83.02 billion in 2025, and is expected to reach USD 110.22 billion by 2030, at a CAGR of 5.83% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic significantly boosted the domestic e-retailing sector and the consumption of processed foods and beverages, pushing the demand for refrigerated storage spaces and logistics. The rise of online groceries, with a significant share of orders for perishables and frozen foods, is also supporting the market demand. The market has also benefitted significantly from the stringent government regulation toward the production and supply of temperature-sensitive products.

- However, the labor shortages in the transportation and warehousing sector, high energy requirements, and the negative environmental impact of the cold chain logistics operations are some of the challenges that may limit the market growth. To tackle the challenges regarding the high energy requirements and negative environmental impact, some companies are introducing solutions that increase the energy required to run the cold chain infrastructure.

- Technologies like Artificial Intelligence (AI), Machine Learning, Internet of Things (IoT), Robotics, Ware, and distribution center automation are being incorporated by players to increase the efficiency of their operations, reduce operational costs, and provide better customer experience.

- More outsourcing is occurring throughout the broader industrial logistics market, with third-party logistics (3PL) providers accounting for 34% of total leasing activity in 2022 through May, up from 30% in the same period of 2021. This trend is particularly common in the cold storage industry due to costs and more complex technology systems.

- According to the US Department of Agriculture (USDA), 72% of the refrigerated storage capacity in the US is outsourced to public refrigerated warehouse (PRW) companies, down from 75% five years ago. The remaining 28% includes in-house cold chain operators, up from 25% five years ago.

- The perishables imports, pharmaceutical industry growth, including the biologics sector, increasing consumption of frozen foods, pharmaceutical temperature monitoring regulations, etc., are the demand drivers for the cold chain logistics market in the United States.

US Cold Chain Logistics Market Trends

Rising fresh produce imports from Mexico

- The United States imports over USD 22 billion worth of fresh produce annually from all over the globe and receives fresh produce from over 125 countries. Thirty-two percent of the country's fresh vegetables and fifty-five percent of its fresh fruit are imported from other countries.

- Almost 70% of all goods shipped via air freight between Latin America and North America consist of perishable products. Seventy-seven percent of the fresh fruits and vegetables imported by the United S come from Mexico, with an additional 11% from Canada.

- Mexico is the largest agricultural trading partner for the United States, totaling USD 71.9 billion (imports plus exports) in 2022. US agricultural exports to Mexico totaled USD 28.5 billion, while imports from Mexico totaled USD 43.4 billion. The main agricultural products imported from Mexico are fruits and vegetables; in fact, 44% of the fruits and 48% of the vegetables imported by the US are from Mexico.

- In 2022, 83.6% of US agricultural imports from Mexico consisted of vegetables, fruit, beverages, or distilled spirits, according to the US Department of Agriculture (USDA).

- The United States imported USD 18.7 billion of produce from Mexico in 2022, including fresh, frozen, and processed fruits, vegetables, and nuts. Just over 98% of these imports entered the United States through land ports between Mexico and Texas, New Mexico, Arizona, and California. When considering only fresh fruits and vegetables, which constitute nearly 89% of the total produce, imports totaled USD 16.6 billion.

- These imports were shipped in 590,906 forty-thousand-pound truckloads. Approximately 55% of the US fresh fruit and vegetable imports from Mexico entered through Texas land ports, arriving in 325,467 truckloads worth USD 11.6 billion.

Increasing popularity of frozen foods

- The American Frozen Food Institute (AFFI) reported that frozen food sales increased 8.6% to USD 72.2 billion in 2022. Unit sales decreased during that time but remained 5% above pre-pandemic levels.

- Between 2018 and 2022, frozen food dollar sales increased a whopping USD 19.4 billion, underlining the impact of the pandemic on the category's growth. While frozen food dollar sales have consistently climbed since 2018, unit sales decreased in both 2021 and 2022 by 3.2% and 5.1%, respectively, highlighting the potential impact of inflation on frozen food costs.

- Despite the decreases, unit sales remain elevated compared to pre-pandemic levels, indicating continued demand for frozen foods. This is particularly true for frozen processed meat, frozen snacks, and seafood, which have seen double-digit increases in unit sales compared to pre-pandemic levels.

- A new survey from AFFI finds that more than a quarter of shoppers are buying more frozen fruits and vegetables than three years ago and identify many benefits with these foods. Frozen fruits and vegetables help make it easier for households and demographic groups to increase their produce consumption and reduce food waste. Overall, penetration in the United States is high, with 94% of American households buying frozen fruits and vegetables.

- The sales of frozen fruits and vegetables in the United States reached USD 7.1 billion over the 52 weeks ending June 26, 2022, and product volume were 271 million pounds above pre-pandemic levels at 3.9 billion pounds. The top products within the segment were plain vegetables, potatoes, onions, and fruit, with sales of USD 2.9 billion, USD 2.3 billion, and USD 1.5 billion, respectively.

US Cold Chain Logistics Industry Overview

The cold chain logistics market of the United States is highly fragmented, aiding the domestic as well as international transportation of temperature-sensitive goods. It is undergoing developments with the introduction of solar-powered refrigerated units, multi-temperature trucks, and freight optimization software. International and local players like FedEx, XPO Logistics, Total Quality Logistics, Americold Logistics and many such companies are operational in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 PHARMACEUTICAL INDUSTRY GROWTH

- 4.2.1.2 RISING FRESH PRODUCE IMPORTS FROM MEXICO

- 4.2.1.3 INCREASING POPULARITY OF FROZEN FOODS

- 4.2.2 Restraints

- 4.2.2.1 EMISSIONS FROM COLD CHAIN OPERATIONS

- 4.2.2.2 LABOUR SHORTAGES

- 4.2.3 Opportunities

- 4.2.3.1 Adopting energy-efficient solutions

- 4.2.3.2 rise of online grocery business

- 4.2.1 Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers/Consumers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Insights on Technological Trends and Automation

- 4.5 Insights on Government Regulations and Initiatives

- 4.6 Industry Value Chain/Supply Chain Analysis

- 4.7 Spotlight on Ambient/Temperature-controlled Storage

- 4.8 Impact of Emission Standards and Regulations on Cold Chain Industry

- 4.9 Impact of Covid-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Services

- 5.1.1 Storage

- 5.1.2 Transportation

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.2 By Temperature Type

- 5.2.1 Chilled

- 5.2.2 Frozen

- 5.2.3 Ambient

- 5.3 By Application

- 5.3.1 Fruits and Vegetables

- 5.3.2 Dairy Products (Milk, Butter, Cheese, Ice Cream, Etc.)

- 5.3.3 Fish, Meat, and Seafood

- 5.3.4 Processed Food

- 5.3.5 Healthcare & Pharmaceuticals

- 5.3.6 Bakery and Confectionary

- 5.3.7 Other Applications

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 FedEx

- 6.2.2 XPO Logistics

- 6.2.3 CH Robinson Worldwide

- 6.2.4 JB Hunt

- 6.2.5 Expeditors

- 6.2.6 Total Quality Logistics

- 6.2.7 Americold Logistics

- 6.2.8 Burris Logistics

- 6.2.9 Prime Inc.

- 6.2.10 Lineage Logistics

- 6.2.11 Arc Best

- 6.2.12 Stevens Transport

- 6.2.13 DHL Supply Chain

- 6.2.14 United States Cold Storage

- 6.2.15 DB Schenker

- 6.2.16 Covenant Transportation Services*

7 FUTURE OF THE MARKET

8 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日