|

|

市場調査レポート

商品コード

1687782

ASEANのコールドチェーン物流:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)ASEAN Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ASEANのコールドチェーン物流:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

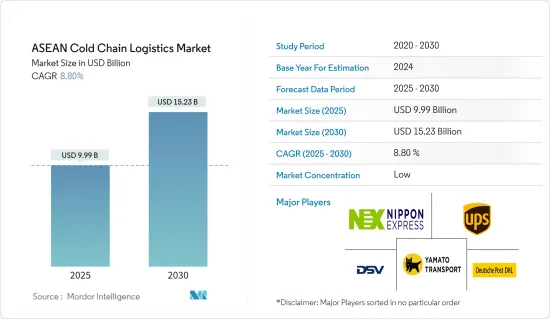

ASEANのコールドチェーン物流市場規模は2025年に99億9,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは8.8%で、2030年には152億3,000万米ドルに達すると予測されます。

主なハイライト

- 都市人口の増加と消費者意識の変化が冷蔵保管・輸送需要を押し上げています。冷蔵/冷凍製品市場は東南アジアで急成長しています。

- 食品の流通は従来の市場からスーパーマーケットやコンビニエンスストアへと急速にシフトしています。大手流通業者が保冷トラックによる輸送を提供しているため、冷蔵・冷凍製品は調達しやすくなっています。

- 現地のコールドチェーン・サービスの質には大きなばらつきがあります。冷蔵不足のために食品が傷むこともあります。東南アジアの食品廃棄物の90%は輸送中に発生すると推定されています。

- インドのコールドチェーン事業はまだ初期段階にあるが、コールドチェーン倉庫・物流業界では最も有望な産業のひとつです。

- 2027年までに、インドは世界第5位の経済大国になります。世界市場において確立された重要なプレーヤーであるため、インドのサプライチェーン・インフラへの投資は年々増加すると思われます。

- 幸いなことに、インド政府はコールドチェーン産業の開発を推進し、さまざまな補助金制度や優遇措置を通じて民間の参入を促しています。食品加工産業省(MoFPI)は、コールドチェーン、付加価値、保存インフラ・プログラムを開始しました。

- ASEAN諸国における所得水準の上昇とライフスタイルの変化は、これらの地域における食肉消費と生産の成長にとって重要な要因です。インドネシアとベトナムが主に成長を牽引しています。

ASEANのコールドチェーン物流市場の動向

ハラルフードが市場を牽引

- 近年、世界・ブランドは購買力の上昇と消費者の消費優先順位の変化を利用するため、イスラム経済に注目し始めています。ASEAN地域には約2億6,000万人のイスラム教徒が住んでおり、そのほとんどがインドネシア、マレーシア、タイ、フィリピン、シンガポール、ミャンマー、ブルネイに住んでいます。過去10年間に地域全体で開催されたハラル・ライフスタイルのイベントやキャンペーンの数は、イスラムの旅行、食品、ファッション、化粧品への関心を刺激しています。

- 韓国の大手食品会社SPCグループは、世界のハラル食品産業2兆米ドルの一部を獲得するため、マレーシアに進出する意向です。シンガポールと国境を接するマレーシアのジョホール州で、SPCグループはハラル認証工場の建設に400億ウォン(約3,000万米ドル)を投資する計画を発表しました。韓国メディアによると、この施設は港があるため、東南アジア全域と中東に商品を送るルートを持つことになるといいます。

- ハラル食品の多くは食肉製品であるため、各国政府のハラル認証を受けたコールドチェーン倉庫で保管する必要があります。最近の動向では、ハラル産業の開発を目的としたいくつかの政策が政府によって示されており、その中にはハラル産業のための経済特区(KEK)の設立も含まれています。

- 加えて、シャリア経済金融国家委員会(KNEKS)とユニリーバ・インドネシアなどの企業との連携は、同国のハラル産業を後押しするものと期待されています。マレーシア政府もまた、ハラル市場の世界マーケットリーダーとなるべく、多くの前進を行っています。ハラル産業のマスタープランとハラルパークは、政府が最近行った進歩です。これらすべてのハラル・イニシアチブが、ASEAN諸国のコールドチェーン物流を牽引しています。

食肉消費の増加がASEANのコールドチェーン物流を促進

- 東南アジアの人口拡大、所得の増加、都市化、小売業は、食肉消費の増加と飼料輸入の増加に寄与しています。この地域の主要新興市場は、インドネシア、マレーシア、フィリピン、タイ、ベトナムの5カ国です。

- 近年、食肉消費も増加しているが、魚介類は消費・生産される最大の食肉源であり、飼料需要の一部を担っています。東南アジア各国は、消費量と生産量に反映されるように、肉の嗜好がそれぞれ異なっています。

- マレーシアは、これら東南アジア諸国の中で最高の生産額を誇る鶏肉部門で、大規模な生産設備を持っています。

- ASEAN諸国におけるハラル食品の需要の高まりは、さまざまな要因によるものです。重要な要因のひとつは、この地域におけるイスラム教徒の人口増加です。イスラム教の食習慣を遵守する人が増えるにつれ、ハラル認証食品に対する需要が増加しています。

- さらに、消費者の間でも、食品の出所や調理法に関する意識や意識が高まっています。イスラム教徒に限らず、多くの人々がハラル認証製品を選ぶようになっており、その理由は、より高品質で衛生的で、より安全に消費できると認識されているからです。

- ASEAN地域はまた、イスラム教徒の多い国からの旅行者を含む観光客の大幅な増加を目の当たりにしています。こうした観光客は旅行中にハラル食品を求め、ハラル認証を受けたレストランや食品の需要を生み出しています。

- こうした需要の高まりに対応するため、ASEAN諸国の企業は食品のハラル認証を積極的に追求しています。ハラール認証は、製品が必要な基準を満たし、イスラムの食事法に則って調理されていることを保証するものです。この認証は消費者を保証し、企業が有利なハラル市場を開拓するのに役立ちます。

ASEANのコールドチェーン物流産業の概要

ASEANのコールドチェーンロジスティクス市場は、世界プレーヤーとローカルプレーヤーが混在する断片的な市場です。現地の中小規模のプレーヤーは、小規模なフリートと保管スペースで市場にサービスを提供しています。シンガポールのように、DHLや日本通運のような世界プレーヤーが強い存在感を示している国もあります。さらに、世界・プレーヤーは、この地域での足跡を増やすために、市場に投資し、現地企業を買収しています。

さらに、日本のロジスティクス企業は、製造業や流通業の国ごとに陸上輸送の拠点をASEAN諸国に設置することで、ASEAN地域での活動を強化し、サプライチェーンの構築を推進しています。また、コールドチェーンの開発にも携わり、青果物、花卉、化粧品、消費財関連の物流にも積極的に投資しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 市場の範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 市場力学

- 促進要因

- コールドチェーンロジスティクスに対する需要の増加

- この地域における国際貿易の拡大

- 抑制要因

- 適切なインフラと施設の不足

- コールドチェーン・ロジスティクスに関連する高コスト

- 機会

- 生鮮品に対する需要の高まり

- 市場を牽引する技術の進歩

- 促進要因

- 冷蔵施設の技術動向と自動化

- 政府の規制と取り組み

- ASEANコールドチェーン産業における日本の役割に関する考察と解説

- 業界のバリューチェーンに関する洞察

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- コールドチェーン業界における排出基準および規制の影響

- 冷蔵倉庫で使用される冷媒と包装材料に関する洞察

- インドネシアとマレーシアのハラール基準と認証に関する洞察

- 環境・温度管理された保管庫に関する洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- サービス別

- 保管

- 輸送

- 付加価値サービス(ブラスト凍結、ラベリング、在庫管理など)

- 温度別

- 常温

- チルド

- 冷凍

- 用途別

- 園芸(生鮮果物・野菜)

- 乳製品(牛乳、アイスクリーム、バターなど)

- 肉・魚

- 加工食品

- 製薬、ライフサイエンス、化学

- その他の用途

- 地域別

- シンガポール

- タイ

- ベトナム

- インドネシア

- マレーシア

- フィリピン

- その他のASEAN諸国

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Nippon Express

- United Parcel Service of America

- Deutsche Post DHL

- Yamato Transport Co. Ltd

- DSV Agility Logistics

- NYK(Yusen Logitics & TASCO)

- Tiong Nam Logistics

- Sinchai Cold Storage

- Jentec Storage Inc.

- JWD Logistics

- KOSPA

- PT. Pluit Cold Storage

- PT. Wahana Cold Storage

- Havi Logistics

- Royal Cargo

- Thai Max Co. Ltd

- MGM Bosco*

第7章 市場の将来

第8章 主要ベンダーとサプライヤー

- ストレージ機器メーカー

- キャリアメーカー

- テクノロジープロバイダー

第9章 付録

- 冷蔵倉庫の年間統計

- 冷凍食品の輸出入貿易データ

- 主要国の食品輸送と貯蔵に関する規制枠組みについての洞察

- 東南アジアの飲食品セクターに関する洞察

The ASEAN Cold Chain Logistics Market size is estimated at USD 9.99 billion in 2025, and is expected to reach USD 15.23 billion by 2030, at a CAGR of 8.8% during the forecast period (2025-2030).

Key Highlights

- The growing urban population and changing consumer perception have boosted refrigerated storage and transport demand. The market for refrigerated/frozen products is rapidly growing in Southeast Asia.

- The distribution of food products is rapidly shifting from traditional markets toward supermarkets and convenience stores. Refrigerated and frozen products are easier to procure, as major distributors offer shipping via insulated trucks.

- The quality of local cold-chain services varies widely. Food products have been damaged due to the lack of refrigeration. It is estimated that 90% of Southeast Asia's food waste is created during transport.

- Indian cold chain business is still in its early stages, it is one of the most promising industries in the cold chain warehousing and logistics industry.

- By 2027, India will have the world's fifth-largest economy. Investment in India's supply chain infrastructure is likely to increase year on year since it is a well-established, important player in the global market.

- Fortunately, the Indian government is a driving factor in the development of the cold chain industry, encouraging private participation through a variety of subsidy programs and incentives. The Ministry of Food Processing Industries (MoFPI) has initiated a cold chain, value addition, and preservation infrastructure program.

- Rising income levels in ASEAN countries and lifestyle changes are key factors for the growth of meat consumption and production in these regions. Indonesia and Vietnam are mainly driving the growth.

ASEAN Cold Chain Logistics Market Trends

Hallal Food is offering traction to the market

- In recent years, global brands have begun to focus on the Muslim economy to capitalize on rising purchasing power and shifting consumer spending priorities. Around 260 million Muslims live in the ASEAN region, most of whom live in Indonesia, Malaysia, Thailand, the Philippines, Singapore, Myanmar, and Brunei. The number of halal lifestyle events and campaigns held across the region in the last decade stimulates interest in Islamic travel, foods, fashion, and cosmetics.

- SPC Group, a major South Korean food company, intends to grow into Malaysia to capture a portion of the USD 2 trillion worldwide halal food industry. In Johor, a Malaysian state bordering Singapore, SPC Group announced plans to invest 40 billion won (about USD 30 million) in the construction of a halal-certified factory. According to South Korean media, the facility will have a route to send goods throughout Southeast Asia and into the Middle East thanks to the location's ports.

- Since most halal food is meat products, they need to be stored in cold chain warehouses that are Halal-certified by the respective Governments. In recent times, several policies aimed at developing the halal industry have been demonstrated by the government, including the establishment of a Special Economic Zone (KEK) for the industry.

- In addition, the collaboration between the National Committee for Sharia Economics and Finance (KNEKS) and companies such as Unilever Indonesia is expected to boost the country's halal industry. The Malaysian government is also making many advancements to become a global market leader in the halal market. The halal industry's master plan and halal park are the recent advancements made by the government. All these halal initiatives are driving the cold chain Logistics in ASEAN countries.

Increase in Meat Consumption Propelling Cold Chain Logistics in ASEAN Countries

- Southeast Asia's expanding population and increasing incomes, urbanization, and retail sectors are contributing to rising meat consumption and growing imports of feedstuffs. The five key emerging markets within the region are Indonesia, Malaysia, the Philippines, Thailand, and Vietnam.

- In recent years, meat consumption has also increased, although fish and seafood are the largest meat sources consumed and produced and are partially responsible for feedstuffs demand. Every Southeast Asian country has different meat preferences, as reflected by their levels of consumption and production.

- Malaysia has a sizable production apparatus in the poultry sector, which has the best production values among these Southeast Asian nations.

- The increasing demand for halal food products in ASEAN countries can be attributed to various factors. One of the key factors is the growing Muslim population in the region. As more people adhere to Islamic dietary practices, the demand for halal-certified food products has increased.

- Moreover, there has been a rise in awareness and consciousness among consumers regarding the source and preparation of their food. Many people, not just Muslims, are opting for halal-certified products as they perceive them to be of higher quality, more hygienic, and safer to consume.

- The ASEAN region has also witnessed a significant increase in tourism, including visitors from predominantly Muslim countries. These tourists seek halal food options during their travels, creating a demand for halal-certified restaurants and food products.

- To cater to this growing demand, businesses in ASEAN countries have been actively pursuing halal certification for their food products. Halal certification ensures that the products meet the required standards and are prepared in accordance with Islamic dietary laws. This certification assures consumers and helps businesses tap into the lucrative halal market.

ASEAN Cold Chain Logistics Industry Overview

The ASEAN cold chain logistics market's landscape is fragmented in nature, with a mix of global and local players. Small- and medium-sized local players still serve the market with small fleets and storage spaces. Some of the countries, like Singapore, have a strong presence of global players, like DHL and Nippon Express. Additionally, global players are investing in the market and acquiring local companies to increase their footprint in the region.

Furthermore, Japanese logistics companies strengthen their activities in the ASEAN region by setting up bases of land transportation in ASEAN countries for each country within the manufacturing and distribution industries, thereby pushing the construction of a supply chain. The companies are also involved in developing the cold chain and actively investing in logistics related to fruits and vegetables, flowers, cosmetics, and consumer goods.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Market

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing demand for cold chain logistics

- 4.2.1.2 Expansion of international trade in the region

- 4.2.2 Restraints

- 4.2.2.1 Lack of proper infrastructure and facilities

- 4.2.2.2 High cost associated to cold chain logistics

- 4.2.3 Opportunities

- 4.2.3.1 Growing demand for perishable goods

- 4.2.3.2 Technological advancements driving the market

- 4.2.1 Drivers

- 4.3 Technological Trends and Automation in Cold Storage Facilities

- 4.4 Government Regulations and Initiatives

- 4.5 Review and Commentary on Role of Japan in the ASEAN Cold Chain Industry

- 4.6 Insights into Industry Value Chain

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Emission Standards and Regulations in the Cold Chain Industry

- 4.9 Insights into Refrigerants and Packaging Materials Used in Refrigerated Warehouses

- 4.10 Insights into Halal Standards and Certifications in Indonesia and Malaysia

- 4.11 Insights into Ambient/Temperature-controlled Storage

- 4.12 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Storage

- 5.1.2 Transportation

- 5.1.3 Value-added Services (Blast Freezing, Labeling, Inventory Management, etc.)

- 5.2 By Temperature

- 5.2.1 Ambient

- 5.2.2 Chilled

- 5.2.3 Frozen

- 5.3 By Application

- 5.3.1 Horticulture (Fresh Fruits and Vegetables)

- 5.3.2 Dairy Products (Milk, Ice-cream, Butter, etc.)

- 5.3.3 Meats and Fish

- 5.3.4 Processed Food Products

- 5.3.5 Pharma, Life Sciences, and Chemicals

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Singapore

- 5.4.2 Thailand

- 5.4.3 Vietnam

- 5.4.4 Indonesia

- 5.4.5 Malaysia

- 5.4.6 Philippines

- 5.4.7 Rest of ASEAN

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Nippon Express

- 6.2.2 United Parcel Service of America

- 6.2.3 Deutsche Post DHL

- 6.2.4 Yamato Transport Co. Ltd

- 6.2.5 DSV Agility Logistics

- 6.2.6 NYK (Yusen Logitics & TASCO)

- 6.2.7 Tiong Nam Logistics

- 6.2.8 Sinchai Cold Storage

- 6.2.9 Jentec Storage Inc.

- 6.2.10 JWD Logistics

- 6.2.11 KOSPA

- 6.2.12 PT. Pluit Cold Storage

- 6.2.13 PT. Wahana Cold Storage

- 6.2.14 Havi Logistics

- 6.2.15 Royal Cargo

- 6.2.16 Thai Max Co. Ltd

- 6.2.17 MGM Bosco*

7 FUTURE OF THE MARKET

8 KEY VENDORS AND SUPPLIERS

- 8.1 STORAGE EQUIPMENT MANUFACTURERS

- 8.2 CARRIER MANUFACTURERS

- 8.3 TECHNOLOGY PROVIDERS

9 APPENDIX

- 9.1 Annual Statistics on Refrigerated Storage Facilities

- 9.2 Import and Export Trade Data of Frozen Food Products

- 9.3 Insights into Regulatory Framework on Food Transportation and Storage in Key Countries

- 9.4 Insights into the Food and Beverage Sector in Southeast Asia