|

市場調査レポート

商品コード

1910947

イタリアのコールドチェーン物流:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Italy Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| イタリアのコールドチェーン物流:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

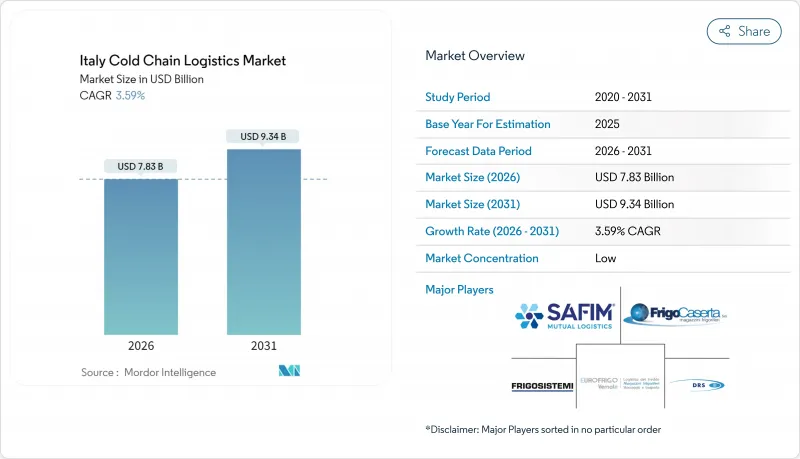

イタリアのコールドチェーン物流市場規模は、2026年に78億3,000万米ドルと推定されております。

これは2025年の75億6,000万米ドルから成長した数値であり、2031年には93億4,000万米ドルに達すると予測されております。2026年から2031年にかけてはCAGR3.59%で成長が見込まれております。

市場が成熟期を迎えることで、急激な成長ではなく着実な伸びが見込まれますが、ライフサイエンス分野の流通、EC食品配送、カーボンニュートラル運営への構造的シフトが投資の勢いを維持します。収益性は、再生可能エネルギーによるエネルギー価格上昇の抑制と、労働力不足を補う自動化の導入能力にかかっています。国際的なプロバイダーが買収を通じてイタリアでの事業基盤を強化する一方、国内の専門企業は地域ネットワークを活用して高収益契約を維持しており、競合は激化しています。技術主導の透明性は必須条件となり、リアルタイムのIoTモニタリングやAIによるルート最適化は、イタリアのコールドチェーン物流市場全体で一般的となっています。

イタリアのコールドチェーン物流市場の動向と洞察

Eコマース食品配送

オンライン食料品販売の急速な普及により、小売業者はラストマイル冷蔵能力の構築を迫られており、信頼性の高い温度管理に対するプレミアム需要が高まっています。イタリア郵便公社(Poste Italiane)とDHLは2024年に1万台の宅配ロッカーを導入し、その多くは顧客が受け取るまで生鮮食品を5℃以下に保つ機能を備えています。ロッカーは滞留時間を短縮し、配達失敗コストを削減するため、ネットワークのさらなる高密度化を促進しています。MDやEverliなどの小売業者は、コールドチェーン保証と連動した当日配送サービスを統合しています。物流事業者は付加価値サービス、特に事前仕分けや集約型マイクロハブ中継拠点の整備で収益化を図っています。都市部の渋滞規制により電気冷蔵バンが優遇され、ゼロエミッションモデルへの車両更新が促進されています。

コンビニエンスフード需要

ライフスタイルの変化により、家庭での調理済み食品や冷凍スナックへの支出が増加しています。これらはエンドツーエンドの冷蔵管理が不可欠です。2024年の食料品プロモーション活動は売上高の24.3%に達し、生鮮・冷凍品が牽引役となりました。DACHSERのイタリア事業部はMuller Fresh Food Logisticsを買収し、ピークシーズンの処理能力を確保しました。小売業者のエッセルンガ社は、プロモーション期間中のサービス水準維持のため、2024年に物流設備のアップグレードに2億5,200万米ドルを投資しました。コンビニエンスストア形式の拡大に伴い、注文規模が細分化され、配送密度の課題が深刻化しています。クロスドックにおける自動化により、混合温度パレットの仕分けが数分で完了し、賞味期限の延長とピッキングミス削減が実現しています。

エネルギー・燃料価格の高騰と変動性

2025年、企業の平均電気料金は24%、ガス料金は27%上昇し、冷蔵設備がコストの焦点となりました。24時間稼働の急速冷凍庫を保有する事業者は影響が拡大し、固定価格契約の利益率が圧迫されています。先物ヘッジや負荷の15~25%を賄う屋上太陽光発電の導入で対応する事業者もあれば、水素対応冷凍機の試験導入を進める事業者もいますが、設備投資額は依然として高額です。価格の不確実性により中小運送業者の車両更新計画が停滞し、繁忙期の輸送能力不足が懸念されます。

セグメント分析

2025年時点で、冷蔵倉庫はイタリアのコールドチェーン物流市場規模の50.55%を占めており、既存事業者を保護する資本障壁の存在が浮き彫りとなっています。オペレーターはミラノとローマ近郊で容量を拡大し、食料品・医薬品荷主からの集約需要を捉えようとしています。成長は、クロスドックゾーン、ピック・トゥ・ライトモジュール、医薬品グレードのクリーンルームを統合したマルチ温度管理型施設に有利です。キット化、ラベリング、GDP文書化などの付加価値サービスはCAGR3.78%で拡大し、基本輸送を上回っています。2025年施行のEU GDP改正に伴う監査強化を受け、規制対応の専門知識を収益化する事業者が増加しています。冷蔵輸送は安定的な輸送量を維持する一方、脱炭素化規制により低排出ゾーン内では電気バンへの車両更新が義務付けられています。2025年までの線路改良に伴う鉄道輸送の混乱により、一部の貨物輸送が道路へ移行し、トラック輸送の収益性を一時的に押し上げる反面、CO2排出強度を高めています。海上・航空複合輸送ソリューションは、完全航空輸送よりも排出量が少ない時間・温度管理を必要とするニッチな医薬品需要を獲得しています。

合併の波が業界再編を示しています。リネージ・ロジスティクスは地域倉庫チェーンを吸収し、MARRはラツィオ州とプーリア州に新プラットフォームを構築し、ホスピタリティ回廊へのサービスを提供しています。投資家が安定した賃料収益を追い求める中、REITが冷蔵倉庫市場に参入しています。自動化投資は増加しており、パレットシャトル、AS/RSクレーン、エネルギーモデリング用デジタルツインなどが対象です。在庫計画にAIを組み込むプロバイダーは、廃棄物を削減し、5~7%の追加利用可能スペースを確保することで、電気料金の上昇にもかかわらず利益率を守っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 温度管理が必要な食料品における電子商取引の成長

- 生鮮・冷凍コンビニエンスフードの需要増加

- バイオ医薬品コールドチェーンの拡大(ワクチン及び生物学的製剤)

- 輸出志向型園芸作物および水産物の取扱量

- オンライン薬局と患者への直接配送の急増

- カーボンニュートラル冷凍ソリューションの導入

- 市場抑制要因

- エネルギー・燃料価格の変動性

- 有資格ドライバーおよび倉庫作業員の不足

- 複雑なEU/イタリアの食品安全基準およびGDP準拠

- 都市部におけるマイクロフルフィルメント用冷蔵ハブの不足

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 排出基準及びEUグリーンディール目標の影響

- COVID-19および地政学的イベントの影響

第5章 市場規模と成長予測

- サービスタイプ別

- 冷蔵保管

- 公共倉庫

- プライベート倉庫

- 冷蔵輸送

- 道路輸送

- 鉄道

- 海上輸送

- 航空便

- 付加価値サービス

- 冷蔵保管

- 温度タイプ別

- 冷蔵(0~5℃)

- 冷凍(-18~0℃)

- アンビエント

- 超低温冷凍(-20℃未満)

- 用途別

- 果物・野菜

- 肉類・家禽類

- 魚介類

- 乳製品・冷凍デザート

- ベーカリー・菓子類

- レトルト食品

- 医薬品・生物製剤

- ワクチン・臨床試験用資材

- 化学品・特殊材料

- その他の生鮮品

- イタリア地域別

- 北イタリア

- 中部イタリア

- 南イタリア

- 島嶼部(シチリア島・サルデーニャ島)

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Safim Logistics

- Frigocaserta Srl

- Eurofrigo Vernate Srl

- Frigoscandia SpA

- DRS Depositi Regionali Surgelati Srl

- Frigogel Srl

- Soluzioni Logistiche Freddo Srl

- Sodele Magazzini Generali Frigoriferi Srl

- Horigel Srl

- Fridocks General Warehouses & Frigoriferi Srl

- Lineage Logistics

- Mazzocco Srl

- Stef Italia

- DHL Supply Chain

- Kuehne+Nagel CoolCare Ital

- DSV

- CEVA Logistics

- Gruppo Marconi Logistica Integrata

- Trans Isole S.r.l.

- Linofrigo Trasporti Srl