|

|

市場調査レポート

商品コード

1687350

ディスクリート半導体:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Discrete Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ディスクリート半導体:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 224 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

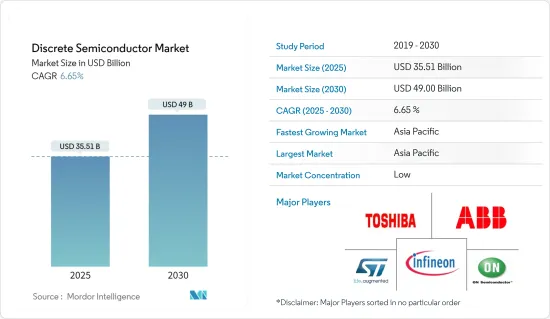

ディスクリート半導体の市場規模は、2025年に355億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.65%で、2030年には490億米ドルに達すると予測されます。

出荷量では、2025年の4,272億1,000万個から2030年には5,449億9,000万個に成長すると予測され、予測期間(2025~2030年)のCAGRは4.99%です。

主なハイライト

- 新しいアプリケーションの登場や既存技術の進化に伴い、より高度で効率的な半導体への需要が高まっています。小型化、電力効率の向上、性能の改善といった進歩は、半導体をさまざまなデバイスやシステムに統合する新たな可能性を開きます。モノのインターネット(IoT)、人工知能(AI)、自律走行車などの分野における革新が、ディスクリート半導体の需要を押し上げています。

- さらに、自動車やエレクトロニクス分野での高エネルギーで電力効率の高いデバイスの需要の高まりや、グリーンエネルギー発電の需要の増加が市場を牽引しています。

- さらに、世界のコンシューマー・エレクトロニクス市場は、可処分所得の増加、ライフスタイルの変化、技術の進歩といった要因に後押しされ、急速な成長を続けています。スマートフォン、タブレット、ウェアラブル、家電製品などの家電製品は、ディスクリート半導体に大きく依存しています。こうした機器の需要の増加は、ディスクリート半導体の需要の増加につながり、市場の成長を牽引しています。

- しかし、市場は成長と開拓に影響を与えるいくつかの抑制要因に直面しています。集積回路(IC)との競合の激化は、市場の成長にとって大きな課題です。ICはコンパクトでコスト効率の高いソリューションを提供するため、ディスクリート半導体の需要が減少しています。このような市場の嗜好の変化は、ディスクリート半導体業界にとって大きな課題となっています。

- 継続的なロシア・ウクライナ紛争や中国の「ゼロ・トレランス政策」は、世界のインフレの大幅な上昇を招き、電子部品業界を含む複数のセクターに影響を与え、ロジック、リニア、ディスクリート、先端アナログ、受動部品の価格上昇につながり、調査対象市場の成長に悪影響を与えています。

ディスクリート半導体市場動向

自動車セグメントが大きな成長を遂げる見込み

- ダイオードやトランジスタなどのディスクリート半導体は、電力の流れを管理し、エネルギー損失を効率的に最小化するために、これらのシステムで利用されています。そのため、自動車産業におけるディスクリート半導体の需要は、自動車の電動化に重点が置かれるようになったことが原動力となっています。

- 自律走行とADAS技術は自動車産業に革命をもたらし、リアルタイムのデータ処理、センサーフュージョン、車両制御を可能にする高度なエレクトロニクスとディスクリート半導体を必要としています。これらのシステムは、正確で信頼性の高い動作を保証するために、高エネルギーで電力効率の高いデバイスに大きく依存しています。

- ディスクリート半導体は、アダプティブ・クルーズ・コントロール、レーン・キーピング・アシスト、衝突回避などの自律走行機能を実現する上で極めて重要です。自律走行やADAS技術に対する需要の急増は、結果として自動車産業における高エネルギーで電力効率の高いデバイスの必要性を高めています。

- さらに、EVへの移行に伴い、SiCベースのインバータ・プロトタイプを製造する自動車会社の数がここ数年で急速に増加しています。この分野では、SiCパワーMOSFET、ダイオード、モジュールの主な用途は、車載電気自動車(EV)充電器、DC/DCコンバータ、ドライブトレイン・インバータです。プラグインハイブリッドEVやBEVは、家庭や公共の充電ステーションで車載充電器を使用して車載バッテリーに燃料を補給します。

- さらに、IEAが強調しているように、世界の自動車産業は大きな変革期を迎えており、その影響はエネルギー部門にも及ぶ可能性があります。予測によると、電動化の進展により、2030年までに1日あたり500万バレルの石油が不要になると予想されています。

中国が市場をリードする見込み

- 中国のディスクリート半導体市場は、国内の産業数の増加と、投資収益率を高めるためのオートメーションとの統合により、大幅な成長を遂げています。中国は世界最大の製造業を擁し、市場需要に大きく貢献しています。中国の製造企業は、業務の最適化と高度化のために4.0ソリューションの採用を優先しており、それによって市場の拡大が促進されています。

- 同国の半導体エコシステム強化に向けた政府のイニシアティブの成長と、自動車および民生用電子機器の世界的生産国としての同国の台頭は、市場の成長を支えると思われます。

- 同国では、自動車製造におけるディスクリート半導体デバイスの需要が高まっているため、市場の成長は自動車分野に大きく影響されると予想されます。例えば、2024年1月、中国自動車工業協会は、中国の自動車産業が年間生産・販売台数3,000万台を突破し、顕著なマイルストーンを達成したと発表しました。これは自動車市場の巨大な成長の可能性を明確に示しています。

- 中国の自動車部門は著しい成長を遂げ、世界の自動車市場における主要企業としての地位を確固たるものにしました。中国政府は、自動車産業を自動車部品分野とともに国家経済の重要な柱と考えています。

- EVの人気は世界的に高まっています。中国は世界的に電気自動車を導入している主要国です。同国の第13次5ヵ年計画では、ハイブリッド車や電気自動車など、環境に配慮した輸送ソリューションの開発を推進し、同国の輸送部門を発展させています。

- 2060年までにカーボンニュートラルを達成するという政府の取り組みは、電気自動車市場を含む様々な分野の成長を活用することで、ディスクリート半導体の必要性を高めると予測されています。中国の新エネルギー自動車産業開発計画(2021-2035)によると、電気自動車は2025年までに25%の市場シェアを獲得する可能性があります。

- そのため、中国は電気自動車の普及を奨励するため、より積極的な施策を実施しており、その結果、電気自動車で幅広く利用されるディスクリート半導体の採用が加速しています。2023年8月、CAAMは、中国が58万9,000台のバッテリー電気自動車(BEV)を製造したと報告しました。また、同月に中国で生産されたプラグインハイブリッド車(PHEV)は25万4,000台で、25万3,000台が乗用PHEV、1,000台が商用PHEVでした。

ディスクリート半導体産業の概要

ディスクリート半導体市場は細分化されており、ABB Ltd、ON Semiconductor Corporation、Infineon Technologies AG、STMicroelectronics NV、Toshiba Electronic Devices &Storage Corporation、NXP Semiconductors NV(Qualcommが買収予定)などの有力企業が存在します。市場各社は、消費者の複雑で進化する要求に応えるため、先進的で包括的な製品の革新に努めています。

- 2024年3月:インフィニオンは、新しい先進MOSFET技術OptiMOS 7 80 Vの最初の製品を発表しました。IAUCN08S7N013は、電力密度が大幅に向上しており、汎用性が高く、堅牢で大電流のSSO8 5 x 6 mm2 SMDパッケージで提供されます。OptiMOS 780 Vは、今後の48 Vボード・ネット・アプリケーションに完全に適合します。この製品は、EVの車載用DC-DCコンバータ、48 Vモーター制御、例えば電動パワーステアリング(EPS)、48 Vバッテリースイッチ、電動2輪車および3輪車など、要求の厳しい車載アプリケーションに必要な高性能、高品質、および堅牢性のために特別に設計されています。

- 2024年2月:オンセミは、最先端のフィールドストップ7(FS7)絶縁ゲートバイポーラトランジスタ(IGBT)技術を採用した1200V SPM31インテリジェントパワーモジュール(IPM)を発表しました。優れた効率とコンパクトな設計で知られるこれらのIPMは、より高い電力密度を誇り、最終的には同業他社と比較してシステム全体のコスト削減につながります。これらの最適化されたIGBTを活用することで、SPM31 IPMは、特にヒートポンプ、業務用HVACシステム、サーボモーター、各種産業用ポンプやファンなどの三相インバータードライブのようなアプリケーションでスイートスポットを見つけることができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン/サプライチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 自動車・エレクトロニクス分野における高エネルギー・省電力デバイスの需要増加

- グリーンエネルギー発電の需要増加が市場を牽引

- 市場抑制要因

- 集積回路の需要増加

第6章 市場セグメンテーション

- デバイスタイプ別

- ダイオード

- 小信号トランジスタ

- パワートランジスタ

- MOSFETパワートランジスタ

- IGBTパワートランジスタ

- その他パワートランジスタ

- 整流器

- サイリスタ

- 業界別

- 自動車

- コンシューマーエレクトロニクス

- 通信機器

- 産業

- その他業界別

- 地域別

- 米国

- 欧州

- 日本

- 中国

- 韓国

- 台湾

第7章 競合情勢

- 企業プロファイル

- ABB Ltd

- On Semiconductor Corporation

- Infineon Technologies AG

- STMicroelectronics NV

- Toshiba Electronic Devices and Storage Corporation

- NXP Semiconductors NV

- Diodes Incorporated

- Nexperia BV

- Semikron Danfoss Holding A/S(Danfoss A/S)

- Eaton Corporation PLC

- Hitachi Energy Ltd(Hitachi Ltd)

- Mitsubishi Electric Corporation

- Fuji Electric Co Ltd

- Analog Devices Inc.

- Vishay Intertechnology Inc.

- Renesas Electronics Corporation

- Rohm Co. Ltd

- Microchip Technology

- Qorvo Inc.

- Wolfspeed Inc.

- Texas Instrument Inc.

- Littelfuse Inc

- WeEn Semiconductors

第8章 投資分析

第9章 市場機会と今後の動向

The Discrete Semiconductor Market size is estimated at USD 35.51 billion in 2025, and is expected to reach USD 49.00 billion by 2030, at a CAGR of 6.65% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 427.21 billion units in 2025 to 544.99 billion units by 2030, at a CAGR of 4.99% during the forecast period (2025-2030).

Key Highlights

- As new applications emerge and existing technologies evolve, the demand for more advanced and efficient semiconductors increases. Advancements such as miniaturization, increased power efficiency, and improved performance open new possibilities for integrating semiconductors into various devices and systems. Innovations in areas like the Internet of Things (IoT), artificial intelligence (AI), and autonomous vehicles drive the demand for discrete semiconductors.

- Additionally, the rising demand for high-energy and power-efficient devices in the automotive and electronics segment and the increasing demand for green energy power generation drive the market.

- Furthermore, the global consumer electronics market continues to experience rapid growth, fueled by factors such as rising disposable incomes, changing lifestyles, and technological advancements. Consumer electronics, including smartphones, tablets, wearables, and home appliances, heavily rely on discrete semiconductors. The increasing demand for these devices translates into a higher demand for discrete semiconductors, driving the market's growth.

- However, the market faces several restraints that impact its growth and development. The increasing competition from integrated circuits (ICs) is a significant challenge for the market's growth. ICs offer a compact and cost-effective solution, which led to a decline in the demand for discrete semiconductors. This shift in the market preference poses a significant challenge for the discrete semiconductors industry.

- Continuous Russia-Ukraine conflict, as well as China's "Zero Tolerance Policy," has led to a significant increase in global inflation, impacting multiple sectors, including the electronic components industry, leading to climbing prices of logic, linear, discrete, advanced analog, and passive component, thus negatively impacting the growth of the market studied.

Discrete Semiconductor Market Trends

Automotive Segment Is Expected to Witness Major Growth

- Discrete semiconductors, such as diodes and transistors, are utilized in these systems to manage power flow and minimize energy losses efficiently. The demand for discrete semiconductors in the automotive industry is thus driven by the growing emphasis on vehicle electrification.

- Autonomous driving and ADAS technologies are revolutionizing the automotive industry, requiring sophisticated electronics and discrete semiconductors to enable real-time data processing, sensor fusion, and vehicle control. These systems heavily rely on high energy and power-efficient devices to ensure precise and reliable operation.

- Discrete semiconductors are crucial in enabling autonomous driving functions like adaptive cruise control, lane-keeping assist, and collision avoidance. The surge in demand for autonomous driving and ADAS technologies has consequently driven the need for high-energy and power-efficient devices in the automotive industry.

- Furthermore, with the transition to EVs, the number of car companies building SiC-based inverter prototypes has rapidly increased in the past few years. In the sector, the primary applications for SiC power MOSFETs, diodes, and modules are onboard electric vehicle (EV) chargers, DC/DC converters, and drivetrain inverters. Plug-in hybrid EVs and BEVs use onboard chargers to refuel the vehicle battery either at home or at a public charging station.

- Moreover, the global automotive industry is undergoing a significant transformation, as highlighted by the IEA, with potentially far-reaching implications for the energy sector. According to projections, the rise of electrification is anticipated to result in a daily elimination of the need for 5 million barrels of oil by 2030.

China is Expected to Lead the Market

- The discrete semiconductor market in China is experiencing substantial growth due to the increasing number of industries in the country and their integration with automation to enhance return on investment. China has the largest manufacturing industry globally, contributing significantly to market demand. Manufacturing companies in China prioritize adopting 4.0 solutions to optimize and elevate their operations, thereby propelling market expansion.

- The growth of governmental initiatives in strengthening the country's semiconductor ecosystem and the country's emergence as a global producer of automotive and consumer electronic sectors would support the market's growth.

- The market's growth in the country is expected to be greatly influenced by the automotive segment, as there is a rising demand for discrete semiconductor devices in automotive manufacturing. For instance, in January 2024, the China Association of Automobile Manufacturers announced that China's automobile industry achieved a remarkable milestone, with production and sales surpassing 30 million units annually. This clearly indicates the immense growth potential of the automobile market.

- China's automotive sector experienced significant growth, solidifying the country's position as a key player in the worldwide automotive market. The Chinese government considers the automotive industry, along with its auto parts segment, to be crucial pillars of the nation's economy.

- The popularity of EVs is rising globally. China is a dominant adopter of electric vehicles worldwide. The country's 13th Five-Year Plan promotes the development of green transportation solutions, such as hybrid and electric vehicles, to advance the country's transportation sector.

- The government's efforts to attain carbon neutrality objectives by 2060 are projected to enhance the need for discrete semiconductors by leveraging the growth of various sectors, including the electric vehicle market. According to China's Development Plan for the New Energy Automobile Industry (2021-2035), electric vehicles could capture a 25% market share by 2025.

- Consequently, China is implementing more assertive measures to incentivize the adoption of electric vehicles, thereby expediting the adoption of discrete semiconductors for their extensive utilization in EVs. In August 2023, CAAM reported that China manufactured 589,000 battery electric vehicles (BEVs), comprising 551,000 passenger BEVs and 38,000 commercial BEVs. Additionally, 254,000 plug-in hybrid electric vehicles (PHEVs) were produced in China during the same month, with 253,000 being passenger PHEVs and 1,000 being commercial PHEVs.

Discrete Semiconductor Industry Overview

The discrete semiconductor market is fragmented, with several prominent players, such as ABB Ltd, ON Semiconductor Corporation, Infineon Technologies AG, STMicroelectronics NV, Toshiba Electronic Devices & Storage Corporation, and NXP Semiconductors NV (to be acquired by Qualcomm). The market players strive to innovate advanced and comprehensive products to cater to consumers' complex and evolving requirements.

- March 2024: Infineon introduced the first product in its new advanced MOSFET technology OptiMOS 7 80 V. The IAUCN08S7N013 features a significantly increased power density and is available in the versatile, robust, and high-current SSO8 5 x 6 mm2 SMD package. The OptiMOS 780 V offering perfectly matches the upcoming 48 V board net applications. It is designed specifically for the high performance, high quality, and robustness needed for demanding automotive applications like automotive DC-DC converters in EVs, 48 V motor control, for instance, electric power steering (EPS), 48 V battery switches, and electric two- and three-wheelers.

- February 2024: Onsemi unveiled its 1200 V SPM31 Intelligent Power Modules (IPMs), showcasing the cutting-edge Field Stop 7 (FS7) Insulated Gate Bipolar Transistor (IGBT) technology. These IPMs, known for their superior efficiency and compact design, boast a higher power density, ultimately translating to a reduced overall system cost compared to their industry counterparts. Leveraging these optimized IGBTs, the SPM31 IPMs find their sweet spot in applications like three-phase inverter drives, notably in heat pumps, commercial HVAC systems, servo motors, and various industrial pumps and fans.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain / Supply Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for High-energy and Power-efficient Devices in the Automotive and Electronics Segment

- 5.1.2 Increasing Demand for Green Energy Power Generation Drives the Market

- 5.2 Market Restraints

- 5.2.1 Rising Demand for Integrated Circuits

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 Diode

- 6.1.2 Small Signal Transistor

- 6.1.3 Power Transistor

- 6.1.3.1 MOSFET Power Transistor

- 6.1.3.2 IGBT Power Transistor

- 6.1.3.3 Other Power Transistor

- 6.1.4 Rectifier

- 6.1.5 Thyristor

- 6.2 By End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Consumer Electronics

- 6.2.3 Communication

- 6.2.4 Industrial

- 6.2.5 Other End-user Verticals

- 6.3 By Geography

- 6.3.1 United States

- 6.3.2 Europe

- 6.3.3 Japan

- 6.3.4 China

- 6.3.5 South Korea

- 6.3.6 Taiwan

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 On Semiconductor Corporation

- 7.1.3 Infineon Technologies AG

- 7.1.4 STMicroelectronics NV

- 7.1.5 Toshiba Electronic Devices and Storage Corporation

- 7.1.6 NXP Semiconductors NV

- 7.1.7 Diodes Incorporated

- 7.1.8 Nexperia BV

- 7.1.9 Semikron Danfoss Holding A/S (Danfoss A/S)

- 7.1.10 Eaton Corporation PLC

- 7.1.11 Hitachi Energy Ltd (Hitachi Ltd)

- 7.1.12 Mitsubishi Electric Corporation

- 7.1.13 Fuji Electric Co Ltd

- 7.1.14 Analog Devices Inc.

- 7.1.15 Vishay Intertechnology Inc.

- 7.1.16 Renesas Electronics Corporation

- 7.1.17 Rohm Co. Ltd

- 7.1.18 Microchip Technology

- 7.1.19 Qorvo Inc.

- 7.1.20 Wolfspeed Inc.

- 7.1.21 Texas Instrument Inc.

- 7.1.22 Littelfuse Inc

- 7.1.23 WeEn Semiconductors