|

市場調査レポート

商品コード

1550331

欧州のディスクリート半導体:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Europe Discrete Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のディスクリート半導体:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

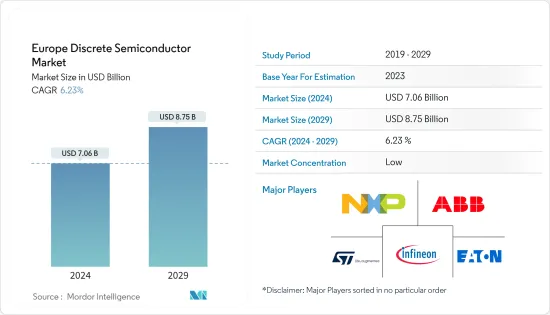

欧州のディスクリート半導体市場規模は、2024年に70億6,000万米ドルと推定、2029年には87億5,000万米ドルに達すると予測、予測期間(2024-2029)のCAGRは6.23%で成長します。

主なハイライト

- 欧州には、ABB Ltd、Infineon Technologies AG、STMicroelectronics NV、NXP Semiconductors NV、Nexperia、Eaton Corporationなど、さまざまなディスクリート半導体企業やベンダーが存在します。また、同地域は主要な製造拠点としても機能しており、産業用および車載用ディスクリート半導体の旺盛な需要につながっています。

- この地域のディスクリート半導体市場は、電気自動車を推進する政府の取り組みにより、有望な可能性を示しています。欧州連合(EU)は2030年までにCO2排出量を1990年比で55%削減する目標を掲げており、英国は2035年までにCO2排出量を70%削減する計画を立てています。こうした取り組みにより、同地域でのEVの普及が促進され、市場の成長が促されると期待されています。

- 欧州自動車工業会(AECA)によると、2023年第2四半期の欧州の電気自動車販売台数は約75万7,800台で、バッテリー電気自動車とプラグインハイブリッド電気自動車の両方を含みます。

- さらに、この地域は、データセンター、クラウドコンピューティング、AIおよびVR技術への大規模な投資のおかげで、予測されるタイムライン中に急速な成長を経験しています。欧州では、社内にITオペレーションを構築する手段を持たない中小規模の組織からデータセンターへの大きなニーズが見られ、通信インフラにおけるディスクリート半導体の需要につながっています。

- 2024年2月、ドイツは欧州諸国の中でデータセンター数が最も多く、クラウド導入競争に積極的に取り組んでいます。CloudSceneによると、ドイツには522のデータセンターがあり、欧州諸国を上回っています。

- 集積回路(IC)やマイクロチップに対する需要の高まりが、市場の成長をさらに妨げる可能性があります。集積回路(IC)またはマイクロチップは、複数の電子回路を1つの半導体基板に集積した電子部品です。対照的に、ディスクリート半導体は、電流の流れの調整、信号の増幅、スイッチングといった特定の機能を実行するように設計された電子部品です。

- いくつかのマクロ経済動向は、市場の成長、経済成長、インフレ、政府支出の優先順位、世界貿易、地政学的力学に影響を与えます。欧州諸国のインフレ率は上昇し、ドイツ、スウェーデン、フランス、英国は2022年1月と比較して大幅に上昇しました。2023年8月までに英国のインフレ率は6.7%に達し、2022年1月の5.5%から上昇しました。こうした発展は、2023年の市場成長を阻害すると予測されます。

欧州のディスクリート半導体市場動向

パワートランジスタセグメントが大きな市場シェアを占める

- MOSFETは金属-酸化膜-半導体電界効果トランジスタとしても知られ、ディスクリート半導体、デジタルロジック、集積回路(IC)、薄膜トランジスタ(TFT)LCDで頻繁に利用されています。この特殊なタイプのトランジスタは、電子信号の増幅やスイッチング用に設計されています。

- MOSFETパワー・トランジスタは、電気自動車(EV)の最適な動作に不可欠です。MOSFETパワー・トランジスタは、モーター駆動システム、バッテリー管理システム、および補助システム用DC-DCコンバーターに使用されています。国内ではEVの普及が進んでおり、市場の拡大が見込まれています。

- 自動車分野は、さまざまな用途でシリコンMOSFETディスクリート半導体に大きく依存しています。これらのMOSFETは、電子制御ユニット(ECU)、バッテリー管理システム、モーター制御ユニット、車載照明システムなどで利用されています。MOSFETは高電圧・高電流に対応し、耐久性に優れているため、自動車の厳しい条件下で最良の選択肢となっています。

- 欧州自動車工業会(ACEA)の報告書によると、2023年の欧州連合の自動車市場は2022年から13.9%増加し、通年の総販売台数は1,050万台に達しました。

- さらに、市場は、MOSFETにSiCを組み込むことによる多くの利点のために、製品の発売が顕著に増加しており、このセグメントに大きな影響を与えています。例えば、Nexperiaは2023年11月、3ピンTO-247パッケージでRDS(on)値が40mホ゜ューと80mホ゜ューの2つの1200Vディスクリートデバイスを発売し、初の炭化ケイ素(SiC)MOSFETを発表しました。この製品は、電気自動車の充電ステーション、無停電電源装置、太陽エネルギー貯蔵システムのインバータなど、さまざまな産業用アプリケーションにおいて、より幅広い高性能SiC MOSFETに対する市場ニーズの高まりに対応するものです。

ドイツが大きな市場シェアを占める見込み

- ドイツ貿易投資総省(GTAI)によると、ドイツは欧州における主要な半導体生産拠点です。同部門は雇用者数で第2位を占めています。ドイツは半導体製造部門を強化し、2030年までに世界の半導体生産のかなりの部分を欧州で確立することを目指しています。目標は、世界の半導体生産の少なくとも20%に達することです。

- さらに、ドイツの連邦大臣は、国の製造部門の競争力を強化するための包括的な青写真である「産業戦略2030」を発表しました。これらの新たな政策とイニシアチブは、工業生産を後押しし、調査対象の市場にとって明るい展望を描くものです。

- さらに、特にドイツは、フォルクスワーゲンAGやダイムラーAGのような主要製造企業の存在により、重要な自動車ハブとして世界的に際立っています。ドイツの自動車産業は、スマート技術を統合し、世界の自動車産業の技術革新をリードしてきました。

- 企業は電気自動車技術に注力しており、ハイブリッド車や電気自動車の台頭が同国の自動車部門の拡大に拍車をかけると期待しています。これは欧州のディスクリート半導体市場の成長にプラスの影響を与えると予想されます。

- 同様に、VDAの報告によると、2023年のドイツ車の生産台数は約412万台で、2022年の340万台から増加しています。こうした動向が市場需要の増加を後押ししています。

欧州のディスクリート半導体産業の概要

欧州のディスクリート半導体市場は断片化されており、複数のプレーヤーで構成されています。同市場に参入している企業は、新製品の投入、事業の拡大、戦略的買収・合併、提携、協力関係の締結などにより、市場での存在感を高めようと絶えず努力しています。主要ベンダーには、ABB Ltd.、Infineon Technologies AG、STMicroelectronics NV、NXP Semiconductors NV、Eaton Corporation PLCなどがあります。

2024年6月、オンセミは、欧州および世界の顧客向けの先進的なパワー半導体のサプライチェーンを強化するため、数年間で最大20億米ドルの投資を計画しています。同社は、垂直統合型の炭化ケイ素(SiC)製造施設をチェコ共和国に建設する予定です。この工場は、電気自動車、再生可能エネルギーシステム、AIデータセンターのエネルギー効率向上に不可欠なオンセミのインテリジェント・パワー半導体の生産に特化する予定です。

2024年5月、インフィニオン・テクノロジーズはSiC MOSFETの開発範囲を650V以下の電圧にまで拡大しました。CoolSiCMOSFET 400Vファミリーの最新ラインアップは第2世代(G2)技術に基づくもので、今年初めに発売されました。このMOSFETの新ラインナップは、AIサーバーのAC/DCステージ向けに特化したもので、インフィニオンの最近のPSUロードマップと一致しています。サーバー・アプリケーション以外にも、これらのデバイスは、インバーター・モーター制御、ソーラー・エネルギー貯蔵システム、SMPS、および住宅環境のソリッド・ステート・サーキット・ブレーカーにも適しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 自動車・エレクトロニクス分野における高エネルギー・省電力デバイスの需要増加

- グリーンエネルギー発電の需要増加が市場を牽引

- 市場の課題

- 集積回路の需要増加

第6章 市場セグメンテーション

- タイプ別

- ダイオード

- 小信号トランジスタ

- パワートランジスタ

- MOSFETパワートランジスタ

- IGBTパワートランジスタ

- その他パワートランジスタ

- 整流器

- サイリスタ

- 業界別

- 自動車

- 民生用電子機器

- 通信機器

- 産業用

- その他業界別

- 国別

- 英国

- ドイツ

- フランス

第7章 競合情勢

- 企業プロファイル

- ABB Ltd

- On Semiconductor Corporation

- Infineon Technologies AG

- STMicroelectronics NV

- Toshiba Electronic Devices and Storage Corporation

- NXP Semiconductors NV

- Diodes Incorporated

- Nexperia BV

- Semikron Danfoss Holding A/S(Danfoss A/S)

- Eaton Corporation PLC

- Hitachi Energy Ltd.(Hitachi Ltd.)

- Texas Instrument Inc.

- Wolfspeed Inc.

- Microchip Technology

- Renesas Electronics Corporation

- Mitsubishi Electric Corporation

- Analog Devices, Inc.

- Vishay Intertechnology Inc.

- Rohm Co. Ltd

- Littelfuse Inc

第8章 投資分析

第9章 市場機会と今後の動向

The Europe Discrete Semiconductor Market size is estimated at USD 7.06 billion in 2024, and is expected to reach USD 8.75 billion by 2029, growing at a CAGR of 6.23% during the forecast period (2024-2029).

Key Highlights

- Europe hosts various discrete semiconductor companies and vendors, including ABB Ltd, Infineon Technologies AG, STMicroelectronics NV, NXP Semiconductors NV, Nexperia, and Eaton Corporation. It also serves as a major manufacturing hub, leading to a strong demand for industrial and automotive-grade discrete semiconductors within the area.

- The discrete semiconductor market in the region shows promising potential due to government initiatives promoting electric vehicles. The European Union has set a target to decrease CO2 emissions by 55% from 1990 levels by 2030, while the United Kingdom plans to reduce carbon emissions by 70% by 2035. These initiatives are expected to boost the adoption of EVs in the region, thereby stimulating the market's growth.

- According to the European Automobile Manufacturers' Association (AECA), Europe witnessed approximately 757,800 electric vehicle sales in the second quarter of 2023, encompassing both battery electric vehicles and plug-in hybrid electric vehicles.

- Additionally, the region is experiencing rapid growth during the projected timeline thanks to significant investments in data centers, cloud computing, and AI and VR technologies. Europe is witnessing a substantial need for data centers from small and medium-sized organizations that do not have the means to establish their in-house IT operations, leading to a demand for discrete semiconductors in communication infrastructure.

- In February 2024, Germany led all European countries with the highest number of data centers and was actively engaged in the race for cloud adoption. According to CloudScene, Germany is home to 522 data centers, outpacing its European counterparts.

- Rising demand for integrated circuits (IC) or microchips may further hamper the market's growth. Integrated circuits (IC), or microchips, are electronic components that integrate multiple electronic circuits onto a single semiconductor substrate. In contrast, discrete semiconductors are electronic components designed to carry out specific functions like regulating current flow, amplifying signals, and switching.

- Several macroeconomic trends affect market growth, economic growth, inflation, government spending priorities, global trade, and geopolitical dynamics. The inflation rates in European countries rose, with Germany, Sweden, France, and the United Kingdom witnessing a significant increase compared to January 2022. By August 2023, the inflation rate in the United Kingdom reached 6.7%, up from 5.5% in January 2022. These developments were anticipated to impede the market's growth in 2023.

Europe Discrete Semiconductor Market Trends

Power Transistor Segment Holds the Significant Market Share

- A MOSFET, also known as a metal-oxide-semiconductor field-effect transistor, is frequently utilized in discrete semiconductors, digital logic, integrated circuits (ICs), and thin-film transistor (TFT) LCDs. This particular type of transistor is designed for amplifying or switching electronic signals.

- MOSFET power transistors are essential for the optimal operation of electric vehicles (EVs). They are used in motor drive systems, battery management systems, and DC-DC converters for auxiliary systems. The increasing popularity of EVs in the country is expected to propel the expansion of the market.

- The automotive sector depends significantly on silicon MOSFET discrete semiconductors for various purposes. These MOSFETs are utilized in electronic control units (ECUs), battery management systems, motor control units, and automotive lighting systems. Their capacity to manage high voltages and currents and their durability position them as the top choice in challenging automotive conditions.

- In 2023, the European Union car market witnessed a notable increase of 13.9% from 2022, leading to a total sales volume of 10.5 million units for the whole year, as per the European Automobile Manufacturers' Association (ACEA) report.

- Furthermore, the market has witnessed a notable increase in product launches due to the numerous advantages of incorporating SiC in MOSFETs, significantly impacting the segment. For instance, in November 2023, Nexperia introduced its initial silicon carbide (SiC) MOSFETs through the launch of two 1200 V discrete devices in 3-pin TO-247 packaging with RDS(on) values of 40 mΩ and 80 mΩ. This product caters to the growing market need for a wider range of high-performance SiC MOSFETs in various industrial applications, such as electric vehicle charging stations, uninterruptible power supplies, and inverters in solar energy storage systems.

Germany is Expected to Hold Significant Market Share

- Germany has been identified as the leading semiconductor production center in Europe, according to Germany Trade & Invest (GTAI). The sector holds the second position in terms of employment figures. Germany aims to strengthen its semiconductor manufacturing sector to establish a substantial portion of the global semiconductor production in Europe by 2030, as outlined in an official government document. The goal is to reach at least 20% of global semiconductor production.

- Furthermore, Germany's Federal Minister has rolled out the Industrial Strategy 2030, a comprehensive blueprint to bolster the nation's manufacturing sector's competitiveness. These new policies and initiatives are set to boost industrial production and paint a positive outlook for the market under study.

- Moreover, Germany, in particular, stands out globally as a significant automotive hub, thanks to the presence of key manufacturing companies like Volkswagen AG and Daimler AG. The German automotive industry has been leading technological innovations in the global automotive industry, integrating smart technologies.

- Companies are focusing on electric vehicle technologies, expecting the rise of hybrid and electric vehicles to fuel the expansion of the country's automotive sector. This is expected to positively affect the European discrete semiconductors market's growth.

- Similarly, the VDA reported that approximately 4.12 million German vehicles were manufactured in 2023, a rise from the 3.4 million cars produced in 2022. These trends are fueling an increase in market demand.

Europe Discrete Semiconductor Industry Overview

The Europe discrete semiconductor market is fragmented and consists of several players. Companies in the market continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic acquisitions and mergers, partnerships, and collaborations. Some of the major vendors include ABB Ltd., Infineon Technologies AG, STMicroelectronics NV, NXP Semiconductors NV, Eaton Corporation PLC, and many more.

In June 2024, Onsemi planned to invest a maximum of USD 2 billion over several years to strengthen the advanced power semiconductor supply chain for its European and global customers. The company intends to construct a vertically integrated silicon carbide (SiC) manufacturing facility in the Czech Republic. This plant is expected to specialize in producing Onsemi's essential intelligent power semiconductors, which are vital in improving energy efficiency in electric vehicles, renewable energy systems, and AI data centers.

In May 2024, Infineon Technologies broadened its SiC MOSFET development to cover voltages under 650 V. The CoolSiCMOSFET 400 V family's latest addition is based on the second-generation (G2) technology and was launched earlier this year. This new lineup of MOSFETs is tailored explicitly for the AC/DC stage of AI servers, which aligns with Infineon's recent PSU roadmap. Apart from server applications, these devices are also suitable for inverter motor control, solar and energy storage systems, SMPS, and solid-state circuit breakers in residential environments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for High-energy and Power-efficient Devices in the Automotive and Electronics Segment

- 5.1.2 Increasing Demand for Green Energy Power Generation Drives the Market

- 5.2 Market Challenges

- 5.2.1 Rising Demand for Integrated Circuits

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Diode

- 6.1.2 Small Signal Transistor

- 6.1.3 Power Transistor

- 6.1.3.1 MOSFET Power Transistor

- 6.1.3.2 IGBT Power Transistor

- 6.1.3.3 Other Power Transistors

- 6.1.4 Rectifier

- 6.1.5 Thyristor

- 6.2 By End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Consumer Electronics

- 6.2.3 Communication

- 6.2.4 Industrial

- 6.2.5 Other End-user Verticals

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 On Semiconductor Corporation

- 7.1.3 Infineon Technologies AG

- 7.1.4 STMicroelectronics NV

- 7.1.5 Toshiba Electronic Devices and Storage Corporation

- 7.1.6 NXP Semiconductors NV

- 7.1.7 Diodes Incorporated

- 7.1.8 Nexperia BV

- 7.1.9 Semikron Danfoss Holding A/S (Danfoss A/S)

- 7.1.10 Eaton Corporation PLC

- 7.1.11 Hitachi Energy Ltd. (Hitachi Ltd.)

- 7.1.12 Texas Instrument Inc.

- 7.1.13 Wolfspeed Inc.

- 7.1.14 Microchip Technology

- 7.1.15 Renesas Electronics Corporation

- 7.1.16 Mitsubishi Electric Corporation

- 7.1.17 Analog Devices, Inc.

- 7.1.18 Vishay Intertechnology Inc.

- 7.1.19 Rohm Co. Ltd

- 7.1.20 Littelfuse Inc