|

市場調査レポート

商品コード

1550335

産業用ディスクリート半導体:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Industrial Discrete Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 産業用ディスクリート半導体:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

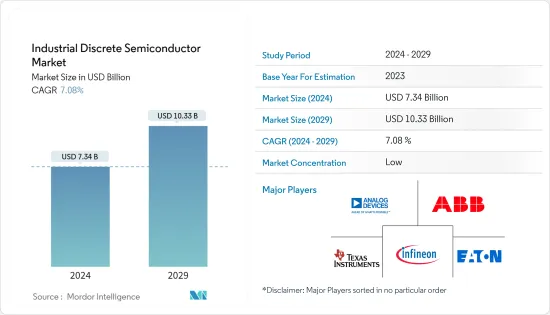

産業用ディスクリート半導体市場規模は、2024年に73億4,000万米ドルと推定され、2029年には103億3,000万米ドルに達すると予測され、予測期間(2024-2029)のCAGRは7.08%で成長します。

主なハイライト

- 産業用ディスクリート半導体は、産業機器、製造装置、機械、UPSなどに広く使用されています。産業分野におけるディスクリート半導体の主な用途は、フォークリフト、無停電電源装置(UPS)システム、ソーラーインバータなどの大型バッテリー駆動アプリケーション、電動工具などの小型電源駆動システムです。また、電力調整、モーター制御、センサー・インターフェースなど、産業プロセスにおける精密な制御と自動化も可能です。

- 産業用システムの効果を最大化するためには、個々のコンポーネントが不可欠です。これらの特定部品は、自動化システムの様々な部分への安定したエネルギー供給を保証します。さらに、産業用オートメーション・システムのスピードと機能性を向上させます。さらに、その適応性により、全体的なパフォーマンスを高めるための簡単なカスタマイズが可能になります。

- 産業用モノのインターネットとインダストリー4.0は、スマートファクトリーオートメーションとも呼ばれる完全なロジスティクスプロセスの進歩、製造、監督において極めて重要です。これらの技術は、インターネットを通じて機械やデバイスの接続を容易にするため、現在、産業部門をリードしています。

- スマート工場は、産業分野におけるもうひとつの顕著な動向です。スマート工場は、生産性を大幅に向上させ、画期的なイノベーションと技術投資を通じて産業界が新しい市場にアクセスできるようにするのに役立ちます。工場の自動化に対する政府投資の増加も、この動向を後押ししています。

- 例えば、米国政府は2023年10月、全米の中小施設におけるスマート製造業を支援するため、2,200万米ドルを投資すると発表しました。大統領の超党派インフラ法(Bipartisan Infrastructure Act)が資金源となる同政権の製造リーダーシップ・プログラムは、米国の炭素排出量の6分の1以上を占める国内製造部門で、スマート製造技術と高性能コンピューティングをより利用しやすくすることを目的としています。

- ICやマイクロチップとしても知られる集積回路の需要が産業分野で高まっていることが、市場の成長をさらに妨げると思われます。ICまたはマイクロチップとも呼ばれる集積回路は、複数の電子回路を1つの半導体基板に集積した電子部品です。一方、ディスクリート半導体は、電流の調整、信号の増幅、スイッチングなど、特定の機能を果たすように設計された電子部品です。

- ロシアとウクライナの紛争は顕著な価格高騰を引き起こし、産業用ディスクリート半導体の製造に不可欠な原材料の入手を制約しています。さらに、米国と中国の緊張激化は、マイクロチップと原材料の不足を招いています。エンジニアリングのサプライチェーンの混乱は広範囲に影響を及ぼし、製品の可用性に影響を与え、業界全体でコストの急激な上昇を引き起こしています。

産業用ディスクリート半導体市場動向

パワートランジスタセグメントが大きな市場シェアを占める

- 産業用ディスクリート半導体は、高い効率と性能向上を実現するため、需要が増加しています。ディスクリート半導体は、大電流や高電圧の管理が必要な状況で重要な位置を占めています。

- IGBTやMOSFETのようなパワー・トランジスタがモーター・ドライブに組み込まれるにつれて、モーター・ドライブの効率は高まっています。特に、炭化ケイ素(SiC)MOSFETは、モーター・ドライブのパワー・ステージでますます使用されるようになっています。IGBTとSiC MOSFETは、その大電流・高電圧定格により、大電力ACパワー段アプリケーションに適しています。

- しかし、SiC MOSFETは、スイッチング周波数要件においてIGBTとは異なります。IGBTが低いスイッチング周波数範囲で動作するのに対し、SiC MOSFETははるかに高いスイッチング周波数範囲で動作します。より高い周波数でスイッチングすることで、電力密度、効率、放熱などのシステム上の利点が得られます。

- 急速に進展するインダストリー4.0の動向は、市場参入企業に多くのチャンスをもたらしており、これがモータ駆動アプリケーションにおけるIGBTのニーズを促進する要因の1つとなっています。多くの企業が、操作を簡素化し、生産量を向上させるために、従来のモーターを先進的なモーター・ドライブに置き換え続けています。

- 例えば2023年7月、Nexperiaは30A NGW30T60M3DFを筆頭とする一連の600Vデバイスを発表し、絶縁ゲートバイポーラトランジスタ(IGBT)市場に参入しました。これらのデバイスは、電力変換、モーター駆動、UPS、20kHzで5kW~20kWのサーボモーター、ロボット、グリッパー、エレベーター、電力インバーター、太陽光発電ストリング、誘導加熱や溶接などの産業用途など、さまざまな用途で電力密度を高めるように設計されています。

- 世界中の産業部門は、顕著な動向として自動化の高まりを目の当たりにしており、その結果、この市場で事業を展開するベンダーに新たな機会が生まれています。産業ロボット連盟によると、産業用ロボットの需要は世界的に安定した成長を遂げています。例えば、前年度の産業用ロボットの世界市場は7%成長し、世界で59万台以上になると予想されています。

- 同様に、vdma.orgによると、昨年、ドイツのロボット産業とオートメーション産業は、国内と輸出を合わせて約175億8,000万米ドルの売上高を記録し、前年より増加すると予測されています。

中国が大きな市場シェアを占める見込み

- 中国経済は長年にわたって大きな変化を経験してきました。中国政府が実施した政策は、経済の高付加価値化を目標に、さまざまな産業の成長を促進する上で重要な役割を果たしてきました。

- 中国における産業部門の急速な拡大は、同国を世界の製造業における重要なプレーヤーとして位置づけました。この分野の成長を引き続き促進するため、中国政府は近年、「メイド・イン・チャイナ2025」構想など、さまざまな戦略を実施しています。このプログラムは、生産効率を向上させ、国際的な品質基準を維持するために、工業企業の先端技術の採用を促進することを目的としています。

- 同様に、2024年4月、中国工業情報化部(MIIT)と他の6つの部門は、産業部門における設備更新を推進するための実施計画を発表しました。

- 中国の製造業における産業設備更新のイニシアチブの範囲は広範で、旧式設備、特に10年以上使用されている工作機械の代替、航空宇宙、太陽エネルギー、バッテリー製造などの重要セクターの設備の強化、産業用ロボットと産業用インターネットの統合、環境の持続可能性を促進するグリーン技術の採用など、さまざまな側面をカバーしています。その結果、こうした発展が新たな機会を生み出すと期待されています。

- 2023年世界ロボット会議報告書によると、中国のロボット産業は目覚ましい発展を遂げています。2022年、同産業の売上高は1,700億元(233億米ドル相当)を超えました。さらに、中国の産業用ロボットの売上高は2022年の世界市場シェアの半分以上を占め、10年連続で世界トップの座を維持しています。

- 中国の特徴は、産業活動の活発化と製造業の増加です。例えば、中国国家統計局のデータによると、2023年、中国の産業部門は国のGDPに約31.7%寄与し、経済成長の主要なエンジンとして機能しています。世界第2位の経済大国である中国が、産業部門だけでドイツの経済全体を上回る価値を生み出していることを強調することは不可欠です。

産業用ディスクリート半導体産業の概要

産業用ディスクリート半導体市場は断片化されており、複数のプレーヤーで構成されています。同市場に参入している企業は、新製品の投入、事業の拡大、戦略的買収・合併、提携、協力関係の締結などにより、市場での存在感を高めようと絶えず努力しています。主なベンダーには、ABB Ltd、Infineon Technologies AG、Texas Instruments Inc.、Analog Devices Inc.、Eaton Corporation PLCなどがあります。

- 2024年6月:Mitsubishi Electric Corporationは、最新製品であるショットキーバリアダイオード(SBD)内蔵炭化ケイ素(SiC)金属-酸化膜-半導体電界効果トランジスタ(MOSFET)モジュールの3.3kV/400Aと3.3kV/200Aモデルの出荷を開始しました。これらのモジュールは、鉄道車両や電力システムなどのヘビーデューティ産業用アプリケーション向けに調整されています。

- 2024年5月:Infineon Technologiesは、SiC MOSFETの開発範囲を650Vより低い電圧にまで拡大しました。今年初めに発表された第2世代(G2)技術に基づくCoolSiCMOSFET 400Vファミリーの導入は、同社の最新製品です。このMOSFETの新ラインナップは、インフィニオンの最近のPSUロードマップに沿った、AIサーバーのAC/DCステージに特化したものです。サーバー・アプリケーション以外にも、これらのデバイスはインバーター・モーター制御、ソーラー・エネルギー貯蔵システム、およびSMPSにおいても目的を果たします。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 産業オートメーションにおける高エネルギー・高電力効率デバイスの需要増加

- 産業分野におけるオートメーションとロボティクスの採用増加

- 市場の課題

- 集積回路の需要増加

第6章 市場セグメンテーション

- タイプ別

- ダイオード

- 小信号トランジスタ

- パワートランジスタ

- MOSFETパワートランジスタ

- IGBTパワートランジスタ

- その他パワートランジスタ

- 整流器

- サイリスタ

- 地域別

- 米国

- 欧州

- 日本

- 中国

- 韓国

- 台湾

第7章 競合情勢

- 企業プロファイル

- ABB Ltd

- On Semiconductor Corporation

- Infineon Technologies AG

- STMicroelectronics NV

- Toshiba Electronic Devices and Storage Corporation

- NXP Semiconductors NV

- Diodes Incorporated

- Nexperia BV

- Semikron Danfoss Holding A/S(Danfoss A/S)

- Eaton Corporation PLC

- Hitachi Energy Ltd(Hitachi Ltd)

- Texas Instrument Inc.

- Wolfspeed Inc.

- Microchip Technology

- Renesas Electronics Corporation

- Mitsubishi Electric Corporation

- Analog Devices Inc.

- Vishay Intertechnology Inc.

- Rohm Co. Ltd

- Littelfuse Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The Industrial Discrete Semiconductor Market size is estimated at USD 7.34 billion in 2024, and is expected to reach USD 10.33 billion by 2029, growing at a CAGR of 7.08% during the forecast period (2024-2029).

Key Highlights

- Industrial discrete semiconductors are widely used in industrial equipment, manufacturing equipment and machines, UPS, etc. The primary use of discrete semiconductors in the industrial sector is in large battery-driven applications, such as forklifts, uninterruptible power supply (UPS) systems, solar inverters, and smaller power-driven systems, like power tools. They also enable precise control and automation in industrial processes, such as power regulation, motor control, and sensor interfacing.

- It is essential to have individual components to maximize the effectiveness of industrial systems. These particular components guarantee a consistent energy supply to various parts of automated systems. Moreover, they boost the speed and functionality of industrial automation systems. In addition, their adaptability allows for simple customization to enhance overall performance.

- The industrial Internet of Things and Industry 4.0 is pivotal in advancing, manufacturing, and supervising the complete logistics process, also called smart factory automation. These technologies are currently leading the way in the industrial sector, as they facilitate the connection of machinery and devices through the internet.

- Smart factories are another prominent trend in the industrial sector. Smart factories help generate significant productivity gains and help industries make new markets accessible through breakthrough innovations and technological investments. The rising government investment in factory automation also supports the trend.

- For instance, in October 2023, the government of the United States announced that it would invest USD 22 million to support smart manufacturing at small and medium-sized facilities across the nation. The administration's Manufacturing Leadership Program, funded by the President's Bipartisan Infrastructure Act, aims to make smart manufacturing technologies and high-performance computing more available in the domestic manufacturing sector, accounting for more than one-sixth of the US carbon emissions.

- Rising demand for integrated circuits, also known as ICs or microchips, in the industrial sector will further hamper the market's growth. Integrated circuits, also known as ICs or microchips, are electronic components that integrate multiple electronic circuits onto a single semiconductor substrate. In contrast, discrete semiconductors are electronic components designed to carry out specific functions like regulating current flow, amplifying signals, and switching.

- The conflict between Russia and Ukraine has caused a notable price surge, constraining the availability of raw materials essential for manufacturing industrial discrete semiconductors. Additionally, escalating tensions between the United States and China have resulted in shortages of microchips and raw materials. The disturbance in the supply chain for engineering has had widespread implications, impacting product availability and causing a sharp increase in costs throughout the industry.

Industrial Discrete Semiconductor Market Trends

Power Transistor Segment Holds the Significant Market Share

- The demand for discrete semiconductors in the industrial sector is increasing as they offer high efficiency and performance improvements. They hold a crucial position in circumstances that require the management of high currents or voltages.

- The efficiency of motor drives is increasing as power transistors like IGBTs and MOSFETs are incorporated into them. Particularly, silicon carbide (SiC) MOSFETs are increasingly used in the power stage for motor drives. Due to their high current and high voltage ratings, IGBTs and SiC MOSFETs fit well in high-power AC power stage applications.

- SiC MOSFETs, however, differ from IGBTs in the switching frequency requirement. While IGBTs operate in a lower switching frequency range, SiC MOSFETs operate in a much higher switching frequency range. Switching at higher frequencies allows system benefits such as higher power density, efficiency, and heat dissipation.

- The rapidly advancing trend of Industry 4.0 has created a stream of opportunities for market participants, which is one of the factors driving the need for IGBTs in motor drive applications. Many businesses continue replacing conventional motors with advanced motor drives to simplify operations and improve output.

- For instance, in July 2023, Nexperia entered the insulated gate bipolar transistor (IGBT) market by introducing a series of 600 V devices led by the 30 A NGW30T60M3DF. These devices are designed to enhance power density in various applications, including power conversion, motor drives, and industrial uses such as UPS, servo motors ranging from 5kW to 20 kW at 20 kHz, robotics, grippers, elevators, power inverters, photovoltaic strings, and induction heating and welding.

- The industrial sector across the globe is witnessing a rise in automation as a prominent trend, thus creating new opportunities for the vendors operating in the market. According to the Industrial Federation of Robotics, the demand for industrial robots is witnessing stable growth globally. For instance, in the previous year, the global market for industrial robots was expected to grow by 7% to more than 590,000 units worldwide.

- Similarly, according to vdma.org, last year, the German robotics and automation industries were forecast to record a combined domestic and export turnover of around USD 17.58 billion, an increase from the year before that.

China is Expected to Hold the Significant Market Share

- China's economy has experienced substantial changes throughout the years. The policies implemented by the Chinese government have played a crucial role in fostering growth across different industries, with the goal of advancing the economy to higher-value-added activities.

- The rapid expansion of the industrial sector in China has positioned the country as a key player in global manufacturing. To continue fostering growth in this sector, the Chinese government has implemented various strategies in recent years, such as the 'Made in China 2025' initiative. This program aims to promote industrial companies' adoption of advanced technologies to improve production efficiency and uphold international quality standards.

- Similarly, in April 2024, China's Ministry of Industry and Information Technology (MIIT) and six other departments released a notice unveiling the Implementation Plan for Advancing Equipment Renewal in the industrial sector.

- The scope of China's initiative to upgrade industrial equipment in manufacturing is extensive, covering various aspects such as substitution of outdated equipment, particularly machine tools that have been in use for over a decade; enhancement of equipment in critical sectors like aerospace, solar energy, and battery manufacturing; integration of industrial robots and the industrial internet; and adoption of green technology to promote environmental sustainability. As a result, these developments are expected to create new opportunities within the market.

- According to the 2023 World Robot Conference report, China's robotics sector has made remarkable advancements. In 2022, the industry generated a revenue of over 170 billion yuan (equivalent to USD 23.3 billion). Moreover, China's sales of industrial robots accounted for more than half of the global market share in 2022, maintaining its position as the top global leader for ten consecutive years.

- China is characterized by a rise in industrial operations and an increase in manufacturing. For instance, data from the National Bureau of Statistics of China revealed that in 2023, China's industrial sector contributed around 31.7% to the nation's GDP, serving as the main engine of economic growth. It is essential to highlight that China, as the world's second-largest economy, produced more value from its industrial sector alone than the entire economy of Germany.

Industrial Discrete Semiconductor Industry Overview

The industrial discrete semiconductor market is fragmented and consists of several players. Companies in the market continuously try to increase their market presence by introducing new products, expanding their operations, or entering into strategic acquisitions and mergers, partnerships, and collaborations. Some of the major vendors include ABB Ltd, Infineon Technologies AG, Texas Instruments Inc., Analog Devices Inc., Eaton Corporation PLC, and many more.

- June 2024: Mitsubishi Electric Corporation started shipping its newest products: a 3.3kV/400A and a 3.3kV/200A model of a Schottky barrier diode (SBD) integrated silicon carbide (SiC) metal-oxide-semiconductor field-effect transistor (MOSFET) module. These modules are tailored for heavy-duty industrial applications, such as rolling stock and electric power systems.

- May 2024: Infineon Technologies broadened its SiC MOSFET development to cover voltages lower than 650 V. The introduction of the CoolSiCMOSFET 400 V family, based on the second-generation (G2) technology released earlier this year, marks the company's latest offering. This new lineup of MOSFETs is tailored explicitly for the AC/DC stage of AI servers, which is in line with Infineon's recent PSU roadmap. Apart from server applications, these devices also serve a purpose in inverter motor control, solar and energy storage systems and SMPS.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for High-energy and Power-efficient Devices in the Industrial Automation

- 5.1.2 Increasing Adoption of Automation and Robotics in the Industrial Sector

- 5.2 Market Challenges

- 5.2.1 Rising Demand for Integrated Circuits

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Diode

- 6.1.2 Small Signal Transistors

- 6.1.3 Power Transistors

- 6.1.3.1 MOSFET Power Transistors

- 6.1.3.2 IGBT Power Transistors

- 6.1.3.3 Other Power Transistors

- 6.1.4 Rectifier

- 6.1.5 Thyristor

- 6.2 By Geography

- 6.2.1 United States

- 6.2.2 Europe

- 6.2.3 Japan

- 6.2.4 China

- 6.2.5 South Korea

- 6.2.6 Taiwan

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 On Semiconductor Corporation

- 7.1.3 Infineon Technologies AG

- 7.1.4 STMicroelectronics NV

- 7.1.5 Toshiba Electronic Devices and Storage Corporation

- 7.1.6 NXP Semiconductors NV

- 7.1.7 Diodes Incorporated

- 7.1.8 Nexperia BV

- 7.1.9 Semikron Danfoss Holding A/S (Danfoss A/S)

- 7.1.10 Eaton Corporation PLC

- 7.1.11 Hitachi Energy Ltd (Hitachi Ltd)

- 7.1.12 Texas Instrument Inc.

- 7.1.13 Wolfspeed Inc.

- 7.1.14 Microchip Technology

- 7.1.15 Renesas Electronics Corporation

- 7.1.16 Mitsubishi Electric Corporation

- 7.1.17 Analog Devices Inc.

- 7.1.18 Vishay Intertechnology Inc.

- 7.1.19 Rohm Co. Ltd

- 7.1.20 Littelfuse Inc.