|

市場調査レポート

商品コード

1550332

米国のディスクリート半導体:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)United States Discrete Semiconductors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のディスクリート半導体:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

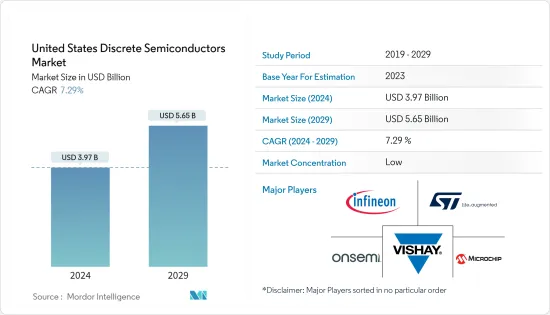

米国のディスクリート半導体市場規模は2024年に39億7,000万米ドルと推定され、2029年には56億5,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは7.29%で成長します。

主なハイライト

- 米国は、ディスクリート半導体を消費する自動車産業やその他の産業が盛んなため、著名な市場のひとつです。半導体産業は、製造、設計、研究のハブとして米国に大きく依存しています。同国の影響力は、電子機器の輸出を刺激し、さまざまなエンドユーザー産業の成長を促進する上で重要な役割を果たしています。家電、通信、自動車を含むこれらの産業は、必須部品としてディスクリート半導体に大きく依存しています。

- 乗用車や先進的な自動車に対する需要の高まりは、国内の自動車産業の大幅な成長につながった。同市場を牽引しているのは、主に人口密度の高さであり、その結果、乗用車の利用が増加しています。その結果、自動車分野では費用対効果の高い一流の部品が求められ続け、市場の成長を牽引しています。

- Wolfspeed Inc.やMicrochip Technology Inc.など、市場の主要プレイヤーの本拠地である同国では、製品の技術革新も著しいです。例えば、2024年6月、Navitas Semiconductorは、AIデータセンター電源、車載充電器(OBC)、高速EVロードサイド・スーパーチャージャー、太陽光/蓄電システム(ESS)向けに、高速スイッチング速度、高効率、電力密度の向上を実現するよう設計されたGen-3 Fast(G3F)650Vおよび1200V SiC MOSFETを発表しました。

- いくつかの要因により、集積回路の需要は最近急増しています。ICはディスクリート半導体に比べ、小型化、高機能化、高性能化など数多くの利点を備えています。このため、自動車から家電、産業分野に至るまで、さまざまなアプリケーションで広く採用されています。ムーアの法則によるトランジスタの微細化など、半導体製造技術の進歩により、ますます複雑化するICを低コストで製造できるようになったことが、市場の成長を抑制しています。

- 米国と中国の緊張の高まりといったマクロ経済的要因が、マイクロチップや原材料の供給不足を招いています。このようなエンジニアリング・サプライチェーンの混乱は、製品の供給力に大きな影響を与え、業界全体のコストを押し上げています。その結果、ディスクリート半導体メーカーはサプライチェーン戦略を見直し、リスクを軽減する必要に迫られています。

米国のディスクリート半導体市場動向

自動車分野が大幅な成長を遂げる

- 自動車分野における電動化へのシフトは、先進的な半導体部品の必要性を高める。米国はEV(電気自動車)市場で重要なプレーヤーとして台頭しており、米国では近年EV販売が大幅に急増しています。コックス・オートモーティブの報告によると、2023年には米国で約119万台のBEV(バッテリー電気自動車)が販売され、テスラ・モデルが総販売台数の55.1%を占めました。2位のフォードは、米国のバッテリー電気自動車販売台数の6.1%を占めるに過ぎなかった。

- 同国では自動車工場の拡張が進んでおり、市場の成長を牽引すると予想されます。例えば、ルシッド・モーターズは2024年1月、アリゾナ州カサ・グランデの組立工場を約300万平方フィート拡張する計画を明らかにしました。この拡張には、新しい製造施設、倉庫、垂直統合型スタンピング施設の追加が含まれます。その結果、拡張される工場の総面積は385万平方フィートを超えることになります。この重要な拡張により、同社は2024年後半に発売予定の待望のSUV「グラビティ」の製造が可能になります。

- 自動車業界では、電力需要の増大に伴い、従来の自動車用電源からより多くの電流を取り出す必要があります。その結果、高性能で効果的な車載用MOSFETの需要が急増しています。さらに、米国ではCO2排出量を抑制するための規制が強化されており、車載用MOSFETの状況は楽観的です。

- 車載用MOSFET(金属-酸化膜-半導体電界効果トランジスタ)の需要急増を支えているのは、高度な車両制御と燃焼技術に対するニーズの高まりです。これらの部品は、現代の自動車エレクトロニクス、特にパワートレイン制御やその他の車両システムにおいて極めて重要です。米国では電気自動車(EV)やハイブリッド車(HEV)の需要が急増しており、自動車市場におけるディスクリート半導体の成長を促進し、イノベーションと事業拡大への道を開いています。

パワートランジスタが大きな市場シェアを占める

- MOSFETの設計や製造など、パワートランジスタの技術的進歩は、高性能MOSFETに対する需要の高まりに後押しされています。MOSFETには、低オン抵抗、高速スイッチング、熱管理の改善といった特長があります。

- 例えば、2024年3月、インフィニオンは新しい先端MOSFET技術の最初の製品であるOptiMOS 7 80 Vを発表しました。この製品は、EVの車載用DC-DCコンバータ、48 Vモーター制御、例えば電動パワーステアリング(EPS)、48 Vバッテリースイッチ、電動2輪車および3輪車のような要求の厳しい車載アプリケーションに必要な高性能、高品質、および堅牢性のために特別に設計されています。

- 2023年12月、インフィニオンテクノロジーズAGは、4.5 kV XHP 3 IGBTモジュールを発表することで、小型化と統合化の要請に応えました。これらのモジュールは、中電圧駆動(MVD)および輸送アプリケーション、特に2レベルおよび3レベルのトポロジーでAC2000V~3300Vで動作するアプリケーションを変革します。

- 米国では、UPS、パワー・コンディショナー、エアコンなど、低電流用途にディスクリートIGBTを使用する家電製品の需要が増加しており、ディスクリートIGBT市場の成長を牽引しています。ディスクリートIGBTは民生品で最も電力損失が少ないことが分かっており、これがこのセグメントの市場成長に影響を与える主要因になると予想されます。

米国のディスクリート半導体産業概要

米国のディスクリート半導体市場は断片化されており、Infineon Technologies AG、STMicroelectronics NV、On Semiconductor Corporation、Vishay Intertechnology Inc.、Microchip Technology Inc.などの大手企業が存在します。同市場のプレーヤーは、パートナーシップ、合併、技術革新、投資、買収などさまざまな市場戦略を採用し、製品ラインナップの充実と持続的な競争優位の獲得に努めています。

2024年1月:Infineon Technologiesがエネルギー貯蔵企業のSinexcel Electricと提携。インフィニオンはこの提携で、Sinexcelに最新の1200V CoolSiC MOSFET半導体デバイスを供給します。これらはインフィニオンの小型1200Vシングルチャンネル絶縁ゲートドライブIC「EiceDRIVER」によって補完され、エネルギー貯蔵システムの効率向上を目指します。SiCパワーソリューションは、今後のグリーンエネルギー生産と蓄電アプリケーションにおいて極めて重要です。

2023年11月ネクスペリアBVは三菱電機と戦略的提携を結び、炭化ケイ素(SiC)MOSFETを共同開発します。この提携により、ネクスペリアと三菱電機は、SiCワイドバンドギャップ半導体のエネルギー効率と性能を次のレベルに押し上げると同時に、高効率のディスクリートパワー半導体に対する急速に高まる需要に応えるために力を合わせた。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 自動車・エレクトロニクス分野における高エネルギー・省電力デバイスの需要増加

- グリーンエネルギー発電の需要増加が市場を牽引

- 市場の課題

- 集積回路需要の増加

- 原材料コストの高騰

第6章 市場セグメンテーション

- タイプ別

- ダイオード

- 小信号トランジスタ

- パワートランジスタ

- MOSFETパワートランジスタ

- IGBTパワートランジスタ

- その他パワートランジスタ

- 整流器

- サイリスタ

- エンドユーザー産業別

- 自動車

- コンシューマーエレクトロニクス

- 通信機器

- 産業

- その他のエンドユーザー産業

第7章 競合情勢

- 企業プロファイル

- Infineon Technologies AG

- STMicroelectronics NV

- On Semiconductor Corporation

- Vishay Intertechnology Inc.

- Microchip Technology Inc.

- Analog Devices Inc.

- Qorvo Inc.

- Diodes Incorporated

- Texas Instrument Inc.

- Wolfspeed Inc.

第8章 投資分析

第9章 市場の将来

The United States Discrete Semiconductors Market size is estimated at USD 3.97 billion in 2024, and is expected to reach USD 5.65 billion by 2029, growing at a CAGR of 7.29% during the forecast period (2024-2029).

Key Highlights

- The United States is one of the prominent markets due to its large automotive and other industries that consume discrete semiconductors. The semiconductor industry dramatically relies on the United States as a manufacturing, design, and research hub. The country's influence plays a crucial role in stimulating the export of electronic equipment and fostering the growth of various end-user industries. These industries, including consumer electronics, communication, and automotive, heavily rely on discrete semiconductors as essential components.

- The rising demand for passenger and advanced vehicles has led to substantial growth in the automotive industry in the country. The market has been primarily driven by the high population density, resulting in an increased utilization of passenger vehicles. Consequently, there is an ongoing requirement for cost-effective and top-notch components in the automotive sector, thus driving the market's growth.

- Being home to some of the major players in the market, such as Wolfspeed Inc. and Microchip Technology Inc., the country also continues to witness significant product innovation. For instance, in June 2024, Navitas Semiconductor introduced the Gen-3 Fast (G3F) 650V and 1200V SiC MOSFETs designed to enhance fast switching speed, high efficiency, and increased power density for AI data center power supplies, on-board chargers (OBCs), fast EV roadside super-chargers, and solar/energy-storage systems (ESS).

- Due to several factors, the demand for integrated circuits has soared recently. ICs offer numerous advantages over discrete semiconductors, such as compactness, increased functionality, and higher performance. This has led to the widespread adoption in various applications, ranging from automotive to consumer electronics and industrial sectors. Advancements in semiconductor manufacturing technologies, such as the miniaturization of transistors through Moore's Law, have enabled the production of increasingly complex ICs at lower costs, thus restraining the market's growth.

- Macroeconomic factors like rising tensions between the United States and China have led to supply shortages in microchips and raw materials. This disruption in the engineering supply chain has significantly impacted product availability, driving up costs industry-wide. Consequently, discrete semiconductor manufacturers have been prompted to reassess their supply chain strategies and reduce risks.

United States Discrete Semiconductors Market Trends

Automotive Sector to Witness a Significant Growth

- The shift toward electrification in the automotive sector drives the need for advanced semiconductor components. With the United States emerging as a critical player in the EV (electric vehicle) market, the nation has witnessed a significant surge in EV sales in recent years. In 2023, Cox Automotive reported that approximately 1.19 million BEVs (battery electric vehicles) were sold in the United States, with Tesla models representing 55.1% of total sales. Ford, the second-ranked automaker, only accounted for 6.1% of US battery electric vehicle sales.

- The rising expansion of automotive plants in the country is expected to drive the market's growth. For instance, in January 2024, Lucid Motors revealed plans to enlarge its Casa Grande, Arizona, assembly plant by approximately 3 million square feet. This expansion encompasses adding a new manufacturing facility, warehouse, and vertically integrated stamping facility. As a result, the expanded plant will encompass a total area exceeding 3.85 million square feet. This crucial expansion will enable the company to manufacture its highly anticipated Gravity SUV, set to be launched in late 2024.

- The automotive sector's escalating power needs necessitate higher current draws from conventional automotive supplies. Consequently, there is a surging demand for proficient and effective automotive MOSFETs. Moreover, with the tightening regulations in the United States to curb CO2 emissions, the landscape for automotive MOSFETs is notably optimistic.

- The rising need for advanced vehicle control and combustion technology is a crucial driver behind the demand surge for Automotive MOSFETs (metal-oxide-semiconductor field-effect transistors). These components are pivotal in contemporary automotive electronics, especially powertrain control and other vehicle systems. The surging demand for electric (EV) and hybrid vehicles (HEV) in the United States is fueling growth in the discrete semiconductors in the automotive market, opening avenues for innovation and business expansion.

Power Transistors to Hold Significant Market Share

- Technological advancements in power transistors, such as MOSFET design and manufacturing, are being propelled by the rising demand for high-performance MOSFETs. These sought-after features include low on-resistance, high-speed switching, and improved thermal management.

- For instance, in March 2024, Infineon introduced the first product in its new advanced MOSFET technology, OptiMOS 7 80 V. The OptiMOS 7 80 V offering perfectly matches the upcoming 48 V board net applications. It is designed specifically for the high performance, high quality, and robustness needed for demanding automotive applications like automotive DC-DC converters in EVs, 48 V motor control, for instance, electric power steering (EPS), 48 V battery switches, and electric two- and three-wheelers.

- In December 2023, Infineon Technologies AG responded to the call for downsizing and integration by introducing the 4.5 kV XHP 3 IGBT modules. These modules are set to transform medium-voltage drives (MVD) and transportation applications, specifically, those operating at 2000 V-3300 V AC in 2, and 3-level topologies.

- In the United States, the increasing demand for consumer electronic appliances like UPSs, power conditioners, air conditioners, etc., which use discrete IGBT types for lower-current applications, is credited with driving the growth of the discrete IGBT market. Discrete IGBTs have been found to have the lowest power losses in consumer goods, which is anticipated to be a key factor influencing the segment's growth in the market.

United States Discrete Semiconductors Industry Overview

The US discrete semiconductors market is fragmented, with the presence of major players like Infineon Technologies AG, STMicroelectronics NV, On Semiconductor Corporation, Vishay Intertechnology Inc., and Microchip Technology Inc. Players in the market are adopting various market strategies such as partnerships, mergers, innovations, investments, and acquisitions to enhance product offerings and gain sustainable competitive advantage.

January 2024: Infineon Technologies partnered with Sinexcel Electric, an energy storage company. Infineon will supply Sinexcel with its latest 1200V CoolSiC MOSFET semiconductor devices in this collaboration. These will be complemented by Infineon's EiceDRIVER compact 1200V single-channel isolated gate drive ICs, which aim to enhance the efficiency of energy storage systems. The SiC power solution is pivotal in upcoming green energy production and storage applications.

November 2023: Nexperia BV partnered strategically with Mitsubishi Electric Corporation to develop silicon carbide (SiC) MOSFETs jointly. Through this partnership, Nexperia and Mitsubishi Electric joined forces to push the energy efficiency and performance of SiC wide bandgap semiconductors to the next level while also responding to the rapidly growing demand for high-efficiency discrete power semiconductors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for High-energy and Power-efficient Devices in the Automotive and Electronics Segment

- 5.1.2 Increasing Demand for Green Energy Power Generation Drives the Market

- 5.2 Market Challenges

- 5.2.1 Rising Demand for Integrated Circuits

- 5.2.2 High Cost of Raw Materials

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Diode

- 6.1.2 Small Signal Transistor

- 6.1.3 Power Transistor

- 6.1.3.1 MOSFET Power Transistor

- 6.1.3.2 IGBT Power Transistor

- 6.1.3.3 Other Power Transistors

- 6.1.4 Rectifier

- 6.1.5 Thyristor

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Consumer Electronics

- 6.2.3 Communication

- 6.2.4 Industrial

- 6.2.5 Other End-user Industries

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Infineon Technologies AG

- 7.1.2 STMicroelectronics NV

- 7.1.3 On Semiconductor Corporation

- 7.1.4 Vishay Intertechnology Inc.

- 7.1.5 Microchip Technology Inc.

- 7.1.6 Analog Devices Inc.

- 7.1.7 Qorvo Inc.

- 7.1.8 Diodes Incorporated

- 7.1.9 Texas Instrument Inc.

- 7.1.10 Wolfspeed Inc.