日本のディスクリート半導体:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)

Japan Discrete Semiconductors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1550334

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

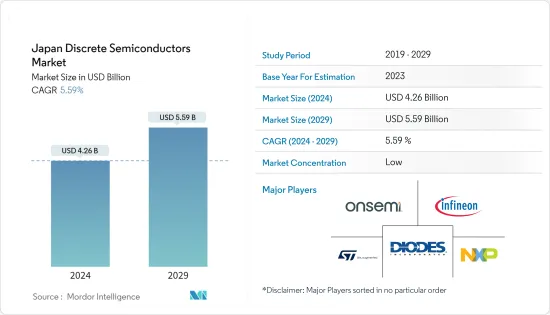

日本のディスクリート半導体市場規模は、2024年に42億6,000万米ドルと推定され、2029年には55億9,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは5.59%で成長すると予測されます。

ディスクリート半導体は、特に車載エレクトロニクス、再生可能エネルギーシステム、民生エレクトロニクスなどの技術進歩において極めて重要です。IoT、電気自動車、スマートデバイスのような新たな動向は、特殊なディスクリート半導体の需要を煽っています。さらに、こうした半導体のメーカーは世界に事業を展開しているため、さまざまな通貨で材料を調達し、販売を行うことが多いです。そのため、為替レートの変動は収益性や競争力に大きな影響を与える可能性があります。

主なハイライト

- ディスクリート半導体、またはディスクリート・コンポーネントやデバイスは、電子回路内で特定の機能を果たすように設計された個々の電子部品で、統合されることなく独立して動作します。ディスクリート半導体の一般的な例としては、ダイオード、トランジスタ、サイリスタなどがあります。これらの部品は通常、回路接続用に2本以上のリード線(ピン)を備えたパッケージに収められています。ディスクリート半導体は、電源や増幅器から制御回路や信号処理に至るまで、エレクトロニクス全般にわたって広範な用途が見出されています。

- ディスクリート半導体は、強化された柔軟性、カスタマイズ性、優れた電力処理能力など、集積回路と比較して大きな利点を提供します。設計者は回路設計と性能を正確に制御し、より高い電圧・電流レベルに対応することができます。しかし、ディスクリート部品は、集積回路に比べて基板スペースが広く、組み立て工程が増える可能性があります。

- さらに、商品価格、特に金属、シリコン、希土類元素などの原材料価格の変動は、ディスクリート半導体の製造コストに直接影響します。こうした変動は利益率に大きな影響を及ぼし、価格戦略の調整が必要となります。

- 効率的な電力管理は、ディスクリート半導体の重要な促進要因のひとつです。先進的なシステムアーキテクチャは、AC-DC電源アダプタの効率を高めると同時に、そのサイズと部品点数を削減しています。さらに、パワー・オーバー・イーサネット(PoE)規格の更新により、より高い電力転送がサポートされるようになり、コネクテッド照明のような革新的なデバイスの開発が促進されています。

- ウェアラブルデバイスは、その基本的な物理学からエンドユーザー体験に至るまで、消費者の普及を促進する上で極めて重要です。ディスクリート半導体企業は、製品設計中に市場動向と課題を注意深く監視することで大きな利益を得ることができ、競争力を維持することができます。移動度が向上し、臨界破壊電界を持つ半導体、特に炭化ケイ素(SiC)の採用が進んでいます。この動向は特にトランジスタ分野で顕著で、ショットキー・バリア・ダイオード(SBD)、接合型電界効果トランジスタ(JFET)、MOSFETトランジスタなどのパワーエレクトロニクス・デバイスにまで及んでいます。

- ロシアのウクライナ侵攻、中国と米国の競争、選挙、イスラエルでの戦争などの地政学的課題は、世界のサプライチェーン、特に伝統産業、防衛、ハイテク分野、航空宇宙、グリーンエネルギーに不可欠な重要原材料に大きな影響を与えています。ロシア・ウクライナ戦争と景気減速は半導体産業に大きな混乱をもたらしました。インフレと金利の上昇は個人消費を減少させ、業界の需要を妨げ、ディスクリート半導体市場の成長鈍化につながりました。

日本のディスクリート半導体市場動向

パワートランジスタが大きな市場シェアを占める見込み

- MOSFETは、主にさまざまな用途で電子信号のスイッチングや増幅に使われる半導体デバイスです。電界効果トランジスタ(FET)に属し、電界を利用して2つの端子間の電流の流れを制御する能力で知られています。低電圧で機能する一方で、素早いスイッチングと最大限の効率を実現します。

- 従来の電力増幅器における電力損失は、入力または出力インピーダンス整合回路を内蔵し、出力電力性能を検証したRFハイパワーMOSFETモジュールの需要を生み出しています。三菱電機などの主要ベンダーは、この新型MOSFETを搭載した900MHzモジュールを来年中に発売し、周波数帯域を拡大する計画です。同社によると、763MHzから870MHz帯で50Wの出力を持ち、総合効率40%のこのモデルは、消費電力の削減と無線通信範囲の拡大に貢献すると予測されています。

- エレクトロニクス業界では、スマートフォン、タブレット、ノートパソコン、スマートウェアラブル、IoT機器など、さまざまな電子機器の需要が急増しています。これらのデバイスは、さまざまな機能のためにパワートランジスタを必要とします。消費者層の拡大と新しい電子機器の継続的なイントロダクションが、パワートランジスタの需要を後押ししています。

- 民生用電子機器セグメントは、国内の大規模な製造現場と、ソニーやパナソニックなどの確立された民生用電子機器企業に支えられて、市場の成長に大きく貢献すると思われます。これにより、民生用電子機器分野で使用される電子部品の製造におけるディスクリート半導体の需要拡大が促進され、日本の市場成長が促進されると思われます。

- さらに、2023年の日本のエレクトロニクス産業は、経済産業省が報告したように、電子部品・デバイスの総生産額が約6兆9,700億円(4,970億米ドル)に達しています。この間の日本のエレクトロニクス産業全体の生産額は約10兆7,000億円(760億米ドル)に達しました。

著しい市場成長が期待される自動車産業

- ディスクリート半導体は、個別の電子機能に合わせて調整され、切り離すことができないため、カーエレクトロニクスを変革する上で極めて重要です。機能を組み合わせる集積回路(IC)とは異なり、ダイオード、トランジスタ、サイリスタなどのディスクリート半導体は自律的に動作し、自動車の機能、安全性、接続性を強化します。このシフトは技術進歩の新時代を告げるものであり、自動車の性能と機能のベンチマークを高めるものです。

- 自動車の需要は、主にディスクリート部品、特にパワー・トランジスタと整流器の市場に拍車をかけています。従来の自動車は何十年もの間、12Vバッテリー・システムに依存してきましたが、現在では最新の自動車の電子的要求の増大を支えるのに苦労しており、よりエネルギー効率の高いソリューションの必要性が浮き彫りになっています。

- 日本政府は2050年までに、日本で新たに販売される自動車をすべて電気自動車かハイブリッド車にするという目標を掲げています。日本政府は、電気自動車用のバッテリーとモーターの進歩を促進するため、民間企業に補助金を提供する意向です。二酸化炭素排出量を削減するため、日本政府は電気自動車(EV)の利用を積極的に推進しており、EVインフラ整備に多額の投資を行っています。EV購入者への政府補助金の結果、日本では、増加する電気自動車に対応するため、EV充電ステーションの数が急増しています。

- さらに、日本自動車販売協会連合会と日本軽自動車二輪車協会が発表したデータによると、2023年には標準サイズの電気自動車(EV)が4万3,991台、日本の有名な軽量軽自動車の電気自動車が4万4,544台販売されます。

日本のディスクリート半導体産業の概要

日本のディスクリート半導体市場は統合されており、STMicroelectronics、Infineon Technologies、NXP Semiconductor、Diodes Incorporatedなどの主要企業が名を連ねています。市場参入企業は、製品ポートフォリオを強化し、持続可能な競争力を確立するために、戦略的にパートナーシップや買収を活用しています。

- 2024年6月:Mitsubishi Electric Corporationは、ウェブベースのサービスを導入する計画を発表しました。このサービスは、新型インバータの設計と検証に関する重要なデータを提供します。このインバーターは、LV100絶縁ゲートバイポーラトランジスタ(IGBT)3個を搭載したモジュールが特徴です。その主な目的は、太陽光発電システムなどの用途に特化した高出力インバータの開発を促進するために顧客を支援することです。インバータのプロトタイプは、LV100産業用IGBTを3個並列に搭載したモジュールで、ハイパワーインバータシステムの標準サイズである100mm x 140mmのコンパクトなフレームに収められています。

- 2024年3月:Infineon Technologiesは、新しいOptiMOS 7 80VパワーMOSFET技術のデビューとなる最新製品IAUCN08S7N013を発表しました。この新製品は、電力密度の顕著な向上を誇り、弾力性のある大電流SSO8 5 x 6 mm2 SMDパッケージに収められています。急成長している48Vボード・ネット・アプリケーション向けに設計されたOptiMOS 7 80Vは、自動車部門に最適です。EV、48 Vモーター制御(電動パワーステアリング(EPS)、48 Vバッテリースイッチ、電動2輪車および3輪車などのアプリケーションを含む)の車載DC-DCコンバータの厳しい基準を満たすように設計されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 自動車・エレクトロニクス分野における高エネルギー・省電力デバイスの需要増加

- グリーンエネルギー発電の需要増加が市場を牽引

- 市場の課題

- 集積回路の需要増加

第6章 市場セグメンテーション

- タイプ別

- ダイオード

- 小信号トランジスタ

- パワートランジスタ

- MOSFETパワートランジスタ

- IGBTパワートランジスタ

- その他パワートランジスタ

- 整流器

- サイリスタ

- 業界別

- 自動車

- 民生用電子機器

- 通信機器

- 産業用

- その他業界別

第7章 競合情勢

- 企業プロファイル

- On Semiconductor Corporation

- Infineon Technologies AG

- STMicroelectronics NV

- NXP Semiconductors NV

- Diodes Incorporated

- Toshiba Electronic Devices & Storage Corporation

- ABB Ltd.

- Nexperia BV

- Semikron Danfoss Holding A/S(Danfoss A/S)

- Eaton Corporation PLC

- Hitachi Energy Ltd.(Hitachi Ltd.)

- Mitsubishi Electric Corp.

- Fuji Electric Co Ltd

- Analog Devices, Inc.

- Vishay Intertechnology Inc.

- Renesas Electronics Corporation

- ROHM Co. Ltd

- Microchip Technology

- Qorvo Inc.

- Wolfspeed Inc.

- Texas Instruments Inc.

- Littelfuse Inc

- WeEn Semiconductors

第8章 投資分析

第9章 市場の将来

目次

The Japan Discrete Semiconductors Market size is estimated at USD 4.26 billion in 2024, and is expected to reach USD 5.59 billion by 2029, growing at a CAGR of 5.59% during the forecast period (2024-2029).

Discrete semiconductors are crucial in technological advancements, especially in automotive electronics, renewable energy systems, and consumer electronics. Emerging trends like IoT, electric vehicles, and smart devices fuel the demand for specialized discrete semiconductors. Moreover, given that manufacturers of these semiconductors have a global presence, they often source materials and conduct sales in various currencies. Consequently, fluctuations in exchange rates can significantly affect their profitability and competitive edge.

Key Highlights

- Discrete semiconductors, or discrete components or devices, are individual electronic components designed to carry out specific functions within electronic circuits that operate independently, without integration. Common examples of discrete semiconductors include diodes, transistors, and thyristors. These components are typically housed in packages featuring two or more leads (pins) for circuit connections. Discrete semiconductors find extensive applications across electronics, from power supplies and amplifiers to control circuits and signal processing.

- Discrete semiconductors provide significant advantages over integrated circuits, including enhanced flexibility, customization, and superior power handling capabilities. They enable designers to precisely control circuit design and performance precisely, accommodating higher voltage and current levels. However, discrete components may necessitate more board space and additional assembly steps compared to integrated circuits.

- Furthermore, fluctuations in commodity prices, particularly in raw materials like metals, silicon, and rare earth elements, directly influence the manufacturing costs of discrete semiconductors. These fluctuations can significantly impact profit margins and necessitate adjustments in pricing strategies.

- Efficient power management is one of the significant driving factors in discrete semiconductors. Advanced system architectures are enhancing the efficiency of AC-DC power adapters while reducing their size and component count. Furthermore, updated power-over-ethernet (PoE) standards now support higher power transfers, facilitating the development of innovative devices such as connected lighting.

- Wearable devices, from their fundamental physics to the end-user experience, are crucial in driving consumer adoption. Discrete semiconductor companies can benefit significantly by closely monitoring market trends and challenges during product design, ensuring they maintain a competitive edge. The adoption of semiconductors with enhanced mobility and critical breakdown fields, particularly Silicon Carbide (SiC), is gaining traction. This trend is especially notable in the transistor range and extends to power electronics devices, including Schottky barrier diodes (SBDs), junction field effect transistors (JFETs), and MOSFET transistors.

- Geopolitical challenges, including the Russian invasion of Ukraine, China-US competition, elections, and the war in Israel, significantly impact the global supply chain, especially critical raw materials vital for traditional industries, defense, high-tech sectors, aerospace, and green energy. The Russia-Ukraine war and economic slowdown caused significant disruption in the semiconductor industry. The increased inflation and interest rates reduced consumer spending, hampered the industry's demand, and led to slow growth in the discrete semiconductor market.

Japan Discrete Semiconductors Market Trends

Power Transistors are Expected to Hold a Significant Market Share

- MOSFETs are semiconductor devices used primarily for switching and amplifying electronic signals in various applications. They belong to the family of field-effect transistors (FETs) and are known for their ability for controlling the flow of current between the two terminals using an electric field. They function at low voltages while providing quick switching and maximum efficiency.

- The power loss in conventional power amplifiers creates demand for RF high-power MOSFET modules that offer a built-in input or output impedance-matching circuit and verified output power performance. Key vendors, such as Mitsubishi Electric, plan to expand the frequency range by launching a 900 MHz module equipped with the new MOSFET in the coming year. According to the company, the model with 50 W power output in the 763 MHz to 870 MHz band and a total efficiency of 40% is projected to help reduce power consumption and increase radio communication range.

- The electronics industry is witnessing a surge in the demand for different electronic devices such as smartphones, tablets, laptops, smart wearables, and IoT devices. These devices require power transistors for various functions. The expanding consumer base and the continuous introduction of new electronic devices drive the demand for power transistors.

- The consumer electronic segment would contribute significantly to the market's growth, supported by the country's large manufacturing landscape and the established consumer electronic companies, including Sony and Panasonic, among others. This would fuel the demand for discrete semiconductor growth in the manufacturing of electronic components used in the consumer electronic segments, which would drive the market growth in Japan.

- Furthermore, in 2023, the electronics industry in Japan witnessed electronic components and devices contributing to a total production value of approximately JPY 6.97 trillion (USD 0.497 trillion), as reported by METI (Japan). The overall production value of the Japanese electronics industry during that period reached around JPY 10.7 trillion (USD 0.076 trillion).

Automotive Industry is Expected to Have a Significant Market Growth

- Discrete semiconductors, tailored for distinct electronic functions and inseparable, are pivotal in transforming automotive electronics. Unlike integrated circuits (ICs), which combine functions, discrete semiconductors, like diodes, transistors, and thyristors, operate autonomously, bolstering automotive capabilities, safety, and connectivity. This shift heralds a new age of technological progress, elevating benchmarks for automotive performance and features.

- Automotive demands are primarily fueling the market for discrete components, particularly power transistors and rectifiers. While traditional vehicles have relied on 12-V battery systems for decades, they are now struggling to support the increased electronic demands of modern cars, highlighting the necessity for more energy-efficient solutions.

- By 2050, the Japanese government has set a target to have all newly sold cars in Japan be electric or hybrid. The country intends to provide subsidies to the private sector to expedite the advancement of batteries and motors for electric-powered vehicles. In an effort to decrease its carbon emissions, the Government of Japan is actively promoting the use of electric vehicles (EVs), leading to significant investments in EV infrastructure development. As a result of government subsidies for EV buyers, Japan has experienced a surge in the number of EV charging stations to accommodate the growing number of electric vehicles.

- Moreover, as per the data released by the Japan Automobile Dealers Association and the Japan Light Motor Vehicle and Motorcycle Association, the year 2023 witnessed the sale of 43,991 standard-size electric vehicles (EVs) and 44,544 electric variants of Japan's renowned lightweight keiminicars.

Japan Discrete Semiconductors Industry Overview

The Japan Discrete Semiconductors Market is consolidated and features key players like STMicroelectronics, Infineon Technologies, NXP Semiconductor, and Diodes Incorporated, among others. Market participants strategically leverage partnerships and acquisitions to bolster their product portfolios and establish a sustainable competitive edge.

- June 2024: Mitsubishi Electric Corporation has announced plans to introduce a web-based service. This service will offer crucial data on the design and validation of the new inverter. The inverter is distinctive, featuring a module housing three LV100 insulated gate bipolar transistors (IGBTs). The primary goal is to assist customers in expediting the development of high-power inverters, specifically for applications like photovoltaic power-generation systems. Notably, the prototype inverter boasts a module that houses three parallel LV100 industrial IGBTs, all within a compact 100mm x 140mm frame, a standard size for high-power inverter systems.

- March 2024: Infineon Technologies introduced its latest product, the IAUCN08S7N013, marking the debut of its new OptiMOS 7 80 V power MOSFET technology. This new offering boasts a notable uptick in power density and comes housed in the resilient and high-current SSO8 5 x 6 mm2 SMD package. Designed for the burgeoning 48 V board net applications, the OptiMOS 7 80 V is primed for the automotive sector. It's engineered to meet the exacting standards of automotive DC-DC converters in EVs, 48 V motor control - including applications like electric power steering (EPS), 48 V battery switches, and electric two- and three-wheelers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand for High-energy and Power-efficient Devices in the Automotive and Electronics Segment

- 5.1.2 Increasing Demand for Green Energy Power Generation Drives the Market

- 5.2 Market Challenges

- 5.2.1 Rising Demand for Integrated Circuits

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Diode

- 6.1.2 Small Signal Transistor

- 6.1.3 Power Transistor

- 6.1.3.1 MOSFET Power Transistor

- 6.1.3.2 IGBT Power Transistor

- 6.1.3.3 Other Power Transistor

- 6.1.4 Rectifier

- 6.1.5 Thyristor

- 6.2 By End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Consumer Electronics

- 6.2.3 Communication

- 6.2.4 Industrial

- 6.2.5 Other End-user Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 On Semiconductor Corporation

- 7.1.2 Infineon Technologies AG

- 7.1.3 STMicroelectronics NV

- 7.1.4 NXP Semiconductors NV

- 7.1.5 Diodes Incorporated

- 7.1.6 Toshiba Electronic Devices & Storage Corporation

- 7.1.7 ABB Ltd.

- 7.1.8 Nexperia BV

- 7.1.9 Semikron Danfoss Holding A/S (Danfoss A/S)

- 7.1.10 Eaton Corporation PLC

- 7.1.11 Hitachi Energy Ltd. (Hitachi Ltd.)

- 7.1.12 Mitsubishi Electric Corp.

- 7.1.13 Fuji Electric Co Ltd

- 7.1.14 Analog Devices, Inc.

- 7.1.15 Vishay Intertechnology Inc.

- 7.1.16 Renesas Electronics Corporation

- 7.1.17 ROHM Co. Ltd

- 7.1.18 Microchip Technology

- 7.1.19 Qorvo Inc.

- 7.1.20 Wolfspeed Inc.

- 7.1.21 Texas Instruments Inc.

- 7.1.22 Littelfuse Inc

- 7.1.23 WeEn Semiconductors

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日