|

|

市場調査レポート

商品コード

1550337

中国のディスクリート半導体:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)China Discrete Semiconductors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のディスクリート半導体:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

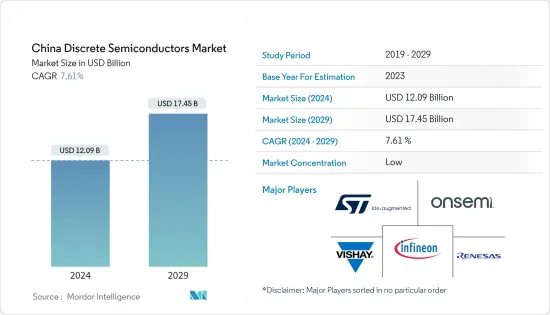

中国のディスクリート半導体市場規模は2024年に120億9,000万米ドルと推定され、2029年には174億5,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは7.61%で成長します。

主なハイライト

- 中国のディスクリート半導体市場は、拡大する業界情勢とROI(投資収益率)向上のための自動化への戦略的軸足により、大幅な成長を遂げています。中国は世界最大の製造業を誇り、市場需要に大きく貢献しています。中国の製造企業は、業務を最適化するために4.0ソリューションの採用を優先しており、市場拡大を後押ししています。

- 中国は、5G技術の世界の導入において傑出したプレーヤーとして浮上しています。MIITは、中国の5Gユーザーが2023年2月までに5億9,201万人に達し、2025年には10億人を突破すると予測しています。この進歩をサポートするために必要なインフラを強化するための重要な取り組みが進行中です。例えば、2023年10月現在、中国の5G基地局は約322万局で、全セルラー基地局の28.1%に相当します。5Gは、製造エコシステムのさまざまな要素間のデータ転送を促進する通信分野の重要なコンポーネントとしての地位を急速に確立しており、こうした市場開拓は中国国内の市場成長を促進する構えです。

- 同国におけるデータセンター開発への支出の増加は、より多くの電気部品への需要を増加させる可能性があり、予測期間中、中国におけるディスクリート半導体の需要を押し上げる可能性があります。例えば、CloudSceneは2023年9月、アジア太平洋データセンター展望における中国の重要性を強調しました。中国は448のデータセンターを誇り、同地域で最高でした。世界全体では、中国は同月のデータセンター総数で4位の座を確保しました。

- ディスクリート半導体の製造には、炭化ケイ素や窒化ガリウムなどが使われます。しかし、これらの原材料は高コストであり、市場拡大の大きな障害となっています。その結果、ディスクリート半導体の製造に必要な原材料費の高騰が市場の成長を妨げています。

- 中国の経済成長のようなマクロ経済要因は、工業生産高と半導体需要に直接影響します。景気減速は投資や個人消費を減少させ、半導体需要に影響を与える可能性があります。国際貿易政策、関税、制裁措置は半導体と原材料の輸出入に影響を与え、サプライチェーンと市場力学に影響を与えます。

中国ディスクリート半導体市場動向

コンシューマーエレクトロニクスは大幅な成長が見込まれる

- 中国のコンシューマーエレクトロニクス市場は急成長を遂げており、同国を世界な舞台における重要なプレーヤーとして位置付けています。この成長を後押ししているのは、eコマースの拡大、中国の消費者の可処分所得の着実な増加、継続的な製品イノベーション、技術進歩、そして極めつけは政府の後押しです。さらに、中国の家電市場は、スマートホーム、拡張現実(AR)および仮想現実(VR)技術の進歩、5Gネットワークの展開に対する需要の高まりに牽引され、今後数年間で継続的な拡大が見込まれています。

- 中国は世界の5G市場をリードしており、2024年までに5Gが同国の主要モバイル技術として4Gを上回ると予測しています。GSMAの予測によると、2025年までに中国は世界最多の5G接続数を誇り、そのユーザー数は10億人に達するといいます。中国は、「デジタル・チャイナ2035」ビジョンに沿った戦略的ロードマップである「デジタル・チャイナ建設配置計画」を発表しました。この構想は、2035年までに中国を世界のデジタル・イノベーションの重要な担い手へと押し上げることを目的としています。

- 同市場のプレーヤーは、民生用電子機器向けのディスクリート半導体を発売しており、市場の成長をさらに後押ししています。例えば、Vishay Intertechnologyは2024年2月、汎用性の高い30VのnチャネルトレンチFETGen VパワーMOSFETを発表しました。このMOSFETは、電力密度の向上と高い熱効率を実現し、コンピュータ、民生、電気通信などさまざまな分野の用途に適しています。3.3mm×3.3mmのコンパクトなPowerPAK1212-Fパッケージには、先進のソースフリップ技術を組み込んだVishay SiliconixSiSD5300DNが搭載されています。

- 同国の半導体エコシステム強化に向けた政府のイニシアチブの成長と、民生用電子機器分野の世界の生産国としての同国の台頭が、市場の成長を支えると思われます。中国の家電産業は数十億米ドル規模に急成長しています。中国国家統計局のデータによると、2024年4月、中国の家電・民生用電子機器の小売販売額は640億人民元(約89億6,000万米ドル)を突破しました。

パワートランジスターが大きな市場シェアを占める見込み

- 絶縁ゲートバイポーラトランジスタは3端子の半導体スイッチングデバイスで、迅速かつ効率的なスイッチングを実現するため、多くの電子機器に応用されています。このデバイスは通常、パルス幅変調(PWM)で複雑な波形をスイッチング/処理するアンプに使用されます。ディスクリート型とモジュール型があります。パワー半導体は急速かつ広範囲に展開されており、そのため、フィールドデータが乏しく、潜在的な不確実性があるため、信頼性に深刻な懸念が生じています。この意味で、IGBTの市場は著しく拡大しています。

- 産業部門は、IGBTパワー・トランジスタの主要なエンド・ユーザーのひとつです。中国で急速に進むインダストリー4.0の動向は、製造能力を強化しハイテク部門を育成する「メイド・イン・チャイナ2025」のようなイニシアティブとともに、市場参入企業に機会の流れを生み出しており、これがモーター駆動アプリケーションにおけるIGBTのニーズを促進する要因の1つとなっています。多くの企業が、操作を簡素化し生産量を向上させるために、従来のモーターを先進的なモーター駆動装置に置き換え続けています。

- 自動車産業は、さまざまな用途でシリコンMOSFETディスクリート半導体に大きく依存しています。MOSFETは、電子制御ユニット(ECU)、バッテリー管理、モーター制御、車載照明システムなどに使用されています。MOSFETは、大電流、高電圧、高耐久性に優れているため、要求の厳しい車載用途に最適です。MOSFETパワートランジスタは、電気自動車(EV)を効率的に機能させる上で極めて重要です。モーター駆動システム、補助システム用DC-DCコンバーターなどに採用されています。EVの力強い成長は、市場の開拓を促進すると思われます。

- バッテリー容量の増加に伴い、SiC MOSFETによる省エネ効果も大きくなります。当初、SiC MOSFETは大型バッテリーを搭載した中・高級EV専用だった。しかし、Chevrolet Bolt EV、Volvo EX40、Kia Niro EV、Nissan Leaf Plus EVなど、50kWhを超えるバッテリー容量を誇る主流および低価格の自動車が登場したことで、SiC MOSFETは中国の主流乗用車市場に進出する態勢が整い、調査対象の市場需要を牽引しています。

中国ディスクリート半導体産業概要

中国のディスクリート半導体市場は断片化されており、STMicroelectronics NV、On Semiconductor Corporation、Vishay Intertechnology Inc.、Infineon Technologies AG、Renesas Electronics Corporation、Texas Instrument Inc.などの大手企業が存在します。中国のディスクリート半導体市場の主要企業は、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、合併、イノベーション、パートナーシップ、投資、買収などの戦略を採用しています。

- 2024年1月、STマイクロエレクトロニクスとLi Autoは、炭化ケイ素(SiC)を中心とした戦略的長期供給契約を締結しました。中国で急成長を遂げる新エネルギー自動車の中心的存在であるLi Autoは、高級電気自動車(EV)の製造、生産、販売に注力しています。今回の協業において、STはLi AutoにSiCMOSFETを提供します。これらのコンポーネントは、様々な市場セグメントにまたがる高電圧バッテリー電気自動車(BEV)におけるLi Autoの取り組みを強化するものです。

- 2024年1月、インフィニオン・テクノロジーズはエネルギー貯蔵会社であるSinexcel Electricと提携しました。インフィニオンはこの提携で、シネクセルに最新の1200V CoolSiC MOSFET半導体デバイスを供給します。これらは、インフィニオンの小型1,200Vシングルチャンネル絶縁ゲートドライブIC「EiceDRIVER」によって補完され、エネルギー貯蔵システムの効率向上を目指します。SiCパワー・ソリューションは、今後のグリーンエネルギー生産と蓄電アプリケーションにおいて極めて重要です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の副作用とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- 5G技術の進歩

- 自動車・エレクトロニクス分野における高エネルギー・省電力デバイスの需要増加

- 電子部品需要の増加

- 市場の課題

- 集積回路の需要増加

- 原材料コストの高騰

- 小型化による設計の複雑化

第6章 市場セグメンテーション

- タイプ別

- ダイオード

- 小信号トランジスタ

- パワートランジスタ

- MOSFETパワートランジスタ

- IGBTパワートランジスタ

- その他パワートランジスタ

- 整流器

- サイリスタ

- 産業別

- 自動車

- 民生用電子機器

- 通信機器

- 産業用

- その他産業別

第7章 競合情勢

- 企業プロファイル

- STMicroelectronics NV

- On Semiconductor Corporation

- Vishay Intertechnology Inc.

- Infineon Technologies AG

- Renesas Electronics Corporation

- Texas Instrument Inc.

- Qorvo Inc.

- Microchip Technology Inc.

- Diodes Incorporated

- Wolfspeed Inc.

- Rohm Co., Ltd.

第8章 投資分析

第9章 市場の将来

The China Discrete Semiconductors Market size is estimated at USD 12.09 billion in 2024, and is expected to reach USD 17.45 billion by 2029, growing at a CAGR of 7.61% during the forecast period (2024-2029).

Key Highlights

- The Chinese discrete semiconductor market is witnessing substantial growth, propelled by the country's expanding industrial landscape and a strategic pivot toward automation to boost ROI (return on investment). China boasts the largest manufacturing industry globally, contributing significantly to market demand. Manufacturing companies in China prioritize adopting 4.0 solutions to optimize operations, propelling market expansion.

- China has emerged as a prominent player in the global implementation of 5G technology. The MIIT projected that China would reach 592.01 million 5G users by February 2023, with expectations of surpassing 1 billion users by 2025. Significant efforts are underway to enhance the necessary infrastructure to support this advancement. For instance, as of October 2023, China had approximately 3.22 million 5G base stations, representing 28.1% of all cellular base stations. With 5G rapidly establishing itself as a crucial component of the communication sector, facilitating data transfer among various elements of the manufacturing ecosystem, these developments are poised to drive growth in the market within the country.

- Rising expenditures on developing data centers in the country may increase the demand for more electrical components, which is likely to boost the demand for discrete semiconductors in China during the forecast period. For instance, CloudScene highlighted China's significance in the Asia-Pacific data center landscape in September 2023. China boasted 448 data centers, the highest in the region. Globally, China secured the fourth spot in total data center count that month.

- Silicon carbide, gallium nitride, and other materials are used to manufacture discrete semiconductors. However, these raw materials are linked to high expenses, a significant market expansion obstacle. As a result, the elevated costs of raw materials necessary for producing discrete semiconductors are impeding the market's growth.

- Macroeconomic factors like China's economic growth directly affect industrial output and semiconductor demand. A slowdown may reduce investment and consumer spending, impacting semiconductor demand. International trade policies, tariffs, and sanctions impact the import and export of semiconductors and raw materials, affecting supply chain and market dynamics.

China Discrete Semiconductors Market Trends

Consumer Electronics is Expected to Witness a Significant Growth

- China's consumer electronics market is witnessing a surge, positioning the country as a significant player on the global stage. This growth is propelled by several factors: the expanding reach of e-commerce, a steady uptick in Chinese consumers' disposable incomes, ongoing product innovations, technological advancements, and, crucially, government backing. In addition, China's consumer electronics market is poised for continued expansion in the coming years, driven by rising demand for smart homes, augmented and virtual reality technologies advancements, and the rollout of 5G networks.

- China leads the global 5G market, with projections indicating that 5G will surpass 4G as the primary mobile technology in the country by 2024. GSMA forecasts that by 2025, China will boast the highest number of 5G connections globally, with an estimated 1 billion users. China unveiled the Layout Plan for the Construction of Digital China, a strategic roadmap aligning with its 'Digital China 2035' vision. This initiative aims to propel China into a significant global digital innovation player by 2035.

- Players in the market are launching discrete semiconductors for consumer electronics, further supporting the market growth. For instance, in February 2024, Vishay Intertechnology introduced a highly versatile 30 V n-channel Trench FETGen V power MOSFET. This MOSFET provides enhanced power density and high thermal efficiency, making it suitable for various applications across various sectors such as computer, consumer, and telecom. The compact 3.3 mm by 3.3 mm PowerPAK1212-F package houses the Vishay SiliconixSiSD5300DN, incorporating advanced source flip technology.

- The growth of governmental initiatives in strengthening the country's semiconductor ecosystem and the country's emergence as a global producer of consumer electronic sectors would support the market growth. China's household appliance industry has burgeoned into a multi-billion dollar sector. Data from the National Bureau of Statistics of China reveals that in April 2024, the retail sales value of household appliances and consumer electronics in China surpassed CNY 64 billion (USD 8.96 billion).

Power Transistors is Expected to Hold Significant Market Share

- An insulated gate bipolar transistor is a three-terminal semiconductor switching device that can be applied to many electronic devices for quick and efficient switching. These devices are typically used in amplifiers for switching/processing complex wave patterns with pulse width modulation (PWM). It comes in both Discrete and Modular varieties. Power semiconductors are being deployed quickly and widely, which has led to severe reliability concerns due to the scant field data and potential uncertainties. In this sense, the market for IGBTs is expanding significantly.

- The industrial sector is one of the major end-users of the IGBT power transistor. The rapidly advancing trend of Industry 4.0 in China with initiatives like "Made in China 2025" to enhance its manufacturing prowess and nurture high-tech sectors has created a stream of opportunities for market participants, which is one of the factors driving the need for IGBTs in motor drive applications. Many businesses continue replacing conventional motors with advanced motor drives to simplify operations and improve output.

- The automotive industry heavily relies on silicon MOSFET discrete semiconductors for various applications. MOSFETs are used in electronic control units (ECUs), battery management, motor control, and automotive lighting systems. Given their capacity to manage high currents, voltages, and durability, these components are the top choice for demanding automotive settings. MOSFET power transistors are crucial in efficiently functioning electric vehicles (EVs). They are employed in motor drive systems, DC-DC converters for auxiliary systems, etc. The robust growth of EVs is likely to drive the development of the studied market.

- As battery capacity rises, the energy savings from SiC MOSFETs also grow. Initially, these MOSFETs were exclusive to mid to high-end EVs with larger batteries. However, with the emergence of mainstream and budget vehicles like the Chevrolet Bolt EV, Volvo EX40, Kia Niro EV, and Nissan Leaf Plus EV, all boasting battery capacities exceeding 50kWh, SiC MOSFETs are poised to make inroads into China's mainstream passenger vehicle market, thus driving the market demand studied.

China Discrete Semiconductors Industry Overview

The Chinese discrete semiconductors market is fragmented, with the presence of major players like STMicroelectronics NV, On Semiconductor Corporation, Vishay Intertechnology Inc., Infineon Technologies AG, Renesas Electronics Corporation, and Texas Instrument Inc. Key players in the Chinese discrete semiconductors market are adopting strategies such as mergers, innovations, partnerships, investments, and acquisitions to enhance product offerings and gain sustainable competitive advantage.

- In January 2024, STMicroelectronics and Li Auto inked a strategic, long-term supply agreement centered around silicon carbide (SiC). Li Auto, a key figure in China's burgeoning new energy vehicle landscape, focuses on crafting, producing, and marketing upscale electric vehicles (EVs). In this collaboration, STMicroelectronics (ST) would provide Li Auto with SiCMOSFETs. These components are set to fortify Li Auto's endeavors in high-voltage battery electric vehicles (BEVs) spanning various market segments.

- In January 2024, Infineon Technologies partnered with Sinexcel Electric, an energy storage company. Infineon would supply Sinexcel with its latest 1,200 V CoolSiC MOSFET semiconductor devices in this collaboration. These will be complemented by Infineon's EiceDRIVER compact 1,200 V single-channel isolated gate drive ICs, which aim to enhance the efficiency of energy storage systems. The SiC power solution is pivotal in upcoming green energy production and storage applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Advancements in 5G Technology

- 5.1.2 Rising Demand for High-Energy and Power-Efficient Devices in the Automotive and Electronics Segment

- 5.1.3 Rising Demand for Electronic Components

- 5.2 Market Challenges

- 5.2.1 Rising Demand for Integrated Circuits

- 5.2.2 High Cost of Raw Materials

- 5.2.3 Increasing Design Complexity Due to Miniaturization

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Diode

- 6.1.2 Small Signal Transistor

- 6.1.3 Power Transistor

- 6.1.3.1 MOSFET Power Transistor

- 6.1.3.2 IGBT Power Transistor

- 6.1.3.3 Other Power Transistors

- 6.1.4 Rectifier

- 6.1.5 Thyristor

- 6.2 By End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Consumer Electronics

- 6.2.3 Communication

- 6.2.4 Industrial

- 6.2.5 Other End-user Verticals

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 STMicroelectronics NV

- 7.1.2 On Semiconductor Corporation

- 7.1.3 Vishay Intertechnology Inc.

- 7.1.4 Infineon Technologies AG

- 7.1.5 Renesas Electronics Corporation

- 7.1.6 Texas Instrument Inc.

- 7.1.7 Qorvo Inc.

- 7.1.8 Microchip Technology Inc.

- 7.1.9 Diodes Incorporated

- 7.1.10 Wolfspeed Inc.

- 7.1.11 Rohm Co., Ltd.