欧州のプラスチックボトル・容器市場:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Europe Plastic Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687178

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

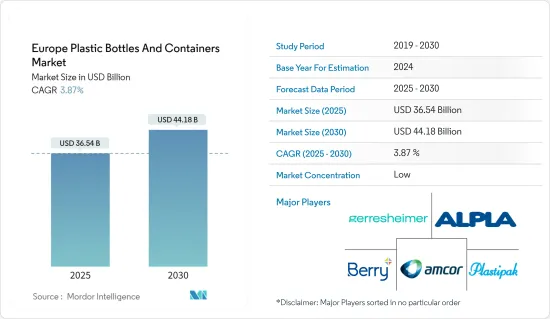

欧州のプラスチックボトル・容器市場規模は2025年に365億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.87%で、2030年には441億8,000万米ドルに達すると予測されます。

主要ハイライト

- ポリエチレンテレフタレート、ポリプロピレン、ポリエチレンのような材料から製造されるプラスチックボトルと容器が、包装産業の主流を占めています。軽量で耐久性に優れているため、主にコスト効率の良さからメーカーに選ばれています。このことは、世界の飲食品への依存と相まって、今後数年間のプラスチックボトル・容器市場に大きな影響を与える舞台となっています。

- プラスチック採用の急増は、その軽量特性に直接結びついています。これは輸送時の省エネを助けるだけでなく、排出物の削減にもつながります。プラスチックの重量の優位性は、輸送に多くの回数を必要とするガラスのような重い代替品と比較すると、より明白になります。

- プラスチックボトルや容器はさまざまな材料から作られるが、ポリエチレンテレフタレート(PET)製のものは、耐久性、汎用性、コスト効率の点で際立っています。欧州の食品、飲食品、製薬セクターが拡大し、技術革新が進むにつれて、プラスチック包装、特にPETボトルの需要もそれに連動して高まっています。多様なフレーバーと包装スタイルで新しい飲料を導入する産業の動向は、硬質プラスチックボトルの需要をさらに高めています。

- 特に飲料セグメントは、ペットボトル入り飲料水とノンアルコール飲料の永続的な需要によって、ペットボトルに大きく依存しています。消費者がボトル入りの水を求めるのは、汚染の可能性のある水道水を避け、ボトル入りの水が提供する利便性と携帯性を重視するためです。

- 環境問題を強調する欧州委員会の調査では、海洋ゴミにペットボトルとその蓋が多く含まれていることが明らかになりました。これを受けて欧州理事会は、使い捨てプラスチックの使用を抑制し、野心的なリサイクル目標を設定することを目的とした厳しい規制を展開しました。

- プラスチック汚染への懸念が高まる中、メーカーも消費者もエコフレンドリー代替包装を模索しています。この変化は、リサイクル可能でエコフレンドリー特性が評価されているアルミニウムやガラスの採用率が上昇していることからも明らかです。

- この動向を示すように、2024年3月、欧州のブルックフィールドドリンクスは、100%海洋プラスチックを使用しないボトルの発売を発表し、話題を呼びました。この革新的なボトルは、同社のNEO WTRシリーズの一部で、テスコのスーパーストア250店舗で発売される予定です。ブルックフィールドドリンクス社の取り組みは、産業初の完全リサイクル海洋プラスチックボトルにリサイクル可能なキャップとラベルを付けた新しい湧水シリーズを発売することで、主要な清涼飲料ブランドを凌ぐ重要なマイルストーンとなります。

欧州プラスチックボトル・容器市場動向

飲料セグメントが大きな市場シェアを占める見込み

- 飲料産業が調査対象市場の大きな成長を牽引しています。プラスチック容器とボトルはこのセグメントで人気を集めており、メーカーが飲料だけでなく他のエンドユーザー産業にも対応するよう促しています。軽量包装は、経済効率と環境への配慮という2つの利点があるため、包装産業において極めて重要な存在となっています。軽量であることから、プラスチックボトルや容器は輸送時のエネルギー消費を削減し、燃料使用量の削減、二酸化炭素排出量の削減、流通業者や小売業者のコスト削減につながります。

- 英国清涼飲料協会の2024年次報告書によると、英国では2023年に30億2,700万リットルのボトル入り飲料水が消費され、プラスチックボトルが95.2%の圧倒的シェアを占めています。ボトル入り飲料水の消費量が増加傾向にあることから、飲料セグメントでの硬質プラスチックボトルの需要は急増するとみられます。

- ペットボトルは、その費用対効果とバリア性の高さから、英国の飲料セグメントで圧倒的なシェアを占めています。英国清涼飲料協会の調査結果によると、清涼飲料の68%、炭酸飲料の53%、希釈飲料の95%、スポーツドリンクとエナジードリンクの42%を占めています。

- 欧州のプラスチックボトル・容器市場では、持続可能性への取り組みが顕著に増加しています。これには、バイオプラスチックのようなサステイナブル原料へのシフトや、製品ラインへのリサイクル材料の統合が含まれ、これらはすべてイノベーションを促進することを目的としています。2025年までに25%、2030年までに30%の再生プラスチックを使用するという、単一使用プラスチック指令の野心的な目標は、産業に革命を起こそうとしています。そのため、メーカーはリサイクル技術への投資を余儀なくされ、持続可能性への確固としたコミットメントを示しています。

- 飲料消費量の増加に伴い、ペットボトルやペットボトル入り飲料水、炭酸飲料、牛乳などの容器の需要が急増しています。例えばドイツでは、1人当たりの清涼飲料消費量が2020年の114.7リットルから2023年には124.9リットルに増加すると予測されており、プラスチック包装に対する同国の旺盛な意欲を裏付けています。

大幅な成長が見込まれるドイツ

- ドイツでは、ソリューション・プロバイダーとエンドユーザーの両方からの先進的な取り組みにより、プラスチック包装ソリューションの導入が進んでいます。メイドイン・ドイツ」製品に対する消費者の認識は高く、同地域の軟質包装企業は特に好意的に受け止められています。

- ドイツ政府はプラスチック包装産業に対して厳しい規制を実施しています。PETボトルは様々なセグメントで普及しているが、飲料、化粧品、衛生用品、洗剤のセグメントではポリエチレン(PE)ボトルが圧倒的な売上を誇っています。

- 化粧品消費の急増とプラスチック包装技術の絶え間ない革新により、市場は成長態勢にあります。軽量で費用対効果が高く、衛生的な特性で知られるプラスチックは、特に保存期間が短い化粧品に適しています。透明で気密性が高く、圧縮強度が高く成形しやすいPETボトルは、高級化粧品の視覚的魅力を高めており、このセグメントの将来が有望であることを示しています。

- PETはボトルと瓶の両方で一般的に使用されており、特に攻めの化粧品に好まれています。一方、ポリ塩化ビニル(PVC)は、有害成分との関連は言うに及ばず、材料と反応して変形する可能性があるため、一般に敬遠されています。この調査は、スキンケア、ヘアケア、経口ケア、メイクアップ、デオドラント、フレグランスなど、さまざまな用途を対象としています。

- ドイツは堅調な美容・パーソナルケア市場を誇り、急成長を遂げています。Personal Care and Detergent Industry Association e. V.によると、市場規模は2021年の147億2,290万米ドルから2023年には171億5,690万米ドルに急増します。このパーソナルケア市場の拡大は、プラスチックボトル・容器の成長におけるドイツの重要性を強調しています。

欧州のプラスチックボトル・容器産業概要

調査した市場はセグメント化されており、重要な参入企業は、Alpha Group、Amcor PLC、Gerresheimer AG、Berry Global Inc.、Plastipak Holdings Inc.、Graham Packaging Company LPなどです。

- 2023年10月-Berry Global Groupは高級水ブランドNEUE専用のrPETボトルを発売しました。この発売は、Berry GlobalがNEUEのプレミアムアルテジアンミネラルウォーターに100%リサイクルPETボトルを提供するという重要なステップです。NEUEウォーターは、現代的でペースの速いライフスタイルを念頭にデザインされています。エコフレンドリー構成に加え、革新的な平らな形態のボトルは携帯に便利で、様々な輸送のポケットやバッグ、座席の背もたれにもシームレスにフィットします。

- 2023年10月-PlastipakとPVG Liquidsは、20リットルの積み重ね可能な容器に合わせた375Gのプリフォームを共同で設計し、今後数年間でPETの消費量を500トン大幅に削減できるよう設計しました。この技術革新により、CO2排出量を年間約200トン削減できると予測されています。プラスティパックのイタリア・ヴェルバーニア工場での生産は、輸送中の排出を最小限に抑えるための戦略的な動きです。コンテナ自体は、革新的なプリフォームと組み合わされた新しい低結晶性樹脂から作られています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 産業バリューチェーン分析

第5章 市場力学

- 市場促進要因

- 軽量包装方式の採用増加

- 人口動態とライフスタイルの変化

- 市場抑制要因

- プラスチックの使用をめぐる環境問題の高まり

- 貿易シナリオ

- EXIMデータ

- 貿易分析(輸出入上位5カ国、価格分析、主要港など)

- 貿易分析(輸出入上位5カ国、価格分析、主要港など)

- 産業の規制と施策と規格

- 技術

- 価格動向分析

- プラスチック樹脂(現在の価格と過去の動向)

第6章 市場セグメンテーション

- 樹脂別

- ポリエチレン(PE)

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- その他の樹脂タイプ(ポリスチレン、PVC、ポリカーボネートなど)

- 製品別

- ボトル

- 瓶

- キャニスター

- 箱

- ガロン

- タブ

- その他

- 最終用途産業別

- 食品

- 飲料

- ボトル入り飲料水

- 炭酸飲料

- 牛乳

- その他飲料

- 医薬品

- パーソナルケア&トイレタリー

- 工業用

- 家庭用化学品

- 塗料

- その他

- 国別

- フランス

- ドイツ

- イタリア

- 英国

- スペイン

- ポーランド

第7章 競合情勢

- 企業プロファイル

- Amcor Group GmbH

- Gerresheimer AG

- Plastipak Holdings Inc.

- ALPLA Group

- Berry Global Inc.

- Alpha Packaging Inc.

- Graham Packaging

- Resilux NV

- Greiner Packaging International GmbH

- Comar LLC

- ヒートマップ分析

- 競合他社分析-新興企業と既存企業

第8章 リサイクルと持続可能性の情勢

第9章 市場の将来

目次

The Europe Plastic Bottles And Containers Market size is estimated at USD 36.54 billion in 2025, and is expected to reach USD 44.18 billion by 2030, at a CAGR of 3.87% during the forecast period (2025-2030).

Key Highlights

- Plastic bottles and containers manufactured from materials like polyethylene terephthalate, polypropylene, and polyethylene, dominate the packaging landscape. Their lightweight and durable nature makes them a preferred choice for manufacturers, primarily due to their cost-effectiveness. This, coupled with the global reliance on packaged foods and beverages, sets the stage for a significant impact on the plastic bottles and containers market in the coming years.

- The surge in plastic adoption is directly tied to its lightweight properties. This not only aids in energy conservation during transportation but also reduces emissions. Plastic's weight advantage becomes even more apparent when compared to heavier alternatives like glass, which necessitate more trips for transportation.

- While plastic bottles and containers can be crafted from various materials, those made from polyethylene terephthalate (PET) stand out for their durability, versatility, and cost-efficiency. As Europe's food, beverage, and pharmaceutical sectors expand and innovate, the demand for plastic packaging, especially PET bottles, rises in tandem. The industry's trend of introducing new beverages in diverse flavors and packaging styles further bolsters the demand for rigid plastic bottles.

- The beverage sector, in particular, heavily leans on plastic bottles, driven by the perpetual demand for bottled water and non-alcoholic drinks. Consumers seek bottled water for its perceived purity, shunning potentially contaminated tap water, and valuing the convenience and portability it offers.

- Highlighting environmental concerns, a European Commission study underscored the prevalence of PET bottles and their lids in ocean debris. In response, the European Council has rolled out stringent regulations, aiming to curb the use of single-use plastics and set ambitious recycling targets.

- Amid mounting worries over plastic pollution, both manufacturers and consumers are exploring eco-friendlier packaging alternatives. This shift is evident in the rising adoption rates of aluminum and glass, lauded for their recyclability and environmentally conscious attributes.

- Illustrating this trend, in March 2024, Europe's Brookfield Drinks made waves by announcing the launch of a 100% Prevented Ocean Plastic bottle. This innovative bottle, part of their NEO WTR range, is set to debut in 250 Tesco superstores. Brookfield Drinks' initiative marks a significant milestone, outpacing major soft drink brands by introducing a new spring water range in the industry's first fully recycled ocean-bound plastic bottle, complete with a recyclable cap and label.

Europe Plastic Bottles and Containers Market Trends

The Beverages Segment is Expected to Hold a Significant Market Share

- The beverage industry is driving significant growth in the market under study. Plastic containers and bottles are gaining popularity within this sector, prompting manufacturers to cater not only to beverages but also to other end-user industries. Lightweight packaging has emerged as a pivotal force in the packaging industry, owing to its dual benefits: economic efficiency and environmental friendliness. Given their lightweight nature, plastic bottles and containers reduce energy consumption during transportation, leading to lower fuel usage, reduced carbon emissions, and decreased costs for distributors and retailers.

- As per the 2024 Annual Report by the British Soft Drink Association, the United Kingdom consumed 3,027 million liters of bottled water in 2023, with plastic bottles representing a dominant 95.2% share. With bottled water consumption on the rise, the demand for rigid plastic bottles in the beverage sector is set to surge.

- Plastic bottles, due to their cost-effectiveness and barrier properties, hold a lion's share in the United Kingdom's beverage landscape. They make up 68% of soft drink consumption, 53% of carbonated drinks, 95% of dilutables, and 42% of sports and energy drinks, as highlighted in the British Soft Drink Association's findings.

- Across the European plastic bottles and containers market, there's a notable uptick in sustainability initiatives. These include a shift towards sustainable raw materials like bioplastics and integrating recycled content into product lines, all aimed at fostering innovation. The ambitious targets set by the Single-Use-Plastic Directive - 25% recycled content by 2025 and 30% by 2030 - are poised to revolutionize the industry. Manufacturers are thus compelled to invest in recycling technologies, signaling a steadfast commitment to sustainability.

- With beverage consumption on the rise, the demand for plastic bottles and containers for bottled water, carbonated drinks, or milk is surging. Germany, for instance, saw its per capita soft drink consumption climb from 114.7 liters in 2020 to a projected 124.9 liters in 2023, underscoring the country's robust appetite for plastic packaging.

Germany is Expected to Witness Significant Growth

- Germany is increasingly embracing plastic packaging solutions, driven by advancements from both solution providers and end users. The renowned consumer perception of "Made in Germany" products has notably favored the region's flexible packaging companies.

- The German government has implemented stringent regulations for the plastic packaging industry. While PET bottles are prevalent across various sectors, polyethylene (PE) bottles dominate sales in beverages, cosmetics, sanitary, and detergent segments.

- With a surge in cosmetic consumption and continuous innovation in plastic packaging technology, the market is poised for growth. Plastic, known for its lightweight, cost-effectiveness, and hygienic properties, is particularly well-suited for cosmetics, especially those with shorter shelf lives. Transparent, airtight, and easily moldable with good compressive strength, PET plastic bottles are enhancing the visual appeal of high-end cosmetics, indicating a promising future for this segment.

- PET finds common use in both bottles and jars, especially favored for aggressive cosmetics. On the other hand, polyvinyl chloride (PVC) is generally shunned due to its potential to react with and distort materials, not to mention its association with hazardous components. The study covers a range of applications, including skincare, haircare, oral care, makeup, deodorants, fragrances, and more.

- Germany boasts a robust beauty and personal care market, witnessing rapid growth. According to the Personal Care and Detergent Industry Association e. V., the market value surged from USD 14,722.9 million in 2021 to USD 17,156.9 million in 2023. This expanding personal care market underscores Germany's significance in the growth of plastic bottles and containers.

Europe Plastic Bottles and Containers Industry Overview

The market studied is fragmented, with some significant players such as Alpha Group, Amcor PLC, Gerresheimer AG, Berry Global Inc., Plastipak Holdings Inc., and Graham Packaging Company LP. These companies increase their market shares by launching new products and forming partnerships and mergers. Some of the recent developments are:

- October 2023 - Berry Global Group introduced a rPET bottle specifically for the upscale water brand, NEUE. This launch marks a significant step as Berry Globalprovides 100% recycled PET bottles for NEUE's premium artesian mineral water. NEUE Water is designed with the contemporary, fast-paced lifestyle in mind. In addition to its eco-friendly composition, the bottle's innovative flat shape ensures convenient portability, fitting seamlessly into pockets, bags, and even seatback storage on various modes of transport.

- October 2023 - Plastipak and PVG Liquids have jointly engineered a 375g preform tailored for a 20-liter stackable container, designed to significantly slash PET consumption by 500 tons in the coming years. This innovation is projected to curtail CO2 emissions by approximately 200 tons annually. The production, situated at Plastipak's Verbania plant in Italy, is a strategic move to minimize emissions during transit. The container itself is crafted from a novel low-crystallinity resin, paired with the innovative preform.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Lightweight Packaging Methods

- 5.1.2 Changing Demographic and Lifestyle Factors

- 5.2 Market Restraints

- 5.2.1 Growing Environmental Concerns Over the Use of Plastics

- 5.3 Trade Scenario

- 5.3.1 EXIM Data

- 5.3.2 Trade Analysis (Top 5 Import-Export Countries, Price Analysis, and Key Ports, Among others)

- 5.4 Trade Analysis (Top 5 Import-Export Countries, Price Analysis, and Key Ports, Among others)

- 5.5 Industry Regulation, Policy and Standards

- 5.6 Technology Landscape

- 5.7 Pricing Trend Analysis

- 5.7.1 Plastic Resins (Current Pricing and Historic Trends)

6 MARKET SEGMENTATION

- 6.1 By Resin

- 6.1.1 Polyethylene (PE)

- 6.1.2 Polyethylene Terephthalate (PET)

- 6.1.3 Polypropylene (PP)

- 6.1.4 Other Resin Type (Polystyrene, PVC, Polycarbonate, etc.)

- 6.2 By Product

- 6.2.1 Bottles

- 6.2.2 Jars

- 6.2.3 Canisters

- 6.2.4 Boxes

- 6.2.5 Gallons

- 6.2.6 Tubs

- 6.2.7 Other Products

- 6.3 By End-use Industries

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.2.1 Bottled Water

- 6.3.2.2 Carbonated Soft Drinks

- 6.3.2.3 Milk

- 6.3.2.4 Other Beverages

- 6.3.3 Pharmaceuticals

- 6.3.4 Personal Care & Toiletries

- 6.3.5 Industrial

- 6.3.6 Household Chemicals

- 6.3.7 Paints & Coatings

- 6.3.8 Other End-use Industries

- 6.4 By Country

- 6.4.1 France

- 6.4.2 Germany

- 6.4.3 Italy

- 6.4.4 United Kingdom

- 6.4.5 Spain

- 6.4.6 Poland

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor Group GmbH

- 7.1.2 Gerresheimer AG

- 7.1.3 Plastipak Holdings Inc.

- 7.1.4 ALPLA Group

- 7.1.5 Berry Global Inc.

- 7.1.6 Alpha Packaging Inc.

- 7.1.7 Graham Packaging

- 7.1.8 Resilux NV

- 7.1.9 Greiner Packaging International GmbH

- 7.1.10 Comar LLC

- 7.2 Heat Map Analysis

- 7.3 Competitor Analysis - Emerging vs. Established Players

8 RECYCLING & SUSTAINABILITY LANDSCAPE

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日