|

市場調査レポート

商品コード

1626333

北米のプラスチックボトル・容器:市場シェア分析、産業動向、統計、成長予測(2025~2030年)NA Plastic Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のプラスチックボトル・容器:市場シェア分析、産業動向、統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

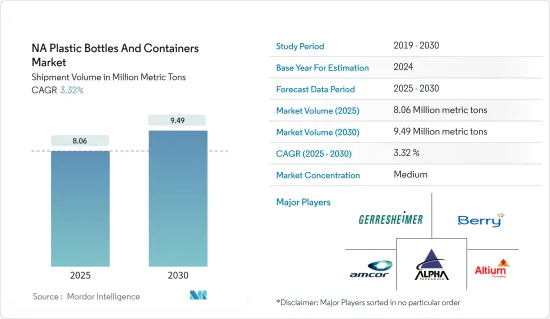

北米のプラスチックボトル・容器市場の出荷量規模は、予測期間(2025~2030年)のCAGR 3.32%で、2025年の806万トンから2030年には949万トンに成長すると予測されます。

北米のプラスチックボトル・容器市場は、確立された製造能力と底堅い輸出部門によって形成されています。包装は消費財と工業製品の消費において極めて重要な役割を果たしています。北米では、持続可能で利便性の高いパッケージング・ソリューションに対する需要の高まりが市場の成長を後押ししています。

主なハイライト

- 新興国が台頭する一方で、米国は世界の製薬業界において支配的な地位を維持しています。大手製薬会社の本拠地である米国は、大きな市場シェアを占めるだけでなく、消費者に最先端の製品を提供しています。この堅調な医薬品情勢は、プラスチックボトル・容器市場の革新と進歩に拍車をかけています。

主なハイライト

- 例えば、米国のBerry Global社は2023年2月、医薬品・ハーブ市場向けの包括的ソリューションを発表しました。ベリー・ヘルスケア・バンドルとして知られるこの新しい製品には、20mlから1,000mlまでのサイズに及ぶ多様な28mmネックのPETボトルが含まれ、タンパーエビデントと小児用耐性を備えた8種類のクロージャーが特徴です。

- 化粧品からスキンケアまでを含む北米の美容・パーソナルケア業界では、プレミアムで革新的な製品に対する需要が急増しています。この動向は、大手ブランド各社が製品ラインナップを充実させる原動力となっています。

- パーソナルケア製品に対する需要の高まりは、プラスチックボトル・容器市場を大きく押し上げています。この急増は、プラスチック包装の実用性、費用対効果、汎用性によるところが大きいです。消費者が化粧品やパーソナルケアにおいて利便性と革新的なデザインに傾倒するにつれ、プラスチック容器が最適なソリューションとして浮上しています。プラスチックボトルは、ローション、クリーム、シャンプー、美容液など、美容・パーソナルケア業界の多様なニーズに巧みに応えることができます。

- 北米では機能性飲料産業が拡大しており、市場の成長を後押ししています。これは、プラスチック包装の利便性と携帯性に起因しており、外出先での飲料や健康中心の飲料に対する消費者の嗜好の高まりと共鳴しています。

- 2024年3月、米国を拠点とする飲料会社Roar Organicは、地元企業から1,000万米ドルの投資を受けました。この資金調達は、ロアー社の製品ラインナップを拡大することを目的としており、同社が風味のある非炭酸の「機能性」飲料をレディ・トゥ・ドリンクと粉末の両形態で導入できるよう支援するものです。このような戦略的投資は、今後数年間の市場の成長を後押しするものと思われます。

- 米国では、PETとHDPEが市場を独占しています。費用対効果と使いやすさからプラスチック製が好まれるため、PETボトルが大きな市場シェアを占めると予想されます。

- しかし、環境意識が高まるにつれ、プラスチック使用の勢いは弱まると予想されます。米国とカナダでは顕著な変化が見られ、消費者は環境に優しいパッケージング・ソリューションに惹かれています。プラスチックに関連する環境上の危険性を認識し、両国とも厳しい規制を制定しているため、代替素材に比べてプラスチックの成長率は抑えられています。

- とはいえ、持続可能なプラスチックボトルに対する需要の高まりは、特にリサイクル素材の開発という点で、市場の企業に新たな道を開いています。

北米のプラスチックボトル・容器市場の動向

飲料用包装材に対する需要の高まりがポリエチレンテレフタレート(PET)の使用を増加させている

- ポリエチレンテレフタレート(PET)は、水蒸気、ガス、希酸、油、アルコールに対する強固なバリア性があるため、飲料用包装材として好まれています。PETはその保護性だけでなく、飛散防止性、適度な柔軟性、リサイクル性にも優れています。その耐久性と安定性により、PETは個々の飲料ボトルや容器を含む食品グレードの製品に理想的な選択肢となっています。

- アースデイ・オーガナイザーによると、米国では毎分100万本ものペットボトルが販売されています。

- 炭酸飲料(CSD)分野ではペットボトルの使用量が急増しているが、北米では現在飽和状態に達しています。ペプシ、コカ・コーラ、キューリグ・ドクター・ペッパーなどの業界大手は、北米のCSD部門の売上が停滞していると報告しています。コカ・コーラの年次報告書では、これら3社が北米市場シェアの80%以上を占めていると推定されています。この優位性は、CSD部門におけるペットボトルの需要が今後も続くことを示唆しています。

- 2024年3月、米国を拠点とする飲料会社Roar Organicは、風味のついた、炭酸の入っていない「機能性」飲料をReady-to-drinkや粉末の形態で含む製品群を拡大するために、地元企業Factory LLCから1,000万米ドルの投資を受けました。このような投資は、予測期間中に市場にチャンスをもたらすと期待されています。

- 清涼飲料の包装は、PETの優れたCO2保持力により、ポリエチレンテレフタレート(PET)ボトルが主流を占めています。しかし、PET包装の汎用性はソフトドリンクにとどまらず、フルーツジュース、エナジードリンク、スポーツドリンク、ワイン、スピリッツ、ビールなどのアルコール飲料にも及んでいます。米国では蒸留酒の販売が急増しており、100%PETボトルの需要がこの地域の市場成長を後押しすると予測されています。

化粧品業界でプラスチック包装の採用が急増する

- プラスチックは、化粧品包装に好まれる素材として際立っています。その柔軟性は詳細なデザインを可能にし、その保護性は中の製品の安全性を保証します。その結果、プラスチックボトルと容器が化粧品業界の包装を支配し、かなりの市場シェアを確保しています。

- 包装機械工業会(PMMI)のデータによると、ボトル、ジャー、コンパクト、チューブなどのプラスチック包装は、化粧品・パーソナルケア業界で61%の圧倒的なシェアを占めています。なかでもプラスチックボトルが突出しており、単独で市場の30%を占めています。

- 米国は、化粧品、パーソナルケア用品、フレグランスの主要市場です。米国ではミレニアル世代の人口が多く、市場の需要を支えています。ミレニアル世代は国の労働力として、デオドラント、香水、化粧品のようなパーソナルケア製品を優先し、外見の重要性を強調しています。その結果、化粧品の需要が急増するにつれて、プラスチック容器を含むパッケージの需要も地域全体で並行して増加しています。

- 持続可能性に向けた協調的な取り組みとして、化粧品会社は環境に優しいプラスチック包装ソリューションをますます追求するようになっています。2020年8月、米国ロレアルは他の60ブランド、政府代表、小売業者、NGOと共同で、2025年までに米国内のすべてのプラスチック包装を再利用可能、リサイクル可能、堆肥化可能のいずれかにすることを約束しました。

北米のプラスチックボトル・容器市場概要

北米のプラスチックボトル・容器市場は断片化されており、複数の企業で構成されています。市場シェアでは、現在少数の大手企業が市場を独占しています。これらの企業は、海外における顧客基盤の拡大に注力しています。これらの企業は、市場シェアと収益性を高めるために、戦略的な共同イニシアティブを活用しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- 地政学的動向の業界への影響評価

第5章 市場力学

- 市場促進要因

- 軽量包装の採用増加

- 化粧品業界におけるプラスチック包装の採用急増

- 市場抑制要因

- 原材料価格の変動

- プラスチック使用に対する環境問題の高まり

第6章 市場セグメンテーション

- 素材タイプ別

- ポリエチレンテレフタレート(PET)

- ポリエチレンテレフタレート(PET)

- 低密度ポリエチレン(LDPE)

- 高密度ポリエチレン(HDPE)

- その他の材料タイプ

- 業界別

- 飲料

- アロコール飲料

- ノンアルコール飲料

- 食品

- 化粧品

- 医薬品

- 家庭用品

- その他業界別

- 飲料

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Alpha Packaging Inc.

- Altium Packaging(Loews Corporation)

- Gerresheimer AG

- Graham Packaging Company LP

- Berry Global Group Inc.

- Plastipak Holdings Inc.

- Amcor Plc

- Graham Packaging

- AptarGroup Inc.

- Comar LLC

第8章 投資分析

第9章 市場の将来展望

The NA Plastic Bottles And Containers Market size in terms of shipment volume is expected to grow from 8.06 million metric tons in 2025 to 9.49 million metric tons by 2030, at a CAGR of 3.32% during the forecast period (2025-2030).

Well-established manufacturing capabilities and a resilient export sector mark North America's plastic bottles and containers market landscape. Packaging plays a pivotal role in the consumption of both consumer and industrial products. In North America, the rising demand for sustainable and convenient packaging solutions is propelling the market's growth.

Key Highlights

- While several emerging nations are making their mark, the United States remains a dominant player in the global pharmaceutical arena. Home to major pharmaceutical companies, the United States not only commands a significant market share but also provides its consumers with access to cutting-edge products. This robust pharmaceutical landscape is spurring innovations and advancements in the plastic bottles and containers market.

- For example, in February 2023, Berry Global, a US company, unveiled a comprehensive solution tailored for the pharmaceutical and herbal markets. This new offering, known as the Berry Healthcare bundle, includes a diverse range of 28 mm neck PET bottles spanning sizes from 20 ml to 1,000 ml and features eight closures with tamper-evident and child-resistant attributes.

- The North American beauty and personal care industry, which includes everything from cosmetics to skincare, is witnessing a surge in demand for premium and innovative products. This trend is driving leading brands to enhance their offerings.

- The rising demand for personal care products is significantly boosting the plastic bottles and containers market. This surge is largely due to the practicality, cost-effectiveness, and versatility of plastic packaging. As consumers lean toward convenience and innovative designs in cosmetics and personal care, plastic containers are emerging as the go-to solution. Plastic bottles can adeptly cater to the diverse needs of the beauty and personal care industry, including lotions, creams, shampoos, and serums.

- The expanding functional beverage industry in North America is fueling market growth. This can be attributed to the convenience and portability of plastic packaging, resonating with consumers' increasing preference for on-the-go and health-centric beverages.

- In March 2024, Roar Organic, a beverage company based in the United States, secured a USD 10 million investment from a local firm. This funding aims to broaden Roar's product lineup, helping the company introduce flavored, non-carbonated "functional" drinks in both ready-to-drink and powdered formats. Such strategic investments are poised to bolster the market's growth in the coming years.

- In the United States, PET and HDPE dominate the market. With manufacturers favoring plastic for its cost-effectiveness and ease of use, PET bottles are expected to hold a significant market share.

- However, as environmental awareness grows, the momentum behind plastic usage is expected to decline. A notable shift is evident in the United States and Canada, where consumers are gravitating toward eco-friendly packaging solutions. Recognizing the environmental hazards linked to plastic, both countries have enacted stringent regulations, leading to a tempered growth rate for plastic compared to alternative materials.

- Nevertheless, the rising demand for sustainable plastic bottles is opening new avenues for companies in the market, particularly in terms of developing recycled materials.

Key Highlights

North America Plastic Bottles & Containers Market Trends

Rising Demand for Beverage Packaging Attributes is Increasing the Usage of Polyethylene Terephthalate (PET)

- Polyethylene terephthalate (PET) is a preferred choice for beverage packaging owing to its robust barrier properties against water vapor, gases, dilute acids, oils, and alcohol. Beyond its protective qualities, PET boasts shatter resistance, moderate flexibility, and recyclability. Its durability and steadfastness make PET an ideal choice for food-grade products, including individual drink bottles and containers.

- According to Earth Day Organizers, the United States sees a staggering sale of about 1 million plastic bottles every minute, primarily fueled by the region's demand for packaged drinking water.

- While the carbonated soft drinks (CSD) segment has seen a surge in plastic bottle usage, it is now reaching saturation in North America. Industry giants, including Pepsi, Coca-Cola, and Keurig Dr Pepper, reported stagnant sales in their North American CSD divisions. Coca-Cola's annual report estimated that these three companies commanded over 80% of the North American market share. This dominance suggests a continued demand for plastic bottles in the CSD segment.

- In March 2024, Roar Organic, a United States-based beverage company, attracted a USD 10 million investment from local firm Factory LLC to expand its product range, including flavored, non-carbonated "functional" drinks in ready-to-drink and powdered formats. Such investments are expected to create opportunities for the market during the forecast period.

- Soft drink packaging is predominantly led by polyethylene terephthalate (PET) bottles due to PET's superior CO2 retention. However, the versatility of PET packaging is not limited to soft drinks; it also encompasses fruit juices, energy drinks, sports drinks, and a range of alcoholic beverages, including wine, spirits, and beer. With the United States witnessing a surge in spirits sales, the demand for 100% PET bottles is projected to boost the regional market growth.

Plastic Packaging Adoption is Set to Surge in the Cosmetics Industry

- Plastic stands out as the preferred material for cosmetics packaging. Its flexibility enables detailed designs, and its protective nature ensures the safety of the products within. Consequently, plastic bottles and containers dominate the cosmetics industry's packaging landscape, securing a substantial market share.

- According to data from the Packaging Machinery Manufacturers Institute (PMMI), plastic packaging, including bottles, jars, compacts, and tubes, commanded a dominant 61% share in the cosmetics and personal care industries. Among these, plastic bottles were particularly prominent, accounting for a notable 30% of the market independently.

- The United States is a leading market for cosmetics, personal care items, and fragrances. A significant segment of the US millennial population fuels the market demand. As the dominant force in the nation's workforce, millennials prioritize personal care products-like deodorants, perfumes, and cosmetics-underscoring the importance of physical appearance. Consequently, as the demand for cosmetics surges, there is a parallel uptick in the demand for packaging, including plastic containers, across the region.

- In a concerted effort toward sustainability, cosmetic companies are increasingly pursuing eco-friendly plastic packaging solutions. Highlighting this dedication, in August 2020, L'Oreal USA, in collaboration with 60 other brands, government representatives, retailers, and NGOs, made a commitment to have all plastic packaging in the US be either reusable, recyclable, or compostable by 2025.

North America Plastic Bottles & Containers Market Overview

The North American plastic bottles and containers market is fragmented and consists of several players. In terms of market share, a few major players currently dominate the market. These players are focusing on expanding their customer base across foreign countries. These companies leverage strategic collaborative initiatives to increase their market shares and profitability.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of Geopolitical Developments on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Lightweight Packaging

- 5.1.2 Plastic Packaging Adoption Set to Surge in the Cosmetics Industry

- 5.2 Market Restraints

- 5.2.1 Fluctuating Raw Materials Prices

- 5.2.2 Growing Environment Concerns Over the Use of Plastics

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Polyethylene Terephthalate (PET)

- 6.1.2 Polyethylene Terephthalate (PET)

- 6.1.3 low-density polyethene (LDPE)

- 6.1.4 high-density polyethene (HDPE)

- 6.1.5 Others Materials Types

- 6.2 By End-user Vertical

- 6.2.1 Beverage

- 6.2.1.1 Alocholic Beverages

- 6.2.1.2 Non-Alocholic Bevearges

- 6.2.2 Food

- 6.2.3 Cosmetics

- 6.2.4 Pharmaceuticals

- 6.2.5 Household Care

- 6.2.6 Other End-user Verticals

- 6.2.1 Beverage

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Alpha Packaging Inc.

- 7.1.2 Altium Packaging (Loews Corporation)

- 7.1.3 Gerresheimer AG

- 7.1.4 Graham Packaging Company LP

- 7.1.5 Berry Global Group Inc.

- 7.1.6 Plastipak Holdings Inc.

- 7.1.7 Amcor Plc

- 7.1.8 Graham Packaging

- 7.1.9 AptarGroup Inc.

- 7.1.10 Comar LLC