|

市場調査レポート

商品コード

1550520

アジア太平洋のプラスチックボトル市場:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Asia Pacific Plastic Bottles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋のプラスチックボトル市場:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

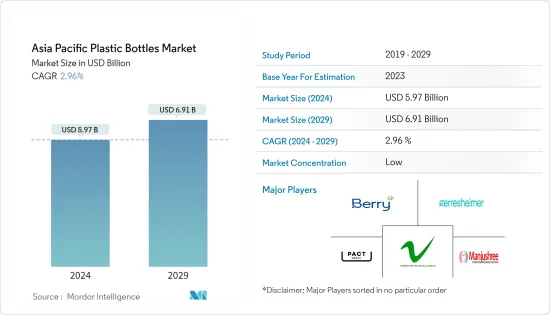

アジア太平洋のプラスチックボトル市場規模は、2024年に59億7,000万米ドルと推定され、予測期間(2024-2029年)のCAGRは2.98%で成長し、2029年には69億1,000万米ドルに達すると予測されます。

生産量では、市場は2024年の650万トンから2029年には749万トンに、予測期間(2024-2029年)のCAGRは2.87%で成長すると予測されます。

ペットボトルは、飲料、食品、化粧品、製薬など様々な分野で重要な役割を果たしています。新技術と耐熱性PETボトルの出現が新たな可能性と選択肢を広げ、予測期間中の市場需要を押し上げる可能性があります。

主なハイライト

- プラスチック包装は軽量で割れにくく、取り扱いが簡単なため、消費者の支持は高まっています。大手メーカーも費用対効果の高さからプラスチック包装に傾倒しています。ポリエチレンテレフタレート(PET)や高密度ポリエチレン(HDPE)のようなポリマーの登場は、プラスチックボトルの用途の幅を広げ、PETボトル需要の急増につながっています。

- エンドユーザーは主にポリエチレンテレフタレート、ポリプロピレン、ポリエチレン製のプラスチックボトルや容器を選んでいます。このような嗜好は、素材が軽量でリサイクルしやすいことに起因しています。さらに、プラスチックの費用対効果は、パッケージ化された加工食品や飲食品への依存度の高まりと相まって、市場力学を形成するように設定されています。

- オリエンタル・グリーン・マテリアルズ・リミテッドによると、台湾では年間平均50億本のペットボトルが使用されており、その半分はオリエンタルの敷地内でリサイクルされています。ボトルは粉砕、洗浄され、ペレットに変換され、ボトルやその他の製品に使用されます。

- さらに、国家環境庁とF&Nフード・シンガポールは数年前、スマートな逆自動販売機(RVM)をシンガポール全土に展開するイニシアチブを開始しました。これは、飲料容器(ペットボトル)をRVMに預けてリサイクルする便利な方法を提供することで、シンガポールの人々にエココンシャスなライフスタイルを奨励することを目的としています。PETはその耐久性、費用対効果、汎用性から好まれています。飲食品、製薬、その他の分野などのエンドユーザー産業が拡大・革新するにつれて、ペットボトルや容器包装のニーズも高まっています。

- プラスチックは重大な汚染物質とみなされ、環境悪化をもたらします。プラスチックの影響に関する意識は、ユーザーや業界のエコシステム全体で高まっています。この意識を高めるために、政府によって多くの公共活動や取り組みが行われています。プラスチックの消費と生産は大量の化石燃料を使用し、環境と気候に悪影響を与えます。その結果、プラスチック包装の使用量はここ数年で顕著に減少しています。

アジア太平洋プラスチックボトル市場動向

ポリエチレンテレフタレート(PET)が成長する

- PETボトルは、その軽量性と耐久性により、従来のガラス瓶に取って代わりつつあります。この変化は、ミネラルウォーターやその他の飲料の包装の再利用性を高め、輸送プロセスを合理化し、費用対効果を高めています。

- PETは透明度が高く、天然のCO2バリア特性を持つため、幅広い用途があり、ボトルへの吹き込みやその他の形状への成形が容易です。PETの特性は、着色剤、UVカット剤、酸素バリアー/スカベンジャー、その他の添加剤で改善することができ、ブランドの特定のニーズに合ったボトルを開発することができます。

- PETは、この地域のボトルメーカーの間で重要な包装材料となっています。さまざまな形状やサイズに対応できるその汎用性は、従来のガラスや金属容器に代わる比類のない選択肢を提供し、包装業界で非常に望ましい選択肢となっています。

- ポリエチレンテレフタレート(PET)ボトルは様々な製品分野で存在感を増しています。PETボトルは低コストで軽量であり、印刷技術の開発が進んでいることから、高級志向の消費者の間で人気が高まっています。中国国家統計局によると、2023年5月の中国のプラスチック製品生産量は630万トンだった。2023年9月には682万トンに増加しました。中国におけるプラスチック生産量の増加は、PET製品の市場を強化すると予想されます。

- クローズドループリサイクルとは、プラスチックがリサイクルされ、同じカテゴリー内の新しい製品の製造に利用されるプロセスを指します。このアプローチはPETボトルで一般的に採用されており、企業は代替樹脂材料よりもPETボトルを優先することができます。その結果、ペットボトルのリサイクルは市場に好影響を与えると予想されます。持続可能な化学企業Indorama Venturesの報告書によると、アジアにおける再生ポリエチレンテレフタレート(rPET)の需要は、2018年の60万トンから2023年には約100万トンに絶えず増加すると予想されています。

飲料分野が市場成長を牽引すると予想される

- PETボトルは、その耐久性とリサイクル性により、ガラスやプラスチックボトルよりも水のパッケージング市場で普及しています。この動向は、軽量で耐久性があり、費用対効果の高いPETが水の包装媒体として定着しつつあることを示しています。さらに、PETボトルは包装の動向や本体に貼るラベルに応じて様々な形状に成形することができます。

- 国連大学の水・環境・健康研究所によると、インドでは一般的にボトル入りの水に使われるPETプラスチックが年間1万4,000トン以上消費されています。さらに、この地域は最も急成長しているミネラルウォーター市場のひとつでもあります。国際ボトルウォーター協会の報告書によると、ボトル入り飲料水の約97%がプラスチック製で、そのうち80%近くがポリエチレンテレフタレート(PET)製です。

- 企業はまた、ボトル入り飲料水のさまざまな形態を革新しています。そのため、各社はユニークな戦略でボトルを宣伝し、市場に話題を提供する機会を得ています。例えば、インドでは2023年12月にISI認証のボトル入り飲料水が導入され、広告主が最低コストでブランディングでき、ブランディングスペースの80%を活用できるようになった。広告主はブランドのアカウントを設定し、デザインをアップロードし、ラベルテンプレートとリンクさせることで、ターゲット層に合わせたマーケティング戦略を立てることができます。

- 消費者側から再利用可能なペットボトルに詰め替える、ペットボトルの製造に生分解性ペットボトルや再生ペットボトルを使用する、環境に優しいデザインを革新する、さまざまなエンドユーザーから発生するペットボトルをリサイクルするために別の協議会を設立するなど、さまざまなスキームを取り入れることで、地域全体の政府が使い捨てペットボトルのリサイクルに力を入れています。この地域のメーカーは、この分野で持続可能なメーカーとなるために、政府の法律や企業のガイドラインに基づくリサイクル可能性の基準を満たす水筒を導入するために技術革新を行っています。

- インドはこの地域で最も強力な市場のひとつであり、人口も最も多いです。同国ではボトル入り飲料水の消費量が大幅に増加しています。Indian Railway Catering and Tourism Corporation Limitedは、ペットボトル入り飲料水のブランド "Rail Neer "を立ち上げ、主に列車や駅で販売しています。ペットボトルの消費量の増加と鉄道部門の成長に伴い、同公社はペットボトルの生産量を2021年の7,530万本から2023年には3億5,770万本に増やしました。

アジア太平洋プラスチックボトル産業概要

アジア太平洋のプラスチックボトル市場は断片化されており、 Gerresheimer AG, Pact Group Holdings Limited, Berry Global Inc., Shenzhen Zhenghao Plastic & Mold, Manjushree Technopack Limitedなど、様々な国内外のプレーヤーが存在します。この地域で事業を展開する企業は、提携、拡大、投資、その他の戦略を通じて事業の拡大に注力しています。

- 2023年12月ビクトリア州の容器寄託制度の開始と同時に、メルボルンで5,000万米ドルの新しい施設が操業を開始しました。この施設では、年間最大10億本の600mlペットボトル飲料をリサイクルできます。サーキュラー・プラスチックス・オーストラリア(PET)が運営するこの工場は、使用済み飲料ボトルを高品質の食品用樹脂に変えます。この樹脂はその後、新しい再生PET飲料ボトルや飲食品パッケージの製造に利用されます。

- 2023年11月ベリー世界は、CPHIインド展示会において、インドおよび南アジア地域向けに、患者中心のパッケージング、ディスペンシングソリューション、ドラッグデリバリー機器のパイオニアであることをアピールしました。ベリーのブースでは、ボトルやその他の製品を含む、同社の膨大なポートフォリオから様々な製品を紹介しました。展示ショーケースでは、使いやすさの向上、投与安全性、医療機器や一次包装の次世代デジタル化、循環型デザインへの取り組みを強調し、同社の最先端ソリューションにスポットライトを当てた。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界の規制と政策、規格

- 関連HSコードのプラスチックボトルの輸出入分析

第5章 市場力学

- 市場促進要因

- 軽量プラスチックボトルの採用増加

- 人口動態とライフスタイルの変化

- 市場の課題

- ペットボトル廃棄に関する懸念の高まり

第6章 市場セグメンテーション

- 樹脂別

- ポリエチレン(PE)

- ポリエチレンテレフタレート(PET)

- ポリプロピレン(PP)

- その他の樹脂タイプ(ポリスチレン、PVC、ポリカーボネートなど)

- エンドユーザー産業別

- 食品

- 飲料

- ボトル入り飲料水

- 炭酸飲料

- アルコール飲料

- ジュースとエナジードリンク

- その他の飲料

- 医薬品

- パーソナルケアとトイレタリー

- 工業用

- 家庭用化学品

- 塗料

- その他のエンドユーザー産業

- 国別

- 中国

- インド

- 日本

- タイ

- オーストラリア・ニュージーランド

- インドネシア

- ベトナム

第7章 競合情勢

- 企業プロファイル

- Gerresheimer AG

- Pact Group Holdings Limited

- ALPLA Group

- Berry Global Inc.

- Alpha Packaging Pvt. Ltd

- Greiner Packaging international GmbH

- Retal Industries Limited

- Zhejiang Xinlei Packaging Co. Ltd

- Shenzhen Zhenghao Plastic & Mold Co. Ltd

- Manjushree Technopack Limited

- Heat Map Analysis

- Competitor Analysis-Emerging vs. Established Players

第8章 リサイクルと持続可能性の展望

第9章 将来の展望

The Asia Pacific Plastic Bottles Market size is estimated at USD 5.97 billion in 2024, and is expected to reach USD 6.91 billion by 2029, growing at a CAGR of 2.98% during the forecast period (2024-2029). In terms of production volume, the market is expected to grow from 6.5 million tonnes in 2024 to 7.49 million tonnes by 2029, at a CAGR of 2.87% during the forecast period (2024-2029).

Plastic bottles are crucial in various sectors, including the beverage, food, cosmetics, and pharmaceutical industries. New technologies and the emergence of heat-resistant PET bottles are opening new possibilities and options, which might push the market demand over the forecast period.

Key Highlights

- Consumers increasingly favor plastic packaging because it is lightweight and unbreakable, simplifying handling. Major manufacturers also gravitate toward plastic packaging because of its cost-effectiveness. The advent of polymers like polyethylene terephthalate (PET) and high-density polyethylene (HDPE) is broadening the horizons for plastic bottle applications, leading to a surge in PET bottle demand.

- End users predominantly choose plastic bottles and containers made from polyethylene terephthalate, polypropylene, and polyethylene. This preference stems from the materials' lightweight nature and recyclability. Furthermore, the cost-effectiveness of plastics, coupled with the growing reliance on packaged and processed foods and beverages, is set to shape the market dynamics.

- According to Oriental Green Materials Limited, Taiwan uses an average of 5 billion PET bottles yearly, half of which are recycled on Oriental's premises. The bottles are smashed, cleaned, and converted to pellets, which are then used to make bottles and other products.

- Further, the National Environment Agency and F&N Food Singapore launched an initiative to roll out smart Reverse Vending Machines (RVMs) across Singapore a few years ago. This aims to encourage Singaporeans to adopt an eco-conscious lifestyle by offering them a convenient recycling method for recycling drinks containers (plastic bottles) by depositing them in the RVMs. PET is preferred owing to its durability, cost-effectiveness, and versatility. As the end-user industries, such as food, beverage, pharmaceutical, and other sectors, expand and innovate, the need for plastic bottles and container packaging also rises.

- Plastic is a considered as significant pollutant, resulting in environmental degradation. Awareness regarding plastic's effects has been growing among users and across the industry ecosystem. Many public drives and initiatives are conducted by governments to increase this awareness. The consumption and production of plastics use large quantities of fossil fuels, which adversely impact the environment and climate. As a result, plastic packaging usage has notably declined over the past few years.

Asia Pacific Plastic Bottles Market Trends

Polyethylene Terephthalate (PET) To Witness Growth

- PET plastic bottles are increasingly supplanting traditional glass bottles, thanks to their lightweight nature and durability. This shift enhances the reusability of packaging for mineral water and other beverages and streamlines the transportation process, making it more cost-effective.

- With its clarity and natural CO2 barrier properties, PET has wide applications and can be easily blown into a bottle or molded into any other shape. PET's properties can be improved with colorants, UV blockers, oxygen barriers/scavengers, and other additives to develop a bottle to match a brand's specific needs.

- PET has become a vital packaging material among bottle manufacturers across the region. Its versatility in accommodating different shapes and sizes has provided unparalleled alternatives to conventional glass and metal containers, making it a highly desirable choice in the packaging industry.

- Polyethylene terephthalate (PET) bottles are gaining a presence in various product areas. PET bottles' low cost and low weight and ongoing developments in printing technology have led to their popularity among premium consumers. According to the National Bureau of Statistics of China, the production of plastic products in China was 6.3 million metric tons in May 2023. It increased to 6.82 million metric tons in September 2023. The rise in the production of plastics in China is expected to enhance the market for PET products.

- Closed-loop recycling refers to a process where plastic is recycled and utilized to manufacture a new product within the same category. This approach is commonly embraced by PET bottles, enabling businesses to prioritize it over alternative resin materials. Consequently, the recycling of plastic bottles is expected to have a favorable influence on the market. As per the report of Indorama Ventures, a sustainable chemical company, the demand for recycled polyethylene terephthalate (rPET) in Asia is expected to increase constantly from 0.6 million metric tons in 2018 to approximately 1 million metric tons in 2023.

The Beverage Sector is Expected to Drive Market Growth

- PET bottles are more prevalent in the water packaging market than glass and plastic bottles due to their durability and recyclability. The trend shows that lightweight, durable, and cost-effective PET is becoming the default packaging medium for water. Moreover, PET bottles can be molded in different shapes according to the packaging trend and the labels to be applied to the body.

- According to the UN University Institute for Water, Environment, and Health, more than 14 lakh tons of PET plastic, commonly used for bottled water, are consumed annually in India. Further, the region is also one of the fastest-growing mineral water markets. According to a report by the International Bottled Water Association, about 97% of bottled water bottles are plastic, and nearly 80% of that is from polyethylene terephthalate (PET).

- Companies also innovate different formats of bottled water. This provides opportunities for the companies to promote the bottles with unique strategies to create a market buzz. For instance, India introduced ISI-certified bottled water in December 2023, which can be branded by advertisers at the lowest cost, leveraging 80% of the branding space. Advertisers can set up an account for their brand, upload their design, and link it to the label template to tailor their marketing strategies for their target audience.

- Governments across the region are focusing on the recycling of single-use plastic bottles by incorporating various schemes, such as refilling a reusable plastic bottle from the consumer side, using biodegradable or recycled PET bottles for the manufacturing of plastic bottles, innovating eco-friendly designs, and setting up a different council to recycle plastic bottles generated by various end users. Manufacturers across the region innovate to introduce water bottles that fulfill the recyclability criteria under government laws and company guidelines to become sustainable manufacturers in the sector.

- India is one of the strongest markets in the region and has the highest population. There has been a significant increase in the consumption of bottled water in the country. The Indian Railway Catering and Tourism Corporation Limited launched a PET bottled water brand, "Rail Neer," which is majorly sold on trains and railway stations. With the rising consumption of water bottles and the growing railway sector, the corporation increased the production of bottles from 75.30 million bottles in 2021 to 357.70 million bottles in 2023.

Asia Pacific Plastic Bottles Industry Overview

The Asia-Pacific plastic bottles market is fragmented, with various domestic and international players such as Gerresheimer AG, Pact Group Holdings Limited, Berry Global Inc., Shenzhen Zhenghao Plastic & Mold Co. Ltd, Manjushree Technopack Limited, and others. The companies operating in the region are focused on expanding their businesses through collaborations, expansions, investments, and other strategies.

- December 2023: A new USD 50 million facility began operations in Melbourne, coinciding with the launch of Victoria's Container Deposit Scheme. This facility can recycle up to one billion 600 ml PET plastic beverage bottles annually. Operated by Circular Plastics Australia (PET), the plant transforms used beverage bottles into high-quality, food-grade resin. This resin is subsequently utilized to manufacture new recycled PET beverage bottles and food packaging items.

- November 2023: Berry Global highlighted its dedication to pioneering patient-centric packaging, dispensing solutions, and drug delivery devices tailored for India and the broader South Asian region at the CPHI India exhibition. Berry's stand featured various products from its vast portfolio, including bottles and other products. The exhibition showcase spotlighted the company's cutting-edge solutions, emphasizing enhanced usability, administration safety, next-gen digitalization for medical devices and primary packaging, and a commitment to circular design.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Industry Regulations, Policies, and Standards

- 4.5 Import and Export Analysis of Plastic Bottles for the Relevant HS Code

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Lightweight Plastic Bottles

- 5.1.2 Changing Demographic and Lifestyle Factors

- 5.2 Market Challenges

- 5.2.1 Growing Concerns Regarding Plastic Bottle Disposal

6 MARKET SEGMENTATION

- 6.1 By Resin

- 6.1.1 Polyethylene (PE)

- 6.1.2 Polyethylene Terephthalate (PET)

- 6.1.3 Polypropylene (PP)

- 6.1.4 Other Resin Types (Polystyrene, PVC, Polycarbonate, etc.)

- 6.2 By End-user Industries

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.2.1 Bottled Water

- 6.2.2.2 Carbonated Soft Drinks

- 6.2.2.3 Alcoholic Beverages

- 6.2.2.4 Juices and Energy Drinks

- 6.2.2.5 Other Beverages

- 6.2.3 Pharmaceuticals

- 6.2.4 Personal Care and Toiletries

- 6.2.5 Industrial

- 6.2.6 Household Chemicals

- 6.2.7 Paints and Coatings

- 6.2.8 Other End-user Industries

- 6.3 By Country

- 6.3.1 China

- 6.3.2 India

- 6.3.3 Japan

- 6.3.4 Thailand

- 6.3.5 Australia and New Zealand

- 6.3.6 Indonesia

- 6.3.7 Vietnam

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Gerresheimer AG

- 7.1.2 Pact Group Holdings Limited

- 7.1.3 ALPLA Group

- 7.1.4 Berry Global Inc.

- 7.1.5 Alpha Packaging Pvt. Ltd

- 7.1.6 Greiner Packaging international GmbH

- 7.1.7 Retal Industries Limited

- 7.1.8 Zhejiang Xinlei Packaging Co. Ltd

- 7.1.9 Shenzhen Zhenghao Plastic & Mold Co. Ltd

- 7.1.10 Manjushree Technopack Limited

- 7.2 Heat Map Analysis

- 7.3 Competitor Analysis - Emerging vs. Established Players