北米のペット用栄養補助食品市場:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

North America Pet Nutraceuticals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 228 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687108

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

北米のペット用栄養補助食品市場規模は2025年に23億9,000万米ドルと推定され、2030年には31億5,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは5.71%で成長する見込みです。

犬は関節の問題や消化器系の問題など、多くの健康問題を抱えやすいため、栄養補助食品の主要な消費者です。

- ペット用栄養補助食品は、ペットの健康と福祉を改善するために特別に配合されたサプリメントです。2022年には、北米ペットフード市場の2.8%を占めていました。栄養補助食品のシェアは2017年と比較して2022年には9.9%増加したが、これは主に予防医療の重要性に対するペットオーナーの意識の高まりによるものです。2021年の調査では、米国の犬猫の飼い主の10人に4人が、パンデミックの開始以降、ペットの健康に気を配るようになったことが明らかになりました。

- 栄養補助食品市場の大半を占めるのは犬で、12億4,000万米ドル、次いで猫が5億8,140万米ドル、その他のペット動物が2億2,600万米ドルです。犬のシェアが大きいのは、他のペットに比べて人口が多いことが主因です。2022年、この地域の犬の数は1億4,400万匹で、猫は9,650万匹、その他のペット動物は1億490万匹でした。米国はこの地域で最もペット数が多く、69%(2億3,900万頭)を占めます。さらに、犬は関節の問題、皮膚アレルギー、消化器系の問題など、より幅広い健康問題に悩まされることが知られており、これがこの地域における栄養補助食品の需要増加につながっています。関節/可動性、ビタミン欠乏症、全般的健康状態、皮膚被毛、免疫力は、ペットの飼い主が犬と猫の両方にお金をかけている最も人気のある症状の一つです。

- ペットの飼い主の人間化傾向の高まり、ペットの高齢化、専門化ニーズの高まり、eコマース・チャネルの台頭が市場を牽引する主要要因であり、予測期間中にCAGR 5.6%を記録すると予測されています。

米国が北米の栄養補助食品市場を独占、主にビタミン・ミネラルセグメントが牽引

- 北米のペット用栄養補助食品市場は近年著しい成長を遂げており、予測期間中もこの傾向が続くとみられます。この成長の主要動因のひとつは、ペットの人間化傾向の高まりであり、ペットの飼い主がペットを家族の一員として扱うようになり、ペットの全体的な健康と幸福に注目するようになっています。

- 米国は北米市場を独占し、2022年には金額ベースで88.7%のシェアを占めました。その優位性は主に、同国のペット数の多さによるもので、2022年には2億3,910万頭に達し、北米ペット数の約69.2%を占めました。この巨大なペット数により、米国のペット用栄養補助食品市場規模は予測期間中にCAGR 5.0%を記録すると予測されています。

- カナダは北米市場で第2位のシェアを持ち、2022年の市場規模は1億2,640万米ドルです。米国に比べペットを飼う世帯数が少ないため、2番目のシェアとなっています。同国では、ペットの健康に対する意識が高まり、ペットへの支出が増加しているため、予測期間中にCAGR 9.1%を記録すると予想されています。例えば、カナダのペット数は2022年には2,830万人でした。

- メキシコは2022年の市場シェアの約3.8%を占めています。同国の市場シェアが限られているのは、主にペット数が限られているためです。しかし、ペットのヒューマニゼーションの動向が高まっていることから、メキシコ市場は予測期間中にCAGR 9.4%を記録すると予測されています。

- その他の北米地域のペット用栄養補助食品市場は、予測期間中にCAGR 10.6%を記録すると予測されます。ペットの健康と福祉に対する飼い主の関心の高まりが、予測期間中に同セグメントを押し上げると予測されています。

北米のペット用栄養補助食品市場動向

若年層やミレニアル世代による猫飼育の増加がキャットフード市場を牽引

- 北米ではペットとしての猫の飼育が増加しているが、これは同伴者としての需要が高く、ペットフードへの支出が犬よりも猫の方が少ないためです。同地域では、ペットの人間化が進んでいることと、猫は犬よりも生活するのに必要な面積が少ないことから、ペットとしての猫は2017~2022年の間に13.6%増加しました。例えば米国では、猫をペットとして飼っている世帯は2020年には26%だったが、2022年には53.5%に増加しました。

- 米国、カナダ、メキシコでは、在宅勤務の文化が同伴者の需要につながり、ペットを飼う人の多くがミレニアル世代であることから、流行期にペットとしての猫の採用が増加しました。例えば、2022年には、米国ではミレニアル世代がペットの親の33%に達しました。2020年には、米国ではペットの猫の40%が動物保護施設から引き取られました。さらに、ペットの親は高収入のためペットショップから猫を購入し、2020年には米国の猫の親の43%がペットショップから猫を購入しています。したがって、この地域のペットとしての猫は2020~2022年の間に5.34%増加しました。

- 同地域では成猫よりも若い猫の方が多く飼われており、その数では米国がリードしています。例えば、2021年の米国の猫の飼育数は68万4,144頭で、若い猫が53.5%を占めています。若い猫の飼育数が増え、ミレニアル世代がペットの親となることで、予測期間中のペットフード製品の成長に貢献すると予想されます。猫の採用と購入の増加、ペットの人間化の増加がペット数の増加に貢献すると予想されます。

犬は猫よりも大量の餌を消費し、消化器系の問題に対する感受性が高いため、支出額が高いです。

- ペットの支出は北米で増加しています。ペット支出の増加は、さまざまな種類のペットフードが入手可能になったことと、米国とカナダでペットフード製品のプレミアム化が進んでいることによる。ペットの親がペットを家族として扱うようになり、特殊なペットフードに対する意識が高まるにつれて、ペット支出は増加すると予測されます。2020年には、ペットの健康ニーズに対する意識の高まりに伴い、ペットの親がペットに高い免疫力と消化器系の改善を望むため、ペット用サプリメントの売上が約200%増加しました。

- ペットの親が最も費用をかけるのはペットフードであり、これは予測期間中に増加すると予測されます。例えば、米国では2022年にペットフードがペット費用の42.4%を占めました。ドッグフードの支出シェアが猫よりも高いのは、犬の飼育数が多いことと、猫よりもフードの消費量が多いためです。ペットの親はペットを家族の一員と考え、高級ペットフードを与え、ペットグルーミングやペットデイケアなどのサービスを利用します。米国では、ペットの親の約40%がプレミアムペットフードを購入し、2022年にはペットのグルーミングや散歩などのサービスに114億米ドルが費やされました。

- ペットの親は、オンライン小売店、スーパーマーケット、ペットショップを通じてペットフードを購入します。様々なペットフード製品がeコマースサイトで販売されているため、オンライン小売業者を通じてペットフードの売上が増加しています。米国では、フードを含むペットケア製品のオンライン販売は、2020年の32%から2022年には40%に増加しました。プレミアム化と高品質フードの利点に関する意識の高まりが、この地域のペット支出を押し上げると予想される要因です。

北米ペット用栄養補助食品産業概要

北米のペット用栄養補助食品市場は適度に統合されており、上位5社で56.78%を占めています。この市場の主要企業は、 ADM, Mars Incorporated, Nestle(Purina)、Schell & Kampeter Inc.(Diamond Pet Foods)、Vetoquinolなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブプロダクト

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット

- 猫

- 犬

- その他

- 流通チャネル

- コンビニエンスストア

- オンラインチャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Alltech

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Dechra Pharmaceuticals PLC

- Mars Incorporated

- Nestle(Purina)

- Nutramax Laboratories Inc.

- Schell & Kampeter Inc.(Diamond Pet Foods)

- Vetoquinol

- Virbac

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

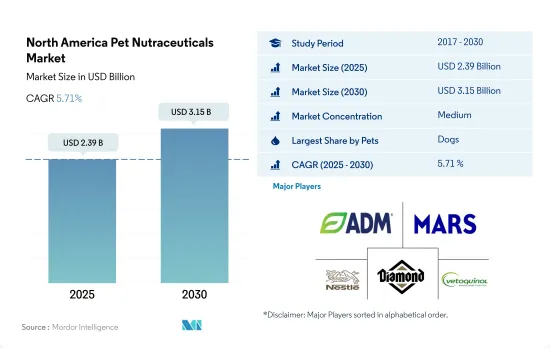

The North America Pet Nutraceuticals Market size is estimated at 2.39 billion USD in 2025, and is expected to reach 3.15 billion USD by 2030, growing at a CAGR of 5.71% during the forecast period (2025-2030).

Dogs are the major consumers of nutraceuticals as they are susceptible to many health problems, such as joint problems and digestive issues

- Pet nutraceuticals are supplements that are specifically formulated to improve the health and well-being of pets. In 2022, they accounted for 2.8% of the North American pet food market. The share of nutraceuticals increased by 9.9% in 2022 compared to 2017, mainly due to the increasing awareness among pet owners about the importance of preventive healthcare. In 2021, a study revealed that four in 10 cat and dog owners in the United States had paid more attention to their pet's health since the start of the pandemic.

- Dogs accounted for the majority of the nutraceuticals market, valued at USD 1.24 billion, followed by cats and other pet animals at USD 581.4 million and USD 226 million, respectively. The larger share of dogs is mainly due to their larger population compared to other pets. In 2022, there were 144 million dogs in the region, while cats and other pet animals accounted for 96.5 million and 104.9 million, respectively. The United States has the largest pet population in the region, accounting for 69% (239 million). Additionally, dogs are known to suffer from a wider range of health issues, such as joint problems, skin allergies, and digestive issues, which has led to increased demand for nutraceuticals in the region. Joint/mobility, vitamin deficiency, general health, skin coat, and immunity are among the most popular conditions where pet owners are spending money on both dogs and cats.

- The growing trend of humanization among pet owners, the aging pet population, growing specialized needs, and the rise of e-commerce channels are the major factors driving the market, and it is projected to register a CAGR of 5.6% during the forecast period.

The United States dominated the North American nutraceutical market, led mainly by the vitamins and minerals segment

- The North American pet nutraceuticals market has witnessed significant growth in recent years and is expected to continue this trend over the forecast period. One of the primary drivers of this growth has been the increasing pet humanization trend, with pet owners increasingly treating their pets as family members and focusing on their overall health and well-being.

- The United States dominated the North American market, accounting for an 88.7% share by value in 2022 . Its dominance was mainly due to the higher pet population in the country, which reached 239.1 million pets in 2022, accounting for about 69.2% of the North American pet population. With this huge pet population, the US pet nutraceuticals market value is anticipated to record a CAGR of 5.0% during the forecast period.

- Canada has the second-largest share in the North American market, valued at USD 126.4 million in 2022. It has the second-largest share because of a lower number of households adopting pets compared to the United States. The country is expected to record a CAGR of 9.1% during the forecast period as there is an increase in awareness about pet health and growing pet expenditure. For instance, the pet population in Canada was 28.3 million in 2022.

- Mexico accounted for about 3.8% of the market share in 2022. The limited market share of the country was mainly due to its limited pet population. However, with the rising trend in pet humanization, the Mexican market is anticipated to register a CAGR of 9.4% during the forecast period.

- The pet nutraceuticals market in the Rest of North America is anticipated to record a CAGR of 10.6% during the forecast period. The growing focus of pet owners on pet health and well-being is anticipated to boost the segment during the forecast period.

North America Pet Nutraceuticals Market Trends

The increasing adoption of cats by young adults and millennials is driving the cat food market

- There is an increase in the adoption of cats as pets in North America owing to the high demand for companionship and lesser expenditure on pet food for cats than dogs. In the region, cats as pets increased by 13.6% between 2017 and 2022 due to a rise in pet humanization and because cats require less area to live than dogs. For instance, in the United States, households owning a cat as a pet was 26% in 2020, which increased to 53.5% in 2022.

- The United States, Canada, and Mexico witnessed higher adoption of cats as pets during the pandemic because of the work-from-home culture leading to a demand for companionship and a higher number of pet owners being millennials. For instance, in 2022, millennials amounted to 33% of pet parents in the United States. In 2020, 40% of the pet cat population was adopted from animal shelters in the United States. Additionally, pet parents purchased cats from pet stores due to high income, and in 2020, 43% of cat parents in the United States purchased cats from pet stores. Therefore, cats as pets in the region increased by 5.34% between 2020 and 2022.

- Young cats are being adopted more than adult cats in the region, with the United States leading in terms of that number. For instance, in 2021, the adopted cat population in the United States was 684,144, and young cats accounted for 53.5% of the cats adopted. The higher population of young cats and millennials being pet parents is expected to help in the growth of pet food products during the forecast period. An increase in the adoption and purchase of cats and an increase in pet humanization are expected to help in the growth of the pet population.

Dogs accounted for higher expenditure as they consume a larger quantity of food than cats and have higher susceptibility to digestive issues

- Pet expenditure is increasing in North America. The rise in pet expenditure is due to the availability of different types of pet food and the growing premiumization of pet food products in the United States and Canada. Pet expenditure is projected to increase as pet parents increasingly treat their pets as family members and the awareness about specialized pet food rises. In 2020, there was a rise in pet supplement sales by about 200% as pet parents wanted their pets to have higher immunity and improved digestive systems, in line with greater awareness about pet health needs.

- The highest expenses of pet parents are on pet food, which is estimated to increase during the forecast period. For instance, pet food accounted for 42.4% of pet expenses in the United States in 2022. The expenditure share of dog food is higher than that of cats because the dog population is higher and because they consume a larger quantity of food than cats. Pet parents provide premium pet food to their pets and use services such as pet grooming and pet daycare in the region as they consider them as family members. In the United States, about 40% of pet parents purchased premium pet food, and USD 11.4 billion was spent on services such as pet grooming and pet walking in 2022.

- Pet parents purchase pet food through online retailers, supermarkets, and pet stores. Higher pet food sales are generated through online retailers as a variety of pet food products are available on e-commerce sites; also, the pandemic increased the number of online orders. In the United States, online sales of pet care products, including food, increased from 32% in 2020 to 40% in 2022. Premiumization and rising awareness about the benefits of quality food are factors anticipated to boost pet expenditure in the region.

North America Pet Nutraceuticals Industry Overview

The North America Pet Nutraceuticals Market is moderately consolidated, with the top five companies occupying 56.78%. The major players in this market are ADM, Mars Incorporated, Nestle (Purina), Schell & Kampeter Inc. (Diamond Pet Foods) and Vetoquinol (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Product

- 5.1.1 Milk Bioactives

- 5.1.2 Omega-3 Fatty Acids

- 5.1.3 Probiotics

- 5.1.4 Proteins and Peptides

- 5.1.5 Vitamins and Minerals

- 5.1.6 Other Nutraceuticals

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Country

- 5.4.1 Canada

- 5.4.2 Mexico

- 5.4.3 United States

- 5.4.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Alltech

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Dechra Pharmaceuticals PLC

- 6.4.5 Mars Incorporated

- 6.4.6 Nestle (Purina)

- 6.4.7 Nutramax Laboratories Inc.

- 6.4.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.4.9 Vetoquinol

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 228 Pages

- 納期

- 2~3営業日