|

市場調査レポート

商品コード

1685837

欧州のペット用栄養補助食品市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Pet Nutraceuticals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のペット用栄養補助食品市場:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 247 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

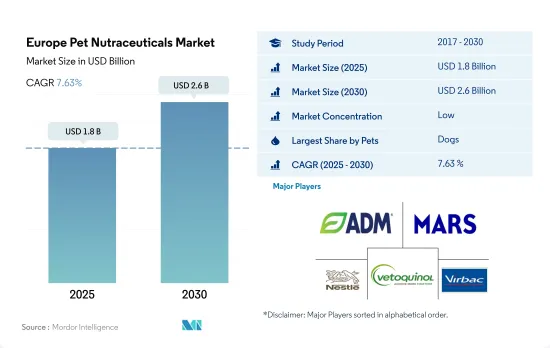

欧州のペット用栄養補助食品市場規模は2025年に18億米ドルと推計され、2030年には26億米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは7.63%で成長する見込みです。

ペットの健康に対する飼い主の関心の高まりにより、この地域では犬と猫がペット用栄養補助食品の最大消費者です。

- ペット用栄養補助食品はペットに栄養と治療効果を提供するように設計されています。ペット用栄養補助食品は、基本的な栄養を超えた健康上の利点を提供する食品源に由来します。これらの製品は、サプリメント、おやつ、噛むもの、粉末、液体など様々な形態で入手できます。欧州では、ペット用栄養補助食品は2022年のペットフード市場の3%を占めました。シェアが小さいのは、コストが高く、栄養補助食品の使い方や取り扱いに関する認識が低いためです。

- 欧州のペット用栄養補助食品市場では犬が大きなシェアを占め、2022年には7億4,490万米ドルと評価されました。ペット用栄養補助食品市場における犬のシェアが大きいのは、2022年の人口がかなり多く、欧州のペット数の30%であったことに関連しています。犬のペット用栄養補助食品市場は2017年から2021年にかけて14.2%成長したが、これは犬の飼育数が増加し、新しいペット用品に対する犬の飼い主の受容性が高まったためです。

- 猫もこの地域のペット用栄養補助食品市場の大半を占めており、2022年には5億2,340万米ドルの金額シェアを占めました。2022年には、猫はペット数の36%を占め、人口の面でも主要なペットです。猫の飼育数の増加と猫の親たちの健康への関心の高まりは、予測期間中にCAGR 8.6%でこの地域における猫用栄養補助食品の使用を促進すると予測されます。

- その他の動物の飼育が増加し、その健康に対する懸念が高まっています。その他の動物は、2022年に1億8,610万米ドルの金額シェアを占めました。

- プレミアム化の進展とペットの健康懸念の高まりが、予測期間中CAGR 7.7%で欧州のペット用栄養補助食品市場を牽引すると予測されます。

英国は、ペットフードの高度に確立された流通網を通じて、欧州市場を独占しています。

- 2022年のペット数は1億970万人で、欧州は世界のペット用栄養補助食品市場で大きな存在感を示しています。ペット用栄養補助食品は、同年の欧州のペットフード市場の約3.0%を占めています。同地域のペットオーナーは、ペットの人間化の進展に牽引され、ペットの健康と福祉への関心の高まりを示し続けています。このような飼い主の意識の変化が、ペット用栄養補助食品の需要を刺激しています。

- 欧州諸国の中では、英国が最大のシェアを占めており、欧州のペット用栄養補助食品市場の約14.7%を占め、2022年には約2億1,440万米ドルと評価されました。英国が占めるこの大きな市場シェアは、ペットの飼い主がペットに最適な栄養を与えることの重要性をますます認識するようになったことが主な原因です。飼い主は、ペットのサプリメントがペットの健康維持に重要な役割を果たすことを認識しています。米国のペットフード購入者の3分の1以上は、サプリメントがペットに機能的なメリットをもたらす最も効率的な手段であることに同意しています。

- ドイツとフランスがこの地域のペット用栄養補助食品の第2位と第3位の市場として続き、2022年の市場規模はそれぞれ1億8,410万米ドルと1億6,000万米ドルです。これらの国の市場シェアが大きいのは、ペット飼育の動向とそれに伴うペット支出の増加が原因です。

- この地域のペットオーナーがペット用栄養補助食品の利点を認識し続け、ペットの健康と福祉をより重視していることから、欧州のペット用栄養補助食品市場は予測期間中にCAGR 7.7%を記録すると予想されます。

欧州のペット用栄養補助食品市場の動向

猫は狭い空間への適応性が高く、幸運の象徴と考えられているため、欧州で飼われている主要なコンパニオンペットである

- 欧州では、猫はペットを飼う親が採用する主要なペットであり、2022年のペット総人口の36.4%を占めています。猫の飼育率が高いのは、主に狭い居住空間への適応性が高いためで、閉塞感を感じることなく室内で飼うことができます。また、英国、ドイツ、ロシアなど一部の欧州諸国では、猫は幸運や幸運の象徴と考えられています。

- ペットを飼うことで、仲間意識、愛情、保護意識が生まれ、飼い主とペットの間に独特の絆が生まれます。2021年、欧州連合(EU)では9,000万世帯がペットを飼っており、これは全世帯数の46%を占めています。また、欧州の猫の飼育数は年々着実に増加しており、2017年から2022年にかけて14.9%増加しています。COVID-19パンデミック後のペットとしての猫の採用率の上昇は、主に孤独や遠隔地での仕事に刺激されたペットの人間化の増加に起因しています。2020年から2022年にかけて、猫の飼育数は7.1%増加しました。

- 欧州ではロシアが猫の飼育数が多く、地域全体の19.6%を占め、次いでドイツ(14.8%)、フランス(13.2%)、英国(11.1%)となっています。ロシアには猫に対する文化的な親近感があり、多くのロシア文学作品に猫が重要なキャラクターとして登場します。ロシアの民間伝承では、猫は幸運の印とされています。ヨーロピアン・ショートヘア、シャルトリュー、ロシアンブルー、シベリアンは、ロシアや欧州全般で飼われている主要な猫種のひとつです。ペット同伴旅行の調和されたルールの採用、猫製品のオンライン販売の増加、比較的低メンテナンス、都市生活などは、猫の飼育数を促進し、同地域の市場成長を後押しすると予想される主な要因の一部です。

プレミアムペットフードの消費の増加と、健康的で栄養価の高いペットフードの利点に関する意識の高まりが、同地域でのペット支出を増加させています。

- 欧州のペット支出は調査期間中に増加したが、これはさまざまな種類のフードへの支出が増加したことと、ペットの親がペットの健康ニーズにより関心を持つようになり、プレミアム化の傾向が強まったためです。これらの要因は、2017年から2022年の間に1匹当たりのペット支出を37.1%増加させるのに役立ちました。2022年には、犬が最大のシェアを占め、37.8%を占めました。犬は専用のペットフードを与えられ、猫よりもペットフードの消費量が多いからです。例えば英国では、2022年の人々の平均ペットフード費は330米ドルで、猫の食費150米ドルを上回りました。犬には、グルーミングや他の犬との社会化のためのトレーニングといったサービスも提供されています。

- ペットの親は、猫や犬などのペットに高級品を与えます。ペットの親は、ペットの人間化の進展と可処分所得の増加により、Royal Canin、Purina、Whiskasといったブランドのフードを好んで与えます。また、中価格帯のペットフードの栄養状態が改善されたため、中価格帯のペットフードの購入も増加しています。

- COVID-19の大流行時には、スーパーマーケットの大半が営業停止で商品数を減らしたため、オンラインチャネルでのペットフードの販売が増加しました。また、eコマースサイトは商品数が多いです。パンデミック以降、年間5億7,900万人以上のアクセスがあり、アマゾンは英国におけるペットフード販売のリーダー的存在となりました。プレミアム・ペットフードの消費量の増加と、健康的で栄養価の高いペットフードの利点に関する意識の高まりが、この地域のペット支出増に貢献しました。

欧州のペット用栄養補助食品産業の概要

欧州のペット用栄養補助食品市場は断片化されており、上位5社で38.27%を占めています。この市場の主要企業は以下の通りです。 ADM, Mars Incorporated, Nestle(Purina), Vetoquinol and Virbac.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- ペット数

- 猫

- 犬

- その他のペット

- ペット支出

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- サブプロダクト

- ミルクバイオアクティブ

- オメガ3脂肪酸

- プロバイオティクス

- タンパク質とペプチド

- ビタミンとミネラル

- その他の栄養補助食品

- ペット

- 猫

- 犬

- その他のペット

- 流通チャネル

- コンビニエンスストア

- オンライン・チャネル

- 専門店

- スーパーマーケット/ハイパーマーケット

- その他のチャネル

- 国名

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ロシア

- スペイン

- 英国

- その他の欧州

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- ADM

- Alltech

- Clearlake Capital Group, L.P.(Wellness Pet Company Inc.)

- Dechra Pharmaceuticals PLC

- Mars Incorporated

- Nestle(Purina)

- Nutramax Laboratories Inc.

- Vafo Praha, s.r.o.

- Vetoquinol

- Virbac

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 48361

The Europe Pet Nutraceuticals Market size is estimated at 1.8 billion USD in 2025, and is expected to reach 2.6 billion USD by 2030, growing at a CAGR of 7.63% during the forecast period (2025-2030).

Dogs and cats are the largest consumers of pet nutraceuticals in the region due to the increased focus of pet owners on pet health

- Pet nutraceuticals are designed to provide nutritional and therapeutic benefits to pets. Pet nutraceuticals are derived from food sources that provide health benefits beyond basic nutrition. These products are available in various forms, such as supplements, treats, chews, powders, and liquids. In Europe, pet nutraceuticals accounted for 3% of the pet food market in 2022. The smaller share was because of their higher cost and lack of awareness concerning the usage and handling of nutraceuticals.

- Dogs held the major share of the European pet nutraceuticals market, valued at USD 744.9 million in 2022. The larger share of dogs in the pet nutraceuticals market was associated with their considerably higher population in 2022, which was 30% of the pet population in Europe. The pet nutraceuticals market for dogs grew by 14.2% between 2017 and 2021 because of the increase in dog population and the receptiveness of dog owners toward new pet products.

- Cats also have a majority share of the pet nutraceuticals market in the region; they accounted for a value share of USD 523.4 million in 2022. Cats were also the major pets in terms of population, accounting for 36% of the pet population in 2022. The growing adoption of cats and rising health concerns among cat parents are estimated to drive the usage of nutraceuticals for cats in the region at a CAGR of 8.6% during the forecast period.

- The adoption of other animals and the concerns about their health are increasing. Other animals accounted for a value share of USD 186.1 million in 2022.

- The increasing premiumization and rising pet health concerns are anticipated to drive the pet nutraceuticals market in Europe at a CAGR of 7.7% during the forecast period.

The United Kingdom dominated the European market with through its highly established distribution network for pet food

- Europe represents a significant presence in the global pet nutraceutical market, with a pet population of 109.7 million in 2022. Pet nutraceuticals constituted around 3.0% of the European pet food market in the same year. The pet owners in the region continue to demonstrate a growing focus on pet health and well-being, driven by increased pet humanization. This evolving mindset among pet owners is stimulating demand for pet nutraceutical products.

- Among European countries, the United Kingdom occupies the largest share, accounting for about 14.7% of the European pet nutraceuticals market, which was valued at about USD 214.4 million in 2022. This larger market share held by the United Kingdom is mainly attributed to the fact that pet owners are becoming increasingly aware of the importance of providing optimal nutrition to their pets. They recognize that pet supplements play a crucial role in maintaining their pet's health. More than a third of pet food buyers in the United States agree that supplements are the most efficient means of delivering functional benefits to pets.

- Germany and France followed as the region's second- and third-largest markets for pet nutraceuticals, with market values of USD 184.1 million and USD 160.0 million, respectively, in 2022. The substantial market shares of these countries can be attributed to the increasing trend of pet ownership and the corresponding rise in pet expenditure.

- As pet owners throughout the region continue to recognize the advantages of pet nutraceuticals and place a stronger emphasis on their pets' health and well-being, the European pet nutraceuticals market is anticipated to register a CAGR of 7.7% during the forecast period.

Europe Pet Nutraceuticals Market Trends

Cats are the major companion pets adopted in Europe due to their adaptability to small spaces and because they are considered a symbol of good luck

- In Europe, cats are the major pets adopted by pet parents; they accounted for 36.4% of the total pet population in 2022. The high adoption of cats is mainly due to their adaptability to smaller living spaces; they can be kept indoors without feeling cooped up. Also, in some European countries, including the United Kingdom, Germany, and Russia, cats are considered to be symbols of good luck or fortune.

- Owning pets creates a sense of companionship, affection, and protection, developing unique bonds between the owners and their pets. In 2021, 90 million households in the European Union had pets, which represented 46% of the total number of households. Also, the European cat population has been steadily increasing over the years, increasing by 14.9% from 2017 to 2022. The higher adoption of cats as pets after the COVID-19 pandemic is mainly attributed to the increase in pet humanization stimulated by loneliness and remote work. From 2020 to 2022, the cat population increased by 7.1%.

- In Europe, Russia consists of a large cat population, which accounted for 19.6% of the total population in the region, followed by Germany (14.8%), France (13.2%), and the United Kingdom (11.1%). There is a cultural affinity for cats in Russia, with many Russian literary works featuring cats as important characters. Cats are considered as a sign of good luck in Russian folklore. European shorthair, Chartreux, Russian Blue, and Siberian are among the major cat breeds adopted in Russia and Europe in general. The adoption of harmonized rules for traveling with pets, growing online sales of cat products, relatively lower maintenance, and urban living are some of the major factors expected to drive the cat population, boosting the market's growth in the region.

Higher consumption of premium pet food and growing awareness about the benefits of healthy, nutritious pet food are increasing pet expenditure in the region

- Pet expenditure in Europe increased during the study period because of increased spending on different types of food and the growing trend of premiumization, with pet parents becoming more concerned about the health needs of their pets. These factors helped in increasing the pet expenditure per animal by 37.1% between 2017 and 2022. In 2022, dogs held the largest share, accounting for 37.8%, as dogs are fed specialized pet food and have a higher consumption of pet food than cats. For instance, in the United Kingdom, people's average pet food expense was USD 330 in 2022, which was more than a cat's food expense of USD 150. Dogs are also provided with services such as pet grooming and training for socialization with other dogs.

- Pet parents provide premium products to their pets, such as cats and dogs. Pet parents prefer to feed their pets food from brands such as Royal Canin, Purina, and Whiskas because of the growing pet humanization and an increase in disposable income. There is also a rise in purchases from the medium-priced segment of pet food due to improvements in the pet food nutrition offered by these medium-priced products.

- During the COVID-19 pandemic, there was an increase in the sales of pet food through online channels, as the majority of supermarkets had fewer product offerings due to the lockdowns. Also, e-commerce websites have a higher number of products available. It helped Amazon to be a leader in pet food sales in the United Kingdom, with the website receiving more than 579 million visits annually since the pandemic. The higher consumption of premium pet food and growing awareness about the benefits of healthy, nutritious pet food helped increase pet expenditure in the region.

Europe Pet Nutraceuticals Industry Overview

The Europe Pet Nutraceuticals Market is fragmented, with the top five companies occupying 38.27%. The major players in this market are ADM, Mars Incorporated, Nestle (Purina), Vetoquinol and Virbac (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Sub Product

- 5.1.1 Milk Bioactives

- 5.1.2 Omega-3 Fatty Acids

- 5.1.3 Probiotics

- 5.1.4 Proteins and Peptides

- 5.1.5 Vitamins and Minerals

- 5.1.6 Other Nutraceuticals

- 5.2 Pets

- 5.2.1 Cats

- 5.2.2 Dogs

- 5.2.3 Other Pets

- 5.3 Distribution Channel

- 5.3.1 Convenience Stores

- 5.3.2 Online Channel

- 5.3.3 Specialty Stores

- 5.3.4 Supermarkets/Hypermarkets

- 5.3.5 Other Channels

- 5.4 Country

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Italy

- 5.4.4 Netherlands

- 5.4.5 Poland

- 5.4.6 Russia

- 5.4.7 Spain

- 5.4.8 United Kingdom

- 5.4.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 ADM

- 6.4.2 Alltech

- 6.4.3 Clearlake Capital Group, L.P. (Wellness Pet Company Inc.)

- 6.4.4 Dechra Pharmaceuticals PLC

- 6.4.5 Mars Incorporated

- 6.4.6 Nestle (Purina)

- 6.4.7 Nutramax Laboratories Inc.

- 6.4.8 Vafo Praha, s.r.o.

- 6.4.9 Vetoquinol

- 6.4.10 Virbac

7 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms