|

市場調査レポート

商品コード

1685846

アジア太平洋地域のRTD茶:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia-Pacific Ready to Drink Tea - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のRTD茶:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 252 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

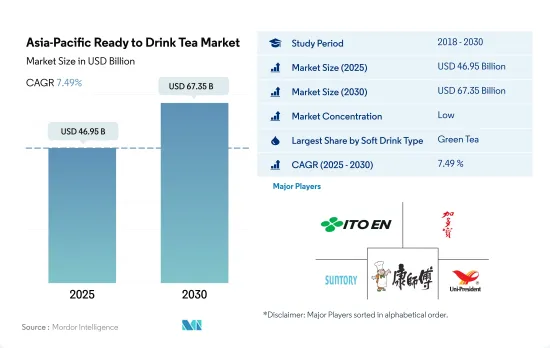

アジア太平洋地域のRTD茶市場規模は2025年に469億5,000万米ドルと推定され、2030年には673億5,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは7.49%で成長する見込みです。

消費者の健康志向の高まりが市場の成長を支える

- 人口の多さと中間層の拡大に牽引され、アジア太平洋地域はレディ・トゥ・ドリンク(RTD)茶の急成長の最前線にあります。この地域では、緑茶、ハーブティー、ウーロン茶といった伝統的な茶葉を好む文化が根付いているため、RTD茶の需要が高まっています。これらの製品の魅力は、その手軽さと持ち運び可能な性質によってさらに高められ、忙しい消費者の間でヒット商品となっています。抽出や後片付けの手間を省くことで、RTDティーは手間のかからない、すぐに飲める選択肢を提供しています。特筆すべきは、アジア太平洋地域におけるRTDティーの販売額が2023年には2021年比で13.2%増と顕著に増加したことです。

- RTD茶の中でも緑茶が市場を独占しており、2020年から2023年にかけての金額成長率は21%という驚異的な数字を記録しました。健康とウェルネスに対する意識の高まりが、RTD緑茶の台頭の主な原動力となっています。RTD緑茶は無糖または低糖であるため、消費者はその健康上の利点や砂糖入り清涼飲料水の代替品としての魅力に惹かれ、RTD緑茶を好むようになっています。さらに、多様なフレーバーが入手可能なため、味の嗜好も多様化しています。アジア太平洋地域市場では、消費者はRTD緑茶の爽やかさと水分補給の品質も高く評価しています。

- 成長のフロントランナーとして台頭してきたハーブRTDティーは、2024~2030年のCAGRが金額ベースで7.84%になる見通しです。この変化は、特に自然な製品を求める人々の間で、手軽で便利な選択肢として支持を集めています。さらに、ハーブティーは、抗がん、抗糖尿病、抗炎症、抗酸化作用など、その潜在的な健康効果が長い間伝統医学で称賛されてきました。

ハーブティーを使ったフレーバーのイノベーションとRTDティーのオンライン販売の増加が成長を促進すると予想されます。

- アジア太平洋地域のレディ・トゥ・ドリンク(RTD)茶市場は、2024年から2030年にかけて7.44%の堅調なCAGRで推移すると予測されます。特筆すべきは、豊かな茶の伝統を背景に中国がこの地域のRTD茶を支配していることです。2023年、中国のRTD茶は同地域の茶消費量全体の41.06%を占めました。中国は活気ある市場を誇っており、伝統的な加糖茶やジャスミン茶からハーブブレンドや革新的なフレーバーまで、多様なRTD茶を提供する地域ブランドや国際ブランドが数多く存在します。今後、中国では健康志向が減糖RTDティーの需要を促進すると予想されます。

- 茶文化が深く根付いている日本は、RTD緑茶への強い親近感を目の当たりにしています。伊藤園やキリンビバレッジのような主要企業は、伝統的な味を維持しながらパッケージと利便性を高めることを重視しています。日本市場では2022年に700種類もの茶系飲料が流通し、毎年100種類以上が新たに導入されています。日本では、緑茶、紅茶、ハーブティー、ウーロン茶など、RTD茶の定番商品は多岐にわたるが、限定商品は動向や季節のフレーバーからヒントを得ることが多いです。

- 2024~2030年のRTD紅茶市場のCAGRは10.50%と予測され、インドが成長チャートをリードします。手軽さと伝統的な風味で知られるRTD茶飲料は、大きな人気を集めています。健康とウェルネスが注目される中、インドの消費者はハーブティー、抗酸化物質、天然成分など、健康に良いとされる成分を含むRTDティーに引き寄せられつつあります。eコマース・プラットフォームの台頭はRTD茶へのアクセスをさらに強化し、消費者はこれらの飲料をオンラインで便利に購入できるようになりました。

アジア太平洋地域のRTD茶市場の動向

RTD茶飲料の利便性が同分野の売上を押し上げる

- 人々は甘い飲料の代わりとして、あるいは食間に、より健康的なRTD茶を摂取する傾向があります。インド、中国、シンガポールなどの新興国がRTD茶の主要市場です。

- 砂糖の大量摂取に関連する健康懸念の高まりが、RTD茶を含むより健康的なRTD飲料の需要を押し上げています。このような消費者の減糖志向の高まりを受けて、メーカーは無糖や減糖の代替品を発売しています。

- アジア市場では、価格競争力が鍵となります。小規模または新しいRTD紅茶ブランドの場合、消費者は新しいブランドを試すために余分な出費をすることを厭わないです。そのため、メーカーは入手可能なブランドと同等の価格を提示しています。

- この地域でよく飲まれている緑茶は、抗炎症作用や心臓の健康に役立つ可能性があることで知られています。同様に、カモミール・ティー、ハイビスカス・ティー、ジャスミン・ティーなどの他の種類は、しばしば鎮静効果に関連しており、消化をサポートする可能性があります。

アジア太平洋地域のRTD茶産業の概要

アジア太平洋地域のRTD茶市場は細分化されており、上位5社で36.85%を占めています。この市場の主要企業は以下の通りです。Ito En, Ltd., JDB Group, Suntory Holdings Limited, Tingyi(Cayman Islands)Holding Corporation and Uni-President Enterprises Corp.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- ソフトドリンクタイプ

- 緑茶

- ハーブティー

- アイスティー

- その他RTD茶

- 包装タイプ

- アセプティックパッケージ

- ガラス瓶

- 金属缶

- ペットボトル

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- スーパーマーケット/ハイパーマーケット

- その他

- オントレード

- オフトレード

- 国別

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- タイ

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Asahi Group Holdings, Ltd.

- Ichitan Group PCL

- Ito En, Ltd.

- JDB Group

- Kirin Holdings Company, Limited

- Nestle S.A.

- Nongfu Spring Co., Ltd.

- PT. Anggada Putra Rekso Mulia

- Sapporo Holdings Limited

- Suntory Holdings Limited

- Tata Consumer Products Ltd

- Thai Beverages PCL

- The Coca-Cola Company

- Tingyi(Cayman Islands)Holding Corporation

- Uni-President Enterprises Corp.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Asia-Pacific Ready to Drink Tea Market size is estimated at 46.95 billion USD in 2025, and is expected to reach 67.35 billion USD by 2030, growing at a CAGR of 7.49% during the forecast period (2025-2030).

Growing health and wellness trends among consumers are supporting the market's growth

- Driven by its sizable population and expanding middle class, the Asia-Pacific region is at the forefront of the ready-to-drink (RTD) tea surge. The region's deep-rooted cultural affinity for traditional tea variants, such as green tea, herbal tea, and oolong tea, is fueling the demand for RTD tea. The appeal of these products is further enhanced by their convenience and on-the-go nature, making them a hit among busy consumers. By eliminating the need for brewing and cleanup, RTD teas offer a hassle-free, ready-to-consume option. Notably, the sales value of RTD tea in the Asia-Pacific region saw a notable uptick of 13.2% in 2023 compared to 2021.

- Among the RTD tea variants, green tea dominates the market, accounting for an impressive 21% growth rate by value from 2020 to 2023. The surge in health and wellness consciousness has been a key driver behind the ascent of RTD green tea. Consumers are gravitating toward it, drawn by its perceived health benefits and its appeal as a healthier alternative to sugary soft drinks, given its unsweetened or low-sugar nature. Additionally, the availability of diverse flavors caters to varying taste preferences. In the Asia-Pacific market, consumers also appreciate RTD green tea for its refreshing and hydrating qualities.

- Emerging as the frontrunner in growth, herbal RTD tea is poised to witness a CAGR of 7.84% by value during 2024-2030. This variant is gaining traction as a quick and convenient choice, particularly among those seeking natural products. Furthermore, herbal teas have long been lauded in traditional medicine for their potential health benefits, including anti-cancer, anti-diabetic, anti-inflammatory, and antioxidant properties.

Rise in innovations in flavors with herbal infusions and online presence of RTD tea is anticipated to drive growth

- The Asia-Pacific ready-to-drink (RTD) tea market is projected to witness a robust CAGR of 7.44% from 2024 to 2030. Notably, China dominates the region's RTD tea landscape, driven by its rich tea heritage. In 2023, RTD tea in China accounted for a significant 41.06% of the region's overall tea consumption. China boasts a vibrant market, with a plethora of regional and international brands offering a diverse array of RTD teas, ranging from traditional sweetened and jasmine teas to herbal blends and innovative flavors. Looking ahead, health-consciousness is expected to fuel the demand for reduced-sugar RTD teas in China.

- Japan, a nation with a deep-rooted tea culture, is witnessing a strong affinity for RTD green teas. Key players like Ito En Ltd and Kirin Beverage Company Limited emphasize maintaining the traditional taste while enhancing packaging and convenience. The Japanese market saw a staggering 700 tea drink variants in circulation in 2022, with over 100 new introductions each year. The perennial RTD tea offerings in Japan span green, black, herbal, and oolong teas, while limited editions often draw inspiration from trending or seasonal flavors.

- India is set to lead the growth charts, projecting a robust CAGR of 10.50% in the value of its RTD tea market during the period 2024-2030. RTD tea beverages, known for their convenience and traditional flavors, have gained significant popularity. As health and wellness take center stage, consumers in India are gravitating toward RTD teas with perceived health benefits, such as herbal infusions, antioxidants, and natural ingredients. The rise of e-commerce platforms has further bolstered the accessibility of RTD teas, enabling consumers to purchase these beverages online conveniently.

Asia-Pacific Ready to Drink Tea Market Trends

The convenience associated with RTD tea beverages boosts the segment sales

- People tend to consume RTD tea as a healthier alternative to sugary drinks or between meals. Emerging countries like India, China, and Singapore among others are a few of the major markets for RTD tea.

- Rising health concerns related to high sugar intake have boosted the demand for healthier RTD drinks including RTD tea. In response to this evolving consumer preference for sugar reduction, manufacturers have been introducing sugar-free and reduced-sugar alternatives.

- In the Asian market, price competitiveness is the key. In the case of smaller or newer RTD tea brands, consumers are not willing to spend extra to try the new brand. Thereby, manufacturers are citing a price at par with available brands.

- Green tea, commonly consumed in the region is known for potential anti-inflammatory and heart health benefits. Likewise, other variants like chamomile tea, hibiscus tea, jasmine tea, and others are often associated with calming effects and may support digestion.

Asia-Pacific Ready to Drink Tea Industry Overview

The Asia-Pacific Ready to Drink Tea Market is fragmented, with the top five companies occupying 36.85%. The major players in this market are Ito En, Ltd., JDB Group, Suntory Holdings Limited, Tingyi (Cayman Islands) Holding Corporation and Uni-President Enterprises Corp. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Soft Drink Type

- 5.1.1 Green Tea

- 5.1.2 Herbal Tea

- 5.1.3 Iced Tea

- 5.1.4 Other RTD Tea

- 5.2 Packaging Type

- 5.2.1 Aseptic packages

- 5.2.2 Glass Bottles

- 5.2.3 Metal Can

- 5.2.4 PET Bottles

- 5.3 Distribution Channel

- 5.3.1 Off-trade

- 5.3.1.1 Convenience Stores

- 5.3.1.2 Online Retail

- 5.3.1.3 Supermarket/Hypermarket

- 5.3.1.4 Others

- 5.3.2 On-trade

- 5.3.1 Off-trade

- 5.4 Country

- 5.4.1 Australia

- 5.4.2 China

- 5.4.3 India

- 5.4.4 Indonesia

- 5.4.5 Japan

- 5.4.6 Malaysia

- 5.4.7 South Korea

- 5.4.8 Thailand

- 5.4.9 Vietnam

- 5.4.10 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Asahi Group Holdings, Ltd.

- 6.4.2 Ichitan Group PCL

- 6.4.3 Ito En, Ltd.

- 6.4.4 JDB Group

- 6.4.5 Kirin Holdings Company, Limited

- 6.4.6 Nestle S.A.

- 6.4.7 Nongfu Spring Co., Ltd.

- 6.4.8 PT. Anggada Putra Rekso Mulia

- 6.4.9 Sapporo Holdings Limited

- 6.4.10 Suntory Holdings Limited

- 6.4.11 Tata Consumer Products Ltd

- 6.4.12 Thai Beverages PCL

- 6.4.13 The Coca-Cola Company

- 6.4.14 Tingyi (Cayman Islands) Holding Corporation

- 6.4.15 Uni-President Enterprises Corp.

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms