|

市場調査レポート

商品コード

1683163

アフリカのRTD茶:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Africa Ready to Drink Tea - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカのRTD茶:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 196 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

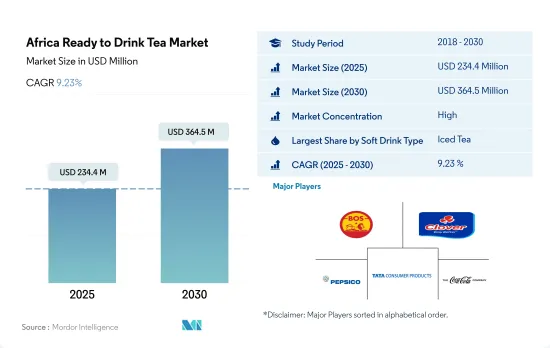

アフリカのRTD茶の市場規模は2025年に2億3,440万米ドルと推定され、2030年には3億6,450万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは9.23%で成長します。

健康志向の高まりとハーブ製品需要の増加がアフリカ全域でRTD茶の売上を促進

- 2021年から2023年にかけて、RTD茶の販売額は15.99%急増しました。この成長は、炭酸飲料よりも健康的な飲料への嗜好の高まりによるものと考えられます。RTD茶の流通も、スーパーマーケット、ハイパーマーケット、食料品店、専門店、コンビニエンスストアなど、さまざまなチャネルで拡大しています。なかでも食料品店は際立っており、消費者の嗜好に合わせて、さまざまなブランドからアイスティーや緑茶など多様なRTDティーの選択肢を提供しています。この動向は市場のさらなる成長を促進すると予想されます。

- 消費者支出の増加は、スーパーマーケットでの購入の利便性と相まって、特に発展途上国のRTD茶メーカーに有望な機会をもたらしています。特筆すべきは、ケニアがアフリカ最大の茶生産国であることです。ケニアには11の茶産地があり、東部大地溝帯の両側の高原地帯に広がっています。特筆すべきは、茶生産の大部分(約3分の2)が小規模農家によるもので、66の工場で加工されていることです。

- 2024年から2030年にかけて、ハーブティーと緑茶のCAGRはそれぞれ9.64%と最も高くなると予測されています。この急成長は、ハーブティーと緑茶の脂肪燃焼効果に対する認識が高まり、健康への関心が高まっていることが背景にあると予想されます。プレミアム・ブランドに対する需要の高まりに対応するため、企業は特に技術に精通した若い消費者をターゲットにしたソーシャル・メディア・キャンペーンを展開しています。こうしたキャンペーンは、価格に見合った価値、パーソナライゼーション、シームレスなデジタル統合を強調しています。特筆すべきは、アフリカ全土でインターネットの普及が拡大していることを反映して、インターネット・ユーザー数が大幅に増加していることです。

糖分を抑えたレディ・トゥ・ドリンク(RTD)茶に対する消費者の嗜好の高まりが、市場の成長を牽引しています。

- アフリカにおけるRTD(レディ・トゥ・ドリンク)茶の販売額は、2023年には2021年比で15.99%の大幅増となりました。この急増は、RTD茶に関連する無数の健康上の利点に対する消費者の意識の高まりによるところが大きいです。これらの利点は、体重管理の補助、身体や頭痛の不快感の緩和から、コレステロール値の低下、さらには心臓発作のリスクの軽減にまで及ぶ。

- 南アフリカはアフリカにおけるレディ・トゥ・ドリンク(RTD)茶の主要市場として際立っています。2023年、南アフリカにおけるRTD茶の販売額は2020年から27.04%増加しました。同国の顕著な動向は、低糖度、天然甘味料、酸化防止剤の添加を強調した健康志向のRTD茶への嗜好の高まりです。The Coca-Cola Company、BOS brands、San Benedetto SpA、Unileverなどの主要業界企業は、この需要に積極的に対応しています。各社はRTD(レディ・トゥ・ドリンク)ティーのラインナップに無糖のオプションを導入し、ショ糖、ステビア、果糖のような天然甘味料を好んで使用しています。

- ナイジェリアはアフリカ諸国の中でRTD茶市場をリードしており、2024年から2030年までの予測値CAGRは14.91%です。ナイジェリアでは都市化の急速な進展と中産階級の拡大が、RTD茶を含む便利な飲食品への需要を押し上げています。市場の成熟に伴い、ナイジェリアの消費者は、機能性成分を配合したものであれ、独自の製法で抽出されたものであれ、革新的なRTD茶への関心を高めていくとみられます。

アフリカのRTD茶市場動向

消費者の健康志向の高まりとフレーバー・プロファイルの革新が市場にプラスの影響

- 東アフリカでは、紅茶、ミルク、スパイスをブレンドしたチャイが人気です。南部アフリカでは、ルイボスとしても知られるレッドブッシュティーが人気のハーブティーです。西アフリカと北アフリカでは、ハイビスカスをベースにしたビサップ(カーケイド)が人気の飲み物です。北アフリカと西アフリカでは、ミント・ティーが人気です。

- 製品属性では、アフリカの消費者は、紅茶、緑茶、ハーブ・ブレンドといった定番の選択肢を含め、さまざまな風味の茶を楽しめるRTD茶を高く評価しています。

- 2022年、ナイジェリアは25.80%のインフレを観測しました。アフリカのインフレはCIP率に悪影響を及ぼし、各国のRTD茶飲料を含む食品のコスト上昇につながっています。しかし、この地域のプレーヤーは、消費者にリーズナブルな価格で製品を提供するために利益率を下げています。

- RTD茶飲料の中では、紅茶飲料が非常に人気があり、消費者に楽しまれています。糖尿病を患っている消費者は、健康上の利点やその他の機能的な利点を求めてこれらの飲料を検討しています。

アフリカのRTD茶産業の概要

アフリカのRTD茶市場はかなり統合されており、上位5社で88.20%を占めています。この市場の主要企業は以下の通りです。 BOS Brands(Pty)Ltd, Clover S.A.(Pty)Ltd, PepsiCo, Inc., Tata Consumer Products Ltd and The Coca-Cola Company(sorted alphabetically).

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- 清涼飲料タイプ別

- 緑茶

- ハーブティー

- アイスティー

- その他のRTD茶

- 包装タイプ別

- アセプティックパッケージ

- ガラス瓶

- 金属缶

- ペットボトル

- 流通チャネル別

- オフトレード

- コンビニエンスストア

- オンライン小売

- スーパーマーケット/ハイパーマーケット

- その他

- オントレード

- オフトレード

- 国別

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- BOS Brands(Pty)Ltd

- Clover S.A.(Pty)Ltd

- CWAY Group

- Dynamic Brands Manufacturing(Pty)Ltd.

- PepsiCo, Inc.

- Tata Consumer Products Ltd

- The Coca-Cola Company

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Africa Ready to Drink Tea Market size is estimated at 234.4 million USD in 2025, and is expected to reach 364.5 million USD by 2030, growing at a CAGR of 9.23% during the forecast period (2025-2030).

Rising health concerns and increasing demand for herbal products propelling RTD tea sales across Africa

- From 2021 to 2023, the value of RTD tea sales surged by 15.99%. This growth can be attributed to a rising preference for healthier beverages over carbonated drinks. The distribution of RTD tea has also expanded across various channels, including supermarkets, hypermarkets, grocery stores, specialist stores, and convenience stores. Among these, grocery stores stand out, offering a diverse range of RTD tea options, such as iced tea and green tea from different brands, catering to consumer preferences. This trend is expected to fuel further market growth.

- The rise in consumer spending, coupled with the convenience of purchasing from supermarkets, presents a promising opportunity for RTD tea manufacturers, especially in developing nations. Notably, Kenya is Africa's largest tea producer owing to its favorable equatorial location, enabling year-round harvesting. The country boasts 11 distinct tea regions, spanning the high plains on both sides of the Eastern Rift Valley. Notably, the majority of tea production, about two-thirds, comes from smallholders and is processed in 66 factories.

- Between 2024 and 2030, both herbal tea and green tea are projected to exhibit the highest CAGRs of 9.64% each. This surge is expected to be driven by the rising awareness of the fat-burning properties of herbal and green teas, aligning with heightened health concerns. To cater to the growing demand for premium brands, companies are crafting targeted social media campaigns, particularly aimed at tech-savvy young consumers. These campaigns emphasize value for money, personalization, and seamless digital integration. Notably, there has been a significant rise in the number of internet users, reflecting the expanding internet penetration across Africa.

The market is witnessing growth, driven by a rising consumer preference for ready-to-drink (RTD) teas with reduced sugar content

- The sales value of RTD (ready-to-drink) tea in Africa experienced a significant increase of 15.99% in 2023, compared to 2021. This surge can be largely attributed to rising consumer awareness of the myriad health benefits linked to RTD tea. These advantages span from aiding weight management and alleviating body and headache discomfort to reducing cholesterol levels and even mitigating the risk of heart attacks.

- South Africa stands out as the leading market for ready-to-drink (RTD) tea in Africa. In 2023, the sales value of RTD tea in South Africa increased by 27.04% from 2020. A discernible trend in the country is the growing preference for health-conscious RTD teas, emphasizing lower sugar levels, natural sweeteners, and added antioxidants. Key industry players, including The Coca-Cola Company, BOS brands, San Benedetto SpA, and Unilever, are actively catering to this demand. Companies are introducing sugar-free options in their ready-to-drink (RTD) tea lineup, favoring natural sweeteners like Sucrose, Stevia, and Fructose.

- Nigeria leads the pack among African nations in the RTD tea market, with a projected value CAGR of 14.91% from 2024 to 2030. The surge in urbanization and the expanding middle class in Nigeria are driving the demand for convenient food and beverages, including RTD teas. As the market matures, Nigerian consumers are expected to display a growing interest in innovative RTD tea offerings, whether infused with functional ingredients or brewed using unique methods.

Africa Ready to Drink Tea Market Trends

Growing healthconsiousness among consumers and innovations in flavor profile is impacting the market positively

- In East Africa, Chai is a popular blend of black tea, milk, and spices. In Southern Africa, Red Bush tea, also known as Rooibos, is a popular herbal tea. In West and North Africa, Bisap, or Kirkade, a hibiscus-based tea, is a popular beverage. In North and West Africa, Mint tea is a popular choice.

- Under the product attributes, African consumers appreciate RTD tea because it provides them with the variety of tea flavors, including classic choices such as black, green, and herbal blends.

- In 2022, Nigeria has observed an inflation of 25.80%. Inflation in Africa has had a detrimental impact on the CIP rate, leading to an increase in the cost of food products, including RTD tea beverages, in various nations. However, players in the region are cutting their profit margins to avail products at a reasonable price to the consumers.

- Under RTD tea beverages, black tea beverages are highly popularized and enjoyed by consumers. Induvial dealing with diabetes are consideration these beverages for its health benefits and other functional benefits.

Africa Ready to Drink Tea Industry Overview

The Africa Ready to Drink Tea Market is fairly consolidated, with the top five companies occupying 88.20%. The major players in this market are BOS Brands (Pty) Ltd, Clover S.A. (Pty) Ltd, PepsiCo, Inc., Tata Consumer Products Ltd and The Coca-Cola Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Soft Drink Type

- 5.1.1 Green Tea

- 5.1.2 Herbal Tea

- 5.1.3 Iced Tea

- 5.1.4 Other RTD Tea

- 5.2 Packaging Type

- 5.2.1 Aseptic packages

- 5.2.2 Glass Bottles

- 5.2.3 Metal Can

- 5.2.4 PET Bottles

- 5.3 Distribution Channel

- 5.3.1 Off-trade

- 5.3.1.1 Convenience Stores

- 5.3.1.2 Online Retail

- 5.3.1.3 Supermarket/Hypermarket

- 5.3.1.4 Others

- 5.3.2 On-trade

- 5.3.1 Off-trade

- 5.4 Country

- 5.4.1 Egypt

- 5.4.2 Nigeria

- 5.4.3 South Africa

- 5.4.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 BOS Brands (Pty) Ltd

- 6.4.2 Clover S.A. (Pty) Ltd

- 6.4.3 CWAY Group

- 6.4.4 Dynamic Brands Manufacturing (Pty) Ltd.

- 6.4.5 PepsiCo, Inc.

- 6.4.6 Tata Consumer Products Ltd

- 6.4.7 The Coca-Cola Company

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms