|

市場調査レポート

商品コード

1684098

米国のRTD茶:市場シェア分析、産業動向、成長予測(2025年~2030年)US Ready to Drink Tea - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のRTD茶:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 199 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

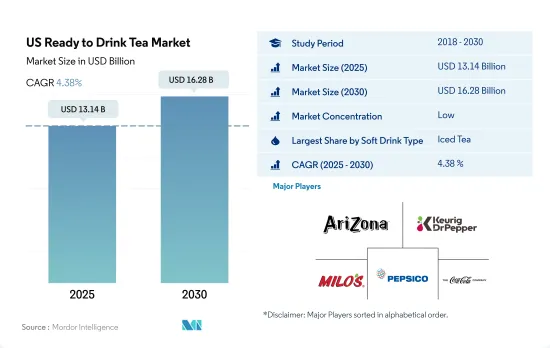

米国のRTD茶市場規模は、2025年に131億4,000万米ドルと推定され、2030年には162億8,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは4.38%で成長する見込みです。

RTD緑茶はその抗酸化特性と潜在的な健康効果により人気を集める

- アイスティー分野が市場を独占しています。2020年から2023年にかけて金額ベースで9.71%の大幅な成長率を記録しました。この急増は、健康とウェルネスの動向の影響によるものと考えられます。消費者は、すぐに飲める(RTD)アイスティーを、糖分の多い清涼飲料水に代わる健康的なものと認識し、ますます好んでいます。2022年現在、米国で消費される紅茶の約75~80%はアイスティーであり、その人気を反映しています。アイスティーの魅力は多様なフレーバーにあり、伝統的な紅茶がトップチョイスです。

- RTD緑茶はRTD紅茶分野で第2位の市場シェアを確保し、2020年から2023年までのCAGRは金額ベースで5.06%と顕著な伸びを示します。緑茶には抗酸化物質が豊富に含まれ、潜在的な健康効果があることから、健康志向の消費者に好まれる選択肢となっています。2021年、アメリカ人は驚異的な850億食分のお茶を消費し、緑茶はその約15%を占めました。この分野で注目すべきブランドには、リプトン、ピュアリーフ、アリゾナなどがあります。

- その他のRTD茶分野は市場で最も急成長しており、2024~2030年のCAGRは金額ベースで6.19%と予測されています。この分野には、紅茶、機能性茶、スパークリングティーなど、さまざまな茶が含まれます。メーカーは成分レベルのイノベーションに注力しており、消費者を魅了する新しいフレーバーや組み合わせを導入しています。抗酸化作用で知られるフラボノイド系飲料の人気の高まりが、この市場をさらに牽引すると予想されます。注目すべきは、2021年に米国で消費される紅茶の84%を紅茶が占めていることです。

米国のRTD茶市場動向

RTD茶飲料の利便性が同分野の売上を押し上げる

- パッケージ化されたRTD紅茶の利便性と、カフェ、小売店、食品販売店の増加も、同国における紅茶消費の増加に寄与しています。さらに、プライベートブランドも農村部で強い存在感を示しているため、市場で重要な役割を果たしています。

- 国内では持続可能なパッケージングに対する需要が高く、各ブランドはパッケージングタイプを改良しています。例えば、ペプシコは2030年までに、再利用可能なモデルで配送される飲料の割合を現在の10%から20%に倍増させる計画です。

- 可処分所得の増加もRTD紅茶の売上を牽引しています。外出先でのRTD紅茶の消費量は、家庭での消費量よりも高いことが記録されています。

- 減量を促進し、体や頭痛の不快感を軽減し、コレステロール値を下げ、心臓発作のリスクを下げるといったRTD茶の健康上の利点が、フィットネス愛好家や病気に苦しむ人々の需要を牽引しています。

米国のRTD茶産業の概要

米国のRTD茶市場は細分化されており、上位5社で38.08%を占めています。この市場の主要企業は以下の通りです。 Arizona Beverages USA LLC, Keurig Dr Pepper, Inc., Milo's Tea Company, Inc., PepsiCo, Inc. and The Coca-Cola Company.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- 清涼飲料タイプ

- 緑茶

- ハーブティー

- アイスティー

- その他のRTD茶

- 包装タイプ

- アセプティックパッケージ

- ガラス瓶

- 金属缶

- ペットボトル

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- スーパーマーケット/ハイパーマーケット

- その他

- オン・トレード

- オフトレード

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Arizona Beverages USA LLC

- Del Monte Foods, Inc.

- Hawaiian Sun Products, Inc.

- Ito En, Ltd.

- Keurig Dr Pepper, Inc.

- Milo's Tea Company, Inc.

- Nestle S.A.

- PepsiCo, Inc.

- Red Diamond, Inc.

- Reily Foods Company

- The Coca-Cola Company

- Walmart, Inc.

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The US Ready to Drink Tea Market size is estimated at 13.14 billion USD in 2025, and is expected to reach 16.28 billion USD by 2030, growing at a CAGR of 4.38% during the forecast period (2025-2030).

RTD green tea gains traction due to its antioxidant properties and potential health benefits

- The iced tea segment dominates the market. It witnessed a significant growth rate of 9.71% by value from 2020 to 2023. This surge can be attributed to the influence of health and wellness trends. Consumers are increasingly favoring ready-to-drink (RTD) iced tea, perceiving it as a healthier alternative to sugary soft drinks. As of 2022, around 75% to 80% of tea consumed in the United States is iced, reflecting its popularity. Iced tea's appeal lies in its diverse flavor offerings, with traditional black tea being a top choice.

- RTD green tea secures the second-largest market share in the RTD tea sector, registering a notable CAGR of 5.06% by value from 2020 to 2023. The antioxidant-rich composition and potential health benefits of green tea have made it a preferred option for health-conscious consumers. In 2021, Americans consumed a staggering 85 billion servings of tea, with green tea accounting for approximately 15% of the total. Notable brands in this space include Lipton, Pure Leaf, and Arizona.

- The other RTD tea segment is the fastest-growing in the market and is projected to register a CAGR of 6.19% by value during 2024-2030. This segment encompasses a variety of teas, such as black tea, functional tea, and sparkling tea. Manufacturers are focusing on ingredient-level innovations, introducing new flavors and combinations to entice consumers. The rising popularity of flavonoid-based beverages, known for their antioxidant properties, is expected to drive this market further. Notably, black tea accounted for 84% of all tea consumed in the United States in 2021.

US Ready to Drink Tea Market Trends

The convenience associated with RTD tea beverages boosts the segment sales

- The convenience of packaged RTD tea and the growing number of cafes, retail stores, and food outlets have also contributed to the increase in consumption of tea in the country. Further, private label brands also play an important role in the market, as they have a strong presence in rural areas.

- People are looking for sustainable packaging with the high demand for sustainable packaging in the country, brands are improving packaging types like PepsiCo plans to double the percentage of all beverage servings it sells delivered through reusable models from a current 10% to 20% by 2030.

- The increasing disposable income is also a driving factor in the sales of RTD tea. It has been recorded that the consumption of RTD tea away from home is higher than at home consumption.

- The health benefits of RTD tea such as promoting weight loss, lessening body and headache discomfort, lowering cholesterol levels, and lowering the risk of heart attacks are driving the demand among fitness enthusiasts and people suffering from the diseases.

US Ready to Drink Tea Industry Overview

The US Ready to Drink Tea Market is fragmented, with the top five companies occupying 38.08%. The major players in this market are Arizona Beverages USA LLC, Keurig Dr Pepper, Inc., Milo's Tea Company, Inc., PepsiCo, Inc. and The Coca-Cola Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Soft Drink Type

- 5.1.1 Green Tea

- 5.1.2 Herbal Tea

- 5.1.3 Iced Tea

- 5.1.4 Other RTD Tea

- 5.2 Packaging Type

- 5.2.1 Aseptic packages

- 5.2.2 Glass Bottles

- 5.2.3 Metal Can

- 5.2.4 PET Bottles

- 5.3 Distribution Channel

- 5.3.1 Off-trade

- 5.3.1.1 Convenience Stores

- 5.3.1.2 Online Retail

- 5.3.1.3 Supermarket/Hypermarket

- 5.3.1.4 Others

- 5.3.2 On-trade

- 5.3.1 Off-trade

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Arizona Beverages USA LLC

- 6.4.2 Del Monte Foods, Inc.

- 6.4.3 Hawaiian Sun Products, Inc.

- 6.4.4 Ito En, Ltd.

- 6.4.5 Keurig Dr Pepper, Inc.

- 6.4.6 Milo's Tea Company, Inc.

- 6.4.7 Nestle S.A.

- 6.4.8 PepsiCo, Inc.

- 6.4.9 Red Diamond, Inc.

- 6.4.10 Reily Foods Company

- 6.4.11 The Coca-Cola Company

- 6.4.12 Walmart, Inc.

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms