|

市場調査レポート

商品コード

1685835

南米のエンジニアリングプラスチック:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)South America Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米のエンジニアリングプラスチック:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 287 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

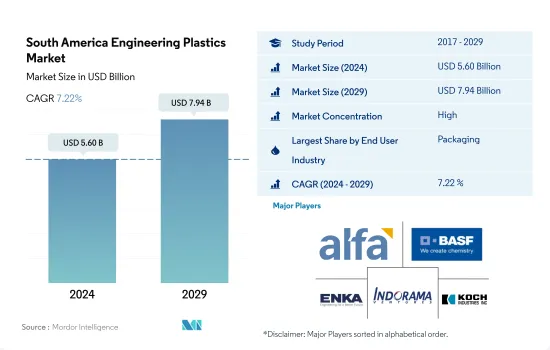

南米のエンジニアリングプラスチック市場規模は2024年に56億米ドルと推定され、2029年には79億4,000万米ドルに達し、予測期間(2024-2029年)のCAGRは7.22%で成長すると予測されます。

予測期間中、市場を独占するのはパッケージング業界

- エンジニアリングプラスチックは、一般的なプラスチックや汎用プラスチックに比べて機械的・熱的特性に優れているため、その用途は無限に広がっています。エンジニアリングプラスチックは、自動車、航空宇宙、建築・建設など、さまざまな応用分野で金属やその他の従来使用されてきた材料に取って代わっています。

- エンジニアリングプラスチックの最大の消費分野はパッケージング業界です。エンプラ製のパッケージには、フィルム、ボトル、容器など、さまざまな素材や形状があり、それぞれに独自の特性があります。これらの特性には、温度範囲、適切な食品用途、保存期間、外観、バリア性などが含まれます。高温と低温の両方の充填に適し、電子レンジによる再加熱も可能なエンジニアリングプラスチックは、予測期間中、この業界からの消費量でCAGR 5.13%が見込まれます。

- 自動車産業はエンジニアリングプラスチックの第2位の消費者であり、高価な金属やその合金に代わって、それぞれ独自の条件や要件に合わせて設計された様々な種類の複合材料が使用されています。同産業は高強度エンジニアリングプラスチックを使用しており、部品加工、組立、メンテナンスのコストを削減するだけでなく、自動車の軽量化とエネルギー効率の向上を実現しています。ブラジルとアルゼンチンはこの地域で最も自動車産業が発達しており、この産業の消費は2023年から2029年にかけて収益ベースでCAGR 6.74%を記録すると予想されます。

- 電気・電子産業は、スマートエレクトロニクスと先進デバイスの需要増加により、最も急成長している分野と予測され、同産業の成長に寄与しています。この業界の需要は予測期間中、数量ベースでCAGR 7.74%を記録すると予測されます。

予測期間中、ブラジルが優位を維持

- 2022年のエンジニアリングプラスチックの世界消費量に占める南米のシェアは、売上高ベースで4.56%でした。エンジニアリングプラスチックは、自動車、包装、電気・電子などさまざまな産業で応用されています。

- ブラジルはエンジニアリングプラスチックの最大消費国で、2022年の売上高は前年比10.18%の伸びを示しました。ブラジルは、南米全体のパッケージングと自動車生産において、それぞれ60%と66%近い数量シェアを占めています。すぐに食べられるコンビニエンス・フードの需要の高まりと、外出の多いライフスタイルの台頭により、包装資材の消費が増加し、同地域のエンジニアリングプラスチックの販売動向が活発化しました。自動車需要の急増は、自家用モビリティ需要の増加の結果です。技術革新が電子機器需要を牽引しています。

- アルゼンチンは自動車産業が主導する消費国として急成長しており、政府は自動車マーキング産業への新規投資を促進し、サプライチェーンを強化するための新法を立法しました。これにより、同産業の輸出志向が強まり、予測期間中に新しいエンジン技術の開発が促進されます。このため、自動車用エンジニアリングプラスチックの需要は増加し、予測期間中に同国のCAGR(収益ベース)は10.77%を記録するとみられます。

- 同地域におけるエンジニアリングプラスチックの消費は、先端材料、有機エレクトロニクス、小型化、破壊的技術の使用により、予測期間中(2023~2029年)に収益ベースでCAGR 7.21%を記録すると予想されます。

南米のエンジニアリングプラスチックスの市場動向

技術革新の急速なペースが業界の成長を後押し

- 南米では、ブラジルが2017年の同地域の電気・電子製品生産収入の40%近い主要シェアを占めています。2017年、ブラジルのエレクトロニクス製品はeコマース分野で20%近い普及率を示しました。同地域における技術の進歩は、スマートテレビ、スマート冷蔵庫、スマートエアコン、その他の電気・電子製品などの家電製品に対する需要を増加させました。南米の電気・電子製品の生産収入は、2017年から2019年にかけて6.16%以上のCAGRを記録しました。

- 2020年、パンデミックによるリモートワークやホームエンターテイメント用の家電製品の需要増加に伴い、同地域の電気・電子製品の生産は、前年比売上高成長率1.1%で増加しました。可処分所得の増加、高級品に対する需要の増加、技術の進歩、生活水準の向上は、電気・電子機器市場の成長を促す主な要因のひとつです。その結果、同地域では、2021年の電気・電子機器生産も売上高で14.9%の割合で増加しました。

- 電子技術革新の急速なペースは、より新しく高速な電気・電子製品に対する一貫した需要を促進しています。その結果、同地域の電気・電子機器生産の需要も増加しています。LG、サムスン、マイクロソフト、パナソニック、デル、インテル、東芝、ソニー、フィリップス、シャープ、アップル、レノボといった多国籍企業の進出も、電気・電子機器市場にプラスの影響を与えています。このような要因はすべて、予測期間中に同地域の電気・電子機器の生産高を7%前後の割合で押し上げると予想されます。

南米のエンジニアリングプラスチックス産業の概要

南米のエンジニアリングプラスチックス市場はかなり統合されており、上位5社で89.63%を占めています。この市場の主要企業は以下の通りです。 Alfa S.A.B. de C.V., BASF SE, Enka, Indorama Ventures Public Company Limited and Koch Industries, Inc.(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 包装

- 輸出入動向

- フッ素樹脂貿易

- ポリアミド(PA)貿易

- ポリカーボネート(PC)貿易

- ポリエチレンテレフタレート(PET)の貿易

- ポリメチルメタクリレート(PMMA)の貿易

- ポリオキシメチレン(POM)貿易

- スチレン共重合体(ABSとSAN)の貿易

- 価格動向

- リサイクルの概要

- ポリアミド(PA)のリサイクル動向

- ポリカーボネート(PC)のリサイクル動向

- ポリエチレンテレフタレート(PET)のリサイクル動向

- スチレン系共重合体(ABS、SAN)のリサイクル動向

- 規制の枠組み

- アルゼンチン

- ブラジル

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 電気・電子

- 工業・機械

- 包装

- その他エンドユーザー産業

- 樹脂タイプ

- フッ素樹脂

- サブタイプ別

- エチレンテトラフルオロエチレン(ETFE)

- フッ素化エチレンプロピレン(FEP)

- ポリテトラフルオロエチレン(PTFE)

- ポリフッ化ビニル(PVF)

- ポリフッ化ビニリデン(PVDF)

- その他のサブレジンタイプ

- 液晶ポリマー(LCP)

- ポリアミド(PA)

- サブレジンタイプ別

- アラミド

- ポリアミド(PA)6

- ポリアミド(PA)66

- ポリフタルアミド

- ポリブチレンテレフタレート(PBT)

- ポリカーボネート(PC)

- ポリエーテルエーテルケトン(PEEK)

- ポリエチレンテレフタレート(PET)

- ポリイミド(PI)

- ポリメチルメタクリレート(PMMA)

- ポリオキシメチレン(POM)

- スチレン共重合体(ABSおよびSAN)

- フッ素樹脂

- 国

- アルゼンチン

- ブラジル

- その他南米

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Alfa S.A.B. de C.V.

- BASF SE

- Celanese Corporation

- China Petroleum & Chemical Corporation

- Covestro AG

- Enka

- Formosa Plastics Group

- Indorama Ventures Public Company Limited

- Koch Industries, Inc.

- LANXESS

- Mitsubishi Chemical Corporation

- SABIC

- Teijin Limited

- Trinseo

- Unigel Plasticos

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The South America Engineering Plastics Market size is estimated at 5.60 billion USD in 2024, and is expected to reach 7.94 billion USD by 2029, growing at a CAGR of 7.22% during the forecast period (2024-2029).

Packaging industry to dominate the market during the forecast period

- Engineering plastics, with their superior mechanical and thermal properties compared to common or commodity plastics, have endless applications. They have replaced metals and other traditionally used materials in various application areas, such as automotive, aerospace, building & construction, and more.

- The packaging industry is the largest consumer of engineering plastics. Packaging made from engineering plastics comes in a variety of material types and forms, including films, bottles, containers, and others, each with its own unique characteristics. These characteristics encompass temperature range, appropriate food use, shelf life, appearance, and barrier properties. Suitable for both hot and cold filling, as well as microwave reheating, engineering plastics are expected to see a CAGR of 5.13% in terms of consumption volume from this industry during the forecast period.

- The automotive industry is the second-largest consumer of engineering plastics, which have replaced expensive metals and their alloys with various types of composites, each designed for unique conditions and requirements. The industry uses high-strength engineering plastics, which not only reduces the cost of part processing, assembly, and maintenance but also makes the vehicle lighter and more energy-efficient. Brazil and Argentina have the most developed automotive industries in the region, and consumption in this industry is expected to record a CAGR of 6.74% in terms of revenue from 2023 to 2029.

- The electrical and electronics industry is projected to be the fastest-growing segment due to the increasing demand for smart electronics and advanced devices, contributing to the industry's growth. The demand in this industry is anticipated to record a CAGR of 7.74% in terms of volume during the forecast period.

Brazil to remain dominant during the forecast period

- South America accounted for a share of 4.56%, by revenue, of the consumption of engineering plastics globally in 2022. Engineering plastics have applications in different industries, such as automotive, packaging, electrical and electronics.

- Brazil is the largest consumer of engineering plastics and witnessed a growth of 10.18% in revenue in 2022 compared to the previous year. Brazil occupied nearly 60% and 66% volume shares of packaging and automotive production, respectively, of overall South America. With the growing demand for ready-to-eat convenience food and the emerging trend of on-the-go lifestyles, the consumption of packaging materials increased, increasing the sales of engineering plastics in the region. The surge in automobile demand is a consequence of the increasing demand for private mobility. Technological innovations are driving demand for electronic gadgets.

- Argentina is the fastest-growing consumer, led by the automotive industry, as the government legislated a new Act to promote new investments in the car-marking industry and strengthen its supply chain. This will reinforce the industry's export-oriented profile, promoting the development of new engine technologies during the forecast period. Therefore, the demand for engineering plastics in automotive is likely to increase, registering a CAGR of 10.77%, by revenue, in the country during the forecast period.

- The consumption of engineering plastics in the region is expected to register a CAGR of 7.21% by revenue during the forecast period (2023-2029), owing to the use of advanced materials, organic electronics, miniaturization, and disruptive technologies.

South America Engineering Plastics Market Trends

Rapid pace of technological innovations to boost the industry growth

- In South America, Brazil held the major share of nearly 40% of the region's electrical and electronics production revenue in 2017. In 2017, Brazilian electronics products had a penetration of nearly 20% in the e-commerce sector. The advancement of technology in the region increased the demand for consumer electronics products, such as smart TVs, smart refrigerators, smart air conditioners, and other electrical and electronic products. South American electrical and electronics production revenue witnessed a CAGR of over 6.16% between 2017 and 2019.

- In 2020, with the rise in demand for consumer electronics for remote working and home entertainment due to the pandemic, the production of electrical and electronic products in the region increased at a growth rate of 1.1% by revenue compared to the previous year. Rising disposable income, increased demand for luxury products, technological advancements, and improvement in living standards are some of the major factors driving the electrical and electronics market's growth. As a result, in the region, electrical and electronics production also increased at a rate of 14.9% by revenue in 2021.

- The rapid pace of electronic technological innovation is driving consistent demand for newer and faster electrical and electronic products. As a result, it has also increased the demand for the production of electrical and electronics in the region. The penetration of multinational companies, like LG, Samsung, Microsoft, Panasonic, Dell, Intel, Toshiba, Sony, Philips, Sharp, Apple, and Lenovo, also positively affects the electrical and electronics market. All such factors are expected to fuel the production revenue of electrical and electronics in the region during the forecast period at a rate of around 7%.

South America Engineering Plastics Industry Overview

The South America Engineering Plastics Market is fairly consolidated, with the top five companies occupying 89.63%. The major players in this market are Alfa S.A.B. de C.V., BASF SE, Enka, Indorama Ventures Public Company Limited and Koch Industries, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.2.1 Fluoropolymer Trade

- 4.2.2 Polyamide (PA) Trade

- 4.2.3 Polycarbonate (PC) Trade

- 4.2.4 Polyethylene Terephthalate (PET) Trade

- 4.2.5 Polymethyl Methacrylate (PMMA) Trade

- 4.2.6 Polyoxymethylene (POM) Trade

- 4.2.7 Styrene Copolymers (ABS and SAN) Trade

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 Argentina

- 4.5.2 Brazil

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymer

- 5.3 Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 BASF SE

- 6.4.3 Celanese Corporation

- 6.4.4 China Petroleum & Chemical Corporation

- 6.4.5 Covestro AG

- 6.4.6 Enka

- 6.4.7 Formosa Plastics Group

- 6.4.8 Indorama Ventures Public Company Limited

- 6.4.9 Koch Industries, Inc.

- 6.4.10 LANXESS

- 6.4.11 Mitsubishi Chemical Corporation

- 6.4.12 SABIC

- 6.4.13 Teijin Limited

- 6.4.14 Trinseo

- 6.4.15 Unigel Plasticos

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms