|

市場調査レポート

商品コード

1685761

米国の外食:市場シェア分析、産業動向、成長予測(2025年~2030年)United States Foodservice - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の外食:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

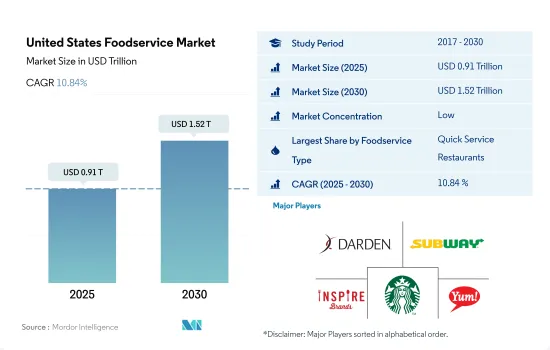

米国の外食市場規模は2025年に9,100億米ドルと推定・予測され、2030年には1兆5,200億米ドルに達し、予測期間中(2025年~2030年)のCAGRは10.84%で成長すると予測されます。

ビーガン、低糖質、グルテンフリーのオプションの導入がフルサービスレストランの成長を促進しています。

- 2022年、米国の外食市場ではクイックサービス・レストランが最大の市場シェアを占めました。このセグメントは予測期間中にCAGR 10.23%を記録しました。市場拡大の重要な指標は、同国における近年の企業の広告費総額です。2021年の米国における主要ファストフードブランドによる広告費は、ドミノ・ピザ(5億1,000万米ドル)、マクドナルド(4億900万米ドル)、タコベル(3億3,400万米ドル)、サブウェイ(3億1,800万米ドル)、ウェンディーズ(2億6,700万米ドル)、バーガーキング(2億2,500万米ドル)、ダンキン(1億3,500万米ドル)、チックフィラ(1億2,900万米ドル)、チポトレ・メキシカン・グリル(1億500万米ドル)、スターバックス(9,700万米ドル)でした。

- フルサービス・レストラン市場は調査期間中CAGR 5.24%を記録しました。2022年には北米料理が38.10%のシェアを占め、同市場で最大となりました。このセグメントの成長は、レストランが伝統的なアメリカ料理にビーガン、低糖質、グルテンフリーのオプションを導入したことに起因しています。FSRの店舗は、国内で栄養食に対する需要が高まっているため、これらの料理をよりヘルシーで消費者にとって魅力的なものにしようとしています。パンケーキ、ワッフル、トーストのような製品は、国内の北米レストランで好まれるオプションです。

- 米国のカフェ&バー分野は、予測期間中に金額ベースでCAGR 9.75%を記録すると予想されます。この成長を支えるのは、同国における紅茶とコーヒーの消費量の増加であり、特にスペシャルティ紅茶やコーヒーのカテゴリーにおいて顕著です。2021年には39億ガロン(約850億人前)以上の紅茶が米国人によって飲まれました。飲まれるお茶の大半は紅茶で(約84%)、緑茶が15%、ウーロン茶、白茶、濃茶が少しです。

米国の外食市場動向

インド料理の人気の高まり、クラウドキッチンの台頭、オンラインフードデリバリーが米国の平均注文額を押し上げます。

- 米国のクイックサービスレストランの店舗数は2017年から2022年にかけてCAGR 0.26%で増加。この市場を牽引しているのは、新しいアイデアの流入、商品の提供、デジタル注文、アクセスのしやすさです。新しいコンセプトの中には、韓国のバーベキューやその他のストリートフードなど、国際的な料理にインスパイアされたものもあります。また、ホットドッグやグリルドチーズサンドイッチのような昔からの人気メニューを、グルメ風にアレンジして再提案する試みもあります。米国ではマクドナルド、チポトレ、スターバックスが大手です。例えば、マクドナルドの今後の戦略は、強力なデジタル・プラットフォームを構築して、アクセスを簡素化し、顧客に購入の選択肢を増やすことです。同様に、チポトレは、堅牢でカスタマイズ可能なメニューが競争力を高めています。そのため、2019年から2022年にかけて、外食産業全体でデジタル注文は23%増加しました。

- フルサービス店舗は、2022年に32.9%と市場で2番目の主要シェアを占めています。フルサービスレストランは、メニューオプションで顧客を魅了することで、より多くの顧客満足を提供します。アップルビーズ(Applebee's)、ルビー・チューズデー(Ruby Tuesday)、チリズ(Chili's)、TGIフライデーズ(TGI Fridays)などのフルサービスチェーンが幅広いメニューを提供することで、店内での食事体験の価値が高まりました。クラウドキッチンの店舗は外食産業で最も急成長している店舗であり、このセグメントは予測期間中にCAGR 9.33%を記録すると予想されています。クラウドキッチンは顧客にサービスを提供するために完全にテクノロジーに依存しています。クラウドキッチンは顧客フィードバック技術の導入でかなり成功しています。テクノロジーの開発と統合の結果、料理の注文と消費は大きな変化を遂げました。

米国では2022年にフルサービス・レストランが台頭し、革新的なメニューと人気料理で健康志向のミレニアル世代に対応しました。

- 米国では、2022年にはフルサービス・レストランの平均注文金額が39米ドルと、他の外食業態と比べて最も高くなることが観察されました。シェフ主導の外食レストランは、より多くの専門的訓練を受けた有名シェフがFSRによってもたらされる成長から利益を得ることに集中するにつれて増加傾向にあります。専門的な訓練を受けたシェフはまた、味覚や健康志向の高まるミレニアル世代のニーズを満たすため、より革新的なメニューや独自のレシピを提供しています。FSRが提供する人気料理は、ブリトー、チラキレス、ポケボウルです。これらの料理の価格はそれぞれ10米ドル、13.5米ドル、17.95米ドルです。

- クイック・サービス・レストランの需要は、消費者行動の変化、人々の多忙なスケジュール、eコマース・チャネルの普及拡大により増加すると予想されます。クイック・サービス・レストランは、持ち帰り、宅配、その他多くのサービスを提供し、顧客体験を向上させ、近代化に対応しているため、特に若者に人気があります。米国の消費者の間でファーストフードに対する食欲が高まっており、クイックサービス・レストランの平均注文額は調査期間中に16.23%増加しました。2022年には、ハンバーガー、ピザ、ソーセージ、ミートボールなど、人気のあるファーストフードの価格は、それぞれ8.75米ドル、16米ドル、8.5米ドル、9.8米ドルでした。近年の鶏肉人気により、アメリカのレストラン・チェーンはメニュー・セレクションを拡大しています。2021年には消費者の21%がチキンを好むようになりました。そのため、多くのQSRやFSRレストランがメニューにフライドチキンを入れています。このような消費者の需要の変化により、事業者は最も満足度の高いメニューを提供するための競争を余儀なくされます。

米国の外食業界の概要

米国の外食市場は断片化されており、上位5社で11.32%を占めています。この市場の主要企業は以下の通り。 Darden Restaurants, Inc., Doctor's Associates, Inc., Inspire Brands, Inc., Starbucks Corporation and Yum!Brands, Inc..

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- アウトレット数

- 平均注文額

- 規制の枠組み

- 米国

- メニュー分析

第5章 市場セグメンテーション

- 外食タイプ

- カフェ&バー

- 料理別

- バー&パブ

- カフェ

- ジュース/スムージー/デザートバー

- コーヒー&ティー専門店

- クラウドキッチン

- フルサービスレストラン

- 料理別

- アジア料理

- ヨーロピアン

- ラテンアメリカ料理

- 中東料理

- 北米料理

- その他のFSR料理

- クイックサービスレストラン

- 料理別

- ベーカリー

- ハンバーガー

- アイスクリーム

- 肉料理

- ピザ

- その他QSR料理

- カフェ&バー

- アウトレット

- チェーン店

- 独立店舗

- ロケーション

- レジャー

- 宿泊施設

- 小売

- 独立型

- 旅行

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- Bloomin'Brands, Inc.

- Brinker International, Inc.

- Chipotle Mexican Grill, Inc.

- Darden Restaurants, Inc.

- Doctor's Associates, Inc.

- Domino's Pizza Inc.

- Inspire Brands, Inc.

- McDonald's Corporation

- MTY Food Group Inc.

- Northland Properties Corporation

- Papa John's International, Inc.

- Restaurant Brands International Inc.

- Seven & I Holdings Co., Ltd.

- Starbucks Corporation

- The Wendy's Company

- Yum!Brands, Inc.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The United States Foodservice Market size is estimated at 0.91 trillion USD in 2025, and is expected to reach 1.52 trillion USD by 2030, growing at a CAGR of 10.84% during the forecast period (2025-2030).

The introduction of vegan, low-sugar, and gluten-free options has fuelled the full-service restaurant's growth

- In 2022, quick service restaurants held the largest market share in the US foodservice market. The segment registered a CAGR of 10.23% during the forecast period. An important indicator of the expansion of the market is the total money that companies spent on advertising in recent years in the country. In 2021, the ad spending by key fast food brands in the United States were Domino's Pizza (USD 510 million), McDonald's (USD 409 million), Taco Bell (USD 334 million), Subway (USD 318 million), Wendy's (USD 267 million), Burger King (USD 225 million), Dunkin' (USD 135 million), Chick-fil-A (USD 129 million), Chipotle Mexican Grill (USD 105 million), and Starbucks (USD 97 million).

- The market for full service restaurants recorded a CAGR of 5.24% during the study period. North American cuisine held the largest share of the market in 2022, with a 38.10% value stake. The growth of the segment can be attributed to the introduction of vegan, low-sugar, and gluten-free options to traditional American dishes by restaurants. FSR outlets have tried to make these dishes healthier and more appealing to the consumer due to the growing demand for nutritional diets in the country. Products like pancakes, waffles, and toast are the preferred options in North American restaurants in the country.

- The cafes & bars segment in the United States is expected to register a CAGR of 9.75%, by value, during the forecast period. The growth will be supported by the rising consumption of tea and coffee in the country, especially in the specialty tea or coffee category. More than 3.9 billion gallons, or about 85 billion servings, of tea were drunk by Americans in 2021. The majority of tea consumed was black tea (about 84%), 15% was green tea, and a little oolong, white, and dark tea.

United States Foodservice Market Trends

The growing popularity of Indian cuisine, the rise in cloud kitchens, and online food delivery driving average order values in the United States

- The number of quick service restaurant outlets in the United States increased at a CAGR of 0.26% from 2017 to 2022. The market is driven by an influx of new ideas, product offerings, digital ordering, and accessibility. Some new concepts are inspired by international cuisines, such as Korean barbecue and other street foods. Others attempt to reintroduce some old favorites, such as hot dogs and grilled cheese sandwiches, by giving them a gourmet makeover. McDonald's, Chipotle, and Starbucks are the leading operators in the United States. For example, McDonald's future strategy is to build a strong digital platform to simplify access and provide customers with more purchasing options. Similarly, Chipotle's robust and customizable menu helps it to compete. Therefore, digital orders grew by 23% across the restaurant industry during 2019-2022.

- Full service outlets held the second major share in the market at 32.9% in 2022. Full service restaurants provide more customer satisfaction by luring customers with their menu options. The value of the on-premise eating experience was enhanced by the provision of a broad range of dishes by full service chains like Applebee's, Ruby Tuesday, Chili's, and TGI Fridays. Cloud kitchen outlets are the fastest-growing outlets in the restaurant industry, and the segment is expected to register a CAGR of 9.33% during the forecast period. Cloud kitchens rely entirely on technology to serve their customers. Cloud kitchens have been quite successful in implementing customer feedback technology. The ordering and consumption of food have undergone significant modifications as a result of technology development and integration.

Full service restaurants rose in the United States in 2022, catering to health-conscious millennials with innovative menus and popular dishes

- In the United States, the average order value was observed as the highest among the full service restaurants in 2022, compared to other foodservice types with a price of USD 39. Chef-driven dining-out restaurants are on the rise as more professionally trained and celebrity chefs focus on benefiting from the growth provided by the FSR. Professionally trained chefs also offer more innovative menus and proprietary recipes to satisfy the needs of the growing taste and health-conscious millennials. Popular dishes offered by the FSR cuisines are Burritos, Chilaquiles, and poke bowls. These cuisines are priced at USD 10, USD 13.5, and USD 17.95, respectively.

- The demand for quick service restaurants is expected to increase due to changes in consumer behavior, people's busy schedules, and growing e-commerce channel penetration. Quick service restaurants are particularly popular with young people since they offer takeaway, home delivery, and many other services to enhance customer experiences and keep up with modernization. With the growing appetite for fast food among American consumers, the average order value for quick service restaurants increased by 16.23% over the study period. In 2022, popular fast food items, including burgers, pizzas, sausages, and meatballs, were priced at USD 8.75, USD 16, USD 8.5, and USD 9.8, respectively. The popularity of chicken in recent years has led American restaurant chains to expand their menu selections. In 2021, 21% of consumers increased their taste for chicken. Thus, many QSR and FSR restaurants include fried chicken in their menus. This consumer demand shift will force operators to compete for the most satisfying offering.

United States Foodservice Industry Overview

The United States Foodservice Market is fragmented, with the top five companies occupying 11.32%. The major players in this market are Darden Restaurants, Inc., Doctor's Associates, Inc., Inspire Brands, Inc., Starbucks Corporation and Yum! Brands, Inc. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Number Of Outlets

- 4.2 Average Order Value

- 4.3 Regulatory Framework

- 4.3.1 United States

- 4.4 Menu Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Foodservice Type

- 5.1.1 Cafes & Bars

- 5.1.1.1 By Cuisine

- 5.1.1.1.1 Bars & Pubs

- 5.1.1.1.2 Cafes

- 5.1.1.1.3 Juice/Smoothie/Desserts Bars

- 5.1.1.1.4 Specialist Coffee & Tea Shops

- 5.1.2 Cloud Kitchen

- 5.1.3 Full Service Restaurants

- 5.1.3.1 By Cuisine

- 5.1.3.1.1 Asian

- 5.1.3.1.2 European

- 5.1.3.1.3 Latin American

- 5.1.3.1.4 Middle Eastern

- 5.1.3.1.5 North American

- 5.1.3.1.6 Other FSR Cuisines

- 5.1.4 Quick Service Restaurants

- 5.1.4.1 By Cuisine

- 5.1.4.1.1 Bakeries

- 5.1.4.1.2 Burger

- 5.1.4.1.3 Ice Cream

- 5.1.4.1.4 Meat-based Cuisines

- 5.1.4.1.5 Pizza

- 5.1.4.1.6 Other QSR Cuisines

- 5.1.1 Cafes & Bars

- 5.2 Outlet

- 5.2.1 Chained Outlets

- 5.2.2 Independent Outlets

- 5.3 Location

- 5.3.1 Leisure

- 5.3.2 Lodging

- 5.3.3 Retail

- 5.3.4 Standalone

- 5.3.5 Travel

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Bloomin' Brands, Inc.

- 6.4.2 Brinker International, Inc.

- 6.4.3 Chipotle Mexican Grill, Inc.

- 6.4.4 Darden Restaurants, Inc.

- 6.4.5 Doctor's Associates, Inc.

- 6.4.6 Domino's Pizza Inc.

- 6.4.7 Inspire Brands, Inc.

- 6.4.8 McDonald's Corporation

- 6.4.9 MTY Food Group Inc.

- 6.4.10 Northland Properties Corporation

- 6.4.11 Papa John's International, Inc.

- 6.4.12 Restaurant Brands International Inc.

- 6.4.13 Seven & I Holdings Co., Ltd.

- 6.4.14 Starbucks Corporation

- 6.4.15 The Wendy's Company

- 6.4.16 Yum! Brands, Inc.

7 KEY STRATEGIC QUESTIONS FOR FOODSERVICE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms