無糖エナジードリンク:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Sugar Free Energy Drinks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 357 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684092

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

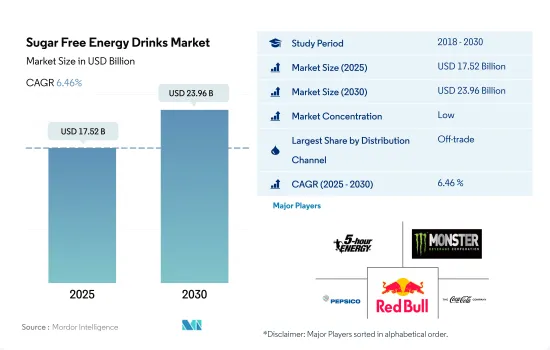

無糖エナジードリンク市場規模は2025年に175億2,000万米ドルと推定・予測され、2030年には239億6,000万米ドルに達し、予測期間(2025年~2030年)のCAGRは6.46%で成長すると予測されます。

流通チャネルによる製品提供のダイナミズムが無糖または低カロリーエナジードリンクの売上を世界的に拡大している

- 2018年から2023年にかけて、オントレード小売業者は無糖または低カロリーエナジードリンクの金額で7.03%の安定したCAGRを示しました。2023年には、この市場で最も急成長しているセグメントに浮上しました。より幅広い消費者層を取り込むため、これらの小売業者はエナジードリンクをメニューに戦略的に配置したり、卓上ディスプレイに陳列したりして、視認性を高め、最終的に売上を強化しています。

- 2023年、エナジードリンク市場は、ウォルマート(Walmart)、ターゲット(Target)、テスコ(Tesco)、アルディ(Aldi)、リドル(Lidl)などの世界的大手を含むハイパーマーケットとスーパーマーケットが極めて重要な役割を果たし、主にオフラインチャネルが主導していました。これらの小売業者は、無糖または低カロリーのエナジードリンクをさまざまなフレーバーとサイズで幅広く提供していました。今後を展望すると、2024年~2028年の間に、非商業的小売業者は金額ベースで26.76%の堅調な成長を遂げると予測されます。この成長は、ロイヤルティプログラムの統合が進み、無糖または低カロリーエナジードリンクのリピート購入が奨励されることによって促進されると予測されます。

- オンライン小売店は、予測期間中のCAGRが8.89%と最も高く、最も急成長するオフトレードチャネルになると予想されます。これはオンライン小売部門の急成長によるもので、成長率では他の伝統的な小売チャネルを凌駕しています。これは、オンライン小売店で容易に入手できる無糖エナジードリンクや低カロリーの需要が増加していることが主な原因です。さらに、エナジードリンクはデジタル・マーケティング戦略やソーシャルメディアを頻繁に利用してターゲット層にリーチし、ブランド認知度と売上を高めています。

消費者の嗜好の変化と、精神的な覚醒度や身体的な健康を高めようとする意向の高まりが市場価値を押し上げると予想される

- 肥満率の上昇とそれに伴う糖尿病などの健康リスクを背景に、無糖または低カロリーのエナジードリンクに対する世界の需要が高まっています。消費者の低糖または無糖の選択肢に対する嗜好の高まりは、複数の要因に起因しています。世界の消費者の半数近く(49%)が体重管理のために、42%が糖尿病への懸念のために、39%が一般的な健康上の懸念のために、これらの飲料を選んでいます。さらに、2021年時点では、世界の消費者の20%が低糖または無糖の代替品の味を好んでいます。

- 北米はエナジードリンク市場のトップランナーであり、調査期間中一貫して金額でリードしています。エナジードリンクの消費は、特にミレニアル世代とZ世代を中心に人気が急上昇しています。エナジードリンクには通常、1杯当たり70~250mgのカフェインが含まれており、エネルギーレベルを高め、精神的鋭敏性を高め、身体的パフォーマンスを向上させることが謳われています。その結果、カフェインを摂取していない人と比べて、より長く、よりハードに働くことが可能になります。北米の消費者における健康への関心の高まりは、市場成長に顕著な影響を与えています。例えば、2022年には、この地域の消費者の大多数(72%)が、飲料に含まれる砂糖を制限するか完全に避けようと積極的に努力しています。

- アフリカは、予測期間中にCAGR 10.67%を予測し、世界的に最も急速な成長を遂げるものと思われます。都市化の急速な進展とアフリカの消費者の健康志向の高まりが相まって、無糖または低カロリーのエナジードリンクの需要に拍車をかけています。これらの飲料は、栄養不足への対応としてだけでなく、バランスのとれた栄養摂取を確保するためにも求められています。アフリカの都市人口は年々着実に増加しています。

世界の無糖エナジードリンク市場動向

低カロリー代替品への需要の高まりと、糖尿病患者に優しい無糖エナジードリンクの入手可能性の増加が市場成長を促進

- 無糖または低カロリーのエナジードリンクは、さまざまなフレーバーやオプションで入手可能であり、無糖エナジードリンクの最も人気のあるフレーバーには、オレンジ、マンゴーレモネード、スイカ、ラズベリーライムなどがあります。

- 世界のエナジードリンク・メーカーは、無糖、低カロリー、カロリーゼロのドリンクを絶えず発売しています。現在、レッドブル、モンスター、ロックスターは、すべての地域で無糖・カロリーゼロのバージョンを市場に投入しています。

- 北米地域のメーカーは、インフレ下でもこのカテゴリーの強さを理解し、一流ブランドや新進気鋭の消費者ブランドから人気商品と革新的商品の両方を仕入れ、無糖エナジードリンクのようなより健康的な選択肢を推進し、中心購買層の人口統計を理解することで、エナジードリンクの売上を伸ばし続けています。

- 健康志向の消費者は、糖分含有量の少ないエナジードリンクや、「無糖」「減糖」と表示されたエナジードリンクを求めることが多いです。砂糖の大量摂取は、肥満や糖尿病を含む様々な健康問題に関連しています。

無糖エナジードリンク産業の概要

無糖エナジードリンク市場は細分化されており、上位5社で27.54%を占めています。この市場の主要企業は以下の通り。 Living Essentials, LLC, Monster Beverage Corporation, PepsiCo, Inc., Red Bull GmbH and The Coca-Cola Company.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 消費者の購買行動

- イノベーション

- ブランドシェア分析

- 規制の枠組み

第5章 市場セグメンテーション

- 包装タイプ

- ガラス瓶

- 金属缶

- ペットボトル

- 流通チャネル

- オフトレード

- コンビニエンスストア

- オンライン小売

- スーパーマーケット/ハイパーマーケット

- その他

- オン・トレード

- オフトレード

- 地域

- アフリカ

- エジプト

- ナイジェリア

- 南アフリカ

- その他のアフリカ

- アジア太平洋

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- 韓国

- タイ

- ベトナム

- その他のアジア太平洋

- 欧州

- ベルギー

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- トルコ

- 英国

- その他の欧州

- 中東

- カタール

- サウジアラビア

- アラブ首長国連邦

- その他の中東

- 北米

- カナダ

- メキシコ

- 米国

- その他の北米

- 南米

- アルゼンチン

- ブラジル

- その他の南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- A.G. BARR P.L.C.

- Carabao Group Public Company Limited

- Congo Brands

- Ghost Beverages, LLC

- Kingsley Beverages Limited

- Living Essentials, LLC

- Monster Beverage Corporation

- PepsiCo, Inc.

- Red Bull GmbH

- Suntory Holdings Limited

- Synergy Chc Corp.

- The Coca-Cola Company

- Woodbolt Distribution, LLC

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 50002089

The Sugar Free Energy Drinks Market size is estimated at 17.52 billion USD in 2025, and is expected to reach 23.96 billion USD by 2030, growing at a CAGR of 6.46% during the forecast period (2025-2030).

Dynamism in product offerings by distribution channels is expanding the sales of sugar-free or low-calorie energy drinks globally

- Between 2018 and 2023, on-trade retailers witnessed a steady CAGR of 7.03% in the value of sugar-free or low-calorie energy drinks. In 2023, they emerged as the fastest-growing segment in this market. To tap into a wider consumer base, these retailers are strategically placing energy drinks on their menus or showcasing them on tabletop displays, ensuring heightened visibility and ultimately bolstering sales.

- In 2023, the energy drink market was predominantly led by off-trade channels, with hypermarkets and supermarkets, including global giants like Walmart, Target, Tesco, Aldi, and Lidl, playing pivotal roles. These retailers offered an extensive range of sugar-free or low-calorie energy drinks in various flavors and sizes. Looking ahead, during 2024-2028, off-trade retailers are projected to witness a robust 26.76% growth by value. This growth is anticipated to be fueled by their increasing integration of loyalty programs and incentivizing repeat purchases of sugar-free or low-calorie energy drinks.

- Online retail stores are expected to be the fastest-growing off-trade channels with the highest CAGR of 8.89% during the forecast period. This is due to the rapid growth of the online retail sector, which is outpacing all other traditional retail channels in terms of growth rate. This is largely attributed to the increasing demand for sugar-free energy drinks and low-calorie, which are readily available at online retail stores. Furthermore, energy drinks frequently use digital marketing strategies and social media to reach their target audience, thus increasing their brand awareness and sales.

Changing consumer preferences with growing intent to increase mental alertness and physical health expected to boost market values

- The global demand for sugar-free or low-calorie energy drinks is rising, driven by escalating obesity rates and the associated health risks, such as diabetes. Consumers' growing preference for low or no-sugar options stems from multiple factors. Nearly half (49%) of global consumers opt for these beverages to manage their weight, while 42% do so due to concerns about diabetes, and 39% are motivated by general health concerns. Additionally, as of 2021, 20% of global consumers favored the taste of low or no-sugar alternatives.

- North America is the frontrunner in the energy drinks market, leading consistently in terms of value during the study period. Energy drink consumption has witnessed a significant surge in popularity, particularly among the millennial and Gen Z demographics. These drinks, typically containing 70 to 250 mg of caffeine per serving, are touted to boost energy levels, enhance mental acuity, and improve physical performance. This, in turn, enables people to work longer and harder compared to their non-caffeinated counterparts. Rising health concerns among North American consumers are notably influencing market growth. For example, in 2022, a substantial majority (72%) of consumers in the region actively sought to limit or completely avoid sugar in their beverages.

- Africa is poised to witness the most rapid growth globally, projecting a value CAGR of 10.67% during the forecast period. The surge in urbanization, coupled with a heightened focus on health among African consumers, is fueling the demand for sugar-free or low-calorie energy drinks. These beverages are sought after not only as a response to nutritional deficiencies but also to ensure a balanced nutrient intake. The urban population in Africa has been steadily increasing year after year.

Global Sugar Free Energy Drinks Market Trends

Rising demand for low-calorie alternatives and increasing availability of diabetic friendly sugar-free energy drinks is propelling the market growth

- Sugar-free or low-calorie energy drinks are available in a variety of flavors and options, some of the most popular flavors of sugar-free energy drinks include orange, mango lemonade, watermelon, raspberry lime, and others.

- Energy drink manufacturers globally are constantly introducing sugar-free, low calorific and calorie free drinks. Currently, Red Bull, Monster, and Rockstar all have sugar-free and calorie-free version in the market across all the regions.

- Manufacturers in the North America region continue to grow energy drink sales by understanding the category's strength even through inflation, stocking both popular and innovative products from leading and up-and-coming consumer brands, promoting healthier options like sugar-free energy drinks, and understanding demographics of the core shopper.

- Health-conscious consumers often seek energy drinks with lower sugar content or those labeled as "sugar-free" or "reduced sugar. High sugar intake is associated with various health issues, including obesity and diabetes.

Sugar Free Energy Drinks Industry Overview

The Sugar Free Energy Drinks Market is fragmented, with the top five companies occupying 27.54%. The major players in this market are Living Essentials, LLC, Monster Beverage Corporation, PepsiCo, Inc., Red Bull GmbH and The Coca-Cola Company (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Buying Behaviour

- 4.2 Innovations

- 4.3 Brand Share Analysis

- 4.4 Regulatory Framework

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Packaging Type

- 5.1.1 Glass Bottles

- 5.1.2 Metal Can

- 5.1.3 PET Bottles

- 5.2 Distribution Channel

- 5.2.1 Off-trade

- 5.2.1.1 Convenience Stores

- 5.2.1.2 Online Retail

- 5.2.1.3 Supermarket/Hypermarket

- 5.2.1.4 Others

- 5.2.2 On-trade

- 5.2.1 Off-trade

- 5.3 Region

- 5.3.1 Africa

- 5.3.1.1 Egypt

- 5.3.1.2 Nigeria

- 5.3.1.3 South Africa

- 5.3.1.4 Rest of Africa

- 5.3.2 Asia-Pacific

- 5.3.2.1 Australia

- 5.3.2.2 China

- 5.3.2.3 India

- 5.3.2.4 Indonesia

- 5.3.2.5 Japan

- 5.3.2.6 Malaysia

- 5.3.2.7 South Korea

- 5.3.2.8 Thailand

- 5.3.2.9 Vietnam

- 5.3.2.10 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 Belgium

- 5.3.3.2 France

- 5.3.3.3 Germany

- 5.3.3.4 Italy

- 5.3.3.5 Netherlands

- 5.3.3.6 Russia

- 5.3.3.7 Spain

- 5.3.3.8 Turkey

- 5.3.3.9 United Kingdom

- 5.3.3.10 Rest of Europe

- 5.3.4 Middle East

- 5.3.4.1 Qatar

- 5.3.4.2 Saudi Arabia

- 5.3.4.3 United Arab Emirates

- 5.3.4.4 Rest of Middle East

- 5.3.5 North America

- 5.3.5.1 Canada

- 5.3.5.2 Mexico

- 5.3.5.3 United States

- 5.3.5.4 Rest of North America

- 5.3.6 South America

- 5.3.6.1 Argentina

- 5.3.6.2 Brazil

- 5.3.6.3 Rest of South America

- 5.3.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 A.G. BARR P.L.C.

- 6.4.2 Carabao Group Public Company Limited

- 6.4.3 Congo Brands

- 6.4.4 Ghost Beverages, LLC

- 6.4.5 Kingsley Beverages Limited

- 6.4.6 Living Essentials, LLC

- 6.4.7 Monster Beverage Corporation

- 6.4.8 PepsiCo, Inc.

- 6.4.9 Red Bull GmbH

- 6.4.10 Suntory Holdings Limited

- 6.4.11 Synergy Chc Corp.

- 6.4.12 The Coca-Cola Company

- 6.4.13 Woodbolt Distribution, LLC

7 KEY STRATEGIC QUESTIONS FOR SOFT DRINK CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

無糖エナジードリンク:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 357 Pages

- 納期

- 2~3営業日