|

市場調査レポート

商品コード

1684038

欧州のMLCC:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のMLCC:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 316 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

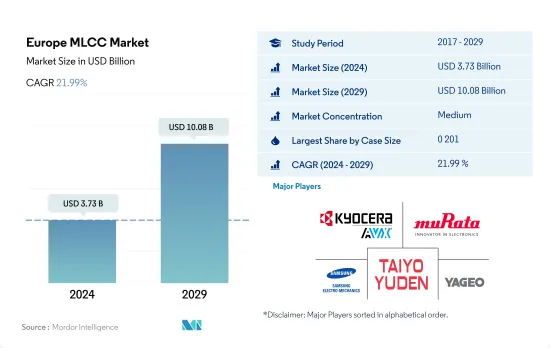

欧州のMLCC市場規模は2024年に37億3,000万米ドルと推定・予測され、2029年には100億8,000万米ドルに達し、市場推計・予測期間(2024年~2029年)のCAGRは21.99%で成長すると予測されています。

5G基地局の展開と地域における軍事費の増加がMLCCのニーズを促進

- ケースサイズ0 201がトップランナーとして浮上し、2022年の数量ベースで34.55%の最大市場シェアを獲得、次いでケースサイズ0 402が19.57%、ケースサイズ0 603が14.10%です。

- ケースサイズ0 402は最もコンパクトで、回路基板の部品密度を高めることができます。欧州の航空宇宙・防衛セクターが通信機器や無人航空機(UAV)などの先端技術やシステムに投資する中、100uF~1000uFの中間容量を持つX7R誘電体0 402 MLCCは、信頼性が高く効率的な電力性能を維持する上で不可欠な役割を果たすため、ニーズが高まると予想されます。医療機器の設計者は現在、ICDやペースメーカーのさらなる小型化を目指し、革新的なデバイス設計の開発に取り組んでいます。これらのデバイスは、いずれも人体内に収納されるため、可能な限り小型でなければならないです。現在、無鉛ペースメーカーの開発が進められており、その大きさは従来のペースメーカーの約10分の1になると推定されています。そのため、コンデンサーを含め、これらの機器に使用される電気部品のさらなる小型化が必要になるかもしれないです。

- 0 603 MLCCの需要を牽引しているのは通信業界です。欧州の通信セクターは、5G基地局の迅速な展開に注力しており、X5R誘電体を使用した0 603ケースサイズのMLCCの需要が増加しています。

5G対応スマートフォンのような民生用電子機器の使用増加や、ARやVRのような新技術の進歩がMLCC需要を牽引しています。

- ドイツがトップランナーに浮上し、2022年の数量ベースで25.07%の最大市場シェアを獲得、次いで14.99%の英国が続きます。

- 英国の家電製造部門が牽引役となっています。英国のような国の家電市場は、今後数年で急成長が見込まれます。5Gネットワーク、スマートホーム、AR・VR技術、機能を強化した家電機器の絶え間ない進化も、この成長に寄与する可能性があります。その結果、100uF以下の低キャパシタンスを持つ0 201ケースサイズの表面実装タイプの設置型積層セラミックコンデンサ(MLCC)の需要が伸びると予想されます。

- ドイツの自動車産業は、同国の経済成長に最も貢献している分野のひとつです。そのため、X7R MLCCの需要は増加傾向にあります。自動運転機能のないエンジン車には通常約3,000個のMLCCが必要だが、電気自動車(EV)には通常8,000~1万個のMLCCが必要です。自動車セクターの現状は、ドイツで行われている急速な技術開発に見ることができます。さらに、ドイツ政府の規制、インセンティブ、割引、eモビリティに対する意識の高まりが、消費者のEV購入を後押ししています。

欧州のMLCC市場動向

厳しい政府規制が電動LCVの普及を促進

- 小型商用車(LCV)の生産台数は、2019年から2022年にかけてまちまちの結果となりました。2019年の252万台から始まり、2020年には211万台とわずかに減少しました。しかし、2021年には218万台と回復し、2022年には214万台と安定し、4年間のCAGRは約4.6%となりました。

- 2019年までの数年間、業界はLCV生産のCAGRが最も高いことを示しました。しかし、その後の数年間は、COVID-19パンデミックを含む混乱と不確実性が顕著となり、自動車業界全体に大きな影響を与えました。サプライチェーンの混乱と消費者需要の減少が生産減少の一因となりました。それにもかかわらず、業界は一定の生産水準を維持することで回復力を示しました。

- 欧州議会が「Fit for 55」パッケージの一環として乗用車と小型商用車の新たなCO2排出量削減目標を承認したことは、MLCC市場を含む自動車産業に大きな影響を与えると思われます。自動車産業がCO2排出量ゼロを目指し、電気自動車の普及が進むにつれて、MLCCの需要は高まると予想されます。

- 欧州委員会が義務付けるOBFCMの設置は、MLCCの需要をさらに押し上げると思われます。これらのコンポーネントは、車両システム内での正確な測定、データ処理、通信を可能にし、CO2排出量とエネルギー消費量の監視をサポートします。販売動向を反映したZLEVインセンティブメカニズムの適応により、ゼロエミッション車の生産と購入が奨励され、MLCCの需要が増加します。

欧州におけるOBFCM装置の採用拡大も乗用車の生産を増加させた

- 欧州では、乗用車の生産台数が減少しました。2019年の生産台数は1,870万台であったが、2022年には1,372万台に減少し、4年間のCAGRは約-8.7%でした。

- この生産台数の減少は、製造施設の一時的閉鎖、消費者の購買力の低下、パンデミックによる市場全体の不確実性など、さまざまな要因によるものと考えられます。しかし、欧州の自動車部門が逆境に直面しても回復力と適応力を示したことは重要です。

- 2019年に小型車CO2規制が施行され、排出ガス削減と気候変動への対応に改めて焦点が当てられました。この規制は、路上での燃料消費と電気エネルギー消費を正確に監視する必要性を強調し、新車への車載燃料・エネルギー消費監視装置(OBFCM)の搭載につながりました。この規制の枠組みは、欧州のMLCC市場で事業を展開する企業にチャンスをもたらします。MLCCは、自動車用電子機器を含む様々な用途に使用される不可欠な電子部品です。OBFCMやその他のモニタリング・デバイスの統合により自動車がより高度化するにつれ、MLCCの需要は増加すると予想されます。これらの部品は、自動車のシステム内で正確な測定、データ処理、通信を可能にする上で重要な役割を果たしています。

- 業界がOBFCMのような先進技術の統合に向けて取り組む中で、MLCCは、実際のCO2削減を達成し、実際の走行条件下で車両が期待通りの性能を発揮するために重要な役割を果たすことになります。

欧州のMLCC産業の概要

欧州のMLCC市場は適度に統合されており、上位5社で51.04%を占めています。この市場の主要企業は以下の通り。 Kyocera AVX Components Corporation(Kyocera Corporation), Murata Manufacturing, Samsung Electro-Mechanics, Taiyo Yuden and Yageo Corporation(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 価格動向

- 銅の価格動向

- ニッケル価格動向

- 銀価格の動向

- 亜鉛価格動向

- 家電販売台数

- エアコン販売台数

- デスクトップPC販売台数

- ゲーム機販売

- ノートパソコン販売

- 冷蔵庫販売

- スマートフォン販売

- 収納機器販売

- タブレット販売

- テレビ販売

- 自動車生産

- バス生産

- 大型トラック生産

- 小型商用車生産

- 乗用車生産

- 自動車生産

- EV生産

- BEV(バッテリー電気自動車)の生産

- PHEV(プラグイン・ハイブリッド車)生産台数

- 産業用オートメーション売上高

- 産業用ロボット販売

- サービスロボット販売

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 誘電体タイプ

- クラス1

- クラス2

- ケースサイズ

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- その他

- 電圧

- 500V~1000V

- 500V未満

- 1000V以上

- 静電容量

- 100uF~1,000uF

- 100uF未満

- 1,000uF以上

- Mlcc実装タイプ

- 金属キャップ

- ラジアルリード

- 表面実装

- エンドユーザー

- 航空宇宙および防衛

- 自動車

- 民生用電子機器

- 産業機器

- 医療機器

- 電力・公益事業

- 通信機器

- その他

- 国名

- ドイツ

- 英国

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Europe MLCC Market size is estimated at 3.73 billion USD in 2024, and is expected to reach 10.08 billion USD by 2029, growing at a CAGR of 21.99% during the forecast period (2024-2029).

5G base station rollouts and the growing military spending in the region are driving the need for MLCCs

- The 0 201 case size segment emerged as the frontrunner, capturing the largest market share of 34.55%, followed by the 0 402 case size segment with 19.57% and the 0 603 case size segment with 14.10% in terms of volume in 2022.

- The case size of 0 402 is among the most compact available, thus increasing the component density of the circuit board. As the European aerospace and defense sector invests in advanced technologies and systems, such as communication equipment and unmanned aerial vehicles (UAVs), the need for 0 402 MLCCs with X7R dielectric with a mid capacitance of 100uF-1000uF is expected to grow due to their essential role in sustaining dependable and efficient power performance. Medical device designers are currently working to develop innovative device designs to reduce the size of ICDs and pacemakers further. These devices must be as small as possible, as they are both contained within the human body. The development of lead-free pacemakers is currently underway, and they are estimated to be approximately one-tenth the size of a traditional pacemaker. Therefore, further miniaturization of the electrical components used in these devices, including capacitors, may be necessary.

- The demand for 0 603 MLCCs is being driven by the telecommunications industry. The European telecommunications sector is focusing on rapid 5G base station deployment, thus increasing the demand for 0 603 case size MLCCs with X5R dielectric.

The increasing usage of consumer electronics like 5G-enabled smartphones and new technological advancements like AR and VR are driving the MLCC demand

- Germany emerged as the frontrunner, capturing the largest market share of 25.07%, followed by the United Kingdom, with 14.99%, in terms of volume in 2022.

- The United Kingdom's consumer electronics manufacturing sector is gaining traction. Consumer electronics markets in countries like the United Kingdom are expected to grow rapidly in the coming years. 5G networks, smart homes, AR and VR technologies, and the constant evolution of consumer electronics devices with enhanced features may also contribute to this growth. As a result, the demand for installed multi-layer ceramic capacitors (MLCCs) of the surface-mount type of 0 201 case size, with a low capacitance below 100uF, is expected to grow.

- The German automotive sector is one of the biggest contributors to the country's economic growth. As a result, the demand for X7R MLCCs is on the rise. An engine-powered vehicle without an automatic driving feature typically needs around 3,000 MLCCs, whereas an electric vehicle (EV) typically requires 8,000-10,000 MLCCs. The current state of the automotive sector can be seen in the rapid technological development taking place in Germany. In addition, the German government's regulations, incentives, and discounts, as well as the growing awareness of e-mobility, are driving consumers to purchase EVs.

Europe MLCC Market Trends

Stringent government regulations increase the penetration of electric LCVs

- Light commercial vehicles (LCVs) production exhibited a mixed performance between 2019 and 2022. Starting at 2.52 million units in 2019, it experienced a slight decline in 2020 to 2.11 million units. However, there was a rebound in 2021 with a production volume of 2.18 million units, followed by stability at 2.14 million units in 2022, indicating a CAGR of around 4.6% over the four years, reflecting the challenging and volatile nature of the market.

- In the years leading up to 2019, the industry witnessed the highest CAGR in LCV production. However, subsequent years were marked by disruptions and uncertainties, including the COVID-19 pandemic, which significantly impacted the overall automotive industry. Supply chain disruptions and reduced consumer demand contributed to the decline in production. Nonetheless, the industry demonstrated resilience by maintaining a certain level of production.

- The approval of new CO2 emissions reduction targets for passenger cars and light commercial vehicles by the European Parliament as part of the "Fit for 55" package will have a substantial impact on the automotive industry, including the market for MLCCs. As the industry moves towards zero CO2 emissions and increased adoption of electric vehicles, the demand for MLCCs is expected to rise.

- The installation of OBFCMs, as mandated by the European Commission, will further drive the demand for MLCCs. These components enable accurate measurement, data processing, and communication within vehicle systems, supporting monitoring of CO2 emissions and energy consumption. Adapting the ZLEV incentive mechanism to reflect sales trends will incentivize the production and purchase of zero-emission vehicles, increasing demand for MLCCs.

The increased adoption of OBFCM devices in Europe also increased the production of passenger vehicles

- In Europe, the production of passenger vehicles witnessed a decline. Starting at a production volume of 18.70 million units in 2019, it decreased to 13.72 million units in 2022, with a CAGR of approximately -8.7% over the four years, mirroring the difficult market conditions and disruptions encountered by the European automotive sector.

- This decline in production can be attributed to various factors, including the temporary closure of manufacturing facilities, reduced consumer purchasing power, and overall market uncertainty caused by the pandemic. However, it is important to note that the European automotive sector has shown resilience and adaptability in the face of adversity.

- With the implementation of the light-duty vehicle CO2 regulation in 2019, there was a renewed focus on reducing emissions and addressing climate change. This regulation emphasizes the need for accurate monitoring of on-road fuel and electric energy consumption, leading to the installation of onboard fuel and energy consumption monitoring devices (OBFCMs) in new vehicles. This regulatory framework creates opportunities for businesses operating in the European MLCC market. MLCCs are essential electronic components used in various applications, including automotive electronics. As vehicles become more sophisticated with the integration of OBFCMs and other monitoring devices, the demand for MLCCs is expected to increase. These components play a crucial role in enabling accurate measurement, data processing, and communication within the vehicle's systems.

- As the industry works toward the integration of advanced technologies, such as OBFCMs, it will play a crucial role in achieving real-world CO2 reductions and ensuring vehicles perform as expected in real-world driving conditions.

Europe MLCC Industry Overview

The Europe MLCC Market is moderately consolidated, with the top five companies occupying 51.04%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Price Trend

- 4.1.1 Copper Price Trend

- 4.1.2 Nickel Price Trend

- 4.1.3 Silver Price Trend

- 4.1.4 Zinc Price Trend

- 4.2 Consumer Electronics Sales

- 4.2.1 Air Conditioner Sales

- 4.2.2 Desktop PC's Sales

- 4.2.3 Gaming Console Sales

- 4.2.4 Laptops Sales

- 4.2.5 Refrigerator Sales

- 4.2.6 Smartphones Sales

- 4.2.7 Storage Unit Sales

- 4.2.8 Tablets Sales

- 4.2.9 Television Sales

- 4.3 Automotive Production

- 4.3.1 Buses and Coaches Production

- 4.3.2 Heavy Trucks Production

- 4.3.3 Light Commercial Vehicles Production

- 4.3.4 Passenger Vehicles Production

- 4.3.5 Total Motor Production

- 4.4 Ev Production

- 4.4.1 BEV (Battery Electric Vehicle) Production

- 4.4.2 PHEV (Plug-in Hybrid Electric Vehicle) Production

- 4.5 Industrial Automation Sales

- 4.5.1 Industrial Robots Sales

- 4.5.2 Service Robots Sales

- 4.6 Regulatory Framework

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Others

- 5.3 Voltage

- 5.3.1 500V to 1000V

- 5.3.2 Less than 500V

- 5.3.3 More than 1000V

- 5.4 Capacitance

- 5.4.1 100µF to 1000µF

- 5.4.2 Less than 100µF

- 5.4.3 More than 1000µF

- 5.5 Mlcc Mounting Type

- 5.5.1 Metal Cap

- 5.5.2 Radial Lead

- 5.5.3 Surface Mount

- 5.6 End User

- 5.6.1 Aerospace and Defence

- 5.6.2 Automotive

- 5.6.3 Consumer Electronics

- 5.6.4 Industrial

- 5.6.5 Medical Devices

- 5.6.6 Power and Utilities

- 5.6.7 Telecommunication

- 5.6.8 Others

- 5.7 Country

- 5.7.1 Germany

- 5.7.2 United Kingdom

- 5.7.3 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms