北米のMLCC:市場シェア分析、産業動向、成長予測(2025年~2030年)

North America MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 306 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684052

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

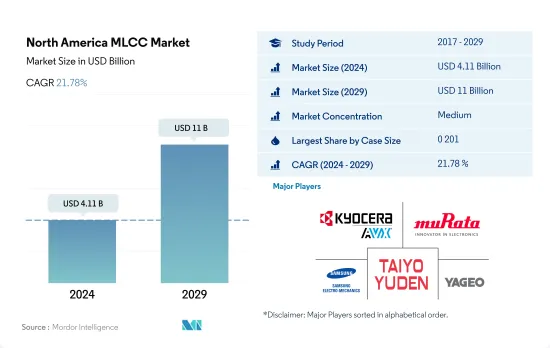

北米のMLCC市場規模は2024年に41億1,000万米ドルと推定・予測され、2029年には110億米ドルに達し、予測期間(2024年~2029年)のCAGRは21.78%で成長すると予測されています。

斬新な技術の出現に対する消費者の意識の高まりが、0 201 MLCCの主な成長刺激要因のひとつです。

- ケースサイズ0 201は、数量ベースで32.73%の最大市場シェアを占め、2022年には6億4,490万米ドルの収益を生み出しました。ケースサイズ0 603は最も急成長しているセグメントで、CAGRは29.10%(2022年~2029年)です。

- 現在進行中の小型化の動向は、部品の高密度化の必要性と相まって、これらの部品の需要を牽引しています。ポータブル機器やコネクテッド機器の人気が高まっていることも、0.201MLCC部品の需要を高めています。北米にはノートパソコン・メーカーや多国籍企業が数社あり、市場で大きな存在感を示しています。ビデオ会議、バーチャル・コラボレーション・ツール、オンライン教育へのニーズの高まりが、ノートパソコンの販売を加速させています。

- 0 1005 MLCCの用途は多岐にわたり、特にスマートフォン、ウェアラブル、IoT機器などの小型電子機器では、メーカーが性能を損なうことなくスマートでコンパクトな設計を実現できるようになっています。カナダでは、消費者が既存の携帯電話のアップグレードを含め、デバイスに費やす金額が増えるにつれて、スマートフォンのユーザー数が年々増加しています。

- ケースサイズ0 402は、表面実装セラミックコンデンサのフォームファクターとして広く採用されています。自動車業界では、エンジン制御ユニット、インフォテインメント・システム、ADASなど、さまざまな用途で0 402 MLCCが使用されています。これらのコンデンサは、過酷な自動車環境において信頼性の高い性能を発揮します。北米では、自動車の安全性重視の高まり、自動車の快適機能に対する需要の高まり、事故時のヒューマンエラーを減らしたいという自動車所有者の願望の高まりにより、自律走行車に対する需要が高まっています。

政府の優遇措置と補助金により、米国でのEV需要が増加する見込み

- 2022年の市場シェアは米国が56.69%で最も大きく、次いでその他が43.31%で僅差で続きます。

- 米国はMLCCにとって最も重要な市場のひとつです。同国は先進自動車、特に電気自動車と自律走行技術のパイオニアのひとつです。MLCCのエンドユーザー向けアプリケーションの主要企業のほとんどは米国に拠点を置いており、同国はMLCCメーカーにとって主要なターゲットとなっています。これらの企業のほとんどが製品提供を進めているため、MLCCの展開数は増加しています。このため、米国は予測期間中、MLCCの重要な市場のひとつになると思われます。

- 環境問題と闘うというカナダのビジョンは、電気自動車とエネルギー貯蔵システム市場の開拓に大きな要因となっており、調査対象市場のベンダーにとってはさらにチャンスとなっています。カナダは、電気自動車への切り替えに向けた新たな国際同盟に調印しました。同国はまた、主にデジタル技術の採用率が高いことから、ハイエンド電子機器の巨大市場を提供しています。カナダ・エンターテインメント・ソフトウェア協会(ESAC)によると、カナダのゲーム産業は活況を呈しており、ハイエンド機器の普及が進んでいます。こうした主な要因がMLCCの需要を促進しています。

北米のMLCC市場動向

eコマース産業の開発が小型商用車を牽引する見込み

- パンデミックは、小型商用車業界において、これまでになかったサプライチェーンの問題を引き起こしたロックダウンやその他の制限をもたらしました。パンデミックは、世界中で前例のないレベルと種類の移動・旅行制限を引き起こしました。インフラ、輸送、ロジスティクスなど、物資を輸送するエンドユーザー産業は完全に機能停止し、製造業や貨物業界に新たな課題を突きつけた。小型商用車(LCV)市場は、北米のeコマース部門と物流の成長によって牽引されています。インターネットにアクセスし、スマートフォンを利用できる人の数が増えるにつれ、オンライン小売店の数も増えています。その結果、小型商用車の需要が増加し、顧客へのタイムリーな商品配送が促進されると予想されます。

- カナダでは、乗用車および小型トラックの温室効果ガス排出規制により、新型小型車に対する温室効果ガス排出上限が設定されました。物流とeコマース分野の拡大により、LCVの需要が増加すると予想されます。都市化の進展により、小型商用車(LCV)市場は、効率的な物流を必要とする新たな小売・eコマースプラットフォームの開発とともに拡大しています。BEVの人気の高まり、EVの新モデルの導入、充電インフラの開発が、市場の成長を促す主な要因となっています。

運転支援システムに対する意識の高まりが需要を創出

- 北米の乗用車市場は驚異的な成長を遂げ、2019年の生産台数は297万台となりました。米国は世界第3位の電気自動車生産国です。EVの成長を促進する政府の取り組みにより、EVへのシフトは現在のペースで続いています。

- COVID-19パンデミックは、世界中のサプライチェーンが崩壊したために自動車の生産に混乱が生じ、市場の成長を阻害しました。しかし、電気自動車が環境に与えるプラスの影響に対する意識の高まりや、各国政府によるさまざまな取り組みにより、予測期間中に市場は大きな成長を遂げることが予想されます。

- いくつかのOEMは、電気自動車の需要増に対応するため、生産能力の増強に関心を持つようになりました。内燃機関車を禁止する政府の政策も電気自動車の販売を後押ししました。世界のさまざまな理由によるガソリンとディーゼルの価格上昇は、電気自動車メーカーにとって販売台数の増加を容易にしました。第3位の市場である米国の電気自動車販売台数は2022年に55%増加し、販売シェアは8%に達しました。

- 2019年5月、連邦政府はゼロ・エミッション車(iZEV)向けインセンティブ・プログラムを開始しました。このインセンティブに基づくイニシアチブは、カナダ人とカナダ企業のゼロ・エミッション車の購入またはリースを支援することを目的としています。2022年、カナダ連邦政府はゼロ・エミッション車の販売義務化を発表しました。2026年までに、カナダ国内で販売される新車の少なくとも20%をゼロ・エミッション車とすることを目標としています。これは2030年までに60%に増加し、2035年までに100%に急増する予定です。

北米のMLCC産業概要

北米のMLCC市場は適度に統合されており、上位5社で41.61%を占めています。この市場の主要企業は以下の通り。 Kyocera AVX Components Corporation(Kyocera Corporation), Murata Manufacturing, Samsung Electro-Mechanics, Taiyo Yuden and Yageo Corporation(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 価格動向

- 銀の価格動向

- 亜鉛の価格動向

- 家電販売台数

- エアコン販売台数

- デスクトップPC販売台数

- ゲーム機販売

- ノートパソコン販売

- 冷蔵庫販売

- スマートフォン販売

- 収納機器販売

- タブレット販売

- テレビ販売

- 自動車生産

- 大型トラック生産

- 小型商用車生産

- 乗用車生産

- モーター生産

- 産業用オートメーション売上高

- 産業用ロボット販売

- サービスロボット販売

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 誘電体タイプ

- クラス1

- クラス2

- ケースサイズ

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- その他

- 電圧

- 500V~1000V

- 500V未満

- 1000V以上

- 静電容量

- 100uF~1,000uF

- 100uF未満

- 1,000uF以上

- Mlcc実装タイプ

- 金属キャップ

- ラジアルリード

- 表面実装

- エンドユーザー

- 航空宇宙および防衛

- 自動車

- 民生用電子機器

- 産業機器

- 医療機器

- 電力・公益事業

- 通信機器

- その他

- 国名

- 米国

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The North America MLCC Market size is estimated at 4.11 billion USD in 2024, and is expected to reach 11 billion USD by 2029, growing at a CAGR of 21.78% during the forecast period (2024-2029).

Increasing awareness among consumers about the emergence of novel technologies is among the primary growth stimulants of 0 201 MLCCs

- Case size 0 201 holds the largest market share of 32.73% in terms of volume and generated a revenue of USD 644.90 million in 2022. The case size 0 603 is the fastest-growing segment, with a CAGR of 29.10% (2022-2029).

- The ongoing trend of miniaturization, coupled with the need for higher component density, drives the demand for these components. The increasing popularity of portable and connected devices further contributes to the demand for 0 201 MLCC components, as they enable manufacturers to achieve compact designs without compromising on performance. North America is home to several laptop manufacturers and multinational companies that have a significant presence in the market. The increased need for video conferencing, virtual collaboration tools, and online education has accelerated laptop sales.

- The usage of 0 1005 MLCCs spans diverse applications, particularly in compact electronic devices such as smartphones, wearables, and IoT devices, enabling manufacturers to achieve sleek and compact designs without compromising performance. The number of smartphone users in Canada is increasing every year as consumers spend more money on devices, including upgrades to their existing phones.

- The 0 402 case size is widely adopted as a form factor for surface-mount ceramic capacitors. The automotive industry relies on 0 402 MLCCs for various applications, including engine control units, infotainment systems, and ADAS. These capacitors provide reliable performance in harsh automotive environments. The demand for autonomous vehicles is rising in North America due to the increased focus on automotive safety, the rise in demand for comfort features in a vehicle, and a growing desire of vehicle owners to reduce the amount of human error in case of accidents.

Favorable government incentives and subsidies are expected to increase the demand for EVs in the United States

- The United States captured the largest market share of 56.69%, followed closely by others with 43.31% in terms of volume in 2022.

- The United States is one of the most significant markets for MLCC. The country is one of the pioneers of advanced automotive, especially electric vehicles and autonomous technology. Most major companies in end-user applications of MLCCs are based in the United States, making the country a major target for MLCC manufacturers. As most of these companies are advancing their product offerings, the deployment of the number of MLCCs is increasing. This is likely to make the United States one of the significant markets for MLCC over the forecast period.

- Canada's vision to combat environmental concerns is a major factor in the development of the electric vehicles and energy storage systems market, which is further creating an opportunity for the vendors in the market studied. Canada signed a new international alliance to switch to electric cars. The country also offers a massive market for high-end electronic devices, mainly due to the high adoption rate of digital technologies. According to the Entertainment Software Association of Canada (ESAC), the gaming industry in Canada is booming, increasing the penetration of high-end devices in the country. These key factors are fueling the demand for MLCCs.

North America MLCC Market Trends

The development of the e-commerce industry is expected to propel light commercial vehicles

- The pandemic resulted in lockdowns and other restrictions that caused supply chain issues in the light commercial vehicle industry that had never been seen before. The pandemic caused unprecedented levels and types of mobility and travel limitations worldwide. The end-user industries that transport goods, such as infrastructure, transportation, and logistics, have completely shut down, posing new challenges for the manufacturing and freight industries. The light commercial vehicle (LCV) market is driven by the growth of North America's e-commerce sector and logistics. As the number of people with internet access and access to smartphones increases, so does the number of online retail outlets. As a result, the demand for light commercial vehicles is expected to increase, facilitating the timely delivery of products to customers.

- Canada established GHG emission caps for new light-duty vehicles by Passenger Automobile and Light Truck Greenhouse Gas Emission Regulations. The expansion of the logistics and e-commerce sectors is expected to increase the demand for LCVs. Due to rising urbanization, the market for light commercial vehicles (LCVs) is expanding with the development of new retail and e-commerce platforms that require effective logistics. The rising popularity of BEVs, the introduction of new EV models, and the development of charging infrastructure are the primary factors driving the market's growth.

The growing awareness of driver assistance systems is creating demand

- The passenger car market in North America experienced tremendous growth, with a production of 2.97 million units in 2019. The United States is the third-largest producer of electric vehicles in the world. The shift to EVs has continued at its current rate, owing to government initiatives to promote EV growth.

- The COVID-19 pandemic hindered the growth of the market, as there was a disruption in the production of vehicles due to the collapse of supply chains across the world. However, the market is expected to witness significant growth during the forecast period due to increasing awareness about the positive environmental impacts of electric vehicles and various initiatives by governments of different countries.

- Several OEMs became interested in increasing their production capacity to meet the growing demand for electric vehicles. The government policy banning ICE engines helped boost the sales of electric vehicles. The increase in the price of gasoline and diesel due to various global reasons has made it easy for EV companies to boost their sales. Electric car sales in the United States, the third largest market, increased by 55% in 2022, reaching a sales share of 8%.

- In May 2019, the federal government launched the Incentives for Zero-Emission Vehicles (iZEV) Program. The incentive-based initiative aims to help Canadians and Canadian businesses purchase or lease zero-emission vehicles. In 2022, the Canadian federal government announced a sales mandate for zero-emission vehicles. With the aim that at least 20% of new passenger vehicles sold in Canada must be zero-emission vehicles by 2026. That will increase to 60% by 2030 and jump to 100% by 2035.

North America MLCC Industry Overview

The North America MLCC Market is moderately consolidated, with the top five companies occupying 41.61%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd and Yageo Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Price Trend

- 4.1.1 Silver Price Trend

- 4.1.2 Zinc Price Trend

- 4.2 Consumer Electronics Sales

- 4.2.1 Air Conditioner Sales

- 4.2.2 Desktop PC's Sales

- 4.2.3 Gaming Console Sales

- 4.2.4 Laptops Sales

- 4.2.5 Refrigerator Sales

- 4.2.6 Smartphones Sales

- 4.2.7 Storage Unit Sales

- 4.2.8 Tablets Sales

- 4.2.9 Television Sales

- 4.3 Automotive Production

- 4.3.1 Heavy Trucks Production

- 4.3.2 Light Commercial Vehicles Production

- 4.3.3 Passenger Vehicles Production

- 4.3.4 Total Motor Production

- 4.4 Industrial Automation Sales

- 4.4.1 Industrial Robots Sales

- 4.4.2 Service Robots Sales

- 4.5 Regulatory Framework

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Others

- 5.3 Voltage

- 5.3.1 500V to 1000V

- 5.3.2 Less than 500V

- 5.3.3 More than 1000V

- 5.4 Capacitance

- 5.4.1 100µF to 1000µF

- 5.4.2 Less than 100µF

- 5.4.3 More than 1000µF

- 5.5 Mlcc Mounting Type

- 5.5.1 Metal Cap

- 5.5.2 Radial Lead

- 5.5.3 Surface Mount

- 5.6 End User

- 5.6.1 Aerospace and Defence

- 5.6.2 Automotive

- 5.6.3 Consumer Electronics

- 5.6.4 Industrial

- 5.6.5 Medical Devices

- 5.6.6 Power and Utilities

- 5.6.7 Telecommunication

- 5.6.8 Others

- 5.7 Country

- 5.7.1 United States

- 5.7.2 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 306 Pages

- 納期

- 2~3営業日