アジア太平洋のMLCC:市場シェア分析、産業動向、成長予測(2025年~2030年)

Asia-Pacific MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 318 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684034

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

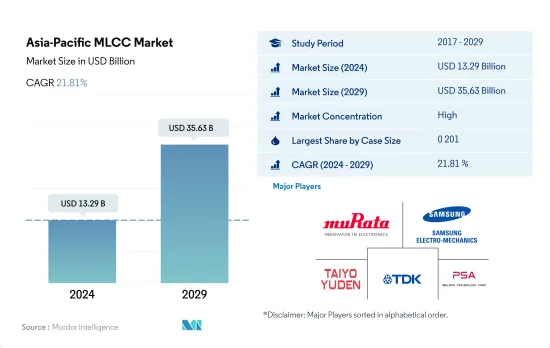

アジア太平洋のMLCC市場規模は、2024年に132億9,000万米ドルと推定され、2029年には356億3,000万米ドルに達すると予測され、予測期間(2024年~2029年)のCAGRは21.81%で成長します。

0 201 MLCCの需要を牽引しているのは、同地域における民生用電子機器と医療機器の需要拡大です。

- 0 201がトップランナーに浮上し、2022年の数量ベースで46.85%の最大市場シェアを獲得、僅差で1 005の16.20%、0 402の12.01%が続きます。

- クラス1に分類される誘電体は、C0G、X8G、U2Jに分けられます。中低域の静電容量を持つC0G MLCCは、スマートフォンやスマートウォッチなどの民生用電子機器業界において、スマートなデザインを実現するための小型化傾向の高まりにより、特に人気が高まっています。

- クラス2の誘電体MLCCは、X7R、X5R、Y5Vに分類されます。これらの誘電体は、高電圧条件に耐える能力があり、自動運転支援システム(ADAS)、インフォテインメントシステム、バッテリ貯蔵能力の向上などの機能の進歩により、車載アプリケーションに理想的な選択肢となっています。

インセンティブや割引が電気自動車需要の増加を後押ししているほか、拡張現実(AR)や仮想現実(VR)などの家電製品の開発もMLCCの需要を押し上げています。

- 2022年には、中国がトップランナーに浮上し、24.79%の最大市場シェアを獲得し、金額ベースでは韓国の20.31%、日本の12.27%が僅差で続いた。

- 中国のコンシューマー・エレクトロニクス製造業は、世界的に見ても最も著名な産業のひとつです。5Gネットワークの導入、スマートホームの普及、拡張現実(AR)および仮想現実(VR)技術、機能を向上させた家電機器の絶え間ない進化によって、中国の家電市場は今後急成長を遂げることが予想されます。その結果、100uF未満の低キャパシタンスで0201ケースサイズの表面実装型積層セラミックコンデンサMLCCに対するニーズも、それに伴って増加すると予想されます。インセンティブや割引が電気自動車の需要増加を後押しし、拡張現実や仮想現実などの民生用電子機器の開発がMLCCの需要を押し上げています。

- 自動車産業は急速な技術開発期にあり、それがMLCCの需要増加につながっています。一般に、自動運転機能を持たないエンジン駆動の自動車には約3,000個のMLCCが必要であるのに対し、電気自動車には8,000~1万個のMLCCが必要となります。自動車部門はインドの経済成長に大きく貢献しており、現状を示すベンチマークと見なすことができます。さらに、インド政府の規制、インセンティブ、割引、e-モビリティに関する認識が、消費者を電気自動車の購入に向かわせ、MLCCの需要を押し上げています。

アジア太平洋のMLCC市場動向

eコマース産業の開発が市場を促進する見込み

- 小型商用車の生産台数は、2019年の525万台から2022年には523万台へと拡大すると予想されます。

- オンライン商取引と物流分野が小型商用車市場を支えます。携帯電話とインターネットへのアクセスの増加により、オンライン小売販売とeコマースが増加しています。商用車の販売は、顧客への商品のタイムリーな配達を改善するために増加すると予想されます。

- COVID-19オンライン販売の結果、世界のeコマース市場のユーザーベースと収入は大幅に拡大しました。2020年に個人によるオンラインショッピングが最も増加したのは、パンデミックによって個人がオンラインショッピングを余儀なくされたためです。しかし、アジア太平洋の小型商用車は、現地当局による電子商取引と旅行に対する厳しい規制のため、2020年の生産台数が前年比11.17%減少しました。

- 小型商用車の生産は、各国政府が小型商用車の電動化に率先して取り組んでいるため、着実に回復しています。地域の主要企業は、電気トラックの開発・製造に共同で取り組んでいます。

電気自動車の採用台数の増加が需要を高めると予想されます。

- 乗用車生産台数は、2019年の4,065万台から2022年には4,232万台へと成長し、期間中のCAGRは1.35%を記録すると予想されます。

- 2020年の乗用車セクターの生産台数は前年比11.88%減となりました。パンデミックとロシア・ウクライナ戦争は世界中のサプライチェーンに大きな影響を与え、乗用車の生産を減速させ、メーカーは生産ラインの一時閉鎖を余儀なくされました。インフレなどの経済課題は、人々が自動車などの大きな買い物を先延ばしにしているため、需要に影響を与えました。しかし、市場は緩やかながらも着実に回復し、2022年の生産台数は前年比10.83%増となりました。

- CO2排出に関する政府政策の変化により、燃料ベースの乗用車需要は徐々に減少しています。各地域の政府は、2030年までに温室効果ガス排出量を削減し、2050年までにネットゼロ排出量を達成することに注力しています。この需要を満たすため、公開会社や政府はハイブリッド車や電気自動車の導入に力を入れており、充電インフラを公共施設に直接設置したり、家庭や職場の自家用充電ステーションに補助金を出して間接的に設置したりしています。アジア太平洋諸国では、欧米諸国と比較して電気自動車の販売台数が高い伸びを示しています。過去10年間、この地域ではBEVの販売台数が大幅に増加しています。

- 前述の要因や開発により、乗用車の生産において予測技術の採用が増加しており、このような前向きな動向は予測期間中、これらの自動車に使用されるMLCCの成長を促進すると予想されます。

アジア太平洋のMLCC産業の概要

アジア太平洋のMLCC市場はかなり統合されており、上位5社で72.07%を占めています。この市場の主要企業は以下の通り。 Murata Manufacturing, Samsung Electro-Mechanics, Taiyo Yuden, TDK Corporation and Walsin Technology Corporation(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 家電販売

- エアコン販売台数

- デスクトップPC販売台数

- ゲーム機販売台数

- ノートパソコン販売台数

- 冷蔵庫販売

- スマートフォン販売

- 収納機器販売

- タブレット販売

- テレビ販売

- 自動車生産

- バス生産

- 大型トラック生産

- 小型商用車生産

- 乗用車生産

- 自動車生産

- 産業用オートメーション売上高

- 産業用ロボット販売

- サービスロボット販売

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 誘電体タイプ

- クラス1

- クラス2

- ケースサイズ

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- その他

- 電圧

- 500V~1000V

- 500V未満

- 1000V以上

- 静電容量

- 100uF~1,000uF

- 100uF未満

- 1000uF以上

- Mlcc実装タイプ

- 金属キャップ

- ラジアルリード

- 表面実装

- エンドユーザー

- 航空宇宙および防衛

- 自動車

- 民生用電子機器

- 産業機器

- 医療機器

- 電力・公益事業

- 通信機器

- その他

- 国名

- 中国

- インド

- 日本

- 韓国

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co ltd

- Murata Manufacturing Co., Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co., Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The Asia-Pacific MLCC Market size is estimated at 13.29 billion USD in 2024, and is expected to reach 35.63 billion USD by 2029, growing at a CAGR of 21.81% during the forecast period (2024-2029).

The demand for 0 201 MLCCs is driven by the growing demand for consumer electronics and medical equipment in the region

- 0 201 emerged as the frontrunner, capturing the largest market share of 46.85%, followed closely by 1 005 with 16.20% and 0 402 with 12.01% in terms of volume in 2022.

- Dielectrics classified as Class 1 can be divided into C0G, X8G, and U2J. The C0G MLCCs with low-mid range capacitance are becoming increasingly popular in the consumer electronic electronics industry, particularly in smartphones, smartwatches, and other devices, due to the increasing trend toward miniaturization in order to achieve sleeker designs.

- Class 2 dielectric MLCCs are classified into X7R, X5R, and Y5V. These dielectrics are an ideal choice for automotive applications due to their ability to withstand high-voltage conditions and the advancement of features such as Automatic Driver Assistance Systems (ADAS), infotainment systems, and improved battery storage capabilities.

Incentives and discounts are driving the increasing demand for electric vehicles, along with the development of consumer electronics such as augmented reality and virtual reality, which is propelling MLCC demand

- In 2022, China emerged as the frontrunner, capturing the largest market share of 24.79%, followed closely by South Korea with 20.31% and Japan with 12.27% in terms of value.

- The Chinese consumer electronics manufacturing industry is one of the most prominent globally. It is anticipated that the Chinese consumer electronics market will experience rapid growth in the future, driven by the introduction of 5G networks, the proliferation of smart homes, augmented and virtual reality technologies, and the continuous evolution of consumer electronic devices with improved features. As a result, the need for installed multi-layer ceramic capacitors MLCCs of surface mount type with 0201 case sizes with low capacitance of less than 100uF is expected to increase accordingly. Incentives and discounts drive the increasing demand for electric vehicles, and the development of consumer electronics such as augmented reality and virtual reality is propelling the MLCC demand.

- The automotive industry is undergoing a period of rapid technological development, which is leading to an increase in the demand for MLCCs. Generally, an engine-driven vehicle without an automated driving feature requires approximately 3,000 MLCCs, while an electric vehicle requires between 8,000 and 10,000 MLCCs. The automotive sector is a major contributor to India's economic growth and can be seen as a benchmark for the current situation. Additionally, Indian government regulations, incentives, discounts, and awareness about e-mobility are driving consumers toward the purchase of electric vehicles, driving the demand for MLCCs.

Asia-Pacific MLCC Market Trends

Development of the E-commerce industry is expected to propel the market

- The light commercial vehicle production was expected to grow from 5.25 million units in 2019 to 5.23 million units in 2022.

- The online commerce and logistics sectors support the market for light commercial vehicles. Owing to increased access to mobile phones and the Internet, there has been an increase in online retail sales and e-commerce. Commercial vehicle sales are expected to increase to improve the timely delivery of goods to clients.

- As a result of COVID-19 online sales, the user base and income of the global e-commerce market greatly expanded. The highest increase in online shopping by individuals in 2020 was caused by the pandemic, which forced individuals to shop online. However, the Asia-Pacific light commercial vehicles witnessed a YoY drop of 11.17% in production in 2020 because of stringent restrictions on e-commerce and travel imposed by the local authorities.

- The production of light commercial vehicles is recovering steadily as governments are taking the initiative to electrify these vehicles. Major regional players are collaborating to develop and manufacture electric trucks.

The rising adoption of electric vehicles is expected to enhance the demand

- The passenger vehicle production was expected to grow from 40.65 million units in 2019 to 42.32 million units in 2022, registering a CAGR of 1.35% during the period.

- The passenger car sector witnessed a drop of 11.88% YoY production in 2020. The pandemic and the Russia-Ukraine war heavily impacted supply chains across the globe, slowing down the production of passenger cars and forcing manufacturers to close production lines temporarily. Economic challenges such as inflation affected demand, as people are postponing large purchases such as cars. However, the market witnessed a slow but steady recovery, with a YoY production growth of 10.83% in 2022.

- The demand for fuel-based passenger vehicles is slowly reducing due to changing government policies concerning CO2 emissions. Governments across the regions are focusing on reducing greenhouse gas emissions by 2030 and achieving net-zero emissions by 2050. To meet this demand, companies and governments are focusing on introducing hybrid or electric cars and installing charging infrastructures directly at public outlets or indirectly through subsidies for private car charging stations in homes and workplaces. Asia-Pacific countries are exhibiting higher growth in the sales of electric vehicles compared to their Western competitors. In the last decade, there has been a significant increase in BEV sales in this region.

- Owing to the aforementioned factors and developments, the adoption of predictive technologies is increasing in the production of passenger vehicles, and such positive trends are expected to enhance the growth of the MLCCs used in these vehicles during the forecast period.

Asia-Pacific MLCC Industry Overview

The Asia-Pacific MLCC Market is fairly consolidated, with the top five companies occupying 72.07%. The major players in this market are Murata Manufacturing Co., Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co., Ltd, TDK Corporation and Walsin Technology Corporation (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Consumer Electronics Sales

- 4.1.1 Air Conditioner Sales

- 4.1.2 Desktop PC's Sales

- 4.1.3 Gaming Console Sales

- 4.1.4 Laptops Sales

- 4.1.5 Refrigerator Sales

- 4.1.6 Smartphones Sales

- 4.1.7 Storage Unit Sales

- 4.1.8 Tablets Sales

- 4.1.9 Television Sales

- 4.2 Automotive Production

- 4.2.1 Buses and Coaches Production

- 4.2.2 Heavy Trucks Production

- 4.2.3 Light Commercial Vehicles Production

- 4.2.4 Passenger Vehicles Production

- 4.2.5 Total Motor Production

- 4.3 Industrial Automation Sales

- 4.3.1 Industrial Robots Sales

- 4.3.2 Service Robots Sales

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Others

- 5.3 Voltage

- 5.3.1 500V to 1000V

- 5.3.2 Less than 500V

- 5.3.3 More than 1000V

- 5.4 Capacitance

- 5.4.1 100µF to 1000µF

- 5.4.2 Less than 100µF

- 5.4.3 More than 1000µF

- 5.5 Mlcc Mounting Type

- 5.5.1 Metal Cap

- 5.5.2 Radial Lead

- 5.5.3 Surface Mount

- 5.6 End User

- 5.6.1 Aerospace and Defence

- 5.6.2 Automotive

- 5.6.3 Consumer Electronics

- 5.6.4 Industrial

- 5.6.5 Medical Devices

- 5.6.6 Power and Utilities

- 5.6.7 Telecommunication

- 5.6.8 Others

- 5.7 Country

- 5.7.1 China

- 5.7.2 India

- 5.7.3 Japan

- 5.7.4 South Korea

- 5.7.5 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co ltd

- 6.4.3 Murata Manufacturing Co., Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co., Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 318 Pages

- 納期

- 2~3営業日