中国のMLCCの市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

China MLCC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 291 Pages

- 納期

- 2~3営業日

- 商品コード

- 1684035

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

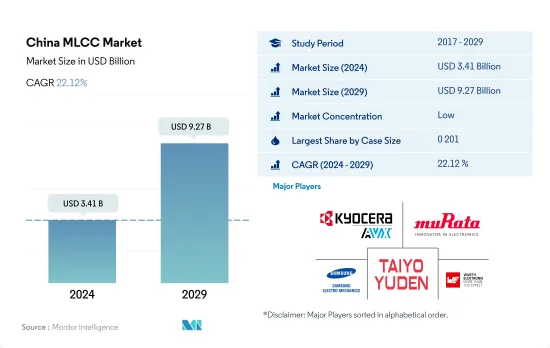

中国のMLCC市場規模は2024年に34億1,000万米ドルと推定・予測され、2029年には92億7,000万米ドルに達し、予測期間(2024年~2029年)のCAGRは22.12%で成長すると予測されます。

ケースサイズダイナミクスと市場成長予測を通じた中国のMLCC市場の繁栄

- 中国のダイナミックなMLCC市場において、0 201ケースサイズセグメントは2022年に数量市場シェアの41.33%を占め、2029年までに35億1,000万米ドルの収益を生み出す見通しです。これらの小型MLCCは極めて重要な部品であり、ウェアラブル、医療機器、IoT機器などの小型電子機器に幅広く使用されています。高密度実装されたPCBレイアウトの中でその卓越した性能は、効率を損なうことなくシームレスな統合を保証します。中国が世界の5G市場を席巻する準備を進める中、0 201 MLCCの需要は、特にコンパクトなフォームファクターが重要な5G対応スマートフォンで急増すると予想されます。

- 0.402ケースサイズのセグメントは、2022年の数量ベースで市場シェアの23.82%を占め、2029年までに20億6,000万米ドルをもたらすと予測されています。長さ0.040インチ、幅0.020インチのコンパクトな部品は、スマートフォン、タブレット、ノートパソコン、ゲーム機などの家電製品に使用されています。

- 中国の0 603ケース・サイズ・セグメントは、2022年の数量市場で18.78%のシェアを占め、2029年までに17億1,000万米ドルの売上が見込まれます。これらのMLCCは長さ0.06インチ、幅0.03インチで、手作業に便利で、識別のしやすさ、手作業でのはんだ付けに利点があります。

- 1 210ケースサイズのセグメントは、2022年の数量市場シェアの16.07%を占め、2029年には9億5,660万米ドルが予測されます。中国の電気自動車市場の成長と高度なスマートフォン技術が、これらのMLCCの必要性を高めており、信頼できる性能を確保し、最新の機能性をサポートしています。

中国のMLCC市場動向

eコマース産業の開発が小型商用車の需要を促進する見込み

- 中国市場の小型軽自動車セグメントであるピックアップは、その使用に関する規制を緩和する政府が増えるにつれて力強い成長が見込まれます。2019年の小型商用車の総生産台数は200万台、国内の小型トラックの販売台数は190万台に達し、継続的な成長を達成しています。

- 小型トラックの販売台数は過去2年間、順調に伸びています。国が低速トラックの製品区分を取り消し、国内のeコマースエクスプレス物流とコールドチェーン輸送の急速な開発により、軽トラックの市場需要は増加し続け、2020年の前年比成長率は7.44%に達しました。中国の軽トラックメーカーは複雑な使用環境に対応するため、関連製品を適宜設計しました。

- 2022年には、中国が電動LCV全体の販売台数で首位に立ち、販売台数は1億3,000万台を超え、LCV販売台数の15%近くが電動となりました。バッテリー電気トラックや燃料電池トラック、職業用車両(LCVを含む)に対する補助金は近年減少しているが、ゼロエミッション商用トラックの販売台数は、1台当たりの補助金が減少しているにもかかわらず、2020年以降増加しており、電気トラックの商業競争力が高まっていることを示しています。国内の速達・物流産業の継続的な発展に伴い、小型トラック全体の販売需要は中長期的に成長傾向を維持すると予想されます。

急速な都市化と先進的な車両技術により、乗用車の需要が増加すると予想される

- 中国は最も急成長している自動車産業の1つであり、OEM(相手先ブランド製造)の主要な存在感を世界的に占めています。乗用車は中国自動車産業の主要セグメントであり、2019年には2,138万台が生産されました。可処分所得の増加、急速な都市化、低層都市からの新車需要、車両コストの低下といった要因が、中国における乗用車の成長を後押ししています。

- 2021年に中国で販売された電気自動車(330万台)は、2020年の世界販売台数(300万台)を上回りました。中国の電気自動車保有台数は2021年に780万台と世界最大を維持し、これはCOVID-19大流行前の2019年のストックの2倍以上でした。2021年には270万台以上のBEVが中国で販売され、電気自動車の新車販売の82%を占めました。

- 2021年の国内自動車販売に占める電気自動車の割合は、2020年の5%から16%に増加し、2021年12月には月間シェア20%に達しました。この目覚ましい成長は、第14次5カ年計画(FYP)(2021~2025年)で脱炭素化を加速させる政府の取り組みと同時に実現したもので、過去数年のFYP期間中、EV市場に対する政策支援を段階的に強化してきた傾向が続いています。現在のFYPには、2025年に電気自動車の販売シェアを年平均20%にするといった運輸分野の中期目標が盛り込まれています。

- 厳しい排ガス規制、変動する燃料価格、環境に優しい交通機関に対する顧客からの需要の高まりにより、乗用車の生産台数は2022年に前年比11.15%増となり、この成長は今後も続くと予想されます。

中国のMLCC産業の概要

中国のMLCC市場は細分化されており、上位5社で0%を占めています。この市場の主要企業は以下の通り。 Kyocera AVX Components Corporation(Kyocera Corporation), Murata Manufacturing, Samsung Electro-Mechanics, Taiyo Yuden and Wurth Elektronik GmbH & Co. KG(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 価格動向

- 銅の価格動向

- ニッケル価格動向

- 銀価格動向

- 家電販売台数

- エアコン販売台数

- デスクトップPC販売台数

- ゲーム機販売

- ノートパソコン販売

- 冷蔵庫販売

- スマートフォン販売

- 収納機器販売

- タブレット販売

- テレビ販売

- 自動車生産

- バス生産

- 大型トラック生産

- 小型商用車生産

- 乗用車生産

- 自動車生産台数

- EV生産

- BEV(バッテリー電気自動車)の生産

- PHEV(プラグインハイブリッド車)生産台数

- 産業用オートメーション売上高

- 産業用ロボット販売

- サービスロボット販売

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 誘電体タイプ

- クラス1

- クラス2

- ケースサイズ

- 0 201

- 0 402

- 0 603

- 1 005

- 1 210

- その他

- 電圧

- 500V~1000V

- 500V未満

- 1000V以上

- 静電容量

- 100uF~1000uF

- 100uF未満

- 1,000uF以上

- Mlcc実装タイプ

- 金属キャップ

- ラジアルリード

- 表面実装

- エンドユーザー

- 航空宇宙および防衛

- 自動車

- 民生用電子機器

- 産業機器

- 医療機器

- 電力・公益事業

- 通信機器

- その他

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Kyocera AVX Components Corporation(Kyocera Corporation)

- Maruwa Co. Ltd

- Murata Manufacturing Co. Ltd

- Nippon Chemi-Con Corporation

- Samsung Electro-Mechanics

- Samwha Capacitor Group

- Taiyo Yuden Co. Ltd

- TDK Corporation

- Vishay Intertechnology Inc.

- Walsin Technology Corporation

- Wurth Elektronik GmbH & Co. KG

- Yageo Corporation

第7章 CEOへの主な戦略的質問CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界・バリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

The China MLCC Market size is estimated at 3.41 billion USD in 2024, and is expected to reach 9.27 billion USD by 2029, growing at a CAGR of 22.12% during the forecast period (2024-2029).

China's thriving MLCC market through case size dynamics and market growth projections

- In China's dynamic MLCC market, the 0 201 case size segment held a substantial 41.33% of the volume market share in 2022, and it's poised to generate a revenue of USD 3.51 billion by 2029. These miniature MLCCs are pivotal components, finding extensive use in small electronic devices like wearables, medical equipment, and IoT devices. Their remarkable performance within densely populated PCB layouts ensures seamless integration without compromising efficiency. As China gears up to dominate the global 5G market, the demand for 0 201 MLCCs is expected to soar, especially in 5G-enabled smartphones, where compact form factors are crucial.

- The 0 402 case size segment, representing 23.82% of the market share by volume in 2022, is projected to yield USD 2.06 billion by 2029. These compact components, measuring 0.040 inches in length and 0.020 inches in width, are the go-to for consumer electronics, including smartphones, tablets, laptops, and gaming consoles.

- China's 0 603 case size segment, with a 18.78% share of the volume market in 2022, is expected to generate USD 1.71 billion by 2029. These MLCCs, measuring 0.06 inches in length and 0.03 inches in width, are convenient to work with manually, providing advantages in ease of identification and hand soldering.

- The 1 210 case size segment, accounting for 16.07% of the volume market share in 2022 and projecting USD 956.60 million by 2029, offers precise measurements that are crucial for optimal integration on circuit boards and electronic devices. The growth in China's electric vehicle market and advanced smartphone technologies are driving the need for these MLCCs, ensuring dependable performance and supporting modern functionalities.

China MLCC Market Trends

The development of the e-commerce industry is expected to propel the demand for light commercial vehicles

- Pickups, a small light-vehicle segment in the Chinese market, are poised for robust growth as more governments relax rules over their use. The total production of light commercial vehicles in 2019 was 2 million units, and the sales volume of light trucks in the country reached 1.9 million units, achieving continuous growth.

- The sales of light trucks have grown steadily in the past two years. Due to the country canceling the product category of low-speed trucks and the rapid development of domestic e-commerce express logistics and cold chain transportation, the market demand for light trucks continued to increase, with a Y-o-Y growth of 7.44% in 2020. Chinese light truck manufacturers designed their related products accordingly to cope with the complex usage environment.

- In 2022, China led in terms of overall electric LCV sales, with over 130 million units sold and nearly 15% of LCVs sold being electric. Subsidies for battery electric and fuel cell trucks and vocational vehicles (including LCVs) have decreased in recent years, but zero-emission commercial truck sales have been growing since 2020, even as subsidies per vehicle have declined, indicating the increasing commercial competitiveness of electric trucks. With the continuous development of the country's express delivery and logistics industry, the overall light truck sales demand is expected to maintain a growth trend in the medium and long term.

Rapid urbanization and advanced vehicle technology are expected to increase the demand for passenger vehicles

- China has one of the fastest-growing auto industries and accounts for a major presence of original equipment manufacturers (OEMs) globally. Passenger cars were a key segment of the Chinese automotive industry, producing 21.38 million units in 2019. Factors such as increasing disposable income, rapid urbanization, demand for new cars from lower-tier cities, and low vehicle costs are driving the growth of passenger vehicles in China.

- More electric cars were sold in China in 2021 (3.3 million) than in the world in 2020 (3.0 million). China's fleet of electric cars remained the world's largest at 7.8 million in 2021, which was more than double the stock of 2019 before the COVID-19 pandemic. Over 2.7 million BEVs were sold in China in 2021, accounting for 82% of new electric car sales.

- Electric cars accounted for 16% of domestic car sales in 2021, up from 5% in 2020, and reached a monthly share of 20% in December 2021, reflecting a much quicker recovery of the EV market relative to conventional cars. This impressive growth came alongside government efforts to accelerate decarbonization in the new 14th Five-Year Plan (FYP) (2021-2025), continuing the trend of progressively strengthening policy support for EV markets in the past few FYP periods. The current FYP includes medium-term objectives in transport, such as reaching an annual average of 20% market share for electric car sales in 2025.

- Stringent emission norms, fluctuating fuel prices, and the growing demand from customers for eco-friendly transportation caused the production of passenger vehicles to witness a Y-o-Y growth of 11.15% in 2022, and this growth is expected to continue in the future.

China MLCC Industry Overview

The China MLCC Market is fragmented, with the top five companies occupying 0%. The major players in this market are Kyocera AVX Components Corporation (Kyocera Corporation), Murata Manufacturing Co. Ltd, Samsung Electro-Mechanics, Taiyo Yuden Co. Ltd and Wurth Elektronik GmbH & Co. KG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Price Trend

- 4.1.1 Copper Price Trend

- 4.1.2 Nickel Price Trend

- 4.1.3 Silver Price Trend

- 4.2 Consumer Electronics Sales

- 4.2.1 Air Conditioner Sales

- 4.2.2 Desktop PC's Sales

- 4.2.3 Gaming Console Sales

- 4.2.4 Laptops Sales

- 4.2.5 Refrigerator Sales

- 4.2.6 Smartphones Sales

- 4.2.7 Storage Unit Sales

- 4.2.8 Tablets Sales

- 4.2.9 Television Sales

- 4.3 Automotive Production

- 4.3.1 Buses and Coaches Production

- 4.3.2 Heavy Trucks Production

- 4.3.3 Light Commercial Vehicles Production

- 4.3.4 Passenger Vehicles Production

- 4.3.5 Total Motor Production

- 4.4 EV Production

- 4.4.1 BEV (Battery Electric Vehicle) Production

- 4.4.2 PHEV (Plug-in Hybrid Electric Vehicle) Production

- 4.5 Industrial Automation Sales

- 4.5.1 Industrial Robots Sales

- 4.5.2 Service Robots Sales

- 4.6 Regulatory Framework

- 4.7 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Others

- 5.3 Voltage

- 5.3.1 500V to 1000V

- 5.3.2 Less than 500V

- 5.3.3 More than 1000V

- 5.4 Capacitance

- 5.4.1 100µF to 1000µF

- 5.4.2 Less than 100µF

- 5.4.3 More than 1000µF

- 5.5 Mlcc Mounting Type

- 5.5.1 Metal Cap

- 5.5.2 Radial Lead

- 5.5.3 Surface Mount

- 5.6 End User

- 5.6.1 Aerospace and Defence

- 5.6.2 Automotive

- 5.6.3 Consumer Electronics

- 5.6.4 Industrial

- 5.6.5 Medical Devices

- 5.6.6 Power and Utilities

- 5.6.7 Telecommunication

- 5.6.8 Others

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Kyocera AVX Components Corporation (Kyocera Corporation)

- 6.4.2 Maruwa Co. Ltd

- 6.4.3 Murata Manufacturing Co. Ltd

- 6.4.4 Nippon Chemi-Con Corporation

- 6.4.5 Samsung Electro-Mechanics

- 6.4.6 Samwha Capacitor Group

- 6.4.7 Taiyo Yuden Co. Ltd

- 6.4.8 TDK Corporation

- 6.4.9 Vishay Intertechnology Inc.

- 6.4.10 Walsin Technology Corporation

- 6.4.11 Wurth Elektronik GmbH & Co. KG

- 6.4.12 Yageo Corporation

7 KEY STRATEGIC QUESTIONS FOR MLCC CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 291 Pages

- 納期

- 2~3営業日