|

市場調査レポート

商品コード

1910903

北米のゲーミング市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)North America Gaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のゲーミング市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

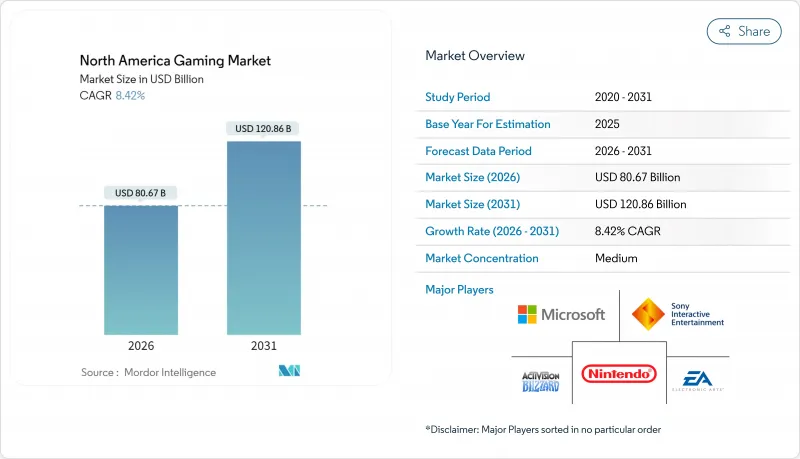

2026年の北米のゲーム市場規模は806億7,000万米ドルと推定され、2025年の744億米ドルから成長が見込まれます。

2031年までの予測では1,208億6,000万米ドルに達し、2026年から2031年にかけてCAGR8.42%で拡大する見通しです。

動的な価格帯別サブスクリプション、AIによるアプリ内購入の誘導、AAAタイトルのクラウド配信が相まって、プラットフォーム横断でのユーザー1人あたりの平均収益(ARPU)を押し上げております。クラウドインフラはハードウェアの障壁を取り除き、スマートフォンや低スペックPCでもコンソール品質の体験を可能にしております。一方、クロスプラットフォームエンジンは開発サイクルを短縮し、対象となるユーザー層を拡大しております。基本プレイ無料のマイクロトランザクションとプレミアムサブスクリプションの相互作用が、マクロ経済の逆風から業界を保護し、プレイヤー支出の二桁成長を持続させております。従来型コンソールメーカー、モバイルファーストパブリッシャー、クラウドゲートキーパーがエコシステム支配権を争う中、競合は激化しております。各社はAIを活用し、獲得コスト削減とプレイヤー生涯価値の最大化を図っております。

北米のゲーム市場の動向と洞察

モバイルファースト型カジュアルゲームの支出急増

パーソナライズされたアプリ内課金アルゴリズムは、バナー広告の3倍以上のコンバージョン率を実現し、カジュアルモバイルタイトルを北米のゲーム市場の成長エンジンとして再定義しています。UnityのVector AIは、毎日数十億のデータポイントを活用して購買傾向を予測し、リアルタイムで入札価格を設定するため、開発者は広告費の拡大なしに収益化が可能となります。広告を排除し、装飾アイテムを解放するサブスクリプションオプションは、摩擦のないプレイを重視するカジュアルユーザー層に支持を集めています。メッセージングやインフルエンサープラットフォームとのソーシャルレイヤー統合は、増加する有料獲得コストを相殺するバイラルリーチを提供します。

サブスクリプションサービス:価格帯の積み重ねによるARPU向上

サブスクリプションカタログは、定額制からユーザーエンゲージメントやデバイスアクセスに応じた複数階層の価格体系へと移行しています。Xbox Game Passはこの動向を体現しており、コンソール専用、PC専用、クロスプラットフォーム対応のバンドルを提供し、明確な支払い意思の閾値をターゲットにしています。パブリッシャーはゲームプレイテレメトリを分析し、弾力的な価格設定をテスト。エンゲージメントがピークに達したタイミングでアップグレードを促すことで、解約率を最小限に抑えています。プレミアム層に組み込まれたクラウドストリーミングはハードウェアの障壁を取り除き、離脱したコンソール所有者を再び消費ファネルに引き戻します。

ハードウェア更新の低迷:パンデミック後の景気減速とマクロ経済の逆風

パンデミック後の需要急増後、コンソールとGPUの需要は鈍化しました。マイクロソフトは、世帯のアップグレード延期によりXboxハードウェア収益が13%減少したと報告しています。アップグレードサイクルの停滞は、プレミアムソフトウェアや周辺機器の付属率低下へと波及し、短期的な成長を抑制しています。クラウドゲーミングはハードウェア依存を軽減しますが、遅延への懸念からコアユーザーはローカル性能に依存し続け、代替手段としての普及は限定的です。

セグメント分析

モバイルタイトルは2025年収益の48.75%を占め、北米のゲーム市場の基幹セグメントとなっています。クラウドゲーミングは2031年までCAGR9.72%が見込まれ、ハイパースケールエッジノードが60fpsのゲームプレイをブラウザや低スペック端末へストリーミングすることで実現されます。北米のゲーム市場におけるモバイルの規模は2031年までに603億5,000万米ドルを超えると予測される一方、クラウドのシェアは同期間に2倍以上拡大する見込みです。5Gのカバー範囲が拡大するにつれ、ユーザーはローカルプレイとストリーミングプレイを切り替え、クロスセーブ機能によりデバイス間で進行状況を維持します。コンソールメーカーは現在、顧客層の拡大を図るためクラウド拡張機能を導入し、PCストアフロントはライブラリの関連性を維持するためリモートプレイモジュールを統合しています。

ハイブリッドプレイパターンがコンテンツ開発計画を再構築しています。開発者はスケーラブルなアセットパイプラインを構築し、モバイルGPU向けにテクスチャ解像度を下げつつ、光回線接続ではフルスペックをストリーミングします。クロスプラットフォームエンジンは移植サイクルを短縮し、スタジオがエンドポイント間で更新や課金イベントを同期可能にします。この統合性により、北米のゲーム市場は孤立したデバイス垂直市場ではなく、エコシステムとしての基盤をさらに強固にしています。

2025年の支出の58.15%を無料プレイモデルが占め、その基盤は装飾アイテムのマイクロトランザクションとシーズンパスによって支えられています。サブスクリプション層は予測可能なキャッシュフローをもたらし、シームレスなアクセスとクラウドポータビリティを約束し、CAGR9.48%で拡大しています。シューターやRPGフランチャイズでは、顧客離脱を防ぐため、低価格サブスクリプション内にシーズンコンテンツ配信を組み込むケースが増加しています。ハイブリッド型の「フリーミアム+サブスクリプション」方式は、価格に敏感な層を疎外することなく収益化の上限を引き上げます。

高額購入層においては、映画的なシングルプレイヤー物語と連動したプレミアムボックス販売が依然として好調です。限定コレクターズエディションや予約特典により発売前の収益を確保し、ライブサービス型DLCで持続的な収益を拡大します。コンテクストターゲティングアルゴリズムによる信号損失の相殺により広告収益は回復傾向にありますが、広告充填率への依存度が高い小規模スタジオはマクロ広告サイクルの影響を受けやすい状況です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- モバイルファースト型カジュアルゲーム支出の急増

- サブスクリプションサービスは価格帯の積み重ねによりARPUを向上させております

- クロスプラットフォームエンジンとライブオペレーションツールの導入による開発サイクルの短縮

- eスポーツへのスポンサー資金流入とメディア権利の価格高騰

- クラウド/エッジインフラがハードウェアの障壁を解消し、AAA級体験を実現

- AIを活用したユーザー獲得・維持モデルがLTVを向上させます

- 市場抑制要因

- コロナ後のハードウェア更新需要の低迷とマクロ経済の逆風

- モバイルにおける獲得コストの上昇と広告シグナルの喪失

- 戦利品ボックスとデータプライバシーに関する規制当局の監視

- 人材の削減による組織的知識の喪失とリリース遅延

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 消費者の交渉力

- 競争企業間の敵対関係

- 代替品の脅威

- マクロ経済動向が市場に与える影響

第5章 市場規模と成長予測

- プラットフォーム別

- コンソールゲーム

- PCゲーム

- モバイルゲーム

- クラウドゲーミングとストリーミング

- 収益モデル別

- プレミアム(定価販売)

- 基本無料/課金制

- サブスクリプションサービス

- 広告・ゲーム内課金

- ジャンル別

- シューティングゲーム

- スポーツ

- ロールプレイング/アドベンチャー

- 戦略

- パズル&カジュアル

- カジノ・ソーシャルカジノ

- ゲーマータイプ別

- カジュアルゲーマー

- 競技志向/eスポーツプレイヤー

- コアゲーマー/ハードコアゲーマー

- ソーシャルゲーマー

- 国別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Activision Blizzard, Inc.

- Electronic Arts Inc.

- Microsoft Corporation

- Sony Interactive Entertainment LLC

- Nintendo Co., Ltd.

- Take-Two Interactive Software, Inc.

- Ubisoft Entertainment SA

- Valve Corporation

- Epic Games, Inc.

- Riot Games, Inc.

- Roblox Corporation

- Square Enix Holdings Co., Ltd.

- Bandai Namco Holdings Inc.

- NetEase, Inc.

- Tencent Holdings Ltd.(North-America studios)

- CD PROJEKT S.A.

- SEGA Corporation

- Warner Bros. Games Inc.

- Bethesda Softworks LLC

- Zynga Inc.

- Capcom Co., Ltd.