|

市場調査レポート

商品コード

1910895

ドイツのコールドチェーン物流:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Germany Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドイツのコールドチェーン物流:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

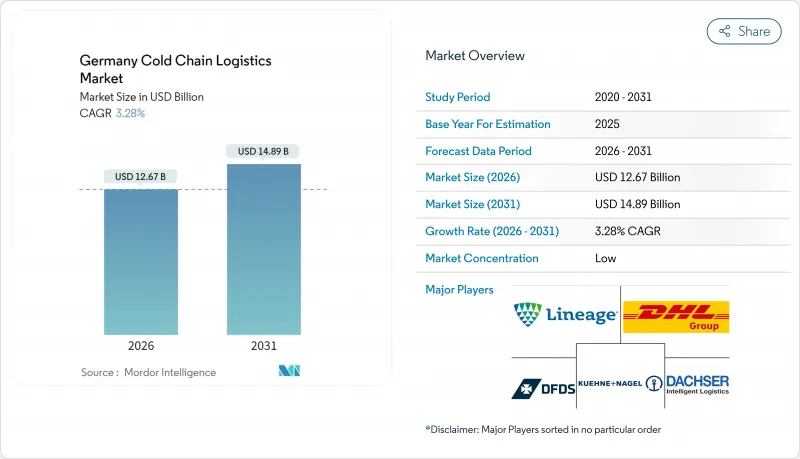

ドイツのコールドチェーン物流市場は、2025年に122億7,000万米ドルと評価され、2026年の126億7,000万米ドルから2031年までに148億9,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは3.28%と見込まれます。

堅調なEC食品需要、持続的なバイオ医薬品輸出の勢い、小売業者の自動鮮度管理プログラムへの投資が短期的な拡大を支える一方、自然冷媒への改修や電動輸送車両の導入が長期的な効率性を強化しています。既存のサードパーティ物流プロバイダーは、IoT追跡、予知保全、AI駆動のルート最適化によるネットワークのデジタル化を進め、上昇するエネルギーコストの抑制と厳格化する環境規制への対応を図っています。超低温貯蔵や統合型付加価値サービスへのポートフォリオ多様化により、顧客がエンドツーエンドのコンプライアンスソリューションを求める中で利益率が拡大しています。ドイツのコールドチェーン物流市場は、欧州貿易ルートの中心という地理的優位性と、持続可能なインフラ更新を支援する公的インセンティブの恩恵を受け続けています。

ドイツのコールドチェーン物流市場の動向と洞察

Eコマース主導のB2C食品流通拡大

オンライン生鮮食品販売額は2024年に32億米ドルに達し、2025年にはさらに15~20%増加が見込まれています。これにより小売業者や専門事業者は、2℃と常温のデュアルゾーン自動化を備えたマイクロフルフィルメントセンターを建設し、1時間あたり1,000件の注文処理を実現しています。アルディの「マイン・アルディ」やピクニックのハブモデルで採用されている電気自動車配送車両は、排出ガス削減と都市部の厳しい騒音規制への対応を実現しています。買い物かごの小型化と配送時間の短縮により、コスト構造は高速・データ駆動型のルート計画ツールへと移行しています。物流事業者は予測分析を活用し、温度感度に基づく配送順序の再編成により、廃棄物の削減とラストマイル走行距離の短縮を実現しています。こうした業務効率化の向上は、ドイツのコールドチェーン物流市場のサービス水準を加速させると同時に、対象となる消費者層を拡大しています。

バイオ医薬品およびmRNAベース医薬品の輸出拡大

2024年、ドイツの医薬品輸出額は1,058億ユーロ(1,167億6,000万米ドル)に達し、温度管理が必要な生物製剤が最も急速な伸びを示しました。DHLグループ単独でも、生物製剤や細胞治療薬の輸送を保護するため、GDP認証ハブ、検知機器、マルチ温度対応車両群に2030年までに20億ユーロ(22億米ドル)を投資予定です。フランクフルトとミュンヘン周辺のバイオテクノロジー回廊では、現在-70℃から+25℃までの連続的な可視性が求められており、リアルタイム追跡、管理連鎖文書化、AIを活用した冷却最適化のアップグレードが促進されています。これらの機能により、ドイツは新規治療法における欧州の主要輸出ゲートウェイとしての地位を確固たるものとし、ドイツのコールドチェーン物流市場全体でプレミアムサービス収益を押し上げています。

認定冷凍技術者の不足

2024年時点で、冷凍技術者の求人枠の60%以上が未充足の状態が続いております。これは労働力の高齢化と新規参入者(特に女性)の不足を反映したものです。人材不足により保守リードタイムとサービスコストが増大し、事業者には遠隔診断や予知保全の導入が迫られております。見習い制度の改革は進められておりますが、ドイツのコールドチェーン物流業界では少なくとも2年間は技能不足が継続する見込みです。

セグメント分析

冷蔵輸送は2025年の収益の60.55%を占め、ドイツが欧州全域のゲートウェイとしての地位を確立していることを裏付けています。高速道路、鉄道、海上、航空の各輸送ルートが相互に連携し、温度管理された貨物を効率的に輸送しています。ヘーゲルマン・グループが導入したテレマティクス対応サーモキングユニット200台は、このセグメントの技術的優位性を示す好例です。予測期間中、自動化と電気自動車(EV)の導入は、国境を越えた物流の流れを円滑化し、生物学的製剤や高級食品ラインの品質保証を継続的に支えてまいります。

付加価値サービスはCAGR4.55%で拡大が見込まれており、この分類内で最も高い成長率です。GDP(温度管理配送計画)やHACCP(危害分析重要管理点)への準拠に関する規制負担の増加が、特殊包装、バッチレベル監視、文書化支援の需要を後押ししています。リネージ・ロジスティクスのような保管事業者は、自動ピッキング・パッキングシステムとリアルタイムダッシュボードを統合し、倉庫保管、輸送、コンプライアンス活動を単一サービス契約に集約しています。したがって、製造業者が複雑な業務を外部委託し、規制当局が監視を強化する中、ドイツのコールドチェーン物流市場における付加価値ソリューションの市場規模は、複数年にわたる複合的な拡大が見込まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- Eコマース主導によるB2C食料品配送の増加

- バイオ医薬品及びmRNAベース医薬品の輸出拡大

- 小売業者の「ダブルフレッシュ」プライベートブランド推進

- 電気自動車対応マルチ温度トラックボディの急増

- 北海沿岸港湾への水産加工のニアショアリング

- アンモニア/CO2自然冷媒への改修に対する税制優遇措置

- 市場抑制要因

- 有資格冷凍技術者の不足

- 大規模冷蔵倉庫における電力価格の変動性

- 夜間配送における自治体ごとの騒音排出規制のばらつき

- 新規倉庫建設における長期化する計画承認手続き

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- サービスタイプ別

- 冷蔵保管

- 公共倉庫

- 民間倉庫

- 冷蔵輸送

- 道路輸送

- 鉄道輸送

- 海上輸送

- 航空輸送

- 付加価値サービス

- 冷蔵保管

- 温度タイプ別

- 冷蔵(0~5°C)

- 冷凍(-18~0℃)

- アンビエント

- 超低温(-20°C未満)

- 用途別

- 果物・野菜

- 肉類および家禽類

- 魚介類

- 乳製品および冷凍デザート

- 製パン・製菓

- 即席食品

- 医薬品・生物学的製剤

- ワクチン・臨床試験用資材

- 化学品・特殊材料

- その他の生鮮品

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Kuehne+Nagel International AG

- DHL Group

- Lineage Logistics LLC

- DFDS Logistics

- Dachser SE

- DSV

- Pfenning Logistics

- NewCold Advanced Logistics

- Heuer Logistics GmbH & Co. KG

- BLG Logistics

- Frigolanda Cold Logistics

- Scan Global Logistics

- Nordfrost GmbH & Co. KG

- Thermotraffic GmbH

- HAVI Logistics GmbH

- Fiege Logistik Stiftung & Co. KG

- CEVA Logistics

- Yusen Logistics

- Hellmann Worldwide Logistics

- Rhenus Logistics