|

|

市場調査レポート

商品コード

1640573

北米の金属缶:市場シェア分析、産業動向、成長予測(2025~2030年)North America Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の金属缶:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

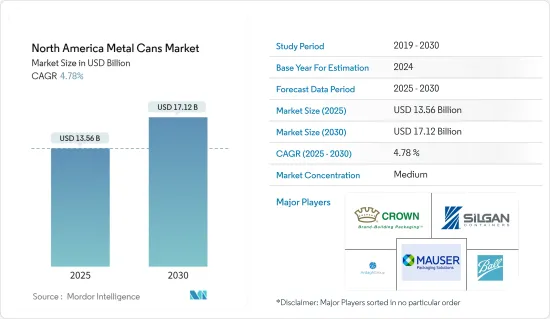

北米の金属缶の市場規模は2025年に135億6,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは4.78%で、2030年には171億2,000万米ドルに達すると予測されています。

金属缶包装市場で大きなシェアを占める飲食品業界は、COVID-19パンデミックの中、必需品に該当するため、大規模な需要を目の当たりにしています。COVID-19パンデミックのために地域全体で実施された封鎖は、消費習慣の大幅な変化を買っています。包装食品、食肉、野菜、果物の需要が増加しています。

主なハイライト

- 金属缶は、この地域の多くの消費者の外出の多いライフスタイルに最適なパッケージング・ソリューションのひとつであり、その利便性が利点のトップに挙げられています。ガラスは割れやすいため、主に制限されています。さらに、エナジードリンクの人気の高まり、新製品のイントロダクション、缶の価格とリサイクル可能性が、調査した市場の成長を後押ししています。

- 多くのブランドが新しいエナジードリンクを発売しています。例えば、北米コカ・コーラは2020年、コークブランド初のエナジードリンク「コカ・コーラ・エナジー・チェリー」(米国限定フレーバー)を発表しました。カロリーゼロのものは、12オンスのスリーク缶で全米で販売される予定です。

- さらに、アルミニウム協会と製缶協会(CMI)の2020年報告によると、米国におけるアルミ缶の業界リサイクル率は55.9%、消費者のリサイクル率は46.1%です。また、材料の価値は1,210米ドル/トンを占めています。

- この地域の化粧品分野も、多くの化粧品・パーソナルケアメーカーが自社製品の金属缶包装を好むため、金属缶市場の成長を牽引しています。例えば、Happi Magazineによると、2020年の米国におけるユニリーバ、プロクター・アンド・ギャンブル、コルゲート・パルモリーブなどの大手消臭剤ベンダーの販売数量は、それぞれ3億2,704万米ドル、2億1,979万米ドル、3,849万米ドルを占めています。

- 金属製缶包装市場で大きなシェアを占める飲食品業界は、COVID-19が大流行する中、必需品に該当するため、莫大な需要を目の当たりにしています。Store Brands社が発表した2020年の調査によると、米国ではCOVID-19の大流行により缶詰の消費量が96%増加しました。また、冷凍ディナーの消費も71%増加しました。

北米の金属缶の市場動向

飲料が大きな市場シェアを占める見込み

- 金属缶は飲料用に最も広く使用されています。ワイン、カクテル、ハードドリンク、ソフトドリンクの缶詰は、北米における携帯性の必要性から金属缶が主流となっています。飲料業界における金属缶の用途は、飲料の性質によってアルコール飲料とノンアルコール飲料に大別されます。ビールのようなアルコール飲料は、歴史的に金属缶を使用してきたが、ワインのような他の種類の酒類は、伝統的にガラス瓶で提供されてきたが、金属缶の採用が増加しています。

- さらに、飲料缶メーカーは、缶の製造に必要なゲージを減らすことで軽量化を実現しています。金属缶は、ソーダの包装に必要な炭酸ガス圧を支えることができます。金属缶はまた、1平方インチあたり90ポンドまでの力に耐えることができます。この要因により、缶は飲料業界におけるパッケージングに適した選択肢となっています。

- 金属缶メーカーは、金属缶の不足によって直面しているサプライチェーンの混乱に対処するため、北米での生産能力を増強しています。ボール社の社長は、2023年まで需要が供給を上回ると予測しています。飲料業界における金属缶の積極的な需要と成長は、調査対象地域におけるこのセクターへの複数の投資に火をつけた。

- 例えば、2021年9月、パッケージ企業のBall Corporationは、ラスベガスの新しいアルミニウム飲料パッケージング工場に複数年かけて2億9,000万米ドルを投資すると発表しました。この工場では、さまざまなサイズの缶が製造される予定です。この工場は2022年後半に生産を開始する予定で、完全稼動時には180人の製造業雇用を創出します。

- さらに、アーダー・グループは2020年10月、ミシシッピ州の生産施設に新たに2つの高速飲料製造ラインを設置できると発表しました。同社は、この投資は、ハードセルツァー、ビール、エナジードリンク、お茶を含む様々な飲料用の特許取得済みの洗練されたデザインラインの生産に対応することを目的としていると発表しました。

米国が最大のシェアを占める

- 同市場では、パンデミックによる缶不足の問題から、多くの企業が既存工場に新ラインを追加し、生産性向上を図っています。例えば、Ball Corporationは2020年9月、パンデミックにより家庭での消費が拡大する北米市場に対応するため、2021年半ばまでにペンシルベニア州ピットストンにアルミ飲料パッケージ工場を開設すると発表しました。同社は当初、2021年までに60億缶の生産拡大を計画していました。ボール社は、2021年末までに2つの新工場を開設し、米国施設に2つの生産ラインを追加することを視野に入れています。

- パンデミックにより多くのレストランやバーが休業し、缶入りアルコール飲料の売上が大幅に増加しました。また、多くの飲料メーカーが製品を缶にシフトしたため、アルミ缶のサプライチェーンに負担がかかった。缶の需要に対応するため、多くのメーカーが増え続ける需要に対応する施設を開設しています。

- 例えば、2021年1月、クラウン・ホールディングスは、バージニア州ヘンリー国とブラジル南東部ミナスジェライス州に2つの飲料缶工場を新設するために投資しました。バージニア州の工場では、スパークリングウォーター、エナジードリンク、炭酸清涼飲料、お茶、機能性飲料、ハードセルツァー、ビール、カクテルなど様々なカテゴリーに対応する飲料缶を供給します。同社はこの工場により北米の供給網を拡大し、拡大する標準および特殊飲料缶市場に対応します。

- さらに、クラウン・ホールディングは2021年4月、米国で3つ目となる飲料缶生産施設の新設計画を発表しました。この工場では、スパークリングウォーター、エナジードリンク、炭酸清涼飲料、機能性飲料、ビールなどの缶を生産します。

- 缶メーカー協会(CMI)の飲料缶メーカーとアルミ缶シートメーカーの会員は、2030年までにリサイクル率70%など、米国の野心的なリサイクル率目標の達成に取り組んでいます。これらの新しい目標は、飲料用アルミ缶の循環性を向上させるとともに、飲料用アルミ缶が市場で最も持続可能なパッケージであり続けるための業界の献身を飲料メーカーと消費者に示すものです。

北米の金属缶産業の概要

北米の金属缶市場の競争は中程度です。市場で大きなシェアを持つ大手企業は、様々な地域で顧客基盤を拡大しています。さらに、多くの企業が市場シェアと収益性を高めるために、複数の企業と戦略的・協力的なイニシアティブを形成しています。市場の最近の動向をいくつか紹介する:

- 2021年3月-Ball Corporationは、スペインの主要飲料企業であるDamm社と提携し、北米でビールの貯蔵・包装用アルミ缶ASI's(The aluminum stewardship initiative)を導入しました。これにより、同社の販売実績の増加が期待されます。

- 2021年2月-アーダッシュ・グループは、金属パッケージング事業をゴアーズ・ホールディングスV社と合併し、上場会社を設立することで合意。この合意により、ユニークな目的の買収会社であるゴアーズ・ホールディングスVがアーダグの金属パッケージング部門と合併し、新たにアーダグ・メタルが設立されます。アーダグはAMPの株式80%を保持し、取引完了時に最大34億米ドルの現金を受け取る。この取引には、ゴアーズ・ホールディングスVからの最大5億2,500万米ドルの現金と、投資家が主導する6億米ドルの第三者割当増資、およびAMPが調達する約23億米ドルの新規債務が含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン分析

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- 金属包装の高いリサイクル率

- 缶詰が提供する利便性と低価格

- 市場抑制要因

- 代替包装ソリューションの存在

第6章 市場セグメンテーション

- 材料タイプ別

- アルミニウム

- スチール

- 業界別

- 食品

- 飲料

- 医薬品

- 化粧品・パーソナルケア

- その他業界別

- 国別

- 米国

- カナダ

第7章 競合情勢

- 企業プロファイル

- Crown Holdings Inc.

- Ball Corporation

- Silgan Containers LLC

- Mauser Packaging Solutions

- Ardagh Group S.A.

- DS Containers Inc.

- CCL Container Inc.

- Independent Can Company

- Technocap Group

- Can-Pack SA

- Allstate Can Corporation

- Envases Group

第8章 投資分析

第9章 市場の将来展望

The North America Metal Cans Market size is estimated at USD 13.56 billion in 2025, and is expected to reach USD 17.12 billion by 2030, at a CAGR of 4.78% during the forecast period (2025-2030).

With a significant share in the metal can packaging market, the food and beverage industry is witnessing massive demand amidst the COVID-19 pandemic, as the industry falls under the essential commodity. The lockdown enforced across the region due to the COVID-19 pandemic has bought a significant change in consumption habits. There has been an increasing demand for packaged food products, meat, vegetables, and fruits.

Key Highlights

- Metal cans are one of the perfect packaging solutions for the on-the-go lifestyle of many consumers in the region, and their convenience is topping the benefits list. These can be easily transported or carried to festivals, beaches, and outdoor and sporting events, whereas glass is mainly restricted due to its breakability. In addition, the increasing popularity of energy drinks, the introduction of new products, and the price and recyclability of cans augment the studied market growth.

- Many brands are introducing new energy drinks. For instance, in 2020, Coca-Cola North America unveiled the first-ever energy drink under the Coke brand Coca-Cola Energy Cherry a flavor available exclusively in the United States. Their zero-calorie counterparts will be available nationwide in 12-oz. sleek cans.

- Furthermore, according to the Aluminum Association and Can Manufacturers Institute (CMI), 2020 report, the industry recycling rate of aluminum can account for 55.9% in the United States, and the Consumer recycling rate of aluminum can account for 46.1%. In addition, the value of material accounted for USD 1,210/tons.

- The cosmetic segment in the region is also driving the growth of the metal cans market in the area as many cosmetic and personal care manufacturers prefer metal cans packaging for their products. For instance, according to Happi Magazine, the unit sales of leading deodorant vendors such as Unilever, Procter, and Gamble, Colgate Palmolive in the United States in 2020 accounted for USD 327.04 million, USD 219.79 million, and USD 38.49 million, respectively.

- The food and beverage industry, with a major share in the metal, can packaging market, has witnessed huge demand amidst the COVID-19 pandemic, as the industry falls under the essential commodity. According to a 2020 survey published by Store Brands, the consumption of canned food due to the Covid-19 pandemic increased by 96% in the United States. Also, frozen dinners consumption also increased by 71%.

North America Metal Cans Market Trends

Beverage is Expected to Account For Significant Market Share

- Metal cans are most widely used for beverages. The most notable trend of canned wine, cocktails, hard drinks, and soft drinks is packaged in metal, driven by the need for portability in North America. The usage of metal cans in the beverage industry can be widely classified into alcoholic drinks and non-alcoholic drinks based on the nature of the beverage. Alcoholic beverages, such as beer, have historically used metal cans, while other kinds of liquor, like wine, traditionally served in glass bottles, are increasingly adopting metal cans.

- Moreover, beverage can manufacturers have reduced the weight by reducing the gauge required to fabricate the cans. Metal cans can support the carbonation pressure that is needed to package soda. Metal cans also resist forces up to 90 pounds per square inch. This factor makes the cans the favored choice for packaging in the beverage industry.

- Metal can manufacturers are increasing the production capacity in North America to address the supply chain disruption faced due to the shortage in metal cans. The President of the Ball Corporation has identified the demand to outstrip the supply until 2023. The aggressive demand and growth of metal cans in the beverage industry sparked multiple investments in the sector in the studied region.

- For instance, in September 2021, Packaging company Ball Corporation announced an investment of USD 290 million over the course of multiple years into a new aluminum beverage packaging plant in Las Vegas. The plant is expected to create a range of can sizes. The facility is scheduled to begin production in late 2022 and will create 180 manufacturing jobs when it is fully operational.

- Further, Ardagh Group announced in October 2020 that the two new high-speed beverages could manufacture lines in its production facility in Mississippi. The company announced that the investment is aimed to cater to the production of its patented sleek design line for various beverages, including hard seltzers, beer, energy drinks, and tea.

United States Accounts for the Largest Share

- Many companies in the market are adding new lines to existing plants and are making productivity enhancements because of the can shortage issues due to the pandemic. For instance, in September 2020, Ball Corporation announced that it would open an aluminum beverage packaging plant in Pittston, Pennsylvania, by mid-2021 to serve the North American market as the at-home consumption grows due to the pandemic. The company initially planned a 6 billion can output expansion by 2021. Ball Corporation is looking forward to opening two new plants and adding two production lines to the United States facilities by the end of 2021.

- Many restaurants and bars were closed with the pandemic, due to which canned alcoholic beverages witnessed a significant increase in sales. Also, many beverage manufacturers shifted their products into cans, which has put a strain on the aluminum can supply chain. To cater to the demand for cans, many manufacturers have been opening facilities to meet this ever-growing demand.

- For instance, in January 2021, Crown Holdings invested in the two new beverage can plant in Henry Country, Virginia, and Minas Gerais State, Southeast Brazil. The plant in Virginia will be supplying beverage cans to serve various categories, including sparkling water, energy drinks, carbonated soft drinks, tea, functional beverages, hard seltzers, beer, and cocktails. The company expands its North American supply network with the plant to address the growing standard and specialty beverage cans market.

- Additionally, in April 2021, Crown Holding unveiled its plan to build its third new beverage can production facility in the United States. The plant will produce cans for sparkling waters, energy drinks, carbonated soft drinks, functional beverages, beers, among other beverages.

- Can Manufacturers Institute (CMI) beverage can manufacturer and aluminum can sheet producer members are committing to achieving ambitious U.S. recycling rate targets, including a 70% recycling rate by 2030. These new targets will improve the circularity of the aluminum beverage can while demonstrating to beverage companies and consumers the industry's dedication to ensuring the aluminum beverage can remain the most sustainable package on the market.

North America Metal Cans Industry Overview

The North America Metal Cans market is moderately competitive. The major players with a significant share in the market are expanding their customer base across various regions. In addition, many companies are forming strategic and collaborative initiatives with multiple companies to increase their market share and profitability. Some of the recent developments in the market are:

- March 2021 - Ball Corporation, along with the partnered company Damm, one of the leading beverage companies in Spain, introduced ASI's(The aluminum stewardship initiative) aluminum cans for storage and packaging of beer in North America. This is expected to increase the sales performance of the company.

- February 2021 - Ardagh Group agreed to merge its metal packaging business with Gores Holdings V, creating a publicly listed company. The agreement will see Gores Holdings V, a unique purpose acquisition company, merge with Ardagh's metal packaging division to form the newly created Ardagh Metal. Ardagh will retain an 80% stake in AMP and receive up to USD 3.4 billion in cash when the transaction completes. The deal includes up to USD 525 million in cash from Gores Holdings V and USD 600 million in a private placement led by investors, along with approximately USD 2.3 billion of new debt raised by AMP.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of COVID -19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclability Rates of Metal Packaging

- 5.1.2 Convenience and Lower Price Offered by Canned Food

- 5.2 Market Restraints

- 5.2.1 Presence of Alternate Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminum

- 6.1.2 Steel

- 6.2 By End-user Vertical

- 6.2.1 Food

- 6.2.2 Beverage

- 6.2.3 Pharmaceuticals

- 6.2.4 Cosmetic and Personal Care

- 6.2.5 Other End-user Verticals

- 6.3 By Country

- 6.3.1 United States

- 6.3.2 Canada

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Crown Holdings Inc.

- 7.1.2 Ball Corporation

- 7.1.3 Silgan Containers LLC

- 7.1.4 Mauser Packaging Solutions

- 7.1.5 Ardagh Group S.A.

- 7.1.6 DS Containers Inc.

- 7.1.7 CCL Container Inc.

- 7.1.8 Independent Can Company

- 7.1.9 Technocap Group

- 7.1.10 Can-Pack SA

- 7.1.11 Allstate Can Corporation

- 7.1.12 Envases Group