|

市場調査レポート

商品コード

1628849

アジア太平洋の金属缶:市場シェア分析、産業動向、成長予測(2025年~2030年)Asia Pacific Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の金属缶:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

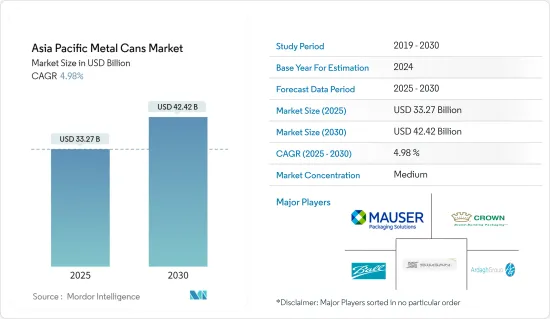

アジア太平洋の金属缶市場規模は2025年に332億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは4.98%で、2030年には424億2,000万米ドルに達すると予測されます。

主要ハイライト

- 金属缶市場は、技術革新と持続可能性の厳しい追求に煽られてパラダイムシフトが起きています。環境に配慮した包装ソリューションを求める世界の動きと歩調を合わせ、メーカーは最先端の材料や環境に優しい手法を採用するようになっています。

- 缶は持ち運びが簡単で軽量であるため、消費者にとって理想的です。さらに、缶を使用することで、こぼれたり割れたりするリスクを最小限に抑えることができるため、アウトドア活動やイベントで特に人気があります。缶入り飲料に対する消費者の嗜好の高まり、エネルギー飲料やスポーツ飲料の人気の高まり、サステイナブル包装材料に対する需要の高まりは、市場の重要な促進要因の一部です。

- アジア太平洋諸国におけるプラスチック廃棄物への懸念は、予測期間中、金属包装の成長要因のひとつとなると考えられます。製造業者と消費者は現在、低コストや利便性といった他の考慮事項を優先しています。しかし、金属包装の将来的な拡大は、包装廃棄物を規制し減少させるための政府イニシアティブの増加によって助長される可能性があります。

- アジア全域で、食品包装産業はその理想的な防腐特性と構造的完全性により賞味期限を延ばすため、金属缶への依存度を高めています。消費者が多忙なライフスタイルや仕事のスケジュールをこなす中で、包装された便利な食品は食生活の主食となっています。

- より小型のマルチパック・フォーマットへの嗜好といった動向が、金属缶市場の成長を牽引しています。インド、中国、日本を含むアジア太平洋市場ではミニ缶の需要が高まっています。これを受けて、多くの地域の飲料メーカーが、従来の缶よりも少量で低コストのミニ缶を導入しています。

- アジアの動向は、東南アジアの成長と絡み合っています。中国と日本のメーカーは、この地域での存在感を高めています。例えば、昭和アルミ缶は、そのプロジェクトを通じて、中期的な事業成長のために戦略的に東南アジアを対象にしています。

- 製造プロセスにおける革新、多様な形態やサイズ、スマート包装の先進性により、金属缶メーカーは市場動向との整合性を保っています。多段階印刷やラベリングに対応するクリーンな表面は、重要なマーケティング革新を引き起こしています。

- 一例として、インドのHindustan Tin Works Ltdは、酸素、湿気、バクテリアに対する優れたバリアを提供し、げっ歯類や害虫を抑止し、消費まで製品の安全性を確保する一般的なライン缶を製造しています。

- 金属缶、特にアルミ缶は、リサイクルをリードしています。ライフサイクルの終わりに品質を損なうことなくリサイクルできることから、プラスチックや紙といった代替品を凌いで、ブランドにとって好ましい包装の選択肢となっています。60日で新品の缶として棚に戻るという迅速さは、食品、飲料、エアロゾル産業におけるアルミの魅力を際立たせています。

- しかし、金属缶は代替包装ソリューションとの厳しい競合に直面しています。特にボトルやペール缶のような形態のプラスチック包装が、主要な競争相手となっています。さらに、ポリマーベースの代替品の出現と原料価格の変動が、この地域の金属缶市場に課題を突きつけています。

アジア太平洋の金属缶市場動向

缶食品が提供する利便性と低価格が市場成長を牽引

- 缶食品市場では、化学品を使用しない選択肢に対する需要の高まりにより、革新的な包装が増加しています。缶食品の多くのブランドがBPAフリーの容器で食品を提供し始めています。

- 食品を有害なバクテリアから守るため、密封され、いたずらできないスチール容器食品の需要は高いです。また、消費者の多忙なライフスタイルにより、缶フードの重要性が増すと予想されます。

- ペットフードの包装は、汚染や腐敗の原因となる湿気やその他の環境条件に対するバリアを提供することで、食品の品質と安全性に大きく影響します。ペットフードの包装には一般的に金属が使用され、一般的には錫やアルミニウムが使われ、食品、臭い、漏れが漏れないように密閉されています。

- 設計の柔軟性が制限され、缶を開けるのに不便であることが、金属製ペットフード缶の重大な欠点でした。このセグメントでは、スチール缶の安全性と、リサイクル可能で再生材料を使用していることによる環境への優しさを強調することで、競合を高めようとしています。金属缶で包装されたペットフードは、缶の密閉性とタンパーエビデンスにより、プラスチックの代替品よりも好まれています。

- その他の利点には、低コスト、長い保存期間、耐久性、ウェットフード製品への適合性などがあります。さらに、開封が容易であることも、継続的なビジネス機会につながると期待されています。金属製食品缶の充填速度の速さとライン効率の良さも、製造に時間がかかり製造コストがかさむプラスチックの代替品への生産シフトをメーカーに消極的にさせています。

著しい成長を遂げるインド

- 近年、インドの飲料産業ではジュースの包装が大きく変化しています。この進化は単に動向を追うだけでなく、消費者の嗜好の変化や環境問題への意識の高まりを反映しています。これを踏まえ、メーカーはインドでサステイナブル製品の発売を優先しています。

- 2024年、Ball Corporationは、革新的でサステイナブルアルミ包装の世界的リーダーであるDel Monte Foodsと提携しました。両社は持続可能性に取り組んでおり、2070年までにネットゼロ排出を達成し、2030年までに炭素集約度を45%削減するというインド政府の野心的な目標に合致しています。Ballの支援により、Del Monte Foodsは従来の3ピースのブリキ缶から、無限にリサイクル可能な2ピースのアルミ製飲料缶に移行しました。

- さらに、使い捨てプラスチックの禁止に関する最近の規制は、プラスチック包装の成長を伸ばすと期待されており、すべての利害関係者との話し合いが終了次第、施行される予定です。インド食品安全基準局(Food Safety and Standards Authority of India)は、環境に優しい代替品に対応するため、使い捨てプラスチック材料の使用禁止を再検討しています。

- アルコール飲料と非アルコール飲料市場の成長に伴い、金属缶包装の需要は国内で大幅に増加すると予想されます。例えば、インドのクラフトビール協会によると、インドの地ビール醸造所の数は過去5年間で20から120に急増しました。

- インドのアルミ飲料缶協会(ABCAI)コンソーシアムは、プラスチックやガラスの包装からアルミへの移行を推進しています。ABCAIは、2030年までにこの数字を約25%まで引き上げることを目標としています。

- また、鉱業省のデータによると、アルミニウムの一次生産量は2022~2023年度の40.73ラカートン(LT)から2023~2024年度には41.59LTに増加し、成長率は2.1%です。このアルミニウム生産量の増加は、金属缶の需要が急増していることを示しています。金属缶の生産はアルミニウムに大きく依存していることから、生産量の増加は、メーカーがこの消費者の旺盛な需要に応えるために金属缶の生産を強化していることを示しています。

- さらに、国内の新興企業によるビール市場の拡大も、インドの金属缶部門を後押ししています。また、Ball Corporationは飲料製品の要件を満たす金属缶を提供しており、インドにおける年間生産能力は13億缶です。ボール社によると、インドの消費量は一人当たり1缶以下であり、金属包装・プロバイダーにとって新興市場を開拓する大きな機会となっています。

- また、飲料メーカーとインドの缶メーカーとの協力関係も金属缶市場の成長を後押ししています。例えば2024年、HEINEKENの子会社であるUnited Breweries of IndiaはCANPACKと提携し、女性らしさをテーマにした限定ビールを発表しました。「Queenfisher」と名付けられたこの新しいプレミアム・ラガーは、同社の主力ブランドである「Kingfisher」を補完するようにデザインされています。

アジア太平洋の金属缶産業概要

アジア太平洋の金属缶市場はセグメント化されており、Ball Corporation、Crown Holdings、Ardagh Group SA、Silgan Holdings Inc.、Mauser Packaging Solutionなど、多様な主要企業で構成されています。これらの企業は、イノベーション、提携、M&Aを通じて、金属缶市場での事業拡大に積極的に注力しています。

2024年5月、サステイナブル包装に向けた大きな動きとして、Ball Corporationは乳製品産業の先駆者であるCavinKareと提携。この提携は、CavinKareの有名なミルクセーキ用のレトルト2ピースアルミ缶を展開することで、乳製品包装を変革することを目的としています。

同社の予測によると、乳製品・乳製品代替品セグメントはインドで極めて重要であり、2028年までに年間4.1%の成長率で拡大すると予測されています。同社は、多様なフレーバーを提供することで、より早い成長を見込んで、レディトゥドリンク部門に注力しています。Ball India社は、乳製品部門のニーズに合わせて特別に設計されたレトルトアルミ缶の製造能力を強化しています。このポートフォリオの拡大は、製品の革新と持続可能性へのコミットメントを強調し、アルミ缶に多様な風味の乳製品を包装することを容易にします。

2023年7月、Crown Holdingsは、10月30日から11月1日までタイのバンコクで開催されるAsia CanTech 2023の講演者スケジュールに参加すると発表しました。同事業では、タイ、ベトナム、カンボジアを含む飲料用アルミ缶のリサイクル率に関する調査結果について議論する予定。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- 金属包装の高いリサイクル率

- 缶が提供する利便性と低価格

- 市場抑制要因

- 代替包装ソリューションの存在

- 地域における原料価格の変動

第6章 市場セグメンテーション

- 材料タイプ

- アルミニウム

- スチール

- 製品タイプ

- 2ピース

- 3ピース

- 缶タイプ

- 食品缶

- 野菜

- フルーツ

- ペットフード

- スープ

- コーヒー

- その他の食品缶

- 飲料缶

- アルコール飲料

- ノンアルコール

- エアロゾル缶

- 化粧品・パーソナルケア

- 家庭用

- 塗料・ワニス

- 医薬品・動物用

- 自動車・産業用

- その他のエアロゾル缶

- その他の缶タイプ

- 食品缶

- 国名

- インド

- 中国

- 韓国

- 日本

- オーストラリアとニュージーランド

第7章 競合情勢

- 企業プロファイル

- Amcor PLC

- Ball Corporation

- Mauser Packaging Solutions

- Crown Holdings Inc.

- CANPACK SA

- Toyo Seikan Group Holdings Ltd

- Showa Denko K.K.

- Hindustan Tin Works Ltd

- AJ Packaging Limited

- Nanchang Ever Bright Industrial Trade Co. Ltd(EBI)

- Shanghai Jima Industrial Co. Ltd

第8章 投資分析

第9章 市場機会と今後の動向

The Asia Pacific Metal Cans Market size is estimated at USD 33.27 billion in 2025, and is expected to reach USD 42.42 billion by 2030, at a CAGR of 4.98% during the forecast period (2025-2030).

Key Highlights

- The metal cans market is witnessing a paradigm shift fueled by a severe search for innovation and sustainability. Manufacturers increasingly adopt cutting-edge materials and eco-friendly practices, aligning with the global push for environmentally responsible packaging solutions.

- Cans are easy to carry and light in weight, making them ideal for consumers. Additionally, using cans helps minimize the risk of spills or breakage, making them especially popular for outdoor activities and events. The increasing consumer preference for canned drinks, the rising popularity of energy and sports drinks, and the growing demand for sustainable packaging materials are some of the critical drivers of the market.

- Concerns about plastic waste in various Asia-Pacific countries will likely be one of the growth factors for metal packaging during the forecast period. Manufacturers and consumers now prioritize other considerations, such as low cost and convenience. However, the future expansion of metal packaging may be aided by increased government initiatives to regulate and decrease packaging waste.

- Across Asia, the food packaging industry increasingly relies on metal cans due to their ideal preservative properties and structural integrity, which extend shelf life. Packaged and convenient foods have become dietary staples as consumers juggle hectic lifestyles and work schedules.

- Trends like a preference for smaller and multi-pack formats are driving the growth of the metal cans market. There is a rising demand for mini-cans in the Asia-Pacific markets, including India, China, and Japan. In response, many regional beverage companies are introducing mini-cans, which offer smaller volumes at a lower cost than traditional cans.

- Asian trends are intertwined with the growth of Southeast Asia. Manufacturers from China and Japan are broadening their presence in the region. For instance, Showa Aluminum Can Corporation, through its project, is strategically targeting Southeast Asia for medium-term business growth.

- Innovations in manufacturing processes, diverse shapes and sizes, and advancements in smart packaging are enabling metal can manufacturers to stay aligned with market trends. Clean surfaces that accommodate multi-stage printing and labeling are drawing significant marketing innovations.

- As an illustration, Hindustan Tin Works Ltd from India produces general line cans that offer superior barriers against oxygen, moisture, and bacteria and deter rodents and pests, ensuring product safety until consumption.

- Metal cans, especially aluminum, lead the way in recycling. Their ability to be recycled without any loss of quality at the end of their life cycle makes them the preferred choice for packaging for brands, surpassing alternatives such as plastic and paper. This swift return to shelves as new cans in 60 days underscores aluminum's appeal in the food, beverage, and aerosol industries.

- However, metal cans grapple with stiff competition from alternative packaging solutions. Plastic packaging, especially in forms like bottles and pails, stands as the primary competitor. Additionally, the emergence of polymer-based substitutes and fluctuating raw material prices pose challenges for the metal cans market in the region.

Asia Pacific Metal Cans Market Trends

Convenience and Lower Price Offered by Canned Food to Drive the Market Growth

- The canned food market is seeing a rise in innovative packaging due to the growing demand for chemical-free options. Many brands of canned food products have started offering food in BPA-free containers.

- The demand for sealed and tamper-proof steel container food is high, as they protect food from harmful bacteria. Also, due to consumers' busy lifestyles, canned food is expected to gain more importance.

- Pet food packaging can significantly influence the quality and safety of the food product by providing barriers to moisture and other environmental conditions that may result in contamination and spoilage. Metal is commonly used in pet food packaging, typically tin or aluminum, and is tightly sealed to prevent any food, odors, or leaks from escaping.

- Limited design flexibility and inconvenience in opening the cans have been the significant disadvantages of metal pet food cans. This segment is trying to increase its competitiveness by emphasizing steel cans' safety and environmental friendliness, owing to their recyclability and use of recycled content. Pet food packaged in metal cans is preferred over plastic alternatives due to cans' tight seal and tamper evidence.

- Other advantages include its low cost, long shelf life, durability, and amenability to wet food products. Additionally, easy opening ends are expected to support continued opportunities. Fast-filling speeds and line efficiencies of metal food cans also make manufacturers reluctant to shift production to plastic alternatives, which are slower to manufacture and involve added production costs.

India to Witness Significant Growth

- In recent years, the Indian beverage industry has seen a significant shift in juice packaging. This evolution goes beyond merely following trends; it reflects changing consumer preferences and a growing awareness of environmental issues. In light of this, manufacturers are prioritizing sustainable product launches in India.

- In 2024, Ball Corporation partnered with Del Monte Foods, a global leader in innovative, sustainable aluminum packaging. Both companies are committed to sustainability, aligning with the Indian government's ambitious goals of achieving net-zero emissions by 2070 and cutting carbon intensity by 45% by 2030. With Ball's backing, Del Monte Foods moved from traditional three-piece tin cans to infinitely recyclable two-piece aluminum beverage cans.

- Additionally, the recent regulation on the ban on single-use plastics is expected to grow plastic packaging growth, which is scheduled to be enforced once the discussion with all the stakeholders is concluded. The Food Safety and Standards Authority of India is reviewing the ban on using single-use plastic materials to accommodate eco-friendly alternatives.

- With the growth of the alcoholic and non-alcoholic beverage market, the demand for metal can packages is expected to increase significantly in the country. For instance, according to the Craft Brewers Association of India, the number of microbreweries in India galloped from 20 to 120 in the past five years.

- The Aluminum Beverage Can Association of India (ABCAI) consortium is pushing for a shift from plastic and glass packaging to aluminum. Aluminum cans hold a mere 5% share of the country's packaging landscape, but ABCAI aims to elevate this figure to approximately 25% by 2030.

- Also, the Ministry of Mines data reveals that primary aluminum production rose from 40.73 lakh tons (LT) in FY 2022-2023 to 41.59 LT in FY 2023-2024, marking a growth rate of 2.1%. This increase in aluminum production signals a burgeoning demand for metal cans. Given that producing metal cans heavily relies on aluminum, the increased production volume indicates that manufacturers are ramping up metal can production to cater to this surging consumer appetite.

- Moreover, the proliferation in the beer market by newer companies in the country is helping the Indian metal can segment. Ball Corporations also provide metal cans that meet the requirement of beverage products, with an annual capacity of 1.3 billion cans in India. According to the Ball Corporation, the consumption in India is less than one can per capita, which presents a massive opportunity for metal packaging providers to tap into the emerging market.

- Also, collaborations between beverage companies and can manufacturers in India fuel the growth of the metal cans market. For example, in 2024, United Breweries of India, a subsidiary of HEINEKEN, partnered with CANPACK to unveil a limited-edition beer prominently featuring a feminine theme. This new premium lager, dubbed 'Queenfisher', is designed to complement the company's flagship 'Kingfisher' brand.

Asia Pacific Metal Cans Industry Overview

The Asia-Pacific metal cans market is fragmented and consists of a diverse array of key players, including Ball Corporation, Crown Holdings, Ardagh Group SA, Silgan Holdings Inc., and Mauser Packaging Solution. These companies actively focus on business expansion in the metal cans market through innovations, collaborations, and mergers and acquisitions.

May 2024: As a major move toward sustainable packaging, Ball Corporation teamed up with CavinKare, a trailblazer in the dairy industry. The collaboration aims to transform dairy packaging by rolling out retort two-piece aluminum cans for CavinKare's renowned milkshakes.

The dairy and dairy alternatives segment is pivotal in India and is projected to expand at an annual growth rate of 4.1% by 2028, as per company projections. The company concentrates on the ready-to-drink segment, anticipating quicker growth by diverse flavor offerings. Ball India has bolstered its capabilities to manufacture retort aluminum cans specifically designed for the dairy sector's needs. This portfolio expansion emphasizes the commitment to product innovation and sustainability and facilitates the packaging a diverse range of flavored dairy products in aluminum cans.

July 2023: Crown Holdings announced it would join the schedule of speakers at Asia CanTech 2023, which will be held in Bangkok, Thailand, from October 30 to November 1. The business will discuss the study's findings on the recycling rates of aluminum beverage cans, including Thailand, Vietnam, and Cambodia.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 High Recyclability Rates of Metal Packaging

- 5.1.2 Convenience and Lower Price Offered by Canned Food

- 5.2 Market Restraints

- 5.2.1 Presence of Alternate Packaging Solutions

- 5.2.2 Fluctuating Raw Material Prices in the Region

6 MARKET SEGMENTATION

- 6.1 Material Type

- 6.1.1 Aluminium

- 6.1.2 Steel

- 6.2 Product Type

- 6.2.1 2-piece

- 6.2.2 3-piece

- 6.3 Can Type

- 6.3.1 Food Cans**

- 6.3.1.1 Vegetables

- 6.3.1.2 Fruits

- 6.3.1.3 Pet Food

- 6.3.1.4 Soups

- 6.3.1.5 Coffee

- 6.3.1.6 Other Food Cans

- 6.3.2 Beverages Cans

- 6.3.2.1 Alcoholic

- 6.3.2.2 Non-alcoholic

- 6.3.3 Aerosol Cans**

- 6.3.3.1 Cosmetics and Personal Care

- 6.3.3.2 Household

- 6.3.3.3 Paints and Varnishes

- 6.3.3.4 Pharmaceutical/Veterinary

- 6.3.3.5 Automotive/Industrial

- 6.3.3.6 Other Aerosol Cans

- 6.3.4 Other Cans Types

- 6.3.1 Food Cans**

- 6.4 Country

- 6.4.1 India

- 6.4.2 China

- 6.4.3 South Korea

- 6.4.4 Japan

- 6.4.5 Australia and New Zealand

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amcor PLC

- 7.1.2 Ball Corporation

- 7.1.3 Mauser Packaging Solutions

- 7.1.4 Crown Holdings Inc.

- 7.1.5 CANPACK SA

- 7.1.6 Toyo Seikan Group Holdings Ltd

- 7.1.7 Showa Denko K.K.

- 7.1.8 Hindustan Tin Works Ltd

- 7.1.9 AJ Packaging Limited

- 7.1.10 Nanchang Ever Bright Industrial Trade Co. Ltd (EBI)

- 7.1.11 Shanghai Jima Industrial Co. Ltd