|

市場調査レポート

商品コード

1851933

米国の農業機械:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)United States Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の農業機械:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年08月08日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

概要

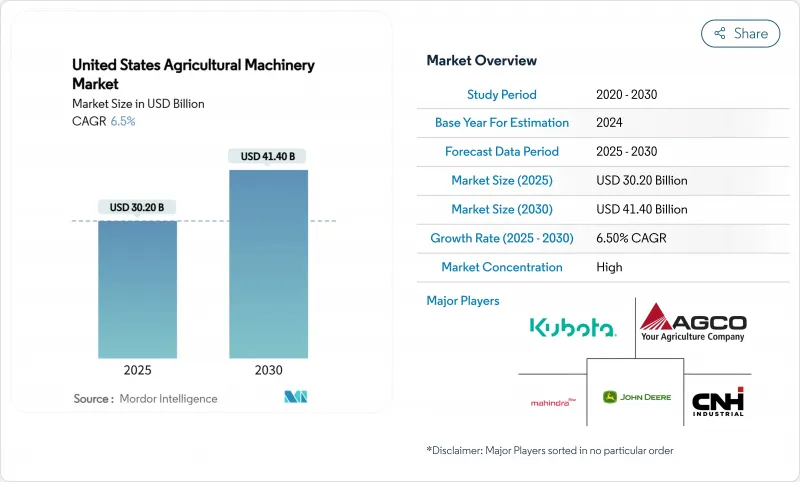

米国の農業機械の市場規模は2025年に302億米ドルとなり、CAGR 6.5%で成長し、2030年には414億米ドルに達すると予測されています。

気候変動に配慮した実践、精密技術の改修、電化投資に対する連邦政府の優遇措置が、周期的な市場の変動を相殺するのに役立っています。設備所有者は、運用コストの削減と持続可能性の目標達成のための機能アップグレードに注力し、テレマティクス、予知保全、自律走行対応システムへの需要が高まる。ディーラーの統合はアフターセールス・サービス網を改善し、リースやサブスクリプションのオプションは金利上昇の影響を緩和するのに役立っています。灌漑分野は、水不足の深刻化と排出ガス規制の強化により、米国の農業機械市場において高い成長率を示しています。

米国の農業機械市場の動向と洞察

精密農業レトロフィットキットの普及

レトロフィット・ソリューションにより、農家は既存の農機の寿命を延ばすと同時に、データ主導の改善により肥料と農薬の使用量を最大30%削減できます。トラクター1台あたり5万米ドルのレトロフィットへの投資は、自律走行対応機器の新規導入に必要な40万米ドルよりも大幅に低く、通常3年以内に投資回収が可能です。中規模の連作農家では、負債を増やすことなくコスト競争力を維持するため、こうしたソリューションの採用が増えています。機器ディーラーは、レトロフィット・キットの設置や校正を通じて、追加のサービス収入から利益を得ており、顧客との関係を強化し、収益性を向上させています。モジュール式アップグレードの採用が進むと、機器の交換サイクルが延びるため、相手先商標製品メーカー(OEM)は、販売台数からソフトウェアや統合サービスに重点を移すようになります。

主要OEMメーカーによる電動化ロードマップ

ディア・アンド・カンパニーは、2026年に初の全電気式自律走行可能トラクターを発売する計画で、バッテリー供給のためにクライセル・エレクトリックに投資しています。AGCOは2024年にフェントe100バリオを試験的に導入し、電動パワートレインに焦点を当てた研究開発費の60%増に支えられました。現在のバッテリー密度では、電動トラクターは120馬力以下の用途に限られており、これは果物、野菜、酪農場の要件に合致しています。自然資源保全局(NRCS)は、購入費用の50%以上をカバーできる費用負担プログラムを提供しており、小規模農場の経済的障壁を軽減しています。メーカー各社は、将来的なバッテリー技術の向上により、より高馬力の用途が可能になることを期待しているが、現在の進捗状況は、部品メーカーに米国でのバッテリーとインバーターの生産拡大を促しています。

ディーラー技術者の不足

機器サービス業界は著しい労働力不足に直面しています。サービス拠点の統廃合により実店舗の数が減少し、重要な作付けや収穫の時期の対応時間が長くなっています。最新の精密機器には、農村部の労働市場で利用可能なスキルを超える専門的な診断能力が要求されるため、相手先商標製品メーカー(OEM)は、遠隔サポート・サービスの拡大やモジュール式部品交換システムの導入を余儀なくされています。こうした労働力の制約から、農家は農業機械の購入を制限しています。

セグメント分析

トラクターは、耕うん、播種、マテリアルハンドリングにおいて重要な役割を果たすことから、2024年の米国の農業機械市場で51%のシェアを維持します。このセグメントの収益成長は高馬力モデルによるものであり、コンパクトトラクターは特殊農業用途向けに電動ドライブトレインを搭載することが増えています。灌漑機器は、セグメントとしては小さいもの、2030年までCAGR 9.4%と最も高い成長率を達成すると予測されます。センターピボット、点滴ライン、センサー制御バルブなどの最新の灌漑システムは、リアルタイムの土壌水分データを統合し、水の消費量を最大25%削減します。この成長は、西部の州の地下水規制と連邦政府のWaterSMARTプログラムのインセンティブに合致しています。

耕うん・耕作システムにおいては、メーカーは土壌の破壊を減らすために深さ可変耕うん技術を取り入れ、不耕起農法の増加にもかかわらず安定した成長を維持しています。先進的な播種・植え付け機械は、正確な単一穀粒の配置を可能にし、出穂率を向上させ、正確な養分施用をサポートします。収穫機械の需要は連作作物価格と相関するが、予測対地速度自動化を特徴とする新しいコンバインは、燃費効率と処理能力を向上させ、買い替え需要を促進します。農家は、新しい機械を購入する代わりに、自律ガイダンスと可変レート・コントローラーを備えた既存の機械をアップグレードすることを選ぶようになっており、その結果、部品とデジタル・サービスの売上が機械の売上を上回っています。機器カテゴリー全体にわたって、センサーシステムとISOBUS互換コントローラーは、ブランドに依存しないエコシステムを確立し、メーカーのロックインを減らし、トラクター市場での地位を維持するために従来のメーカーがオープンAPIを提供することを要求しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 精密農業レトロフィット・キットの普及

- 主要OEMによる電動化ロードマップ

- テレマティクスに基づく予知保全の採用増加

- 気候スマート助成金インセンティブ

- オーダーメイド機器リース・モデルの急増

- 特殊作物をターゲットとするベンチャー企業によるロボット工学スタートアップ

- 市場抑制要因

- ディーラー技術者不足

- コネクテッド・マシナリー向け5Gカバレッジの地方における乏しさ

- 不安定な商品価格変動が農家の設備投資を抑制する

- 環境保護庁の第5次排出ガス規制対応に要する期間

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- トラクター

- 耕うん・耕作機械

- 耕うん機

- ハロー

- 耕運機および耕うん機

- その他の耕作・開墾機械

- 植え付け機械

- 種まき機

- プランター

- 散布機

- その他の植え付け機械

- 収穫機械

- コンバインハーベスター

- 飼料収穫機

- その他の収穫機械

- 牧草および飼料機械

- 草刈機

- ベーラー

- その他の牧草および飼料機械

- 灌漑機械

- スプリンクラー灌漑

- 点滴灌漑

- その他の灌漑機械

- その他の農業機械

- 農場規模別

- 500エーカー未満

- 500-2,000エーカー

- 2,000エーカー以上

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Ltd.

- CLAAS KGaA mbH

- KUHN SAS

- Same Deutz-Fahr S.P.A.

- Kinze Manufacturing

- Horsch, LLC

- Ploeger Oxbo Group B.V.

- Argo Tractors S.p.A.

- Netafim Limited(An Orbia Business)

- Valmont Industries, Inc.

- Yanmar Holdings Co., Ltd.