インドの石油・ガス-市場シェア分析、産業動向、成長予測(2025年~2030年)

India Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 95 Pages

- 納期

- 2~3営業日

- 商品コード

- 1639490

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

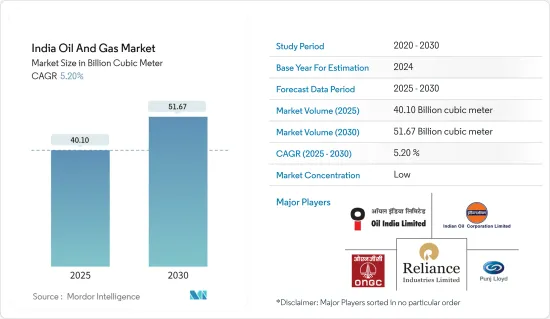

インドの石油・ガス市場規模は2025年に401億立方メートルと推定され、予測期間(2025~2030年)のCAGRは5.2%で、2030年には516億7,000万立方メートルに達すると予測されます。

COVID-19の発生による地域的な操業停止と石油精製品の需要減少に基づき、市場はマイナスの影響を受けました。現在、市場は流行前の水準まで回復しています。

主要ハイライト

- 天然ガスパイプライン容量の増加や石油製品需要の増加といった要因が、予測期間中のインドの石油・ガス市場を牽引するとみられます。また、石油・天然ガス市場はエネルギー市場の主要産業であり、世界の主要燃料として世界経済に影響力のある役割を果たしています。石油・ガスの生産と流通に関わるプロセスとシステムは非常に複雑で、資本集約的であり、最先端の技術を必要とします。

- しかし、国内需要を満たすための原油・天然ガスの輸入に大きく依存していることや、原油価格の変動が大きいことが、インドの石油・ガス市場の成長を妨げると予想されます。

- KG盆地では、ガスハイドレートが大量に発見されています。経済的に採掘可能なガスハイドレートは、企業にとって大きなビジネス機会となり、天然ガス生産量の増加につながる可能性があります。

インドの石油・ガス市場動向

下流部門が著しい成長を遂げる見込み

- インドのエネルギー需要は、今後20年間で50%成長すると予想されています。この需要の伸びは、世界人口の増加と発展途上国の生活水準の向上に起因しています。新エネルギーや再生可能エネルギーが世界中で普及しつつある石油燃料は依然として世界的に主要なエネルギー源です。この動向は今後数十年間続くと予想され、石油・ガス下流市場の成長に有利に働いています。

- 国内各地に新たな製油所の設立が決まった。例えば、2023年2月、Hindustan Petroleum Corp(HPCL)は、2024年1月までにラジャスタン州に年産900万トンのバルマー製油所と石油化学プロジェクトを開始する予定であると発表しました。

- 年度(2021~2022年)の同国の石油精製処理量は2億4,922万トンで、約2億3,397万トンだった2017年の数値から伸びた。この数値の増加は、モーターガソリンやディーゼルといった輸送用燃料の高い需要と、市場の住宅セグメントにおけるLPGの常に高い需要の結論です。

- 高い精製能力が求められるようになったもう1つの大きな要因は、国内、特にクリシュナ・ゴダヴァリ盆地とラジャスタン州のバルマー地方で油田が増加していることです。これらの油田からの天然ガス生産量が多いため、国内の製油所や石油化学コンビナートの能力が拡大しています。

- 今後予定されているいくつかの大型プロジェクトにより、下流部門は予測期間中に大きな成長を遂げることが予想されます。

中流部門への投資の増加が市場を牽引する可能性

- パイプラインは、天然ガス、原油、石油製品を長距離輸送する最も経済的な方法です。今後数年間、インドの石油・ガス市場では、中流部門がそれなりのシェアを占めると予想されます。

- 2022年3月現在、インドには約10,419kmの原油パイプライン(陸上:9,825km、海上:594km)、17,389kmの天然ガスパイプライン(陸上:1万7,365km、海上:24km)、1万4,729kmの石油精製品パイプラインがあり、IOCL、BORL、Cairn India、OIL、HMEL、ONGCによって運営されています。パイプラインに加え、インドには2022年3月現在、5つのLNG基地があります。

- 2022年2月、インド政府は国内生産量を増やすため、石油・ガスの探鉱面積を2025年までに50万平方キロ、2030年までに100万平方キロに倍増すると発表しました。

- 2022年6月30日現在、Gas Authority of India Ltd(GAIL)は3万3,815kmの天然ガスパイプライン網で最大のシェアを占めています。

- 2022年現在、インドの原油パイプライン網の50.88%(1万5,113km)をIndian Oil Corporationが占めています。インド政府は、国内のガスパイプライン網を拡大するために99億7,000万米ドルを投資する予定であり、市場の成長に拍車をかけています。

- 2022年3月、ndian Oil Corporation(IOC)は、9つの地域における都市ガス配給(CGD)ネットワークの開発に9億3,260万米ドルを投資することを承認しました。

- したがって、中流部門への投資の増加がインドの石油・ガス市場を牽引しています。パイプラインのカバー率は予測期間中に大幅に増加すると予想され、石油製品パイプラインはこのセグメントで最も増加すると予想されます。

インドの石油・ガス産業概要

インドの石油・ガス市場は断片的です。主要参入企業(順不同)には、Oil and Natural Gas Corporation(ONGC)、Oil India Limited(OIL)、Reliance Industries、Indian Oil Corporation Limited(IOCL)、Punj Lloyd Limited.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの天然ガス生産量予測(単位:1億立方メートル)

- 2028年までの原油生産量予測(単位:1億立方メートル)

- 2028年までの製油所設置容量と予測(単位:1,000バレル/日)

- 2028年までのLNGターミナル設置容量(MTPA)と予測

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- PESTLE分析

第5章 市場セグメンテーション

- セクター

- 上流

- 展開場所

- オンショア

- オフショア

- 下流

- 製油所

- 石油化学プラント

- 中流

- 輸送

- 貯蔵

- LNGターミナル

- 上流

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 市場シェア分析

- 企業プロファイル

- Oil and Natural Gas Corporation

- Oil India Limited

- Reliance Industries

- Indian Oil Corporation Limited

- Punj Lloyd Limited

- Bharat Petroleum Corporation Limited

- GAIL (India) Limited

- Hindustan Petroleum Corporation Limited

- Cairn India

第7章 市場機会と今後の動向

目次

The India Oil And Gas Market size is estimated at 40.10 billion cubic meter in 2025, and is expected to reach 51.67 billion cubic meter by 2030, at a CAGR of 5.2% during the forecast period (2025-2030).

The market was negatively impacted by the outbreak of COVID-19 due to regional lockdowns and a decline in demand for refined petroleum products. Currently, the market has rebounded to pre-pandemic levels.

Key Highlights

- Factors such as the increasing natural gas pipeline capacity and the increasing demand for petroleum products are expected to drive the Indian oil and gas market during the forecast period. Also, the oil and natural gas market is a major industry in the energy market and plays an influential role in the global economy as the world's primary fuel source. The processes and systems involved in producing and distributing oil and gas are highly complex, capital-intensive, and require state-of-the-art technology.

- However, a huge dependence on imports of crude oil and natural gas to satisfy domestic demand and the high volatility of crude oil prices are expected to hinder the growth of the Indian oil and gas market.

- There have been significant gas hydrate discoveries in the KG Basin. Economically feasible extraction of the gas hydrates may create immense opportunities for the companies, which may lead to a boom in natural gas production.

India Oil and Gas Market Trends

The Downstream Sector is Expected to Witness Significant Growth

- Indian energy demand is anticipated to grow by 50% in the next two decades. This growth in demand can be attributed to the growing world population and an improvement in living standards in developing countries. Even though new and renewable energy sources are gaining popularity around the world, petroleum fuel remains a major energy source globally. This trend is expected to continue for the next few decades and favors the growth of the oil and gas downstream market.

- New refineries were set to be established in various parts of the country. For instance, in February 2023, Hindustan Petroleum Corp (HPCL) announced that the company plans to start its 9 million tonne-a-year Barmer refinery and petrochemical project in Rajasthan state by January 2024.

- The country's oil refinery throughput in the fiscal year (2021-2022) was 249.22 million metric tons, a growth from the 2017 figures, which were around 233.97 million metric tons. The increased value is the conclusion of the high demand for transport fuels like motor gasoline and diesel and the constantly high demand for LPG in the market's residential segment.

- The other major factor that has led to the requirement of high refining capacity is the increasing number of fields in the country, especially in the Krishna-Godavari Basin and Barmer Region of Rajasthan State. The high natural gas production from these fields has led to an expansion in the capacity of refineries and petrochemical complexes in the country.

- Owing to several major upcoming projects, the downstream sector is expected to witness significant growth during the forecast period.

Increasing Investment in the Midstream Sector May Drive the Market

- The pipeline is the most economical way of transporting natural gas, crude oil, and petroleum products over a long distance due to increasing investments in upcoming pipelines in the country. The midstream segment is expected to contribute a decent share in the Indian oil and gas market in the coming years.

- As of March 2022, the country had around 10,419 km of crude oil pipelines (onshore: 9,825 km and offshore: 594 km), 17,389 km of natural gas pipelines (onshore: 17,365 km and offshore: 24 km), and 14,729 km of refined products pipelines, being operated by IOCL, BORL, Cairn India, OIL, HMEL, and ONGC. In addition to the pipelines, India had 5 LNG terminals in March 2022.

- In February 2022, the government of India announced to double its exploration area of oil and gas to 0.5 million sq. km. by 2025 and to 1 million sq. km. by 2030 with a view to increasing domestic output.

- As of June 30, 2022, the Gas Authority of India Ltd (GAIL) had the largest share of the country's natural gas pipeline network, i.e., 33,815 km.

- As of 2022, Indian Oil Corporation accounted for 50.88% (15113 km) of India's crude pipeline network. The Indian government is set to invest USD 9.97 billion to expand the gas pipeline network across the country, culminating in the growth of the market.

- In March 2022, Indian Oil Corporation (IOC) Limited approved to invest USD 932.6 million for the development of City Gas Distribution (CGD) network in 9 geographical areas.

- Hence, increasing investments in the midstream sector have driven the India oil and gas market. Pipeline coverage is expected to increase substantially during the forecast period, with the petroleum product pipeline expected to increase the most in the segment.

India Oil and Gas Industry Overview

The India oil and gas market is fragmanted. Some of the key players (in no particular order) include Oil and Natural Gas Corporation (ONGC), Oil India Limited (OIL), Reliance Industries, Indian Oil Corporation Limited (IOCL), and Punj Lloyd Limited., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Natural Gas Production Forecast in billion cubic meters, till 2028

- 4.3 Crude Oil Production Forecast in billion cubic meters, till 2028

- 4.4 Refinery Installed Capacity and Forecast in thousand barrels per day, till 2028

- 4.5 LNG Terminals Installed Capacity and Forecast in MTPA, till 2028

- 4.6 Recent Trends and Developments

- 4.7 Government Policies and Regulations

- 4.8 Market Dynamics

- 4.8.1 Drivers

- 4.8.2 Restraints

- 4.9 Supply Chain Analysis

- 4.10 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Sector

- 5.1.1 Upstream

- 5.1.1.1 Location of Deployment

- 5.1.1.1.1 Onshore

- 5.1.1.1.2 Offshore

- 5.1.2 Downstream

- 5.1.2.1 Refineries

- 5.1.2.2 Petrochemical Plants

- 5.1.3 Midstream

- 5.1.3.1 Transportation

- 5.1.3.2 Storage

- 5.1.3.3 LNG Terminals

- 5.1.1 Upstream

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Oil and Natural Gas Corporation

- 6.4.2 Oil India Limited

- 6.4.3 Reliance Industries

- 6.4.4 Indian Oil Corporation Limited

- 6.4.5 Punj Lloyd Limited

- 6.4.6 Bharat Petroleum Corporation Limited

- 6.4.7 GAIL (India) Limited

- 6.4.8 Hindustan Petroleum Corporation Limited

- 6.4.9 Cairn India

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 95 Pages

- 納期

- 2~3営業日