|

市場調査レポート

商品コード

1640341

英国の石油およびガス:市場シェア分析、産業動向、成長予測(2025年~2030年)United Kingdom Oil And Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 英国の石油およびガス:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

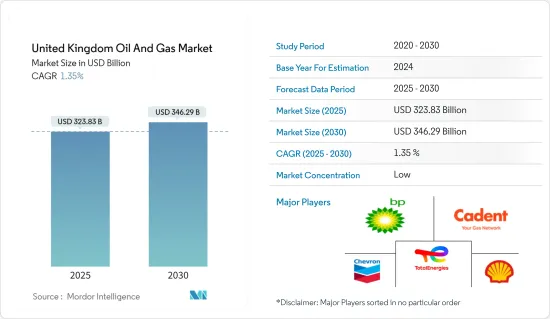

英国の石油およびガス市場規模は2025年に3,238億3,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは1.35%で、2030年には3,462億9,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、同国の石油およびガス生産の増加と石油およびガスインフラ開発への投資の増加が、予測期間中の市場調査を推進するとみられます。

- 一方、再生可能エネルギー技術の成長と最近の地政学的動向による石油およびガス価格の変動は、予測期間中の市場開拓を抑制すると予想されます。

- とはいえ、国中で新たな石油およびガス田が発見されれば、予測期間中に調査対象市場に大きなビジネスチャンスが生まれると期待されています。

英国の石油およびガス市場動向

上流セグメントが市場を独占する見込み

- 英国は、北海にかなりの石油およびガス埋蔵量を有しており、数十年にわたり主要な生産源となってきました。埋蔵量は減少しているもの、現在も継続的な探鉱・生産努力が必要な相当量の資源を有しています。

- 英国は、北海における海洋探査・生産のためのインフラが十分に発達しています。このインフラには、海上プラットフォーム、パイプライン、貯蔵施設が含まれます。こうしたインフラの存在は、石油およびガス資源の効率的な採掘と輸送を可能にするため、上流企業に競争上の優位性をもたらします。

- さらに、英国は北海におけるオフショア石油およびガス事業の長い歴史を有しており、その結果、石油およびガス資源の探査・生産に関する重要な技術的専門知識が開発されました。業界は、掘削技術、油層管理、生産最適化などの分野で知識と経験を蓄積してきました。こうした専門知識により、英国は石油上流事業において優位に立っています。

- 世界エネルギー統計レビューによると、2022年の英国の原油生産量は日量77万8,000バレルで、2021年に比べてほぼ11%減少しました。この減少の主な理由は、北海の埋蔵量の減少です。これに対抗するため、英国の企業は他の地域の石油およびガス生産の探査を開始しています。

- 例えば、2023年2月、英国の地元上流企業であるデルタ・エナジー社は、ライセンスP2252のペンサコーラ地域で重要な石油およびガスを発見したと発表しました。同社は、潜在的な天然ガス貯留層には300bcf以上の天然ガスが存在するとしています。

- したがって、上記の点から、予測期間中、英国の上流部門が石油およびガス市場を独占すると予想されます。

再生可能エネルギーの成長が市場を抑制する見通し

- 英国は、低炭素経済への移行という野心的な目標を掲げています。カーボンプライシング、再生可能エネルギーへのインセンティブ、排出基準の厳格化といった政府の政策と規制は、再生可能エネルギーの開発と採用を促進するためのものです。これらの政策は、特に発電や輸送など再生可能エネルギーによる代替が可能な分野において、石油およびガス需要を減少させる可能性があります。

- さらに、再生可能エネルギー部門が拡大し続けるにつれ、多額の投資が集まるようになります。このため、石油およびガス産業から資金が流出し、従来の石油およびガス・プロジェクトが資金を確保することがより困難になる可能性があります。投資家は、再生可能エネルギー・プロジェクトの方が長期的に財務的に実行可能であり、環境的にも持続可能であると見なし、新規の石油およびガス探査・生産プロジェクトへの投資が減少する可能性があります。

- 例えば、国際再生可能エネルギー機関によると、2022年、英国の再生可能エネルギー設備容量は2021年比で7%以上増加しました。2022年の再生可能エネルギー設備容量は、2021年の4,890万kWに対し、5,200万kWを超えました。

- 2022年12月、ヴェスタスは、英国のInfinergyが所有するLimekilnプロジェクト向けに108MWを受注したと発表しました。業務範囲には、V136-4.5MWタービンの設置、供給、試運転が含まれます。タービンの総数は24基近くになります。設置と試運転は2024年までに完了する予定です。

- 再生可能エネルギーの成長は、石油およびガスなどの化石燃料の需要減少につながる可能性があります。風力、太陽光、水力などの再生可能エネルギー源は、コスト競合が激化しており、より環境に優しいと考えられています。このようなエネルギー消費パターンの転換は、特に再生可能エネルギーへの転換が容易な分野では、石油およびガス全体の需要を減少させることができます。

- 従って、上述の指摘の通り、再生可能エネルギー源の適応の増加は、予測期間中の英国石油およびガス市場の成長を妨げると予想されます。

英国の石油およびガス産業の概要

英国の石油およびガス市場は断片化されています。同市場の主要企業(順不同)には、Shell PLC、BP PLC、TotalEnergies SE、Chevron Corporation、Cadent Gas Ltd.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模および需要予測(単位:米ドル)

- 石油・天然ガスの生産量と2028年までの予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 国内の石油およびガス生産量

- 石油およびガスインフラ開発への投資

- 抑制要因

- 再生可能エネルギーの成長

- 促進要因

- サプライチェーン分析

- PESTLE分析

第5章 市場セグメンテーション

- セクター別

- アップストリーム

- ミッドストリーム

- ダウンストリーム

第6章 競争情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Shell PLC

- BP PLC

- TotalEnergies SE

- Chevron Corporation

- Cadent Gas Ltd

- ESSO UK Limited

- BG Group Limited

- Valaris PLC

- Centrica PLC

- Dana Petroleum E&P Limited

第7章 市場機会と今後の動向

- 新たな石油およびガス田の発見

目次

Product Code: 51677

The United Kingdom Oil And Gas Market size is estimated at USD 323.83 billion in 2025, and is expected to reach USD 346.29 billion by 2030, at a CAGR of 1.35% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the country's increasing oil and gas production and increasing investments in oil and gas infrastructure developments are expected to drive the market studied during the forecast period.

- On the other hand, the growth of renewable energy technologies and volatility in oil and gas prices due to recent geopolitical developments are expected to restrain the growth of the market studied during the forecast period.

- Nevertheless, the discovery of new oil and gas fields across the country is expected to create significant opportunities in the market studied during the forecast period.

UK Oil & Gas Market Trends

Upstream Segment Expected to Dominate the Market

- The United Kingdom has significant oil and gas reserves in the North Sea, which have been a major production source for several decades. Although the reserves have declined, they still present a substantial resource base that requires ongoing exploration and production efforts.

- The United Kingdom has a well-developed infrastructure for offshore exploration and production in the North Sea. This infrastructure includes offshore platforms, pipelines, and storage facilities. The presence of this infrastructure provides a competitive advantage for upstream companies as it enables efficient extraction and transportation of oil and gas resources.

- Moreover, the United Kingdom has a long history of offshore oil and gas operations in the North Sea, resulting in the development of significant technical expertise in the exploration and production of oil and gas resources. The industry has accumulated knowledge and experience in areas such as drilling techniques, reservoir management, and production optimization. This expertise gives the United Kingdom an advantage in upstream activities.

- According to the statistical review of world energy, the United Kingdom produced 778 thousand barrels per day of crude oil in 2022, a decrease of almost 11% compared to 2021. The primary reason for this decline is the declining reserves in the North Sea. To counter this, companies in the United Kingdom have started exploring other regions for oiling gas production.

- For instance, in February 2023, Delta Energy, a local upstream player in the United Kingdom, announced that they had made a significant oil and gas discovery at the Pensacola region on license P2252. The company claims that the potential natural gas reservoir has more than 300 bcf of natural gas in the reservoir.

- Therefore, as per the points mentioned above, the upstream sector in the United Kingdom is expected to dominate the oil and gas market during the forecast period.

Growth of Renewables Expected to Restrain the Market

- The United Kingdom has set ambitious targets to transition to a low-carbon economy. Government policies and regulations such as carbon pricing, renewable energy incentives, and stricter emission standards are designed to promote the development and adoption of renewable energy sources. These policies may reduce demand for oil and gas, particularly in sectors where renewable alternatives are feasible, such as power generation and transportation.

- Moreover, as the renewable energy sector continues to expand, it attracts significant investment. This can divert capital from the oil and gas industry, making it more challenging for traditional oil and gas projects to secure funding. Investors may view renewable energy projects as more financially viable and environmentally sustainable in the long term, leading to a reduction in investment in new oil and gas exploration and production projects.

- For instance, according to the International Renewable Energy Agency, in 2022, the installed renewable energy capacity in the United Kingdom increased by more than 7% compared to 2021. In 2022, the total renewable energy installed capacity crossed 52 GW compared to 48.9 GW in 2021.

- In December 2022, Vestas announced that it had received an order for 108 MW for the Limekiln project owned by Infinergy in the United Kingdom. The work scope includes installing, supplying, and commissioning V136-4.5 MW turbines. The total number of turbines is nearly 24. The installation and commissioning is expected to be completed by 2024.

- The growth of renewable energy can lead to a decline in demand for fossil fuels, including oil and gas. Renewable energy sources such as wind, solar and hydroelectric power are becoming increasingly cost-competitive and are considered more environment-friendly. This shift in energy consumption patterns can reduce the overall demand for oil and gas, particularly in sectors that can readily switch to renewable alternatives.

- Therefore, as per the points discussed above, the increasing adaption of renewable energy sources is expected to hinder the growth of the UK oil and gas market during the forecast period.

UK Oil & Gas Industry Overview

The UK oil and gas market is fragmented. Some of the key players in the market (in no particular order) include Shell PLC, BP PLC, TotalEnergies SE, Chevron Corporation, and Cadent Gas Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Crude Oil and Natural Gas Production and Forecast, till 2028

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Domestic Oil and Gas Production

- 4.6.1.2 Investments in Oil and Gas Infrastructure Development

- 4.6.2 Restraints

- 4.6.2.1 Growth of Renewable Energy

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Shell PLC

- 6.3.2 BP PLC

- 6.3.3 TotalEnergies SE

- 6.3.4 Chevron Corporation

- 6.3.5 Cadent Gas Ltd

- 6.3.6 ESSO UK Limited

- 6.3.7 BG Group Limited

- 6.3.8 Valaris PLC

- 6.3.9 Centrica PLC

- 6.3.10 Dana Petroleum E&P Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Discovery of New Oil and Gas Fields