アジア太平洋地域のEV用ニッケル水素電池:市場シェア分析、産業動向、成長予測(2025~2030年)

Asia Pacific Nickel Metal Hydride Battery For Electric Vehicle Application - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1636537

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

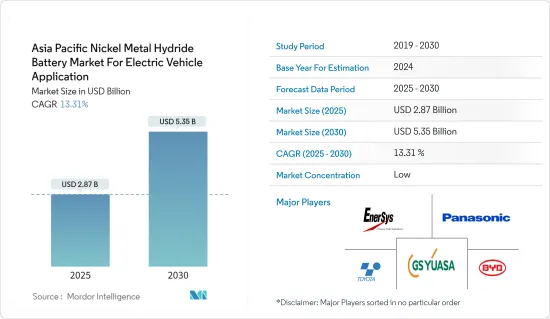

アジア太平洋地域のEV用ニッケル水素電池市場は、2025年の28億7,000万米ドルから2030年には53億5,000万米ドルに成長すると予測、予測期間(2025-2030年)のCAGRは13.31%です。

主なハイライト

- 中期的には、ハイブリッド電気自動車(HEV)の普及の高まりと、中国、インド、日本などの国々における補助金や税制優遇措置などのEV普及促進政策が、予測期間中の電気自動車用途のニッケル水素電池市場の需要を牽引すると予想されます。

- 一方、リチウムイオン技術の急速な進歩とコスト削減は、今後数年間の市場成長の妨げになると予想されます。

- とはいえ、APACの各国政府は電池のリサイクル・インフラに投資しており、リサイクル・プロセスが容易なニッケル水素電池は、近い将来、電気自動車用途のニッケル水素電池市場に大きな機会をもたらすと予想されます。

- 予測期間中、ハイブリッド車に対する政府の補助金が増加するため、アジア太平洋地域のEV用ニッケル水素電池市場ではインドが最も急成長する地域になると予想されます。

アジア太平洋地域のニッケル水素電池市場動向

リチウムイオン技術の急速な進歩とコスト削減が市場を抑制

- リチウムイオン(Li-ion)技術の進歩と生産コストの着実な低下により、アジア太平洋地域(APAC)地域の電気自動車(EV)用ニッケル水素(NiMH)電池市場が再構築されています。EV市場がバッテリー電気自動車(BEV)に軸足を移す中、優れたエネルギー密度、効率、価格低下により、リチウムイオン電池が好まれています。

- さらに、アジア太平洋地域(APAC)地域では、航続距離の延長、優れたエネルギー効率、コストの低下により、リチウムイオン電池を搭載した完全電気自動車(EV)が普及しています。ブルームバーグNEFの報告によると、2023年のバッテリー価格は大幅に急落し、139米ドル/kWhに達し、13%以上の下落を記録しました。継続的な技術の進歩や製造プロセスの改善を考慮すると、予測ではさらに下落し、2025年には113米ドル/kWh、2030年には80米ドル/kWhという野心的な目標を目指しています。

- 加えて、中国、日本、韓国などの国々は一貫してリチウムイオン技術に投資しており、技術革新を推進し、リチウムイオン電池をニッケル水素電池よりもコスト効率と適応性を高めています。

- 例えば、中国は2024年5月に、電気自動車(EV)用の次世代電池技術の進歩に約60億元(8億4,500万米ドル)を投資する予定です。最先端技術であるASSBは、固体電解質を利用することで従来のリチウムイオン電池(LIB)を強化します。このような投資は、アジア太平洋地域におけるリチウムイオン電池の成長を強化すると予想される一方、予測期間中はニッケル水素電池の拡大を抑制する可能性があります。

- さらに、その優れたエネルギー密度、急速充電能力、適応性により、自動車メーカーは最新のハイブリッドモデルや完全電気自動車モデルにリチウムイオン電池を徐々に組み込んでおり、同地域ではニッケル水素電池が敬遠されがちです。

- しかし、ニッケル水素電池はリチウムイオン電池よりもリサイクルしやすく、APAC地域全体で持続可能性を重視する傾向が強まっています。リサイクル技術とインフラの進歩により、ニッケル水素市場は予測期間中、一部の用途で長寿を見出す可能性があります。

- したがって、リチウムイオン技術の急速な進歩とコスト削減は、予測期間中、アジア太平洋地域のEVバッテリー市場の状況を根本的に変えています。

著しい成長を遂げるインド

- インドの電気自動車(EV)用途のニッケル水素(NiMH)電池市場は、リチウムイオン電池の優位性と比較するとニッチです。これらのニッケル水素電池は、安全性が高く、ライフサイクルが長く、幅広い温度範囲で効率的な性能を発揮するため、主にハイブリッド電気自動車(HEV)やその他のEVに応用されています。

- ニッケル水素電池は、優れた熱安定性と高温への耐性により、インドの厳しい気候条件下で好まれ、リチウムイオン電池を上回っています。ニッケル水素電池を搭載したEVの需要は、近年大幅に急増しています。電気自動車工業会(SMEV)によると、2024年10月までに全国のEV販売台数は4万9,306台に達します。販売台数は2020年度から24年度にかけて37倍に急増しており、政府の政策やイニシアティブに後押しされ、今後数年間でさらなる成長が見込まれています。

- さらに、電気自動車の早期導入・製造(FAME)制度や、ハイブリッド車のGST引き下げといった政策が、ハイブリッド車へのニッケル水素電池技術の採用を間接的に後押ししました。さまざまな州政府が、ハイブリッド車やバッテリー電気自動車を促進するためのいくつかの制度を全国で発表しました。

- 例えば、2024年7月、インドのウッタル・プラデーシュ州政府は、ハイブリッド車に対する道路税の免除を発表しました。この政策は、クリーンカーの導入を奨励し、従来のガソリン車やディーゼル車が環境に与える影響を軽減することを目的としています。このような取り組みにより、地域全体でハイブリッド乗用車が普及し、今後数年間でニッケル水素電池の需要が高まる可能性が高いです。

- インドでは、ハイブリッド車が内燃機関車(ICE)と完全な電気自動車との橋渡し役と見なされるようになっています。トヨタやマルチ・スズキをはじめとする大手自動車メーカーがハイブリッドモデルを展開しており、ニッケル水素電池の需要を押し上げています。

- その一例として、2024年10月、ヒュンダイ・モーター・インディア・リミテッド(HMIL)は、今後数年間にインドでハイブリッド車を発売する戦略を発表しました。同社の拡大計画は、2025年までに17万台の初期増強、2028年までにさらに8万台という2段階で展開されます。これらの構想は、ハイブリッドEV部門を強化し、予測期間中にニッケル水素電池に大きなチャンスをもたらします。

- したがって、こうした取り組みや計画によって、予測期間中、地域全体のEV販売が強化され、ニッケル水素電池の需要が高まる可能性が高いです。

アジア太平洋地域のニッケル水素電池産業の概要

アジア太平洋地域のEV用ニッケル水素電池市場は半分断されています。主なプレーヤー(順不同)は、パナソニック株式会社、豊田自動織機株式会社、BYD Company Limited、GSユアサ株式会社、EnerSysなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- ハイブリッド電気自動車の普及拡大

- EVに対する補助金と税制優遇措置の急増

- 抑制要因

- リチウムイオン技術の急速な進歩とコスト削減

- 促進要因

- サプライチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 推進タイプ別

- バッテリー電気自動車

- ハイブリッド電気自動車

- プラグインハイブリッド電気自動車

- 燃料電池電気自動車

- 車両タイプ別

- 乗用車

- 商用車

- 地域別

- 中国

- インド

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Panasonic Corporation

- Toyota Industries Corporation

- Primearth EV Energy Co., Ltd.

- GS Yuasa Corporation

- Samsung SDI Co., Ltd.

- Hitachi, Ltd.

- BYD Company Limited

- EnerSys

- Toshiba Corporation

- LG Energy Solution

- その他の有名企業一覧

- 市場ランキング分析

第7章 市場機会と今後の動向

- 確立された電池リサイクルプロセスの革新

目次

Product Code: 50003954

The Asia Pacific Nickel Metal Hydride Battery Market For Electric Vehicle Application Industry is expected to grow from USD 2.87 billion in 2025 to USD 5.35 billion by 2030, at a CAGR of 13.31% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, the rising adoption of hybrid electric vehicles (HEV) and policies promoting EV adoption, such as subsidies and tax incentives in countries like China, India, and Japan, are expected to drive the demand for nickel metal hydride battery market for electric vehicle application during the forecast period.

- On the other hand, rapid advancement and cost reduction in lithium-ion technology are expected to hinder market growth in the upcoming years.

- Nevertheless, governments in APAC are investing in battery recycling infrastructure, and NiMH batteries, with their easier recycling process, are expected to create significant opportunities for the nickel metal hydride battery market for electric vehicle applications in the near future.

- India is expected to be the fastest-growing region in Asia Pacific's nickel metal hydride battery market for electric vehicle applications due to rising government subsidies for hybrid vehicles during the forecast period.

Asia Pacific Nickel Metal Hydride Battery Market Trends

Rapid Advancement and Cost Reduction in Lithium-ion Technology are Restrain the Market

- The advancements in lithium-ion (Li-ion) technology and a steady decline in production costs have reshaped the nickel-metal hydride (NiMH) battery market for electric vehicles (EVs) in the Asia-Pacific (APAC) region. With the EV market pivoting towards battery electric vehicles (BEVs), lithium-ion batteries are preferred due to their superior energy density, efficiency, and falling prices.

- Moreover, in the Asia-Pacific (APAC) region, fully electric vehicles (EVs) powered by lithium-ion batteries are popular owing to their extended ranges, superior energy efficiency, and decreasing costs. Bloomberg NEF reported that 2023 battery prices took a significant plunge, landing at USD 139/kWh and marking a drop of over 13%. Given the continuous technological advancements and enhancements in manufacturing processes, forecasts indicate a further dip, aiming for USD 113/kWh by 2025 and an ambitious target of USD 80/kWh by 2030.

- In addition, countries such as China, Japan, and South Korea have consistently invested in lithium-ion technology, driving innovation and rendering lithium-ion batteries more cost-effective and adaptable than NiMH batteries.

- For instance, in May 2024, China is set to invest approximately 6 billion yuan (USD 845 million) into advancing next-generation battery technology for electric vehicles (EVs). ASSBs, a cutting-edge technology, enhance traditional lithium-ion batteries (LIBs) by utilizing a solid electrolyte. Such investments are anticipated to bolster the growth of lithium-ion batteries across the Asia-Pacific region, while potentially curbing the expansion of nickel-metal hydride (NiMH) batteries during the forecast period.

- Further, due to their superior energy density, quicker charging capabilities, and adaptability, automakers are progressively integrating lithium-ion batteries into their latest hybrid and fully electric models, often sidelining NiMH batteries in the region.

- However, NiMH batteries boast easier recyclability than their lithium-ion counterparts, resonating with the increasing emphasis on sustainability across the APAC region. With advancements in recycling technologies and infrastructure, the NiMH market could find longevity in select applications during the forecast period.

- Hence, the rapid advancements and cost reductions in lithium-ion technology have fundamentally reshaped the landscape of the Asia-Pacific battery market for EV applications during the forecast period.

India to Witness Significant Growth

- India's market for nickel-metal hydride (NiMH) batteries in electric vehicle (EV) applications remains niche when juxtaposed with the dominance of lithium-ion batteries. These NiMH batteries are primarily applied in hybrid electric vehicles (HEVs) and other EVs owing to their strong safety profile, extended lifecycle, and efficient performance across a broad temperature spectrum.

- NiMH batteries are favored in India's challenging climatic conditions for their superior thermal stability and resilience to high temperatures, outpacing lithium-ion batteries. Demand for NiMH battery-powered EVs has surged significantly in recent years. According to the Society of Manufacturers of Electric Vehicles (SMEV), by October 2024, EV sales nationwide reached 49,306 units. Sales have skyrocketed 37 times from FY20 to FY24, with further growth anticipated in the coming years, bolstered by government policies and initiatives.

- Furthermore, policies such as the Faster Adoption and Manufacturing of Electric Vehicles (FAME) scheme and a reduced GST on hybrid vehicles indirectly bolstered the adoption of NiMH battery technology in hybrids. The various state governments announced several schemes to promote hybrid and battery electric vehicles across the country.

- For instance, in July 2024, the Uttar Pradesh government of India announced a waiver of road tax on hybrid cars. This policy aims to encourage the adoption of clean vehicles and reduce the environmental impact of traditional gasoline and diesel-powered cars. Such initiatives are likely to promote hybrid passenger cars across the region and raise the demand for NiMH batteries in the coming years.

- In India, hybrid vehicles are increasingly seen as a bridge between internal combustion engine (ICE) and fully electric vehicles. Major automotive players, including Toyota and Maruti Suzuki, are rolling out hybrid models, boosting the demand for NiMH batteries.

- As a case in point, in October 2024, Hyundai Motor India Limited (HMIL) unveiled its strategy to launch hybrid vehicles in India over the next few years. The company's expansion plan unfolds in two phases: an initial boost of 170,000 units by 2025 and another 80,000 units by 2028. These initiatives are poised to elevate the hybrid EV sector, presenting a significant opportunity for NiMH batteries during the forecast period.

- Hence, these initiatives and plans are likely to enhance EV sales across the region and raise the demand for NiMH batteries during the forecast period.

Asia Pacific Nickel Metal Hydride Battery Industry Overview

Asia Pacific's nickel metal hydride battery market for electric vehicle applications is semi-fragmented. Some key players (not in particular order) are Panasonic Corporation, Toyota Industries Corporation, BYD Company Limited, GS Yuasa Corporation, and EnerSys, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growing Adoption of Hybrid Electric Vehicles

- 4.5.1.2 Surge in Subsidies and Tax Incentives for EVs

- 4.5.2 Restraints

- 4.5.2.1 Rapid Advancement and Cost Reduction in Lithium-ion Technology

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Propulsion Type

- 5.1.1 Battery Electric Vehicles

- 5.1.2 Hybrid Electric Vehicles

- 5.1.3 Plug-In Hybrid Electric Vehicles

- 5.1.4 Fuel Cell Electric Vehicles

- 5.2 Vehicle Type

- 5.2.1 Passenger Vehicles

- 5.2.2 Commercial Vehicles

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 South Korea

- 5.3.4 ASEAN Countries

- 5.3.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Panasonic Corporation

- 6.3.2 Toyota Industries Corporation

- 6.3.3 Primearth EV Energy Co., Ltd.

- 6.3.4 GS Yuasa Corporation

- 6.3.5 Samsung SDI Co., Ltd.

- 6.3.6 Hitachi, Ltd.

- 6.3.7 BYD Company Limited

- 6.3.8 EnerSys

- 6.3.9 Toshiba Corporation

- 6.3.10 LG Energy Solution

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Innovation in Established Battery Recycling Processes

アジア太平洋地域のEV用ニッケル水素電池:市場シェア分析、産業動向、成長予測(2025~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日