|

市場調査レポート

商品コード

1690193

イタリアの医薬品:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Italy Pharmaceutical - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| イタリアの医薬品:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 80 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

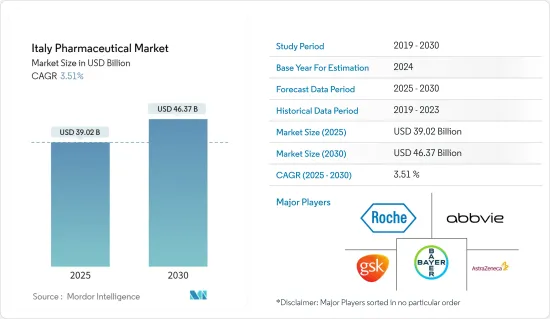

イタリアの医薬品の市場規模は2025年に390億2,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは3.51%で、2030年には463億7,000万米ドルに達すると予測されます。

イタリアは世界有数の医薬品市場です。

COVID-19の大流行は前例のない健康問題であり、世界中の地域社会、産業、企業、生活に悪影響を及ぼしています。多くの企業はすでにSars-CoV-2ウイルスに対するワクチンの承認を得ており、現在もCOVID-19に対する治療薬の開発に研究開発に注力しています。COVID-19の直接的かつ直接的な潜在的影響により、すでに数百万人の命が失われ、ヘルスケアコストが大幅に増加しています。ワクチンが開発される前に複数の潜在的な医薬品が試され、コロナウイルスによる感染症の治療に使用されているため、それによって他の病状が発生し、市場が補完されると予想されています。例えば、ロピナビル/リトナビル、ヒドロキシクロロキン(HCQ)、レムデシビルなどの医薬品は、世界の多くの国でコロナウイルス感染症の治療に再利用されています。イタリアは生産施設の数が最も多い国であるため、閉鎖により労働力が不足し、生産量が減少したことが、同産業の市場成長を妨げています。

近年、イタリアの医薬品産業は、成長、付加価値、貿易、投資の面で著しく拡大しています。調査に関しては、イタリアは欧州連合(EU)全体で認可された臨床試験件数の約18%を占めています。長年にわたり、糖尿病、がんなどの多くの慢性疾患や感染症の有病率や発症率は世界中で何倍にも増加しており、これが世界中で医薬品の高い需要につながっているため、研究市場の成長を牽引しています。

しかし、今後数年間、イタリアの医薬品部門は様々な障害を受ける可能性があります。GDPと比較したイタリア国の債務の増加、国の恵まれない成長軌道は、国の資金の流れを減少させる可能性があります。

イタリアの医薬品市場動向

処方薬部門が最大のシェアを占め、予測期間中も同様と予想

イタリアの処方薬部門は、予測期間中最大のシェアを占めると予測されます。この分野の成長要因は、技術、規制状況、製薬メーカーのRx医薬品志向、新薬の発売などです。

処方薬は、処方医による有効な処方箋があれば入手できます。これらの医薬品は規制が厳しく、医師の診察、診断が必要であり、薬が効いているか、安全に効いているかを確認するために医師によるモニタリングが必要です。医師が処方箋を書く際には、患者の現在の状態、服用している他の薬、バイタル統計、薬物アレルギーなど、患者に関する多くの情報が考慮されます。そのため、ある人にとっては安全で効果的な処方薬でも、別の人にとっては危険な場合があるのです。さらに、人口の増加、心血管疾患やがんなどの慢性疾患の増加も、この市場の成長に寄与しています。さらに、同国における一人当たり医療費の増加とともに、人々の裁量所得の増加も、2020年~2025年の予測期間中、処方薬セグメントの市場成長を牽引すると予想されます。

新たな臨床試験、研究開発費の増加、製品上市の増加、世界の疾病負担の増大は、予測期間中に処方薬セグメントを牽引すると予想される要因です。例えば、2021年8月、米国のZydus Pharmaceuticals Inc.は、Italfarmaco Groupの子会社であるイタリアのCHEMI SpAと、ロベノックス(エノキサパリンナトリウム注射液)のジェネリック同等品(7種類の用法・用量)を米国で発売するためのライセンス・供給契約を締結しました。ロベノックス(エノキサパリンナトリウム注射液)は、腹部、股関節、膝関節の置換手術を受ける患者に使用されます。このように、上記の要因により、医療用医薬品セグメントは市場成長に大きく貢献すると予想されます。

イタリアの医薬品産業概要

イタリアの医薬品市場は競争が激しく、複数の大手企業が参入しています。市場シェアの面では、現在、少数の大手企業が市場を独占しています。また、一部の大手企業は、同国での市場ポジションを強化するため、他社との買収や合弁を精力的に行っています。現在市場を独占している主要企業には、AbbVie Inc.、AstraZeneca plc、Bayer AG、C.H. Boehringer Sohn AG &Ko.KG、グラクソ・スミスクラインplcです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 研究開発費の増加

- 慢性疾患罹患率の上昇

- 市場抑制要因

- 薬剤コストの高騰

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- ATC/治療クラス別

- 血液・造血器系

- 循環器系

- 皮膚科学

- 消化器系および代謝系

- 神経系

- 呼吸器系

- その他

- 薬剤タイプ別

- ブランド

- ジェネリック

- 処方タイプ別

- 処方薬(Rx)

- OTC薬

第6章 競合情勢と企業プロファイル

- 企業プロファイル

- AbbVie Inc.

- AstraZeneca plc

- Bayer AG

- C.H. Boehringer Sohn AG & Ko. KG

- GlaxoSmithKline plc

- F. Hoffmann-La Roche AG

- Bristol Myers Squibb Company

- Eli Lilly and Company

- Merck & Co., Inc.

- Sanofi S.A.

第7章 市場機会と将来動向市場機会と今後の動向

The Italy Pharmaceutical Market size is estimated at USD 39.02 billion in 2025, and is expected to reach USD 46.37 billion by 2030, at a CAGR of 3.51% during the forecast period (2025-2030).

Italy is one of the world's leading pharmaceutical markets.

The COVID-19 pandemic is an unprecedented health concern and is adversely affecting communities, industries, businesses, and lives around the world. Many companies have already received approval for their vaccines against the Sars-CoV-2 virus and still focusing their research and development on the development of therapeutics against the COVID-19. COVID-19's immediate and direct potential impact has already led to the loss of millions of lives and a considerable increase in healthcare costs. As multiple potential medicines were tried before the development of vaccines and are used to treat the coronavirus-induced infection, other medical conditions arise due to it which is expected to complement the market. For instance, the medications such as Lopinavir/Ritonavir, hydroxychloroquine (HCQ), and Remdesivir are being repurposed to treat coronavirus infection in many countries around the world. As the country has the maximun number of production facilites, the lockdown reduced the production due to the less workforce presence which hampered the market growth of the industry.

In recent years, the Italian drug industry has expanded significantly in terms of growth, value-added, trade, and investment. With respect to research, Italy holds around 18% of the overall number of clinical trials authorized throughout the European Union. Over the years, the prevalence and incidence of many chronic and infectious diseases such as diabetes, cancer, and others, have increased many folds around the world which led to the high demand of the pharmaceutical products around the world and thus, driving the growth in the studied market.

However, In the next few years, the pharmaceutical sector in Italy may undergo a variety of obstacles. The rise in the Italian country's debt compared to GDP, and the country's underprivileged growth track may reduce the flow of money in the country, which means that the industry may falter, thus the development of the industry in the country can be hampered.

Italy Pharmaceutical Market Trends

Prescription Drugs segment Holds the Largest Share and Expected to do Same in the Forecast Period

Italy Prescription Drugs category is estimated to account for the largest share over the forecast period. The growth drivers for this sector are technology, the supportive regulatory landscape, the preference of pharmaceutical manufacturers towards Rx medicines, and new drug launches have also led to this rising trend.

Prescription drugs are available with a valid prescription from a prescriber. These drugs are heavily regulated and require a visit to a doctor, a diagnosis and monitoring by a doctor to ensure the medication is working and that it is working safely. These drugs are intended for use by one individual patient to treat a specific condition and when doctors write prescriptions, they take into consideration a lot of information about their patients, including their current condition, other medications they may be taking, their vital statistics, and drug allergies they may have. That's why a prescription medication that is safe and effective for one person may be dangerous for another. Furthermore, the increasing growth in population and rise in the chronic disease such as cardiovascular and cancer which is the leading cause of death in the country, have also contributed to the growth of this market. Moreover, along with a growth in the per-capita healthcare spending in the country, the rise in people's discretionary income is also expected to drive the market growth of the Prescription drugs segment during the forecast period from 2020-2025.

The new clinical trials, increased research and development expenditure, increased product launches, growing burden of diseases globally are the factors which are expected to drive the prescription drugs segment during the forecast period. For instance, in August 2021, Zydus Pharmaceuticals Inc, USA entered into a license and supply agreement with CHEMI SpA of Italy, a subsidiary of Italfarmaco Group, to launch the generic equivalent of Lovenox (Enoxaparin Sodium Injection) in seven dosage strengths in the United States. It is used in patients undergoing abdominal, hip or knee replacement surgery. Thus, owing to the above-mentioned factors, prescription drugs segment is expecetd to contribute significantly to the market growth.

Italy Pharmaceutical Industry Overview

The Italy pharmaceutical market is highly competitive and consists of several major players. In terms of market share, few of the major players are currently dominating the market. And some prominent players are vigorously making acquisitions and joint ventures with the other companies to consolidate their market positions in the country. Some of the Key companies which are currently dominating the market are AbbVie Inc., AstraZeneca plc, Bayer AG, C.H. Boehringer Sohn AG & Ko. KG, and GlaxoSmithKline plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising R&D Expenditure

- 4.2.2 Rising Incidence of Chronic Disease

- 4.3 Market Restraints

- 4.3.1 High Cost of Drugs

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By ATC/Therapeutic Class

- 5.1.1 Blood and Hematopoietic Organs

- 5.1.2 Cardiovascular System

- 5.1.3 Dermatological

- 5.1.4 Gastrointestinal System and Metabolism

- 5.1.5 Nervous System

- 5.1.6 Respiratory System

- 5.1.7 Others

- 5.2 By Drug Type

- 5.2.1 Branded

- 5.2.2 Generic

- 5.3 By Prescription Type

- 5.3.1 Prescription Drugs (Rx)

- 5.3.2 OTC Drugs

6 COMPETITIVE LANDSCAPE & COMPANY PROFILES

- 6.1 Company Profile

- 6.1.1 AbbVie Inc.

- 6.1.2 AstraZeneca plc

- 6.1.3 Bayer AG

- 6.1.4 C.H. Boehringer Sohn AG & Ko. KG

- 6.1.5 GlaxoSmithKline plc

- 6.1.6 F. Hoffmann-La Roche AG

- 6.1.7 Bristol Myers Squibb Company

- 6.1.8 Eli Lilly and Company

- 6.1.9 Merck & Co., Inc.

- 6.1.10 Sanofi S.A.