|

市場調査レポート

商品コード

1636507

アジア太平洋の電気自動車用電池負極:市場シェア分析、産業動向、成長予測(2025年~2030年)Asia Pacific Electric Vehicle Battery Anode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋の電気自動車用電池負極:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

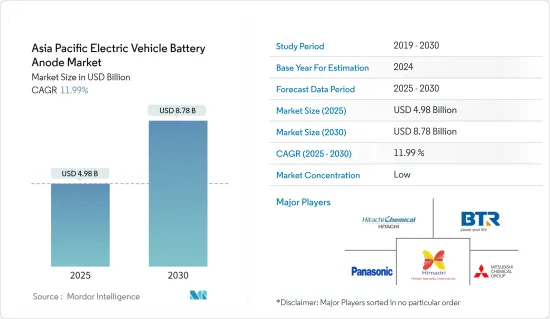

アジア太平洋の電気自動車用バッテリー負極市場規模は2025年に49億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは11.99%で、2030年には87億8,000万米ドルに達すると予測されます。

主要ハイライト

- 今後数年間、アジア太平洋の電気自動車用電池負極市場は、電気自動車の普及拡大、電池原料コストの低下(リチウムイオン電池の低価格化につながる)、政府の支援施策などの要因によって成長する見込みです。

- 逆に、原料の埋蔵量に限りがあることやサプライチェーンにおけるギャップといった課題は、市場の拡大を妨げる可能性があります。

- しかし、電池負極技術の進歩や野心的な電気自動車の長期目標は、市場参入企業に大きな機会をもたらします。

- アジア太平洋の主要参入企業の中では、インドが電気自動車用バッテリー負極市場で顕著な成長を遂げる国として際立っています。

アジア太平洋の電気自動車用バッテリー負極市場動向

リチウムイオン電池セグメントが市場を独占

- リチウムイオン電池産業の初期には、リチウム電池の主要市場は民生用電子機器製品でした。しかし、年月が経つにつれ、顕著な変化が起こった。電気自動車(EV)メーカーがリチウムイオン電池の主要消費者として台頭し、アジア太平洋におけるEV販売の急増がその原動力となりました。

- 過去10年間、アジア太平洋では、特に自動車セグメントでリチウムイオン電池の採用が急増しています。中国、インド、日本、インドネシアなどの国々では、容量対重量比が優れているため、リチウムイオン二次電池の支持が高まっています。さらに、EVに使用されるリチウム電池は、NOX、CO2、その他の温室効果ガスを排出しないため、従来の内燃機関(ICE)車に比べて環境負荷が大幅に低いです。この利点を認識し、多くの国々がEVの普及を促進し、補助金や政府のイニシアチブを通じて電気自動車用電池負極市場の開拓を促進しています。

- 2023年5月、電気自動車用電池の正極と負極市場で著名なHimadri Speciality Chemical Ltd.は、Sicona Battery Technologies Pty Ltd.に1,032万豪ドルの戦略的投資を行い、12.79%の株式を確保したと発表しました。シドニーを拠点とするシコナは、リチウムイオン(Li-ion)電池の負極(マイナス電極)に不可欠な技術を提供し、モビリティセグメントと再生可能エネルギー貯蔵の両方に貢献しています。

- 電気自動車の普及が進むにつれ、リチウムイオン電池正極市場は大幅な成長を遂げようとしています。さらに、負極技術の進歩がこの市場拡大をさらに推進することになります。

- 国際エネルギー機関(IEA)によると、中国におけるバッテリー式電気自動車の販売台数は2023年に540万台に達し、その95%以上がリチウムイオン電池技術に依存し、前年比22.7%増を記録します。このようなバッテリー電気自動車セグメントの力強い成長を考えると、リチウムイオン電池はその明確な利点により、アジア太平洋電気自動車バッテリー負極市場で大きなシェアを獲得すると予測されます。

- 2024年8月、BTR新材料グループはインドネシアでリチウムイオン電池用負極材の新工場を稼働させました。同社は、この施設が完全に拡大されれば、中国以外で最大の負極材生産拠点になるとしています。4億7,800万米ドルの投資による第1期建設は、年間8万トンの負極材生産能力を想定しています。2024年末に開始される第2段階では、2億9,900万米ドルが追加投資され、施設の生産量を多様化し、電気自動車、民生用電子機器用バッテリー、エネルギー貯蔵システム向けに負極材を供給することを目的としています。このような戦略的な動きは、アジア太平洋EVバッテリー負極市場におけるEVリチウムイオン電池の優位性の高まりを強調するものです。

- リチウムイオン電池セグメントでのこうした進歩を考えると、アジア太平洋の電気自動車用電池負極材市場は、今後数年で大きく成長することが予想されます。

アジア太平洋市場を独占するインド

- パリ協定と国連SDGsの一環として、インド政府は世界のプラットフォームで温室効果ガス排出量の削減に取り組んでいます。電気自動車(EV)の普及を促進し、インドをEV用バッテリー製造の世界の拠点と位置づけるため、政府は電気自動車用バッテリーと関連負極市場の参入企業にリベート、インセンティブ、輸入譲許を導入しました。

- 2024年3月15日、インド政府は電気自動車製造スキーム(SMEC)を承認しました。この構想は、新規のグリーンフィールド電気自動車製造工場を設立する自動車メーカーに輸入関税の譲許を与えるものです。このスキームでは、メーカーは年間8,000台までのEVを5年間15%の軽減関税で輸入することができます。この優遇措置は、認可を受けてから3年以内に国内生産能力を確立することが条件となっています。その結果、こうした開発がEV用リチウムイオン電池技術の台頭を後押しし、インドにおける負極材の成長に直接的に拍車をかけています。

- その大きな可能性と政府の強力なバックアップにより、インドは電気自動車市場を狙う企業にとって格好の製造拠点として台頭しつつあります。例えば、Epsilon Advanced Materialsは2024年9月、米国とインドにそれぞれ年産3万トンの工場を設立する計画を発表しました。これらの工場は中国以外では最大の負極材生産工場となり、インドが電気自動車用バッテリー負極材の大規模サプライヤーとしてデビューすることになります。

- 2024年9月、電池材料の主要企業であるEpsilon Advanced Materialsは、カルナータカ州にも最先端の電気自動車用電池負極材製造施設を設立する意向を明らかにしました。投資予定額は900億インドルピ(約106億米ドル)で、年間生産能力は9万トンを目指します。投資戦略は2段階で展開されます。Epsilon Groupのマネージング・ディレクターが詳述しているように、最初の投資額は400億インドルピー(約47億米ドル)、続く第2段階での追加投資額は500億インドルピー(約59億米ドル)です。

- 2024年1月、HEG Limitedの子会社でLNJ Bhilwaraグループ傘下のAdvanced Carbons Company(TACC)は、マディヤ・プラデシュ州デワス県サーソーダ村に黒鉛陽極製造装置を立ち上げました。同社は2022年、このグリーンフィールドプロジェクトに約1,850億インドルピー(約21億米ドル)を投資していました。100エーカーの敷地に広がるこの施設では、年間2万トンの陽極材を生産し、エネルギー貯蔵とモビリティの急増する需要に対応する予定です。

- 2023年、インド政府は、電気自動車(EV)用バッテリーパックの平均価格が13%大幅に下落し、前年から139米ドル/kWhまで下がったことを指摘しました。技術の進歩や製造効率の向上に伴い、バッテリーパック価格はさらに低下し、2025年には113米ドル/kWh、2030年には80米ドル/kWhまで下落すると予測されています。このような動向は、インドにおけるリチウムイオン電気自動車用電池負極市場の重要性の高まりを裏付けています。

- こうした新興国市場の開拓により、インドは今後数年間で、リチウムイオン電池負極市場において支配的な地位を確立するものと考えられます。

アジア太平洋の電気自動車用負極産業概要

アジア太平洋の電気自動車用電池負極市場は適度にセグメント化されています。市場の主要企業(順不同)には、BTR New Material Group、Himadri Speciality Chemical Ltd.、Hitachi Chemical Company Ltd、Panasonic Holdings Corporation、Epsilon Advanced Materials Pvt. Ltd.などが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 電気自動車の普及拡大

- 有利な政府施策

- リチウムイオン電池の価格低下

- 抑制要因

- サプライチェーンのギャップ

- 促進要因

- サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威製品・サービス

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 電池タイプ別

- リチウムイオン

- 鉛蓄電池

- その他

- 材料タイプ別

- シリコン

- 黒鉛

- リチウム

- その他

- 地域別

- 中国

- インド

- 日本

- マレーシア

- インドネシア

- タイ

- ベトナム

- その他のアジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BTR New Material Group Co., Ltd

- Shenzhen Dynanonic Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Hitachi Chemical Company Ltd

- Northern Graphite Corporation

- Panasonic Corporation

- Targray Technology International Inc.

- Epsilon Advanced Materials Pvt. Ltd.

- Himadri Speciality Chemical Ltd

- その他の著名な企業一覧

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 負極材における進行中の調査と進歩

The Asia Pacific Electric Vehicle Battery Anode Market size is estimated at USD 4.98 billion in 2025, and is expected to reach USD 8.78 billion by 2030, at a CAGR of 11.99% during the forecast period (2025-2030).

Key Highlights

- In the coming years, the Asia Pacific Electric Vehicle Battery Anode Market is poised for growth, driven by factors such as the rising adoption of electric vehicles, decreasing costs of battery raw materials (leading to lower prices for Li-ion batteries), and supportive government policies.

- Conversely, challenges like limited raw material reserves and gaps in the supply chain may hinder the market's expansion.

- However, advancements in battery anode technologies and ambitious long-term electric vehicle targets present significant opportunities for market players.

- Among the key players in the Asia-Pacific region, India stands out as a country poised for notable growth in the electric vehicle battery anode market.

Asia Pacific Electric Vehicle Battery Anode Market Trends

Lithium-ion Battery Segment to Dominate the Market

- In the early decades of the lithium-ion battery industry, the primary market for lithium batteries was consumer electronics. However, over the years, a notable shift took place. Electric vehicle (EV) manufacturers emerged as the leading consumers of lithium-ion batteries, driven by surging EV sales in the Asia-Pacific region.

- Over the past decade, the Asia-Pacific has seen a meteoric rise in the adoption of lithium-ion batteries, especially in the automotive sector. Countries like China, India, Japan, and Indonesia are increasingly favoring lithium-ion rechargeable batteries due to their superior capacity-to-weight ratio. Moreover, lithium batteries used in EVs do not emit NOX, CO2, or other greenhouse gases, resulting in a significantly lower environmental impact compared to traditional internal combustion engine (ICE) vehicles. Recognizing this advantage, numerous countries are promoting EV adoption and fostering the development of the Electric Vehicle Battery anode Market through subsidies and government initiatives.

- In May 2023, Himadri Speciality Chemical Ltd., a prominent player in the EV Battery Cathode and Anode market, announced a strategic investment of AUD 10.32 million in Sicona Battery Technologies Pty Ltd, securing a 12.79 percent stake. Sicona, based in Sydney, offers technology crucial for the anodes (negative electrodes) of lithium-ion (Li-ion) batteries, serving both the mobility sector and renewable energy storage.

- As electric vehicle adoption continues to rise, the lithium-ion battery cathode market is poised for substantial growth. Additionally, advancements in anode technologies are set to further propel this market expansion.

- According to the International Energy Agency (IEA), battery electric vehicle sales in China hit 5.4 million in 2023, with over 95% relying on Li-ion battery technology, marking a 22.7% increase from the previous year. Given this robust growth in the battery electric vehicle sector, lithium-ion batteries, with their distinct advantages, are projected to capture a significant share of the Asia-Pacific Electric Vehicle Battery Anode Market.

- In August 2024, BTR New Material Group inaugurated its new anode materials plant for lithium-ion batteries in Indonesia. The company claims that, once fully expanded, this facility will be the largest anode production site outside of China. The first construction phase, supported by a USD 478 million investment, is designed for an annual production capacity of 80,000 tons of anode material. A second phase, commencing at the end of 2024 with an additional USD 299 million investment, aims to diversify the facility's output, supplying anode materials for electric vehicles, appliance batteries, and energy storage systems. Such strategic moves underscore the growing dominance of EV Li-ion batteries in the Asia-Pacific EV Battery Anode Market.

- Given these advancements in the lithium-ion battery sector, the market for anode materials in the Asia-Pacific region's electric vehicle battery market is set for significant growth in the coming years.

India to Dominate the Market in Asia Pacific

- As part of the Paris Agreement and the United Nations SDGs, the Government of India has committed to reducing GHG emissions on global platforms. To bolster the adoption of Electric Vehicles (EVs) and position India as a global hub for EV battery manufacturing, the government has introduced rebates, incentives, and import concessions for players in the electric vehicle batteries and associated anode markets.

- On March 15, 2024, the Indian government approved the Scheme for Manufacturing of Electric Cars (SMEC). This initiative offers concessional import duties to automakers establishing new greenfield electric vehicle manufacturing plants. Under the scheme, manufacturers can import up to 8,000 EVs annually at a reduced duty of 15% for five years. This concession is granted on the condition that they establish domestic production capabilities within three years of receiving approval. Consequently, these developments are bolstering the rise of Li-ion battery technology for EVs, directly fueling the growth of anode materials in India.

- Given its vast potential and robust government backing, India is emerging as a prime manufacturing hub for companies eyeing the electric vehicle market. For instance, in September 2024, Epsilon Advanced Materials announced plans to set up two plants, each boasting a capacity of 30,000 tonnes per annum-one in the United States and the other in India. These facilities are poised to be the largest producers of anode material outside of China, marking India's debut as a large-scale supplier of electric vehicle battery anode material.

- In September 2024, Epsilon Advanced Materials, a key player in battery materials, disclosed its intent to set up another cutting-edge EV battery anode material manufacturing unit in Karnataka. With a projected investment of INR 9,000 crore (~USD 10.6 billion), the facility targets an annual production capacity of 90,000 tonnes. The investment strategy unfolds in two phases: an initial INR 4,000 crore (~USD 4.7 billion) infusion, followed by an additional INR 5,000 crore (~USD 5.9 billion) in the second phase, as detailed by Epsilon Group's Managing Director.

- In January 2024, the Advanced Carbons Company (TACC), a HEG Limited subsidiary and part of the LNJ Bhilwara group, launched its graphite anode manufacturing unit in Sirsoda village, Dewas district, Madhya Pradesh. The company had earmarked approximately INR 1850 crores (~USD 2.1 billion) for this greenfield project back in 2022. Spread over 100 acres, the facility is poised to churn out 20,000 metric tonnes of anode material annually, meeting the surging demands of energy storage and mobility.

- In 2023, the Government of India noted a significant 13% drop in average battery pack prices for electric vehicles (EVs), bringing them down to USD 139/kWh from the previous year. With ongoing technological advancements and enhanced manufacturing efficiencies, projections indicate a further decline in battery pack prices, forecasting USD 113/kWh by 2025 and an ambitious drop to USD 80/kWh by 2030. Such trends underscore the growing significance of the Lithium-ion Electric Vehicle Battery Anode Market in India.

- Given these developments, India is poised to emerge as a dominant player in the studied market in the coming years.

Asia Pacific Electric Vehicle Battery Anode Industry Overview

The Asia Pacific Electric Vehicle Battery Anode Market is moderately fragmented. Some of the major players in the market (in no particular order) include BTR New Material Group Co., Ltd., Himadri Speciality Chemical Ltd., Hitachi Chemical Company Ltd, Panasonic Holdings Corporation, and Epsilon Advanced Materials Pvt. Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Growing Adoption of Electric Vehicles

- 4.5.1.2 Favorable Government Policies

- 4.5.1.3 Decreasing Price of Lithium-ion Batteries

- 4.5.2 Restraints

- 4.5.2.1 The Supply Chain Gap

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Battery type

- 5.1.1 Lithium-ion

- 5.1.2 Lead-acid

- 5.1.3 Other Technologies

- 5.2 By Material Type

- 5.2.1 Silicon

- 5.2.2 Graphite

- 5.2.3 Lithium

- 5.2.4 Other Materials

- 5.3 Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 Malaysia

- 5.3.5 Indonesia

- 5.3.6 Thailand

- 5.3.7 Vietnam

- 5.3.8 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BTR New Material Group Co., Ltd

- 6.3.2 Shenzhen Dynanonic Co., Ltd.

- 6.3.3 Mitsubishi Chemical Group Corporation

- 6.3.4 Hitachi Chemical Company Ltd

- 6.3.5 Northern Graphite Corporation

- 6.3.6 Panasonic Corporation

- 6.3.7 Targray Technology International Inc.

- 6.3.8 Epsilon Advanced Materials Pvt. Ltd.

- 6.3.9 Himadri Speciality Chemical Ltd

- 6.4 List of Other Prominent Companies

- 6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ongoing Research and Advancement in Anode Material